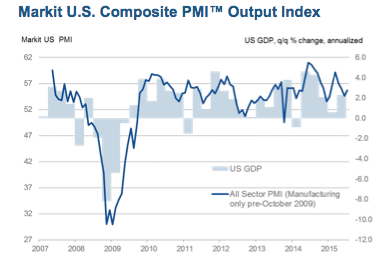

The composite output index, which covers manufacturing and services, posted 55.7 last month, up from June’s five-month low of 54.6. Markit noted that although the latest reading points to a relatively strong increase in US private sector output, the rate of expansion was fractionally weaker than that recorded on average in the second quarter of 2015.

US services activity improved in July

To round off the services PMIs, the US survey is just out and shows activity strengthened in July, led by the fastest rise in new work in three months.

The Markit US services PMI recorded 55.7 in July, up from 54.8 in June.

Markit said:

July data indicated a slight rebound in service sector activity growth, following the five-month low recorded in June. The latest survey also highlighted a strong and accelerated rise in new work, alongside a further robust upturn in payroll numbers. However, service providers’ confidence regarding the year-ahead business outlook dipped to its lowest since June 2012.”

Meanwhile, revisions to back data by the UK’s Office for National Statistics paint a slightly different picture of Britain’s economic recovery from the 2009 recession in the wake of the global financial crisis.

After today's ONS revisions and last week's from BEA, US and UK recoveries since Q2 2009 troughs have been v similar. pic.twitter.com/DmO54xnKKJ

— Mike Bird (@Birdyword) August 5, 2015

UK recession was worse than US, US recovery slowed much more than thought in 2013, UK stagnation in 2012 not as bad as thought.

— Mike Bird (@Birdyword) August 5, 2015

Wall Street set to open higher after jobs data

Wall Street is set to open higher after data showed hiring in the private sector slowed in July, which raised hopes that the Fed could wait until December before putting up interest rates, which would be the first hike in nearly a decade.

The ADP National Employment Report showed private employers took on 185,000 workers, the smallest increase since April and below the 215,000 increase forecast by economists. The figures come ahead of the monthly non-farm payrolls data on Friday.

Fed governor Jerome Powell told CNBC on Wednesday that policy makers had not yet made up their minds about whether to raise rates in September, and that data on the labour market would be key to that decision.

Nothing has been decided. I haven’t made any decisions about what I would support, and certainly the committee hasn’t.

The economy is moving along about as expected ... the labor market continues to be strong.”

But “more recent data has been mixed,” including a weaker than expected reading of wages in the second quarter.

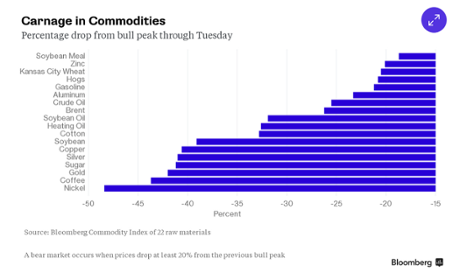

Here’s an interesting chart on the commodities meltdown, courtesy of Bloomberg. Commodities are crashing like it’s 2008 all over again.

Updated

Following reports that former Bank of England deputy governor Sir Charlie Bean will lead a review into the state of the UK’s national economic statistics, Paras Anand, head of European Equities at Fidelity Worldwide Investment, said:

This is an area we have been interested in for some time. The real economy has evolved over time due to the impact of technology, the emergence of new business models and changing consumer preferences. This has meant that the traditional means of measurement have at best led to confusion and at worst led to mis-representation.

For example, there is a lot of negative commentary on collapsing productivity. The challenge is that the Office of National Statistics (ONS) currently uses GDP per capita to measure productivity, but the GDP statistic fails to capture services that were previously paid for but are now available for free, such as postal services (replaced by email), music (streaming services) or news. The fact they are now free means that people are using them more and we have therefore become significantly more productive. However, the way this is being captured statistically is suggesting the opposite.

