UK and US markets head higher

With European markets may have been closed for May Day, but shares in London and New York both managed to move higher.

The FTSE 100 finished up 25.32 points at 6985.95, while on Wall Street the Dow Jones Industrial Average is currently up around 100 points.

There are a number of uncertainties ahead, of course. Crunch talks between Greece and its creditors are set to continue over the weekend, while in the UK there is the general election to contend with. And on the same day as the poll result - Friday - come the latest non-farm payroll figures from the US.

On that note, it’s time to close up for the evening. Thanks for all your comments, and we’ll be back next week to cover all the major events.

US consumer confidence rose slightly in April, according to the University of Michigan’s latest survey released earlier, to its highest level since January.

The index came in at 95.9, unchanged from the initial April reading, and up from the March figure of 93. But analysts had been expecting a slightly better level of 96.

#Consumer sentiment +2.9 to 95.9 in Apr. High optimism+steady payroll growth+firmer wage growth=cons spending +3% '15 pic.twitter.com/E688FrxjJG

— Gregory Daco (@GregDaco) May 1, 2015

Updated

Back with the US, and a Federal Reserve rate rise in the near future is even less likely given today’s economic figures, according to James Knightley at ING. He said:

Today’s US data isn’t particularly helpful for those looking for a June rate hike. The April manufacturing ISM index came in at 51.5, the same as in March, but below the 52.0 consensus figure. That said, the activity numbers weren’t all that bad with actual production rising to 56.0 from 53.8 while new orders rose to a four month high, albeit well down on the 60+ levels seen in the fourth quarter of 2014. Interestingly, new export orders actually strengthened despite plenty of commentators suggesting that dollar strength is damaging the US economy and should mean that the Fed delays policy tightening.

There was more support for an “on hold” Fed from the weakness seen in the employment component of the ISM report. It dropped from the break-even 50.0 level in March to 48.3, indicating that the sector saw job losses in April. This is the weakest jobs number since September 2009 and it supports our view that after the first quarter’s economic weakness, labour market hiring will take a little while to pick up – hence our sub consensus 185,000 call for next Friday’s payrolls figure.

We have also seen a big fall in construction spending in March (-0.6% month on month versus consensus forecast of a 0.5% rise) while the April final reading of University of Michigan sentiment was unchanged from the preliminary figure of 95.9.

Taking it all together, the numbers are a little disappointing and if the jobs data is indeed on the softer side of expectations next Friday it will make a June rate hike look unlikely.

Updated

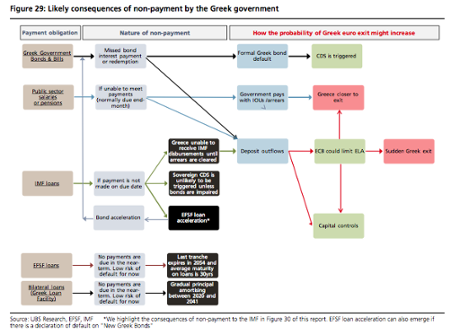

UBS has been looking at the prospects of a Greek default, in response to queries from investors, and has come up with this chart:

Updated

The eurozone would recover reasonably quickly if Greece left the single currency, but the effect on investor confidence could be more serious, according to the managing director of sovereign risk at ratings agency Moody’s. Alastair Wilson told CNBC:

We think the immediate impact would be relatively slight, Greece is a very small part of the eurozone economy, trade with Greece is a very small of overall eurozone trade.

What is more difficult to predict is the impact on confidence in financial markets and therefore the potential implications for eurozone debt markets, which of course are the dynamics we saw at the height of the crisis in 2011-2012.

The impact of a member of the currency union leaving the currency union is bound to have an impact on the confidence of investors who need to be able to allow governments to roll over very significant amounts of debt every year.

Updated

And the second US manufacturing survey is also downbeat.

The Institute for Supply Management’s index of factory activity was 51.5 in April, unchanged from the March figure but lower than 52 figure expected by economists. A rebound in new orders was offset by employment falling to its lower level in more than five years.

