Davos: business leaders less optimistic than a year ago

The plunging oil price has knocked the confidence of business leaders in Russia and other energy producing nations, according to a survey of top bosses published on Tuesday to coincide with the start of the Davos meeting of the World Economic Forum. Larry Elliott and Jill Treanor write from Davos:

The survey found that company bosses are less optimistic than they were a year ago.

Last year 44% of chief executives surveyed by accountants PricewaterhouseCoopers thought global growth would improve but that has fallen to 37% for 2015.

Dennis Nally, chairman of PwC said: “CEO confidence is down notably in oil-producing nations around the world as a result of plummeting crude oil prices. Russia CEOs, for example, were the most confident in last year’s survey, but are the least confident this year. Confidence also slipped among CEOs in the Middle East, Venezuela, and Nigeria.”

More than twice as many of the company bosses as last year thought global economic growth will decline. The survey was conduced after a year in which Chinese growth had slowed and the eurozone stagnated, raising expectations that Mario Draghi, head of the European Central Bank, will try to bolster the eurozone by launching a quantitative easing programme on Thursday.

Bosses surveyed in the UK are more optimistic than their EU counterparts, more than 60% of UK CEOs believing there are more growth opportunities for their company today than three years ago - more than any of their European peers. But Ian Powell, UK chairman and senior partner at PwC, said that “the high levels of optimism we saw last year have been tempered by concerns about access to key skills, disruptive trends and geopolitical uncertainty”.

The full story is here:

Davos 2015: sliding oil makes chief executives less upbeat than last year

On that note it’s time to shut up shop for the evening. The team in Davos will re-open the blog in the case of any major events, but otherwise we’ll be back tomorrow as usual. Thanks for all your comments, and see you soon.

Updated

European markets lifted by China and QE hopes

Despite the IMF cutting its global forecasts, shares moved higher again as Chinese GDP came in better than expected, albeit at 7.4%, lower than the government’s 7.5% target. And of course, investors are still betting on quantitative easing from the European Central Bank on Thursday. Even an opening fall on Wall Street, hit by declines in energy shares as oil dipped again and disappointing results from Morgan Stanley and Johnson & Johnson, failed to dampen the mood. The final scores showed:

- The FTSE 100 finished up 34.57 points or 0.52% at 6620.10

- Germany’s Dax rose 0.14% to 10,257.13

- France’s Cac closed up 1.16% at 4446.02

- Italy’s FTSE MIB added 0.91% to 19,658.66

- Spain’s Ibex ended 1.24% higher at 10,283.9

On Wall Street, the Dow Jones Industrial Average is currently down 120 points or 0.7%.

My colleague Graeme Wearden has arrived in Davos and here are some early snapshots:

US housebuilder sentiment dipped slightly in January but still remains strong, according to the latest industry survey.

The NAHB/Wells Fargo Housing Market index fell to 57 from 58 in December (itself revised up from 57). Analysts had been expecting a reading of 58. But the index has not been below 50 since June last year, and NAHB chairman Kevin Kelly said:

After seven months above the key 50 benchmark, builder sentiment is reflecting the gradual improvement that is occurring in many markets throughout the nation.

Following Monday’s market closure for Martin Luther King day, investors are taking some profits in early trading.

The Dow Jones Industrial Average is currently down 59 points or 0.33%, although it has recovered from larger falls earlier after the housebuilding figures.

Energy shares came under pressure as oil slipped again in the wake of the IMF’s cut in its global growth forecasts.

Update from the Bank for International Settlements: lending to Russia by overseas banks fell by $11bn in the third quarter of 2014.

That was contrary to the broader trend, with cross-border lending overall up by $493bn, boosting the annual growth rate to 5% from 1% in the second quarter. The increase was concentrated in Japanese yen and US dollars, BIS said.

The TUC has a few frank words for the global thinkers gathering in Davos for the World Economic Forum this week.

The message is that the delegate list should be more representative of the issues being discussed, and not just an elite talking shop.

Frances O’Grady, general secretary, gets the point across:

Just one per cent of the global population owns half the world’s wealth, so we need some voices at Davos to speak up for the other 99 per cent. That’s why I’m here as part of a delegation of international trade union leaders.

