Closing summary

That’s all for tonight. A quick reminder of the main events....

In a dramatic start to his tenure in office, Greece’s new prime minister, Alexis Tsipras, has begun unpicking the deeply unpopular austerity policies underpinning the debt-stricken country’s bailout programme.

After storming to power on Sunday, the leftwinger said there was no time to waste. “We will continue with our plan,” he told his first cabinet meeting on Wednesday. “We don’t have the right to disappoint our voters.”

Full story: Alexis Tsipras begins rolling back Greek austerity policies

In another busy day in Greece, finance minister Yanis Varoufakis vowed to end the mistakes of the past, help reboot Europe’s economy, and rehire the sacked cleaners whose struggle symbolises the public battle against Greece’s bailout terms.

Blogpost: Helena Smith: Unforgettable scenes at finance ministry

Other ministers also began unpicking the Age of Austerity, freezing plans to privatise state assets.

Our earlier summary has full details

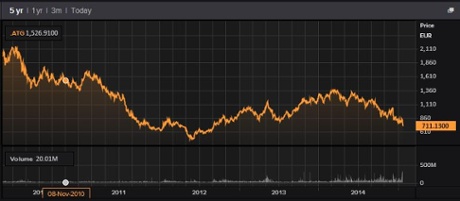

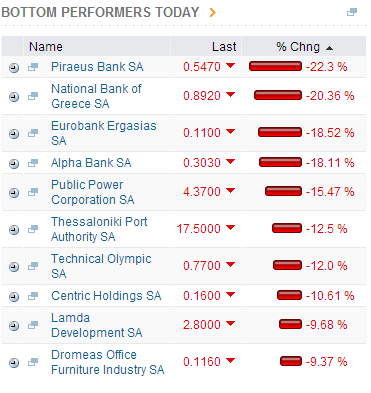

Greece’s stock market tumbled, with its banks suffering their worst day ever. Financial stocks slumped by a third, raising fears that they might be nationalised.

Blogpost: Black day for Greek stock markets

And tonight, Standard & Poor’s took the first step towards cutting Greece’s credit rating further into junk territory. It warned that Greece’s credit-worthiness was at risk, and flagged up the danger of a bank run....

We’ll be back tomorrow. Thanks for reading, and for all the comments. GW

The most important line in S&P’s statement on Greece is its comment about savers taking out their money from their banks....

S&P "views recent accelerated pace of deposit withdrawals from Greek banks as a credit concern." Word.

— Katie Martin (@katie_martin_FX) January 28, 2015

Brutal day for Greek banks. Again. More than a whiff of the crisis days. http://t.co/t55Nu8JI5K pic.twitter.com/wNKDsEvBb0

— Robin Wigglesworth (@RobinWigg) January 28, 2015

Reuters is helpfully snapping the key points from S&P’s statement on Greece, released a couple of minutes ago:

- S&P REVISES GREECE SOVEREIGN CREDIT OUTLOOK TO CREDITWATCH NEGATIVE FROM STABLE; CURRENT RATING IS B

- S&P SAYS IF NEW GREECE GOVT FAILS TO STRIKE AGREEMENT WITH OFFICIAL CREDITORS FOR FINANCIAL SUPPORT, THIS WOULD WEAKEN GREECE’S FUNDING POSITION

- S&P SAYS COULD LOWER GREECE’S RATINGS IF NEGOTIATIONS WITH THE EU, EUROPEAN CENTRAL BANK, AND INTERNATIONAL MONETARY FUND STALL

- S&P - “IF NEW GREEK GOVERNMENT FAILS TO AGREE WITH OFFICIAL CREDITORS ON FURTHER FINANCIAL SUPPORT, WOULD FURTHER WEAKEN GREECE’S CREDITWORTHINESS”

- S&P-GREECE’S RATING REFLECTS SOME OF ECONOMIC,BUDGETARY POLICIES ADVOCATED BY NEWLY ELECTED GOVERNMENT INCOMPATIBLE WITH POLICY FRAMEWORK AGREED

- S&P - “VIEW RECENT ACCELERATED PACE OF DEPOSIT WITHDRAWALS FROM GREEK BANKS,CONCOMITANT INCREASE IN ECB FINANCING TO THE BANKS, AS A CREDIT CONCERN”

Updated

S&P cuts Greece's credit rating outlook

Late news.... Standard & Poor’s has just threatened to cut Greece’s credit rating.

S&P has revised the outlook on Greece’s B rating to creditwatch negative, from stable. That’s the first step towards a formal downgrade.

S&P changes Greek sovereign rating outlook to 'watch negative' from 'stable', maintains rating at 'B'

— RANsquawk (@RANsquawk) January 28, 2015

Finance ministry cleaning ladies rehired and banking index down 26.7%: they may end up cleaning the nationalised banks too #Greece

— wolf piccoli (@wolfpiccoli) January 28, 2015

Could Greece’s banks be nationalised?! Renaissance Capital’s Charles Robertsons reckons it’s possible, if relations between Athens and its lenders flounder.

On Monday I was called gloomy for suggesting Greek banks may be nationalised MT @EfiEfthimiou: since Monday banks have lost more than 43%

— Charlie Robertson (@RencapMan) January 28, 2015

Black day for Greek stock market

Today’s plunge sent the Greek stock market down to its slowest level since September 2012.

That means it has lost all the gains since Mario Draghi vowed to do whatever it takes to save the euro.

Turnover was brisk, as investors raced to sell stocks, driving the banking sector down by a shocking 30%. That’s the biggest selloff in their history, according to the FT.

Piraeus, the country’s largest bank by assets, has now halved in value in the last month.