On Wall Street the Dow Jones Industrial Average is up 116 points or 0.65% after the ISM and Markit surveys. After the weak US GDP figure earlier in the weak, the prospects for an interest rate rise in the immediate future have receded still further.

#ISM unchanged at 51.5 .. US soft patch disappearing only at slow pace ... not suggesting a sell-off in US rates pic.twitter.com/KRiP11lDyv

— Peter van der Welle (@pvanderwelle) May 1, 2015

Updated

Back to Greece and a court is set to rule on whether a series of cuts to pensions over the years is unconstitutional. The Kathimerini newspaper reported:

The Council of State is expected to rule in the coming days on whether or not a series of cuts to pensions over the years, carried out in line with the demands of international creditors, are Constitutional or not, with most of the court’s judges said to be leaning toward an unconstitutional ruling, Skai understands.

Speaking to Skai television, the Syriza MP and deputy parliament speaker Alexis Mitropoulos said the court’s judges regard the cuts as a violation of the Constitution.

He said the fiscal cost of such a decision, once released, will amount to between €3.5bn and €4bn. According to Mitropoulos, the same judges deem the proposed abolition of a zero deficit clause for pension funds, and the prospect of further cuts, as unconstitutional.

US factory growth slows, says Markit

The first of two US manufacturing surveys is out, and it shows a slowdown in factory activity growth in April.

Markit’s final PMI reading came in at 54.1 compared to the earlier estimate of 54.2 and a figure of 55.7 for March.

April’s growth was the slowest so far this year and Markit chief economist Chris Williamson said:

The survey results raise worries that the dollar’s appreciation is hurting the economy.

Updated

Yanis Varoufakis could not resist bragging. Shortly after Greece’s new leftist government struck a deal with creditors to extend the country’s bailout to the end of next month, the finance minister and glamour boy for the Syriza radicals waxed triumphalist about how he had outfoxed the eurozone.

“We no longer have this unified group against Greece,” he declared in a lengthy radio interview. “We now have a side that has broken down into many different sides, some of which are very open to our proposals. This by itself is a great success.”

So far, the extension of the bailout from 20 February to the end of June has remained the only breakthrough achieved by the brinkmanship of Alexis Tsipras’ government in talks with eurozone creditors.

The condition was that Tsipras comes up with a reform programme that could satisfy lenders. With the clock ticking and the odds shortening on a Greek default, they are still waiting for the Tsipras programme.

Varoufakis’ boast might have gone down well at home, but it was 180° wrong.

Rather than splitting the eurozone, he has managed to unite the other 18 single-currency countries against himself and against Greece more firmly than ever before. As an object lesson in how to make enemies and lose friends, it was quite a feat.

“He annoyed a lot of people, burned a lot of trust,” said one senior EU diplomat.

Two months on and following last week’s disastrous meeting of eurogroup finance ministers in Riga, Varoufakis was defenestrated. Ministers and officials were shockingly open in venting their exasperation and their contempt for the Greek finance minister, who stayed away from the group dinner.

Tsipras quickly read the runes, reshuffled his negotiating team, and shunted Varoufakis aside.

FDR, 1936: "They are unanimous in their hate for me; and I welcome their hatred." A quotation close to my heart (& reality) these days

— Yanis Varoufakis (@yanisvaroufakis) April 26, 2015

Only months ago, it seemed everyone loved Varoufakis. By last weekend he was tweeting how everyone hated him, and bitterly complaining about his “political deconstruction”...

Wall Street opens higher

US shares have opened higher.

- Dow Jones: +0.3% at 17,888.09

- S&P 500: +0.3% at 2,091.71

- Nasdaq: +0.5% at 4,965.17

The Greek prime minister Alexis Tsipras has taken to Twitter with some rallying words for his people on May Day...

We will prevail in our struggles to bolster and protect our rights, our #Democracy and our dignity. #MayDay #May1 pic.twitter.com/db4lRYQmPm

— Alexis Tsipras (@tsipras_eu) May 1, 2015

The FTSE 100 is up 0.1% at 6,966.

