The UK housing market could see a credit boom like that of the early 2000s and see annual prices increase by almost 7% if interest rates are kept on hold in 2016, one of the world’s biggest banks has warned.

Researchers at BNP Paribas said that while the deferral of a rate rise until 2017 might seem like good news for homeowners, it could lead to higher prices and force the Bank of England to act to restrict mortgage lending.

The bank said it expected house prices in the UK to rise by 4.4% in 2016 if the base rate started to rise slowly from its current level of 0.5%, and that this would be followed by a 6.7% rise in 2017.

This level of growth would see the average house price, as measured on Nationwide’s monthly index, rise from £197,582 in December 2015 to £206,256 by the end of 2016, and £220,116 a year later.

BNP Paribas said that improved household finances and confidence in the economy would bolster demand for homes, and prices paid, but the lack of supply of property for sale remained “a serious concern”.

If the base rate rise is delayed, the bank said prices could rise by 6.9% in 2016 and by 11.5% in 2017, increasing prices to £211,215 then £235,500 respectively.

Adrian Owen, head of residential at BNP Paribas Real Estate, said: “While on the face of it a deferral would be good news for homeowners, we believe this scenario is a cautionary tale for the UK economy as a whole.

“There is already concern at the Bank of England over the pace of house price growth, and while the current lack of housing supply is a significant driver, the sustained low cost of finance is also a major contributor.”

Mortgage rates have fallen to record lows this year, with the average rate on a two-year fixed-rate mortgage at 75% of a property’s value now at just 1.87%, and the average five-year deal at 2.78%.

In some areas of the country house prices are now at a higher multiple of earnings than ever before, although intervention by the Bank of England in 2014 has reduced the amount of lending that is being done at more than four-and-a-half times an applicant’s salary.

The Bank of England’s governor, Mark Carney, has indicated that rates could stay on hold until well into 2016 and that other measures may be needed to cool the market.

Owen said: “Even under our central scenario that base rates rise next year, it is likely that the Bank of England will seek to place a brake on house price growth by introducing further restrictions on the availability of finance.

“This may achieve the desired dampening effect, although does not address the underlying structural issue in the market of insufficient supply.”

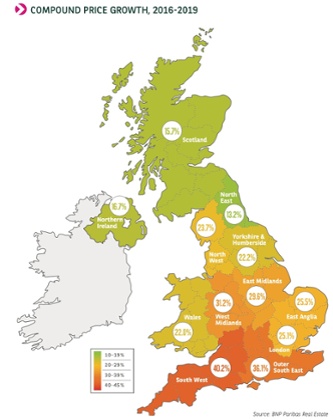

The researchers predict that across the UK house prices will increase by almost 27% by the end of 2019. In the south-west of England they said prices could grow by 40.2% by 2020, while in the south-east (excluding London) the increase could be 36.1%. In London prices are expected to grow by 25.1% over the period.

George Osborne’s announcement that buyers of any kind of second property will face a 3% stamp duty surcharge has been factored into the forecasts. The researchers found the move would have little national impact, but would dampen house price growth in regional town centres and in London. They said that as a result they had reduced expectations for price rises in London in 2016 from 5.6% to 4.7%.

As a result, their forecast for the average price of a London home in 12 months time has been cut by £5,000 to £468,893.