Paychex, Inc. (PAYX), headquartered in Rochester, New York, offers integrated human capital management solutions (HCM) that encompass payroll, benefits, human resources (HR), and insurance services for small to medium-sized businesses. With a market cap of $46.1 billion, the company's services range from calculating payroll and filing tax payments to administering retirement plans and workers' compensation. The industry-leading HCM company is expected to announce its fiscal first-quarter earnings for 2026 before the market opens on Tuesday, Sep. 30.

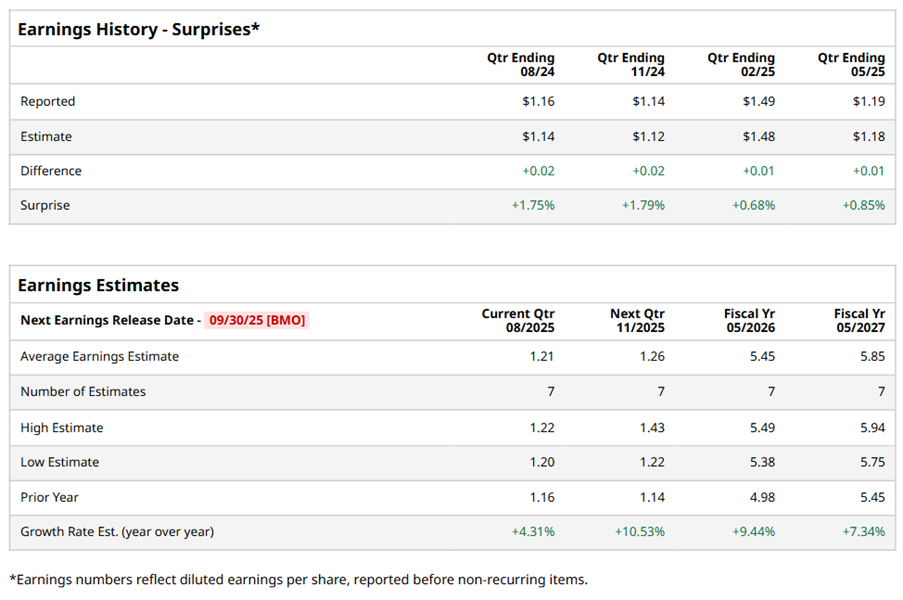

Ahead of the event, analysts expect PAYX to report a profit of $1.21 per share on a diluted basis, up 4.3% from $1.16 per share in the year-ago quarter. The company has consistently surpassed Wall Street’s EPS estimates in its last four quarterly reports.

For the full year, analysts expect PAYX to report EPS of $5.45, up 9.4% from $4.98 in fiscal 2025. Its EPS is expected to rise 7.3% year over year to $5.85 in fiscal 2027.

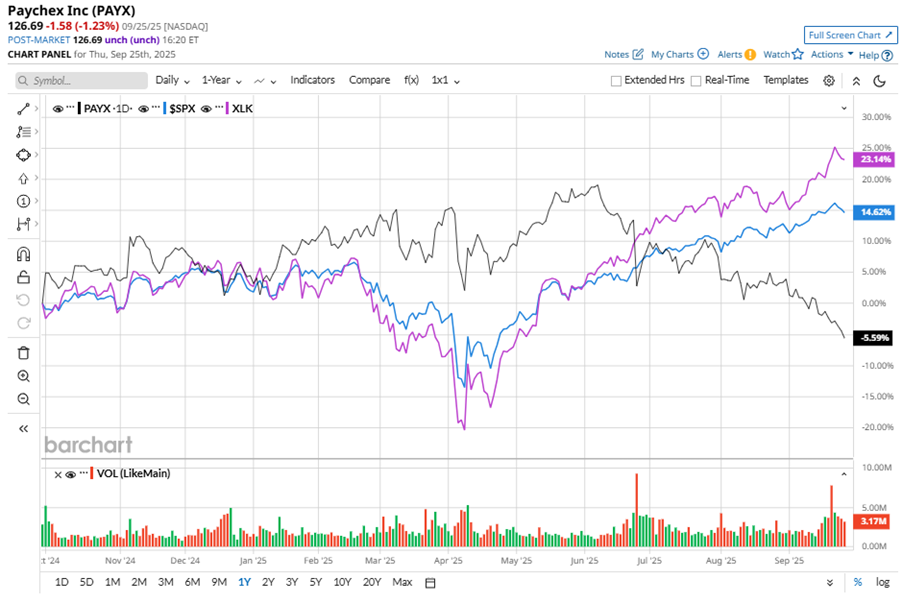

PAYX stock has underperformed the S&P 500 Index’s ($SPX) 15.4% gains over the past 52 weeks, with shares down 4.4% during this period. Similarly, it considerably underperformed the Technology Select Sector SPDR Fund’s (XLK) 24% gains over the same time frame.

On Jun. 25, PAYX shares closed down more than 9% after reporting its Q4 results. Its adjusted EPS of $1.19 surpassed Wall Street expectations of $1.18. The company’s revenue was $1.43 billion, surpassing Wall Street forecasts of $1.41 billion.

Analysts’ consensus opinion on PAYX stock is cautious, with a “Hold” rating overall. Out of 16 analysts covering the stock, 14 give a “Hold,” and two recommend a “Strong Sell.” PAYX’s average analyst price target is $147.42, indicating a potential upside of 16.4% from the current levels.