Lloyds Banking Group is still the biggest riser, now up 7.4% at 83p as investors welcomed confirmation that a dividend will be paid this year, for the first time since the 2007 bailout.

Surge in UK consumer credit

Bank of England figures published earlier showed that lending to British consumers grew at the fastest rate since before the financial crisis in March.

Consumer credit grew by £1.24bn, beating forecasts of an £800m increase. It was the biggest monthly increase since February 2008, and the biggest annual jump since May 2006.

The backdrop for consumers has improved recently, with inflation falling to an all-time low of zero signalling an end to six years of falling real pay.

James Knightley, economist at ING:

Credit growth continues to perform robustly, suggesting that households remain upbeat. Net consumer credit rose £1.2bn on the month – you have to go back 10 years to when the UK was previously seeing that level of borrowing on a consistent basis.

Mortgage approvals fell slightly however, despite mortgage rates falling to new record lows. There were 61,341 loans approved for house purchase last month, compared with 61,523 in February.

March’s figure was up on the previous six-month average of 60,303, but below the 67,033 approvals in the same month of 2014.

ECB's Honohan is 'slightly optimistic' over a Greek deal

A member of the European Central Bank’s governing council claims he is “slightly optimistic” that a deal will be agreed between Greece and its creditors.

Not hugely bullish from Patrick Honohan, who is also the governor of Ireland’s central bank.

Speaking at a press conference in Dublin, he said:

I’m slightly optimistic that there will be an outcome that’s good and favourable. I don’t like to talk about any alternatives.

Greek governments seeks to delay more difficult reforms

Here in Athens, the Greek government has announced that until it gets “concrete signs” of the country’s liquidity asphyxiation being eased, it is not going to bear the political cost of putting a potentially explosive list of reforms before parliament.

Hosting a cabinet meeting late Thursday, prime minister Alexis Tsipras expressed optimism that an interim agreement was close to being reached but he continued to insist that it would be “within the bounds of the popular mandate that we have received, which is defined by the red lines that we have put forward.”

As such, his anti-austerity administration would only present an omnibus of reforms once it had a guarantee that steps were in the pipeline to loosen the economic noose. “Red lines for the government remain labour protection, the reduction of wages and pensions, the sell-off of public property and the increase in VAT,” officials said.

Insiders say the Syriza-dominated coalition wants to put off dealing with the more difficult demands being made by creditors until the end of June, the deadline set for the debt-stricken nation to seal a final agreement with lenders. “That way the package could include some good things and bad things because progress may have been made [in collecting revenues],” said one.

Forced to survive on emergency liquidity assistance from the ECB, Greece has not received any bailout funds from the EU or IMF since last August.

The finance minister Yanis Varoufakis (who was mobbed this morning by supporters as he participated in a rally to mark May Day in Athens) also signalled concessions could be made once an initial deal is reached to unlock funds.

“After June, we are willing to look at many issues.”

The prospect of any “red lines” being crossed has sent tensions spiralling within Tsipras’s Syriza party, with leftwing militants covering the capital with May Day posters proclaiming “we are not going to be blackmailed – not a step backwards. Nothing can stop a people who are determined.”

Hardliners, led by the energy minister Panaghiotis Lafazanis, fear the government is heading for “a humiliating capitulation” and called on it this morning to “encourage the Greek people and to speak to it frankly about alternative solutions.”

Over in Greece, monthly pension payments appear to have gone through, following angry scenes outside Athens banks on Thursday.

Greek officials denied a technical hitch delayed payments, but the confusion was a reminder that the government is under intense pressure at home as well as in Brussels.

Agreement has yet to be reached with its creditors on a package of Greek reforms - essential if another tranche of bailout funding is to be released.

In the meantime attention will soon shift to 6 May, the deadline for Greece’s next repayment (€200m) to the International Monetary Fund.

Finance watchdog looks at new market-rigging claims

In other UK news, the Financial Conduct Authority is looking into a series of complaints over the manipulation of a key contract used to price savings products and mortgages.