Another issue is the way the current account deficit is measured, with a focus on sales rather than profit. It is questionable whether this truly reflects the value of exports vs the value of imports vs the price of the finished goods. In an example where you are importing smartphones from overseas but some of the core components such as software, chipsets and security features being provided by UK companies, the value equation between the imports and exports might be a lot more balanced that is being suggested by the measure.

We welcome this evolution as we think it is important, but there will be challenges. Replacing the statistics that exist today with new forms of measure is by no means is an easy task – the ONS will have a large mountain to climb to find suitable alternatives. It may require some thought around different and, in some cases, quite esoteric forms of measurement. Some of the answers may actually exist in measures which grew in prevalence through the tech boom. The tech bust had the consequence of discrediting a lot of the measurement techniques that were put forward to think about the new economy. We should be open minded about the possibility that there may be some upside in dusting off some of those abandoned methodologies and consider whether at least some of them may have more saliency in the future.”

Updated

ECB's Nouy: Greek banks could be recapitalised via bailout money

The European Central Bank is closely monitoring Greek banks and any capital shortfalls could be plugged using some of the money from the next (and third) bailout, the ECB’s banking supervision chair Daniele Nouy said. Greece is still hammering out the details of the agreement, which could total €86bn.

She said in a letter to a member of the European Parliament:

If this assessment identifies capital shortfalls for one or more significant institutions, these may be covered by the capital buffer to be established under a new Greek programme, after applying the legal framework.

#Greece's Tsipras says loan deal w/ lenders close. Markets not so enthusiastic. 2y ylds unchg. http://t.co/8R9g7zM9XS pic.twitter.com/xtaUvouBKe

— Holger Zschaepitz (@Schuldensuehner) August 5, 2015

Early elections won't solve any of Tsipras' parl majority problems if he won't b able to xclude dissenters from Syriza ballot lists. #Greece

— Yannis Koutsomitis (@YanniKouts) August 5, 2015

Updated

The latest US figures show the trade deficit widened more than expected in June, with imports of food and cars reaching a record high, while exports fell for the second month in a row.

The US Commerce Department said the trade gap increased 7.1% to $43.8bn. Wall Street had expected a deficit of $42.8bn. The strong dollar and sluggish global demand held back exports, which slipped 0.1% to $188.6bn. Exports to the EU fell 2.3%.

Imports increased 1.2% to $232.4bn as domestic demand picked up. The strong dollar, which has gained 15% against the currencies of the US’ main trading partners over the past year, is also making imports cheaper.

The Greek prime minister said during a visit to Greece’s agriculture ministry, according to Reuters:

We are on the final stretch of concluding a deal with the institutions... Despite the difficulties we are facing we hope this agreement can end uncertainty on the future of Greece and of the eurozone.

Tsipras: Greece close to bailout deal; government spokeswoman: elections 'likely' in autumn

Over in Greece, prime minister Alexis Tsipras says the country is on the “final stretch” of concluding a deal with lenders, Reuters reports. Despite difficulties, he is is hopeful the deal will end the uncertainty surrounding the future of Greece and the eurozone.

And a Greek government spokeswoman has suggested that Athens will hold elections in the autumn.

Early elections "likely" in the autumn ~#Greece gov't spokeswoman

— Yannis Koutsomitis (@YanniKouts) August 5, 2015

Updated

The Economist has taken a look at what the slide in commodity prices means for commodity exporters – mainly emerging markets. The magazine writes:

FIVE years ago, two views were fairly common. The future belonged not to the sluggish, ageing advanced economies but to the emerging markets. Furthermore, those economies had such demand for raw materials that a “commodity supercycle” was well under way and would last for years.

Commodity prices peaked in 2011, and have been heading remorselessly downwards ever since. Their decline of more than 40% so far is a huge bear market; had it happened in equities, the talk would be of calamity and collapse.

News coverage in the Western media tends to view the decline in commodity prices as a benign phenomenon, as indeed it is for countries that are net importers. But it is not good for commodity exporters, many of which are emerging markets. That helps explain why emerging-market equities have had only one positive year since 2011, and have underperformed their rich-country counterparts by a significant margin in recent years. The latest sign of trouble came in China, where the Shanghai Composite fell by 8.5% on July 27th...