If Davos is a closed shop for the wealthy and powerful elites who caused today’s global inequality, it won’t come up with the answers needed for a more fair and prosperous future for all the world’s workers and their families.

We need to get living wages and the protection of public services onto the agenda. And we need the business leaders attending to commit to cleaning up supply chains, paying their taxes and investing in decent jobs instead of the casino capitalism that caused the crash.

The scale and nature of the European Central Bank’s hotly anticipated foray into quantitative easing on Thursday continues to occupy economists’ minds.

Franck Dixmier of Allianz Global Investors says action needs to be bold.

The stakes are extremely high in the run-up to the ECB’s QE announcement on Thursday and [ECB President] Mario Draghi would do well to adopt a bold, yet simple plan of attack to stave off a prolonged period of deflation and boost economic prospects in the Eurozone.

As the ECB finalizes plans for firing the last major weapon in its monetary policy arsenal, markets are hoping for a QE programme of at least EUR 500 billion and anything less will be perceived as a huge disappointment.

Eligible assets will certainly include government bonds, but the addition of corporate investment grade securities would be a welcome surprise for investors, which is not currently priced into the market.

The worst mistake the ECB could make, in my view, would be to attach too many conditions and caveats to pacify the QE sceptics. Such an approach would make QE difficult to execute and obscure its full implications and consequences for investors.

Larry Elliott, the Guardian’s economics editor, asks whether it will be a case of “too little too late”, here. A taster below:

For Mario Draghi, Thursday is the day the talking stops. It is two and a half years since the president of the European Central Bank said he would do “whatever it takes” to safeguard the future of the euro. Financial markets now want him to deliver on his pledge.

All the hurdles - economic, political and legal - have allegedly been cleared. The ECB will announce a programme of sovereign bond purchases, its equivalent of the quantitative easing programmes that were announced by the US Federal Reserve and the Bank of England six years ago.

Having ramped up expectations, there is now a danger that the long-awaited plan proves a damp squib. Markets want Draghi to put a figure on the size of his programme (preferably at least €1 trillion) and they want to know exactly how it will be operated. Given the length of time that has elapsed since Draghi’s “whatever it takes” speech, they will be unhappy with anything less.

Copper is trading higher after China’s growth figures were not as weak as many analysts had feared.

The world’s second largest economy grew by 7.4% in 2014, the weakest since 1990 and a touch below the government’s official 7.5% forecast but not as low as the 7.2% growth predicted in a Reuters poll.

Copper is considered a barometer for global economic demand and is closely linked to developments in China - its largest consumer.

Three-month copper on the London Metal Exchange was trading up 1% at $5,735 a tonne. Last week copper prices hit a five-and-a-half year low on the back of global growth fears.

Updated

The business blog’s very own Graeme Wearden is in Switzerland and is making his way to Davos.

Ok, is this the right way up? https://t.co/CDzPVNu9ui

— Graeme Wearden (@graemewearden) January 20, 2015

Other modes of transport are available:

A participant arrives by private helicopter for the #WEF15. LIVE coverage out of #Davos: http://t.co/pf3BsK2WcE pic.twitter.com/TAnxrv29c3

— Reuters Davos (@Reuters_Davos) January 20, 2015

The UK will remain in the European Union, analysts and traders are convinced.

Of the 500 people surveyed for Bloomberg’s quarterly global poll, 71% believe the UK will be part of the EU for the foreseeable future.

A further 15% expect the UK to break away within five years, and another 8% said the UK would exit within a decade.

The Conservatives have promised a referendum on UK membership of the EU by the end of 2017 should they win the general election in May, increasing the chances of an exit.

Back with George Osborne and his appearance at the Treasury committee:

Osborne says budget will contain further tax cuts for oil and gas industry - http://t.co/Es6vlFPJhy

— AndrewSparrow (@AndrewSparrow) January 20, 2015

Updated

Morgan Stanley is the latest big US bank to report results, and they have come in below expectations, with fourth quarter revenues of $7.8bn and earnings per share of $0.47.

