Forget Bitcoin, high-speed memory is the new digital gold, and companies that supply data storage have seen their stock prices explode this year.

Memory has become a crucial bottleneck as AI training programs produce massive amounts of data, and memory companies like Micron Technology Inc. (NASDAQ: MU) can’t keep up with their insatiable demand.

But memory storage has a finite supply, and hyperscalers are siphoning that supply from companies accustomed to a cyclical business.

Video game companies re one group that have suddenly found themselves as have-nots, especially those that manufacture memory-needy gaming consoles, which sit in the crosshairs of one of the biggest trends in the tech sector.

DRAM and NAND memory, key components in gaming console construction, have doubled since last year, and the major suppliers are reporting capacity shortages into 2028. High-performance memory is a must for next-gen consoles, and it can’t be engineered out of the bill of materials.

The following three companies are directly or indirectly affected by the memory shortage. And considering how much capex hyperscalers are committing, investors may want to avoid these names until the memory shortage abates.

Nintendo: New Hardware Launching Directly Into the Shortage

Nintendo Co. Ltd. (OTCMKTS: NTDOY) is most exposed to memory shortages as it lacks diversification beyond the console market and has a new device early in its lifecycle.

The Switch 2 was released in June last year at $449, making it the most expensive console the company had ever released.

CEO Doug Bowser (yes, Bowser runs Nintendo) defended the price point, citing the console’s premium features and high demand.

But now the console is facing unexpected headwinds due to higher memory costs, forcing management to announce a Sept. 1 price hike to $499.

The timing of the price hike couldn’t be worse. Nintendo’s margins were already under pressure from tariffs, and now the company is forced to increase prices on its already expensive next-gen console just 15 months after launch.

Nintendo’s typical console launch strategy involves promotions and discounts to build a customer base, and then selling high-margin software to that wide base. But the company is projecting Switch sales to drop 17% year-over-year (YOY) from fiscal 2026 to 2027, with overall net sales declining 11% and net profits declining 27%. With margins already under pressure, Nintendo has no choice but to pass on expanding costs to customers.

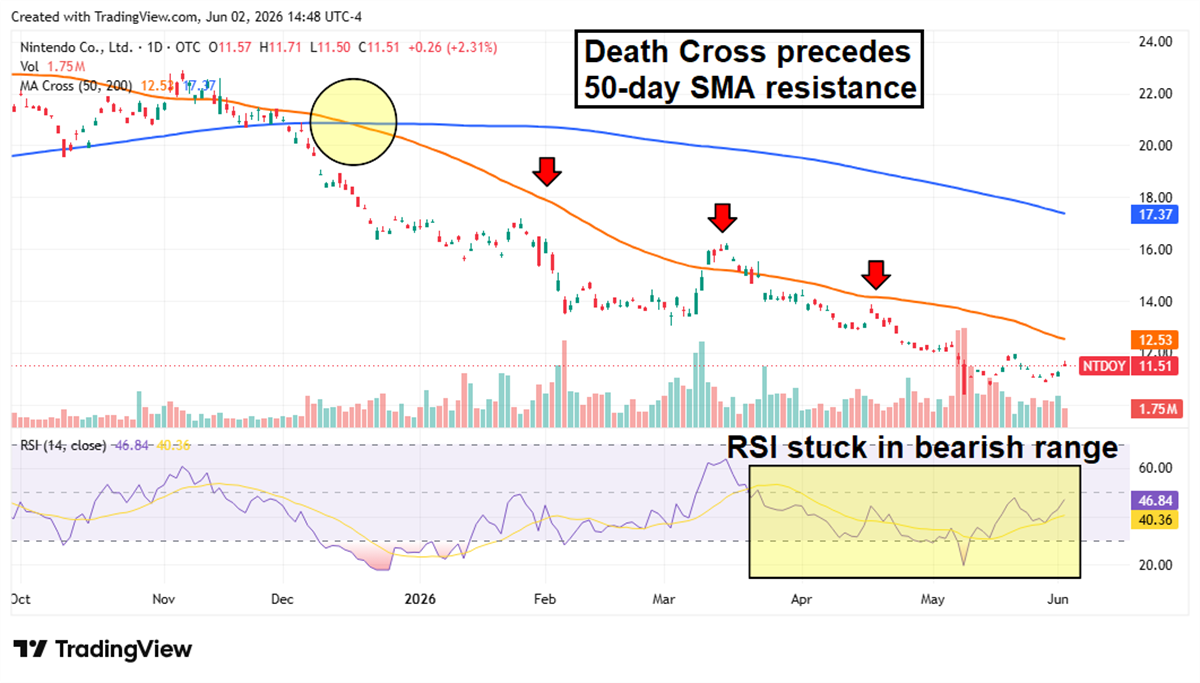

NTDOY shares have been in a steady downtrend since the start of the year, highlighted by December’s Death Cross that reinforced resistance at the 50-day moving average. All attempted breakouts have been thwarted, and the Relative Strength Index (RSI) remains trapped in a bearish cycle.