This report from my colleague Julia Kollewe:

The City watchdog is scrutinising a series of complaints over manipulation of a key contract used to price savings products and mortgages.

The complaints allege the systematic rigging of short-term interest rate contracts (Stirs) by traders on the London International Financial Futures Exchange (Liffe) in recent years.

The Financial Conduct Authority is looking into a number of complaints made by traders and former Liffe officials, including one passed to it from the Bank of England. The watchdog, which declined to comment, works closely with the central bank. However, it appears that regulators have stopped short of launching a full investigation into the claims of market abuse.

The Times reported that several current and former traders, including former Liffe officials, were concerned that large volume trades on Stirs could be placed in the market with no intention of being traded.

The practices are said to be similar to the techniques used by Navinder Sarao, the “flash crash” trader. Trading videos seen by the Times show trades as large as 24,000 lots, with a notional value of £12bn, being placed and then rapidly withdrawn.

Now for some reaction to the weak manufacturing PMI from City economists (whose forecasts were far wide of the mark) and other experts.

Uncertainty over the outcome of next week’s general election, as well as a stronger pound against the euro, are cited as two of the main reasons behind the sharp slowdown in manufacturing growth in April.

Christian Schulz, senior economist at Berenberg, says bad luck is partly to blame for the failed rebalancing of the economy.

In a way, bad luck has prevented a more balanced recovery in the UK, where consumption continues to be the most reliable driver of growth. When sterling was low in 2009 - 2013, it did not help UK exporters very much because demand from the major export market, the eurozone, was weak due to the global financial crisis and the euro crisis.

Now that the eurozone is rebounding, UK exporters struggle to defend their market share due to the weaker euro. Still, we expect the return to more normal growth in the eurozone to benefit UK manufacturers as well over time. The large April drop in the UK manufacturing PMI is likely to be a blip and buoyant domestic demand will support activity.

Mark Stephenson, head of UK manufacturing at Deloitte:

This decelerating pace of growth is strongly linked to the general uncertainty that has crept into the manufacturing and industrials sector in the past few months. The strengthening of the pound against the euro continues to bring concerns over exports, impacting on the UK’s competitiveness and margins.

Furthermore, the looming general election adds further unease to the sector in terms of EU membership and any possible changes to taxation.

Howard Archer, chief UK and European economist at IHS Global Insight:

This is a disappointing survey that adds to the evidence that the economy has recently lost momentum, which likely partly reflects increased business caution ahead of the highly uncertain general election.

It is also evident that UK manufacturers are being hampered in key eurozone export markets by sterling’s strength against the euro.

The weakened April manufacturing managers’ survey highlights the importance for the economy that a sustainable government emerges from next Thursday’s general election. Prolonged political uncertainty could take a significant toll on the economy.

Lee Hopley, chief economist at manufacturing trade body EEF:

Recent data points to a marked loss of momentum in manufacturing activity since the start of the year. While consumer facing sectors are still forging ahead thanks to low inflation and a pick-up in wage growth, any sign that export growth was about to turn around at the end of last year now looks to have been a false dawn.

Nevertheless, it would be premature to write off manufacturing’s contribution to growth in the future, not least because continued employment growth points to some confidence about longer term prospects.

Still, this is another reminder that the next government must focus on delivering a competitive and predictable environment to keep business growth on track.

UK manufacturing output slumps to 7-month low. PMI slides to 51.9, way below all 31 estimates in @ReutersPolls pic.twitter.com/A1xXa0rgv8

— Jamie McGeever (@ReutersJamie) May 1, 2015

Shockingly weak. That’s the only way to describe news highlighting the continuing struggles of Britain’s manufacturers last month.

Its easy to see why the health check of industry from Markit/CIPS raised eyebrows. The snapshots of the three most important sectors of the economy - manufacturing, construction and services - are closely watched because they are the first evidence of the state of the economy in the month and they are forward rather than backward looking.

So while City analysts were taken aback by the halving of growth in the first three months of 2015 they comforted themselves with the thought that the slowdown was a blip. They were looking for a pick up in the Markit/CIPS purchasing managers’ index to show that the weakness since the turn of the year had been a temporary aberration.