Given the background, this does not seem the most obvious time for the world’s leading central bank to be tightening monetary policy. Of course, the Fed is supposed to focus on domestic conditions, not the international environment. But higher American rates will probably mean a stronger dollar, and thus tighter monetary policy for countries that peg their currencies to the greenback. And it will create a problem for economies with lots of dollar debt. Several emerging-market currencies are already at multi-year or record lows.

The hope is that the signs of a slowdown will prove mistaken. The IMF expects both the global growth rate and that of emerging economies to pick up in 2016. Perhaps it will be right. Unfortunately, it has often been over-optimistic in the past.

IMF staff: delay adding yuan to currency basket

The International Monetary Fund’s board has been told to delay any move to add the yuan to its benchmark currency basket until after September 2016. That’s the recommendation given by the Washington-based organisation’s staff in a report that showed the Chinese currency lagged other major currencies in in terms of meeting key financial benchmarks.

The report comes after Beijing made a major diplomatic push for the yuan to be added to the IMF’s Special Drawing Rights basket as part of its long-term strategic goal of reducing dependence on the dollar.

The IMF board is due to make a decision in November on whether to include the yuan in the basket of currencies, which includes dollars, euros, pounds and yen, although the decision could be pushed back if policymakers decide they need more information.

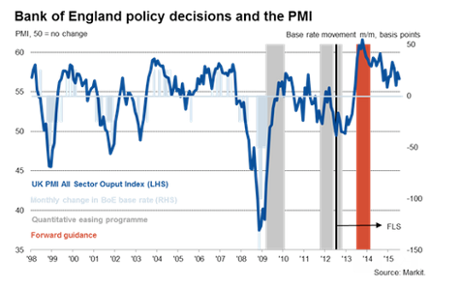

A UK rate rise does appear to be getting closer, judging by the Bank of England’s recent rhetoric.

Citi economist Michael Saunders says:

We expect no change in either Bank Rate or QE from the MPC on Thursday. The MPC’s core policy message is likely to be in line with the governor’s recent speech, namely that MPC tightening is on the horizon but probably not imminent.

The meeting may well feature the first split vote since last December.

We expect the MPC will lift their growth forecast, but lower the inflation outlook.

Two key wild card factors are the scale of any minority vote for a hike and whether the MPC put greater emphasis on domestically-generated inflation measures.

George Buckley, UK economist at Deutsche Bank, says:

Some MPC rhetoric – including that from the governor – is hinting that a rate rise is getting closer, and that as inflation rises around the turn of the year this should become more evident. Not all Committee members agree, with the Bank’s chief economist being one of the more vocal dovish voices.

Chris Hare at Investec says:

Mood music for a rate rise has become louder in recent weeks, underscored by the previously-reputed MPC dove David Miles saying that an interest rate hike should come ‘soon’. And the minutes from the 8 July meeting pointed out that, absent Greece-related concerns, the decision to raise rates was becoming ‘more finely balanced’ for ‘a number’ of members. Now that Greek risks have receded, and the insights from updated forecasts will be on the table, that could well be enough for a hawk or two (perhaps Martin Weale and Ian McCafferty) to pull the trigger.

That said, we do not think that the majority will vote for a rate hike until Q1 next year. One of the main reasons is that currently, with headline inflation at zero, a rate rise is presentationally more difficult than it should be in 16Q1. At that point we expect inflation to be above 1% as past falls in energy and food prices drop out of the calculation.

Money markets are now pricing in a Bank of England rate hike in the first quarter of next year, rather than in May as at the start of the week. Rates are then seen rising gradually to 2% by the middle of 2018. What seems certain is that the Fed will act first.

While Britain’s economy is recovering, inflation remains low.

“Super Thursday” should shed more light on the Bank’s thinking. Minutes of its monthly meeting are expected to reveal a split on the nine-member monetary policy committee, with two or three votes for a rate rise this month.

