WEC Energy Group, Inc. (WEC), headquartered in Milwaukee, Wisconsin, provides regulated natural gas and electricity services, as well as nonregulated renewable energy services. Valued at $37.5 billion by market cap, the company’s infrastructure spans 35,500 miles of overhead and 36,500 miles of underground distribution lines, with extensive gas mains, transmission lines, and storage capacity. The leading energy company is expected to announce its fiscal third-quarter earnings for 2025 before the market opens on Thursday, Oct. 30.

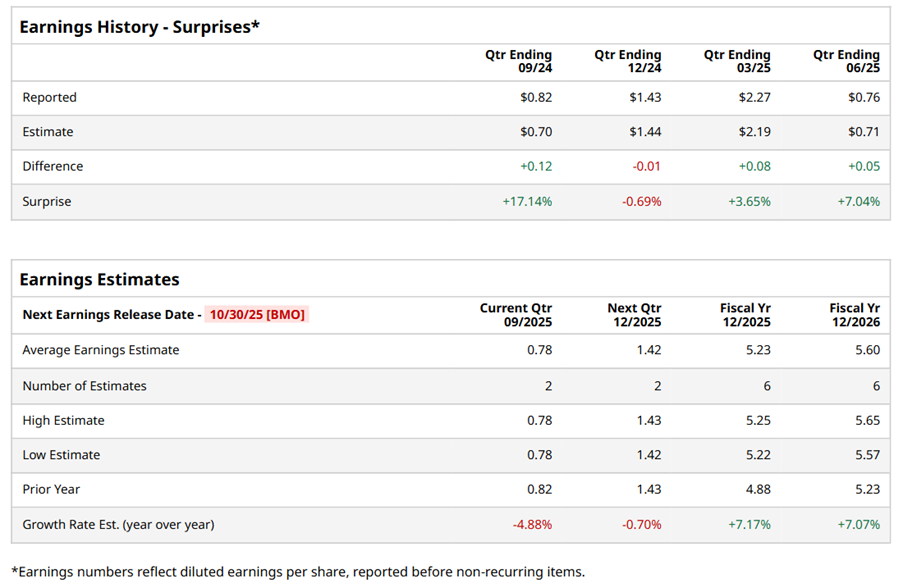

Ahead of the event, analysts expect WEC to report a profit of $0.78 per share on a diluted basis, down 4.9% from $0.82 per share in the year-ago quarter. The company beat the consensus estimates in three of the last four quarters while missing the forecast on another occasion.

For the full year, analysts expect WEC to report EPS of $5.23, up 7.2% from $4.88 in fiscal 2024. Its EPS is expected to rise 7.1% year over year to $5.60 in fiscal 2026.

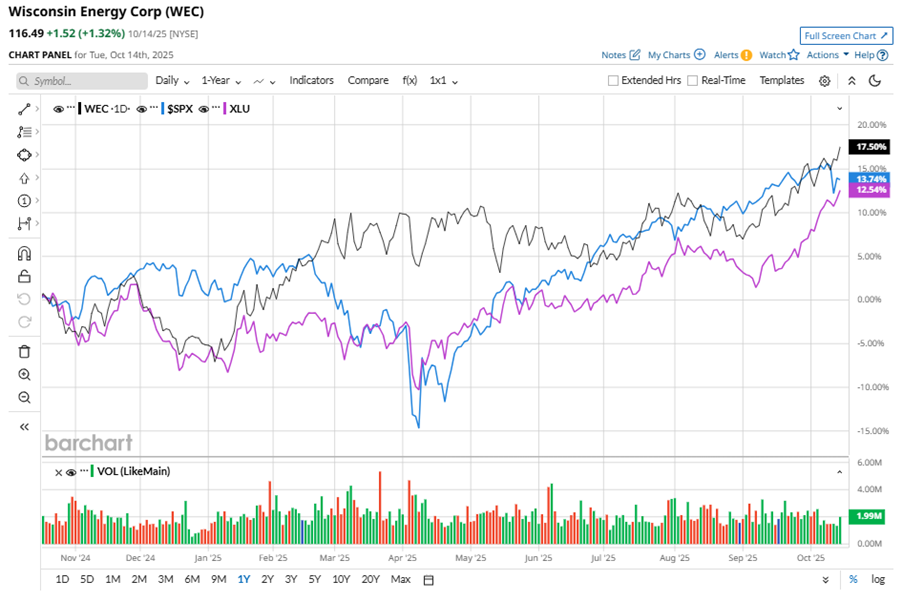

WEC stock has outperformed the S&P 500 Index’s ($SPX) 13.4% gains over the past 52 weeks, with shares up 21% during this period. Similarly, it outperformed the Utilities Select Sector SPDR Fund’s (XLU)14.3% gains over the same time frame.

WEC's strong performance likely stems from increased infrastructure spending and rising electricity prices.

On Jul. 30, WEC shares closed down marginally after reporting its Q2 results. Its EPS of $0.76 beat Wall Street expectations of $0.71. The company’s revenue stood at $2 billion, up 13.4% year over year. WEC expects full-year EPS to be between $5.17 and $5.27.

Analysts’ consensus opinion on WEC stock is reasonably bullish, with a “Moderate Buy” rating overall. Out of 15 analysts covering the stock, five advise a “Strong Buy” rating, nine give a “Hold,” and one recommends a “Strong Sell.” While WEC currently trades above its mean price target of $114.38, the Street-high price target of $131 suggests an upside potential of 12.5%.