Instead, the PMI weakened sharply. Manufacturing is growing - just about - but only because of demand for consumer goods. Companies making investment goods or intermediate goods (products that are used to make things by other manufacturers) are having a tough time.

What does this tell us? Firstly, the economy has come off its sugar-rush high. Growth was boosted in 2013 and early 2014 by a booming housing market. Since the Bank of England reined in mortgage demand, the pace of activity has slackened. This is despite more than six years or 0.5% interest rates and the halving of oil prices in the second half of 2014.

Secondly, the economy remains dangerously unbalanced. There has not been the shift to manufacturing, investment and exports promised by George Osborne back in 2010. The strong pound is hitting sales of goods to Europe and companies are not investing. Consumer demand remains the main source of growth.

Finally, the Government’s claim to have turned round the economy in the past five years is bunk. The Conservatives chose this week to focus on the economy in the expectation that they could point to signs of success. Their timing could not have been worse.

First it was the halving of the growth rate. Now the news is that the outlook for UK manufacturers is deteriorating fast. This has not been a good week for the Government’s claim to have turned round the economy.

The unexpected and sharp fall in the headline manufacturing PMI to 51.9 in April from 54 in March was driven by broad weakness in the sector.

It was the slowest growth for UK factories in seven months, as growth in output, new orders, and employment all slowed.

Job creation in the sector was the slowest in almost two years.

This is not good news for the Conservatives, following the GDP shocker on Tuesday (growth halved in Q1 to 0.3%).

With less than a week to go before the general election, the signal from the manufacturing PMI is that that the economy got off to a poor start in the second quarter.

That is a blow to David Cameron and George Osborne, who have marked out the economy as a key election battleground for the Conservatives.

Consumer goods were behind the (weak) growth in manufacturing orders and output in April according to the PMI.

Given growth in the sector was dependent on domestic work and not work abroad, that poses another difficulty for the current government: it’s stated ambition is to rebalance the economy away from a heavy reliance on consumer spending and towards more manufacturing and exports.

As yet, exports have yet to provide a boost to the economy and more than six years on from the beginning of the financial crisis, manufacturing output has yet to surpass it’s pre-crisis peak.

This is what Rob Dobson, senior economist at Markit, had to say:

Coming on the back of weaker-than-expected GDP numbers on Tuesday and only six days before the general election, today’s UK PMI delivered less than positive news on the health of the manufacturing sector.

Rates of expansion in production and order books both slowed sharply in April, meaning manufacturing is again unlikely to provide much of a boost to broader economic growth. This keeps the emphasis for maintaining the recovery highly reliant on the services sector.

Growth remains largely consumer-led, with the strong performance of the consumer goods sector in stark contrast with other sectors.

The investment and export pictures are also subdued. A decline in capital goods new orders is a weak bellwether for business investment spending, while a slowing global economy and strong sterling- euro exchange rate are hurting the competitiveness of exporters.

A key challenge for the next government is to revive manufacturing and help it at least regain its pre-crisis peak, as any signs of rebalancing the economy towards manufacturing and exports remain frustratingly elusive.

Pound falls on UK manufacturing slowdown

The far weaker-than-expected manufacturing PMI has sent the pound lower.

It fell to a three-week low against the euro, down half a per cent with one euro worth 73.45p.

The pound also fell against the dollar, to $1.5322 from $1.5370.

Updated

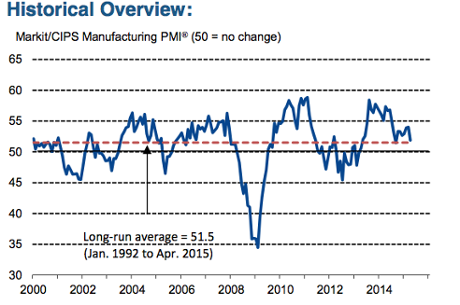

Breaking: growth in UK manufacturing sector slows sharply

The headline index on the Markit/CIPS manufacturing PMI fell to 51.9 in April, from 54.6 in March.