Martin Beck, senior economic advisor to the EY ITEM Club, said:

As we move ever closer to ‘Super Thursday’ – the first simultaneous publication of the MPC decision, minutes and Inflation Report – there was little in this survey to suggest that the MPC will be close to pulling the trigger on rate rises this month. Though selling prices accelerated, they did so at a pace which was in line with the long-run average, while input cost inflation remains very weak. Therefore, while it is perfectly possible that we will see two, or maybe even three votes in favour of a rate hike on Thursday, in our view the chances of a move this year remain low.”

Updated

Pound hits two-week high vs euro on rate rise expectations

Sterling is holding up against the resurgent dollar, amid expectations that any rise in US interest rates will be swiftly followed by a Bank of England rate hike.

Growing expectations that the Fed will act on rates as early as September initially sent the pound 1 cent lower against the dollar, but it later recovered and is now 0.1% higher on the day at $1.5581. Against the euro, it climbed to a two-week high of 69.65p per euro.

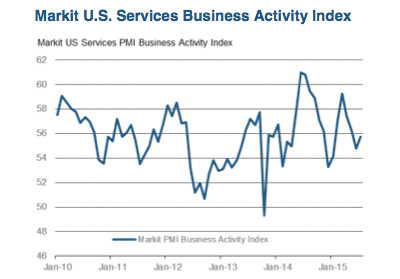

JPMorgan economist Allan Monks says the UK services PMI is “holding its ground”.

Its current level remains broadly in line with its average for 1H15 and is more than a point higher than its long run average of 56.0. The details also look firmer than suggested by the headline, with new business rising from 57.2 to 58.6. Overall, the July PMIs this week suggest that manufacturing is still stagnating, but with enough momentum from the service sector to keep overall GDP growth looking firm.

One noteworthy development in the services PMI is the large drop in the employment reading from 56.0 to 53.8. While still high in an absolute sense, the decline is large and echoes some other labour market indicators which point to a slowing in employment growth. If output growth holds up as expected, this offers some further hints of a better productivity outturn for this year.

Greek air traffic controllers strike, seeing EU-based reforms

Greek air traffic controllers have gone on strike a the height of the tourism season, causing several domestic and international flights to be cancelled.

At Athens airport, about 22 flights were cancelled and 173 rescheduled due to the four-hour stoppage. The controllers are striking from 11.00 to 15.00 GMT. They are asking for EU-based reforms – calling for their government agency to be restructured and an independent one set up in line with EU rules. They believe this would hep Greece deal with staff shortages and a lack of funds for the maintenance of air traffic control systems.

The air traffic controllers’ union has threatened to step up action from 14 August if the government does not respond to its demands. Tourism accounts for a fifth of Greece’s economic output.

Updated

Athens stock market loses further 3.6%, banks down sharply

The Athens stock exchange is once again in the red, for the third day running since reopening on Monday following a five-week suspension. It has lost 3.6%, with the banks posting further sharp falls.

Piraeus Bank -29.59%

Alpha BAnk -29.56%

Eurobank -26.76%

Attica Bank -16.67%

National Bank of Greece -15.14%

European stock markets are still trading higher. Britain’s FTSE 100 index has been boosted by better-than-expected results from insurer Legal and General and the London Stock Exchange. A rebound in the mining sector has also helped – despite a lacklustre copper price which remains near six-year lows, hit by concerns over demand from China and expectations of a rate hike in the US.

UK’s FTSE 100 index up 0.2% at 6699.84

Germany’s Dax up 1.06% at 11576.99

France’s CAC up 1.04% at 5165.47

Updated

Markets: oil prices rise for second day, dollar at 3-month high

Turning to the markets, oil prices are up for a second day after falling below $50 a barrel on Monday, a six-month low. Oil has been boosted by weekly data that showed a fall in US crude stocks, although the strong dollar held back gains.

Brent crude is trading at $50.25 a barrel, up 0.5%, while New York light crude is at $45.91, up 0.37%.

The dollar rose to its highest level in over three months after hawkish comments overnight from a voting member of the US Federal Reserve’s policy setting committee. Atlanta Fed president Dennis Lockhart said there would need to be a “significant deterioration” in economic activity to hold the Fed back from raising rates in September.