$MS miss on both their EPS and revenue, trading lower by 3% ahead of the Wall Street open

— RANsquawk (@RANsquawk) January 20, 2015

Morgan Stanley is the latest US bank to report below-forecast earnings numbers. Last week results from BoA, Citi and JPM all disappointed^FR

— FOREX.com (@FOREXcom) January 20, 2015

Meanwhile chancellor George Osborne is currently being quizzed by the Treasury committee about more tax powers for Scotland.

My colleague Andrew Sparrow is live blogging the sesssion here.

In China-related news, Unilever has warned this morning that it does not expect market conditions to improve in 2015 because of a downturn in emerging markets and weakness in Europe.

The consumer goods giant behind Marmite, Ben & Jerry’s ice-cream and Persil washing powder, said sales were down 20% in China in the fourth quarter, as retailers ran down their stocks of personal care products.

Overall, underlying sales rose 2.1% in the fourth quarter, disappointing City expectations of a 2.6% rise. Unilever shares are down 1.2% at £26.97.

Paul Polman, Unilever’s chief executive:

We do not plan on a significant improvement in market conditions in 2015. Against this background, we expect our full-year performance to be similar to 2014 with the first quarter being softer but growth improving during the year.

Updated

Some more reaction to the IMF’s revised growth forecasts now, specifically on the UK.

The shadow chancellor Ed Balls has (unsurprisingly) taken a different view on the forecasts to George Osborne, who was overwhelmingly positive this morning.

Balls says:

It’s worrying that the IMF has downgraded its forecasts for the UK economy for last year and next year too. In contrast the IMF says the US will grow faster than us this year and next year and has seen its growth forecasts upgraded.

This shows why the complacency of David Cameron and George Osborne is so misplaced. Claims that the economy is fixed will ring hollow to millions of working people who are on average £1,600 a year worse off under this government.

We need stronger and more balanced growth that delivers sustained rises in living standards for all, not just a few. That’s what Labour’s economic plan is all about.

Meanwhile Danny Alexander, the Liberal Democrat chief secretary to the Treasury, had this to say on the forecasts:

Today’s forecast update from the IMF confirms expectations that the UK economy has grown faster than any other G7 country in 2014. It is also encouraging that along with the US we are one of only two G7 countries not to have seen our growth downgraded in 2015.

However while this marks real progress we need to continue sticking to our plan to build the stronger economy and fairer society that we aspire to.

Updated

Scottish Power’s move to cut prices follows the decision by British Gas on Monday to cut prices by 5%, with effect from 27 February.

Last week E.ON announced it was immediately cutting prices by 3.5%.

Scottish Power - owned by the Spanish utility company Iberdrola - said its average annual gas bill on a standard tariff would fall £33.

In a statement, Neil Clitheroe, Scottish Power’s head of retail and generation, said:

Today’s decision has been made to benefit our customers and keep our prices competitive. We will continue to keep our prices under review. Our pricing reflects all of the costs that contribute to a customer’s bill.

The wholesale price of energy accounts for half of a customer’s gas bill, but non-energy costs such as transmission and distribution networks and environmental and social obligations remain unaffected by any wholesale energy price movements.

On Monday, Ed Miliband described the 5% cut in gas prices by British Gas as “too little, too late”. His argument is that energy companies are not passing on enough of the 20% fall in wholesale gas prices.

Energy companies counter the argument by saying bills are made up of various costs, and are not simply determined by wholesale prices.

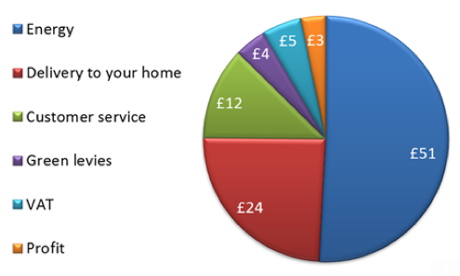

To demonstrate the point, Scottish Power has published a bar chart. For every £100 spent by a gas customer, the typical breakdown of costs is shown below.

Updated

Scottish Power cuts gas prices

Breaking: Scottish Power has become the latest energy company to cut its household gas prices. Prices will be cut 4.8% from 20 February. More soon.