This is a bit of a shocker. Economists were expecting 54.6 (where anything above 50 signals growth). The March number was revised down to 54 from 54.4.

More soon...

Updated

UK manufacturing growth expected to accelerate in April

At 9.30am we will get the earliest indication of how the UK economy was performing as the second quarter got underway.

The Markit/CIPS manufacturing PMI survey for April will be closely watched by markets and policymakers alike.

The headline index - combining output, orders and employment - is expected to edge up slightly to 54.6 from 54.4 in March (where anything above 50 indicates growth).

A disappointing figure is likely to trigger investor nerves, following that shockingly weak GDP number on Tuesday which showed growth halved unexpectedly in the first quarter to just 0.3%.

Some positive data out of the eurozone - not least strong growth in Spain - suggests the region might well have outperformed the UK in the first three months of the year. The first official estimate of eurozone growth will be published on 13 May.

Updated

While most European markets are closed today for the May Day holiday, Michael Hewson, chief market analyst at CMC Markets UK, reflects on their recent performance and considers what might lie ahead in the short term.

It’s not been a good week for European equity markets with the rebound in the euro knocking the German DAX down quite heavily, posting its first monthly loss this year.

The declines this month and this week also raise the prospect of more losses to come, particularly if the euro continues to rise in the coming weeks, which seems quite likely, given that it is becoming increasingly likely that any prospect of a US rate hike has receded by at least three months.

The fact is the sell euro/buy European equities trade had become a crowded one and what we’ve seen at the back end of April is a recognition that it might be time to cash in some of those chips.

TSB sell-off dents Lloyds profits

Lloyds Banking Group has taken a £745m hit from the forced sell-off of its TSB branch network.

A reminder, if needed, of how the impact of the financial crisis that began in 2007/8 is still being felt.

The Guardian’s Jill Treanor reports:

Lloyds Banking Group has taken a £745m hit from its TSB branch network, denting profits at the bailed-out bank in the first three months of the year.

Lloyds was forced to sell off the 631-branch network under terms agreed with the EU before its 2008 taxpayer bailout. The government originally took a 43% stake in Lloyds but this has now fallen to 20.95% through a series of share sales.

Although the bank’s profits were dented by the cost of the TSB sell-off, Lloyds made no further provision for payment protection insurance compensation, which has wiped £12bn off profits since 2011.

Finance director George Culmer was careful not to rule out any further PPI charges and pointed out the bank still had £1.7bn set aside for compensation payments.

“A number of risks and uncertainties remain, in particular the total expected future complaint volumes,” the bank said.

Lloyds’ profits fell 11% to £1.2bn although the bad debt charge was just £177m, down by 59%. The bank signalled this charge would rise through the rest of the year but less quickly than it had originally anticipated and that it would remain in sharp contrast to the first year of its bailout when the bad debt charge was £13.4bn.

FTSE 100 falls

The FTSE 100 is down 0.5% in early trading at 6926.

Lloyds Banking Group is the top riser, up 3.3% at 80p after publishing its first-quarter results (more on those soon).

On the flip side, 3i Group is the worst performer, down 2.9% at 492p.

The agenda: UK and US manufacturing data; Greece

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

The latest manufacturing data for China was published overnight, showing the sector barely grew in April.

The official Purchasing Managers’ Index (PMI) came in at 50.1, unchanged from March. Given anything above 50 indicates expansion, it is clear that China’s manufacturing sector is struggling to gain momentum.

There will have been a certain amount of relief however, as the PMI was in line with expectations.

The equivalent survey for the Chinese services sector showed growth slowed in April, with the official non-manufacturing PMI easing slightly to 53.4 from 53.7 in March.

Most European markets are closed today for May Day, but the UK and US are open for business.

On both sides of the Atlantic, manufacturing PMIs for April will give the latest snapshot of how the sector is performing.

They will also be taken as crucial indicators of what sort of start the UK and US economies made in the second quarter, after a hugely disappointing first quarter for both countries.

We will also be bringing you the latest developments on Greece, where the poker game negotiations continue between the country and its creditors.