The dollar hit a 3 1/2 month high against a basket of currencies. That took the euro to a two-week low of $1.0847. Markets are eagerly expected Friday’s non-farm payrolls data.

Eurozone retail sales fall 0.6%, weaker than expected

More data: Retail sales in the eurozone were weaker than expected in June. According to Eurostat, they fell by 0.6% from the previous month.

The all-sector PMI for the UK, which measures the combined output of services, manufacturing and construction, fell to 56.7 in July, the lowest since December 2014, from 57.4 in June.

Chris Williamson, chief economist at survey compiler Markit, said the latest PMI surveys for the UK sent out mixed signals for the Bank of England:

While the slowdown in business activity signalled by the surveys was only modest, the hiring trend was more worrying. Employment growth fell sharply to the lowest since September 2013.

Despite falling, the PMI remains at a level which has encouraged the Bank of England to tighten policy in the past, which will add to the hawkish mood among a divided Monetary Policy Committee. However, there are plenty of excuses to hold off from hiking interest rates any time soon, including zero inflation, a waning rate of job creation, a strong pound hurting exports and the latest signs of growth cooling. Policymakers will also be concerned about the global economic outlook, and slower growth in emerging markets in particular, which the manufacturing PMI showed to have slipped back into contraction in July.

While a rate hike later this year remains a distinct possibility, the majority of Monetary Policy Committee members will most likely want to see stronger numbers than today’s PMI before feeling comfortable about voting for higher interest rates.

Updated

UK services growth slows as hiring hits 16-month low

Growth in Britain’s services sector has slowed more than expected, as hiring eased to its slowest pace since March 2014. This suggests the economic recovery weakened at the start of the second half of the year.

The Markit/CIPS services PMI dipped to 57.4 in July from 58.5 in June, still indicating expansion among services businesses.

Taking together with this week’s manufacturing and construction surveys, the reading points to economic growth of 0.6% in the three months to July, slightly lower than the 0.7% reported by the Office for National Statistics for the three months to June.

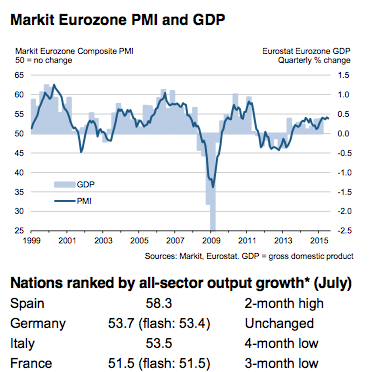

The current period of job creation is the longest achieved since 2011, Markit said. Germany, Italy and Spain all reported higher employment last month, with the rates of increase accelerating in Germany (five-month high) and Spain (100-month record).

Markit went on to say:

Spain registered the best rate of economic growth of the ‘big-four’ eurozone nations, with the pace of expansion moving back towards April’s 101-month record. Growth in Germany remained solid and steady, whereas decelerations were signalled in both France and Italy.”

Eurozone private sector growth eases due to France and Italy

Markit’s composite index for the eurozone as a whole shows growth in the private sector eased in July. It dropped to 53.9 from 54.2 in June.

Markit said:

The latest PMI data showed the rate of expansion in eurozone economic activity slowing slightly at the start of the third quarter. However, growth remained close to June’s four-year high, with the extent of the easing less marked than that signalled by the earlier flash estimate.”

So Eurozone has Spain to thank for PMI Services beat? Que pasa?

— Mike van Dulken (@Accendo_Mike) August 5, 2015

Updated

Some instant reaction...