As speculation about the outcome of Sunday’s Greek election mounts, read the Guardian’s datablog here for the latest facts and figures.

The big fear among financial markets is that a victory for the radical left and anti-austerity party Syriza - currently ahead in the polls - will ultimately lead to a Greek exit from the eurozone.

Greece Election 2015: the politics and economics in numbers http://t.co/VU7Y9biqJQ #ekloges2015

— Alberto Nardelli (@AlbertoNardelli) January 20, 2015

German confidence surges

Confidence among Germany’s analysts and investors jumped to an 11-month high in January, beating expectations.

Low oil prices, a weak euro, and expectations that the ECB will announce quantitative easing on Thursday, boosted hopes that Europe’s biggest economy will rebound after weakening in the second half of last year.

The closely-watched ZEW survey of economic sentiment rose for a third month to 48.4 in January from 34.9 in December. It was the highest since February last year and beat economists’ forecasts of a smaller increase to 40.

Jennifer McKeown, a senior European economist at Capital Economics, said it was a sign that confidence was holding up well in Germany despite uncertainty over the Greece.

Presumably any worries about the effect of the Greek crisis on the German economy were offset by expectations of ECB quantitative easing and hopes of a boost to exports from the weakening euro.

This may suggest that German GDP growth, which stalled around the middle of 2014 and seems likely to have been very weak in Q4, will pick back up this year.

But note that the ZEW survey has not been a particularly reliable indicator of actual activity in the past and if the Greek situation deteriorates in the aftermath of this week’s election or ECB QE disappoints, investors may well take a dimmer view of Germany’s prospects.

For now, we expect German GDP to expand by a steady but unspectacular 1% this year and 1.5% next, which will do little to reduce the risk of a long bout of deflation in the euro-zone as a whole.

Consumer goods group Reckitt Benckiser has received a slap on the wrist from the Financial Conduct Authority in the form of a £539,800 fine over share dealing by its senior executives.

The FCA said its disclosure to the market of share dealing by two senior executives was late and incomplete as a result of inadequate monitoring.

When the company became aware of the share deals, it should have informed the market by the end of the next business day but it failed to do so.

Ukraine is confident that there will be a positive outcome from negotiations with the IMF over further financial aid, Reuters is reporting.

Ukraine has been pushed to the financial brink as a result of the pro-Russian separatist war in the east and is facing huge debt repayments. It has asked the IMF to extend an existing programme to plug a $15bn (£9.9bn) funding gap.

The existing package is worth $17bn and has so far paid out $4.6bn in two tranches.

The IMF team arrived in Kiev on 8 January for the latest round of talks which are expected to last until the end of the month. The Fund has said any additional money will depend on Kiev’s ability to deliver long-promised reforms.

Reuters is quoting Oleksander Pisaruk, the first deputy head of Ukraine’s central bank.

The talks are constructive. Co-operation with the IMF is fruitful. I feel optimism about the possible outcome.

Demand rises for eurozone bank loans

The European Central Bank has reported a rise in companies seeking a bank loan in the fourth quarter. Demand is also expected to rise in the first three months of 2015.

In its latest quarterly survey of bank loans, the ECB said that a quarter of banks surveyed saw an increased in demand for home loans in the final quarter of 2014, with a fifth expecting another increase this quarter.

A few extracts from the report:

The heterogeneity across countries continued to reduce somewhat, with banks in Germany, France, the Netherlands and particularly in Spain reporting an increase in demand for loans to enterprises and Italian banks indicating unchanged demand.

For housing loans, net loan demand was particularly positive in the Netherlands, Italy and Germany and to a lesser extent in Spain, while remaining unchanged in France down from a strong increase in the previous quarter.

Brent crude oil prices were down on Tuesday morning, trading at just above $48 a barrel.

Nariman Behravesh, the chief economist of data provider IHS, says plunging oil prices will transfer roughly $1.5 trillion (£990bn) in wealth from producers of oil to consumers of it.

The Davos delegate says this will mean an additional 0.3 to 0.5 percentage points for world growth.