Sony: Gaming Segment Margins Getting Tougher to Defend

Sony Group Corp. (NYSE: SONY) is far more diversified than Nintendo thanks to its music, movies, and financial services platforms.

But the gaming segment is typically a profit machine, and Sony is feeling the heat after two price increases: one for the PlayStation 5 family of consoles and another for new PlayStation Plus subscribers.

Like Nintendo, PlayStation consoles are a lower-margin product that drives recurring high-margin software and subscription sales.

And while the PS5 is an aging product, the memory shortage is forcing management to consider delaying the PlayStation 6 release.

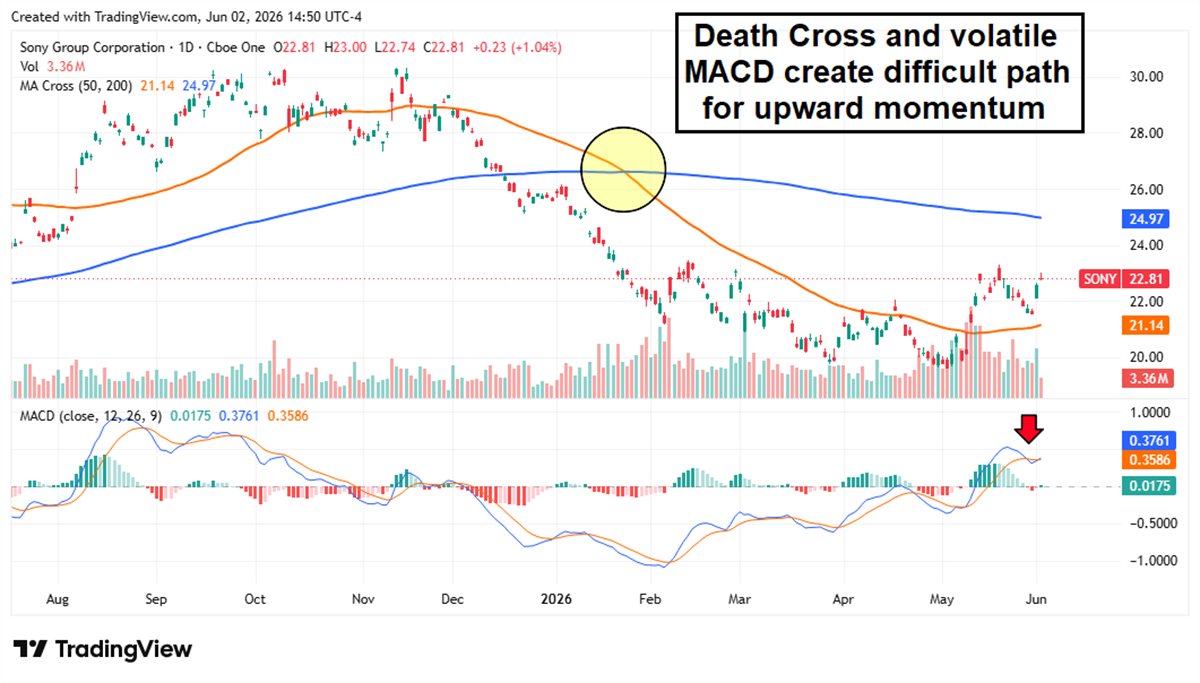

Sony stock shows some signs of a revival, but the long-term technical trend remains murky. The Moving Average Convergence Divergence (MACD) indicator is volatile but trending up, and the share price recently overtook the 50-day moving average. However, January’s Death Cross still looms large, and the MACD looks to be forming a new bearish crossover that could see the share price re-challenge the 50-day MA.

Take-Two Interactive: Exploding Memory Prices Indirectly Influencing Company’s Biggest Launch

Take-Two Interactive Software Inc. (NASDAQ: TTWO doesn’t purchase any memory, and its products face minimal margin compression from sky-high memory prices.

Instead, Take-Two Interactive is the largest publicly traded game developer, responsible for popular titles like Grand Theft Auto and Red Dead Redemption.

This year, the company is pushing all in with Grand Theft Auto 6, a long-awaited sequel that’s finally out of Development Hell.

Take-Two is planning a Nov. 19 release for GTA6 on PlayStation and Xbox consoles.

But if price hikes continue to push consoles out of reach for consumers, the launch could be softer than anticipated.

The company projects fiscal 2027 revenue between $7.9 billion and $8.1 billion, with nearly all of it expected to come from GTA6 sales. Any misfire on this launch could be bad news for a stock that already trades at 34x forward earnings and 6x sales.

Following a Death Cross and massive drawdown earlier this year, the stock has actually rebounded nearly 15% since the end of March. But the rebound appears headed for rejection as the price has failed to sustain a breakout above the 200-day moving average. The RSI has also dipped into bearish territory, and the stock now needs to defend the 50-day MA or risk a further decline.

The article "How the Memory Shortage Is Crushing the Gaming Industry" first appeared on MarketBeat.