Germany Markit Services PMI came in at 53.8, above expectations (53.7) in July http://t.co/V7IDfzdqP3 #Forex http://t.co/04eMTitzeb

— FX in Effect (@FXinEffect1) August 5, 2015

France Markit services PMI final July 52.0 as exp: No great shakes here - 52.0 prev - composite 51.5 as exp/pr... http://t.co/Q7QvyT9RZc

— Forex Warrior (@Forex_warrior) August 5, 2015

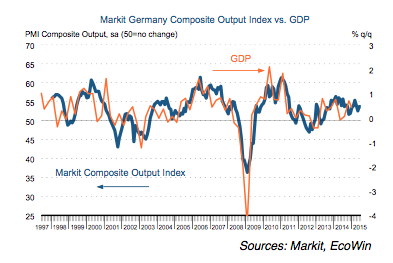

The German composite index, which measures the combined output of the manufacturing and service industries, was also unchanged from June’s reading, signalling further “solid activity growth at German private sector firms,” according to survey compiler Markit.

German services sector continues to rise at above-average pace

Finally, Germany’s services sector grew at the same above-average pace last month as in June, with the PMI coming in at 53.8, unchanged from June. A reading above 50 indicates expansion; a reading below points to contraction in business activity.

Service sector activity in #Germany continues to rise at above-average pace. Headline index at 53.8 in July http://t.co/IrdkHft8pY #PMI

— Markit Economics (@MarkitEconomics) August 5, 2015

French economic recovery slows

Markit economist Jack Kennedy said about the drop in the French composite index:

Having picked up to the fastest rate in nearly four years during June, activity growth took a step back in July. The service sector looks to be still struggling to generate much upward momentum in a persistently subdued demand environment.

A return to job cutting and dip in business expectations in the latest survey period suggest that companies are far from convinced about the recovery and that last month’s stronger numbers may have been something of a false dawn.”

Updated

The French services sector has also slowed, with the PMI dropping to 52 last month from 54.1 in June. The composite index, which comprises services and manufacturing, is also lower, at 51.5 from 53.3 in June, indicating slower economic activity.

Markit #France Services Activity Index falls to 52.0 (54.1 in June). Composite Output Index at 51.5 (53.3 in June) http://t.co/qlnVTkMyqp

— Markit Economics (@MarkitEconomics) August 5, 2015

Italy's services growth eases

Italy’s services PMI has come in lower than expected with a reading of 52 for July, from 53.4 in June (a 12-month high), indicating slower growth. Encouragingly, however, the new business sub-index rose to 53.7 from 52.7.

The eurozone’s third biggest economy is emerging from a three-year slump and is forecast to return to modest growth this year after national output rose 0.3% in the first quarter, ending its longest recession since World War II.

Updated

Athens stock market in the red again, banks drop further

Meanwhile, the Athens market has turned red again, opening 1.6% lower. Greek bank shares drop a further 7.9% in early trading.

Other European stock markets have opened higher, as expected.

FTSE 100 index up 0.15% at 6696.96

Dax up 0.75% at 11542.15

CAC up 0.9% at 5159.29

Updated

SPAIN SERVICES PMI MASSIVE BEAT IN JUNE: 59.7 (55.5 expected, 56.1 previous) #Euroboom2015 http://t.co/y81fUGMVMO pic.twitter.com/YIhtQt4yeF

— BI UK Finance (@BIUK_Finance) August 5, 2015

#Spain - growth in economic activity very strong again in July. Composite PMI 58.3 vs 55.8 in June. pic.twitter.com/zmlKa6vWIK

— Edward Hugh (@Edward_hugh) August 5, 2015

To fix its economy Spain made some brave, unpopular choices that seem to be working out http://t.co/4h0yH6dcGA

— Bloomberg Business (@business) August 4, 2015

https://twitter.com/Simon_Nixon/status/628832774414303232

Updated

Spain's services growth 'massive beat'

Here we go – the PMI for Spain is out. Growth in Spain’s services sector has hit a three-month high, beating economists’ expectations. Markit’s purchasing managers’ index (PMI) of service companies jumped to 59.7 in July from 56.1 in June.

The survey showed that service companies hired staff at the fastest rate in eight years as the tourism season got under way.

Official figures last week showed the economy grew at the fastest quarterly rate since 2007 in the second quarter.

Updated

Turning to Greece, a leading think tank in the UK has warned that the new round of austerity measures demanded by its international creditors will mean that the battered economy remains stuck in permanent depression – unless it receives substantial debt relief.