Everyone right now is talking about the impact of the oil price plunge. While clear winners and losers are being created, the net effect will be positive as roughly $1.5 trillion in wealth is transferred from producers of oil to consumers of it. This will translate to an additional 0.3 to 0.5 percentage point to world growth.

As a point of reference, the 67% drop in oil prices in 1985 and 1986 was followed by a boom. While three decades later the global environment is different, and a boom may not be in the offing, the big drop in oil prices will help growth.

Despite multiple divergent trends, global growth is likely to accelerate a little in 2015. Falling oil prices and more stimuli from key central banks will boost global growth in 2015 to 3% from 2.7 percent in 2014

It’s that time of year again when world leaders and the big names in business and economics put their heads together in the Swiss mountains to debate pressing issues of global significance.

Many of the delegates are currently making their way to Davos, before the event officially opens later today.

Here is a reminder of what is likely to be on the agenda.

Guardian reporters will be bringing you all the news from Davos over the coming week. Follow @jilltreanor and @graemewearden for updates.

On the Davos agenda: from Al Gore on global warming to fears over eurozone http://t.co/bhmtuw6dB1

— Jill Treanor (@jilltreanor) January 20, 2015

European markets open higher

European investors have shrugged off the IMF’s weaker global outlook this morning, with all major indices trading higher.

The news from China that growth was the slowest in 24 years in 2014 was not exactly positive, but markets are signalling relief: it could have been worse.

- FTSE 100: +0.4% at 6,609.63

- Germany’s DAX: +0.2 at 10,265.18

- France’s CAC: +0.5 at 4,415.51

- Spain’s IBEX: +0.5 at 10,211.4

- Italy’s FTSE MIB: +0.5 at 19,586.22

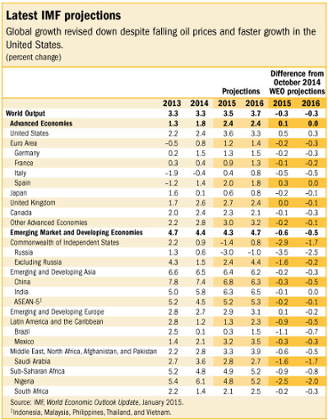

Here is a table of the IMF’s latest projections.

Back on the IMF, the outlook for the UK was unchanged for 2015, with growth of 2.7% forecast. It nudged down the forecast for 2016 to 2.4% from 2.5%.

The Washington-based Fund believes official figures will soon confirm that the UK was the fastest growing G7 economy last year with growth of 2.6%. (The Office for National Statistics will publish its first estimate of fourth-quarter and full-year growth on 27 January.)

The Chancellor George Osborne has given his verdict on the forecasts:

Today’s IMF forecast shows that Britain is pulling ahead, while the global economy is being downgraded. There’s confirmation that we grew faster than any other major economy last year, and we’re set to grow faster this year*.

But there are risks out there in the global economy and it’s a timely reminder that we’ve got to go on working through our long term economic plan if we want to stay ahead.

*It’s worth pointing out here that UK growth is forecast to accelerate to 2.7% this year from 2.6% last year. But US growth is expected to outpace the UK this year at 3.6%.

IMF forecast shows that Britain is pulling ahead while the global economy is downgraded. Fastest in G7 in 2014 and growing faster in 2015

— George Osborne (@George_Osborne) January 20, 2015

Updated

Good morning, and welcome to our rolling coverage of the financial markets, the world economy, business and finance.

The International Monetary Fund has become the latest heavyweight forecaster to downgrade its outlook for the global economy.

In an update to coincide with the World Economic Forum meeting in Davos - which kicks off later today in the Swiss ski resort - the IMF predicted global growth would be 3.5% this year, and not 3.8% as previously expected.

The Fund’s growth forecasts for 2016 were also cut to 3.7% from 4%.

It blamed the looming recession in Russia and slowdown in China for the gloomier outlook, warning the negative effects would outweigh the boost from lower oil prices. Read our full story here.

Meanwhile China confirmed overnight what everyone feared - the economy grew at the slowest rate since 1990 in 2014.

Growth of 7.4% was below the government’s 7.5% target - the first time the official target has been missed for 16 years.

We’ll be tracking all the main events through the day....

.jpg?w=600)