The National Institute of Economic and Social Research estimates that a haircut of 55% on Greek debt is needed to give the country a chance of reducing its debt to 120% of GDP by 2020. It warned that continuing to insist on “unrealistic fiscal targets” will ensure that the Greek economy will “remain in depression”.

It said the VAT increases reluctantly accepted by Athens in exchange for a new bailout will lead to a 1% fall in national output next year.

The Greek economy is expected to contract sharply again, with GDP falling 3% in 2015. Our latest analysis on Greece: http://t.co/aAsoN8p6Lz

— NIESR (@NIESRorg) August 5, 2015

Updated

Ex-BOE's Bean: UK's official statistics out of date

Sir Charlie Bean, former deputy governor of the Bank of England launches his official review into Britain’s official economic statistics on Wednesday. He told the Financial Times (£) that the “Big Data” revolution on the internet has rendered Britain’s stats out of date.

Bean noted that the framework for for the national accounts “was developed in the aftermath of the Great Depression”.

As an economy develops, the traditional ways of thinking about it cease to be so relevant,”

he said, expressing concerns that official numbers are struggling to keep up with the internet age where consumers, for example, book their holidays online, bypassing travel companies.

Back in the 1970s the UK was “probably the world leader in statistics”, he added, but it is not “quite the leader of the pack now”.

The BOE’s former chief economist was last month appointed to lead a root-and-branch review of the UK’s economic statistics.

Updated

The pound is also in focus again, ahead of Super Thursday – the Bank of England’s big day when for the first time it will announce interest rates and release the minutes of its policy meeting at the same time. On top of this, the central bank will release its inflation report with the latest growth and inflation projections.

Angus Campbell, senior analyst at FxPro Daily, has looked at the interest rate outlook in the UK and US and the impact on the pound:

This wealth of data could overwhelm investors and we are likely to see some volatility following the release, where the market is expecting the first votes for a hike from at least a couple of monetary policy committee members since the hawks were last calling for the base rate to rise last year.

What has been made clear by both the Federal Reserve’s Janet Yellen and the BOE’s Mark Carney is that rates are going to move upwards soon. For the BOE the challenge is to determine whether, at a time of very low inflation, wage growth is robust enough to warrant the commencement of rises later this year or early next year, especially at a time when recent data has been indicating the economy is coming off the boil. This week alone has seen unimpressive PMI surveys for the UK and this morning sees the important services PMI release which is expected to dip from 58.5 to 58.0. Anything lower than 58.0 could put sterling under pressure.

For the US the debate is not indifferent with the Fed’s voting member Lockhart overnight calling for the start of rate hikes in September, but the market is expecting later in the year and we have two important nonfarm payrolls releases ahead of then, the first being on Friday. Today sees the ADP payroll expected to come in at 215k so anything better could see the dollar add to its overnight gains following the comments from Lockhart.

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

We’ve woken up to news that China’s services sector expanded at its fastest pace in 11 months in July, offsetting some of the pressure from a faltering manufacturing industry.

The Caixin/Markit purchasing managers’ index (PMI) climbed to 53.8 from 51.8 in June, marking the 12th consecutive month of expansion. A reading above 50 indicates expansion while one below points to contraction. This is a private survey; China’s official services PMI released at the weekend showed a slight pick-up in activity in July.

All eyes are now on services PMIs for the eurozone and the UK, out later this morning. Britain’s manufacturing and construction surveys were mixed, with manufacturing improving slightly while construction saw a surprise slowdown due to housing.

European markets are set to open slightly higher following their mixed performance on Tuesday. The Athens stock market closed down 1.2%, the day after its 16.2% record fall when it reopened after a five week halt in trading. But banking shares took another hammering, falling close to 30% again.

The US dollar was lifted on Tuesday by some hawkish comments from FOMC voting member and Atlanta Fed president Dennis Lockhart, who said there would need to be a “significant deterioration” in economic activity to hold the Fed back from raising rates in September.

In light of the comments, investors will be focused on the latest economic data with the private ADP jobs report for July (ahead of non-farm payrolls on Friday), the June trade figures, and the ISM services survey for July.