They can extend Greek bailout loans for 50 years, 100 years, whatever. The bond that matters most is held by ECB and comes due in July

— Charles Forelle (@charlesforelle) January 28, 2015

In case you missed it, here’s our profile of Greece’s new finance minister -- the “accidental economist” who’s unlikely to back down in a row with lenders:

Yanis Varoufakis: maverick economist with Greece’s fate in his hands

Greek media are reporting that Alexis Tsipras will meet with his economics ministers shortly. They’ll discuss strategies ahead of Eurogroup head Jeroen Dijsselbloom’s visit on Friday.

#Greek FinMin says cleaning ladies will be rehired at the Finance Ministry

— Nektaria Stamouli (@nstamouli) January 28, 2015

Just in: Athens stock market has plunged by over 9%, and the banking sector has seen a quarter of its value wiped out. That’s an extraordinary selloff.

#Greece Athens stock exchange ends -9.24%, banks -26.67% (since Monday banks have lost more than 43%)

— Efthimia Efthimiou (@EfiEfthimiou) January 28, 2015

Summary: Greek government takes aim at austerity

Greece’s new anti-austerity government has got down to work, and started to unpick the austerity programme that drove the country deep into recession.

In another action-packed day in Athens, ministers have been racing to unwind the actions of their ousted predecessors.....and shares have been tumbling on the local stock exchange.

1) Prime minister Alexis Tsipras told his ministers that they must not let voters down. At their first cabinet meeting, he declared:

We are coming in to radically change the way that policies and administration are conducted in this country.”

Tsipras insisted that Greece must renegotiate debt relief, but vowed to avoid a destructive clash with lenders. Photos are here.

2) Finance minister Yanis Varoufakis also pledged to end the mistakes of the past. At a dramatic press conference, he vowed to end austerity, and rehire sacked cleaners -- paid for by paying for fewer consultants.

3) The day began with ministers announcing that they were halting plans to sell stakes in Greece’s biggest port, and its main electricity provider. Both sales were demanded by the Troika.

Roll-back time in #Greece: new ministers queuing to announce the reversal and cancellation of measures approved under the MoU

— wolf piccoli (@wolfpiccoli) January 28, 2015

4) Greek bank stocks have slumped in value today, with some tumbling by a third of their value. Greek bonds have also been hit, driving up their yields painfully high.

Last one on Greek bank stocks for now - they're having their worst day ever: pic.twitter.com/5PKMRiwRSq

— Jamie McGeever (@ReutersJamie) January 28, 2015

The main Athens market is down over 9% in late trading

5) Analysts predict a fierce battle between Athens and its lenders. Berenberg bank suggests there is a 35% chance that Greece will quit the eurozone.

Updated

The sacked finance ministry cleaners are delighted to have won their jobs back (as finance minister Varoufakis pledged at his handover ceremony) .

Helena Smith reports:

Katerina Capodistrias, one of the dozens who have daily camped outside the finance ministry to press demands for reinstatement.

“Yanis Varoufakis is a star, a great economist and even better from Crete. We love him...He’s the best choice for the post of finance minister.”

Despoina Kostopoulou, the cleaners’ unofficial spokeswoman, said as far as she knew ALL of the cleaners would be rehired. “We are ecstatic,” she told me.

“We are now just waiting for the decision to be made, officially. We want to see it, and our names in it, with our own eyes. This is out 268th day outside the ministry but we have spent over a year and a half protesting on the streets. I expect that we will be here in the tents for a couple more days.”

Updated

Helena Smith: Unforgettable scenes at finance ministry

Yanis Varoufakis’s first ever press conference at the finance minister was quite an event.

Our correspondent Helena Smith reports:

As hand-overs of government posts go, today’s at the finance ministry will remain indelible in the minds of those who were there. Pained, raucous and joyful (with lots of spontaneous applause), it brought home in every way that this was a changing of guard – a turning not of the page but a book – in the country at the centre of the debt crisis.

Out went the old era and in came the new, the besuited Gikas Hardouvelis looking both relieved and alarmed as he passed the chair to Yanis Varoufakis, his successor in trendy jacket and open-necked shirt. “I sincerely wish the [new] government well,” said Hardouvelis, eyes fixed firmly ahead, adding;

“Greece doesn’t have the luxury of waiting to June to conclude the review of its programme with our partners.”

And then Varoufakis was off, rocking and rolling his way through Hardouvelis’ script, demolishing the philosophy of a government that had, he said, thrown Greece into a self-perpetuating economic death spiral as a result of “the huge toxic mistake that had been made in this very building.”

Greece had no intention of clashing with its creditors but the logic of austerity was such that policies conducted in its embrace could only fail. “You don’t need to be an economist to see that,” he said as some of those in the room (ministry staff perhaps?) began to clap.

“Today the denial of the problem is over, we are determined to change the logic [behind] the problem.”

At some point Hardouvelis, slumped in his chair, his deputy Christos Staikouras seated to his right, and now looking anything but happy, began to drum his fingers. An expression of disbelief flashed across his face as Varoufakis, all guns blazing, declared that

- the ministry would clamp down on expensive advisers and re-hire the cleaners that had become the face of austerity’s injustice (much applause there) (and outside)

- that it would seek a Pan European New Deal to “reboot” the economies not only of Greece but the continent at large,

- that under the radical leftists Athens would build a relationship “of friendship and sincerity” with Europe.

And then it was over. Varoufakis, hugging Hardouvelis and kissing him on both cheeks (to Hardouvelis’s somewhat dazed amazement) was out of his chair and off to begin “the hard work .” HS

Updated

Another symbolic moment: The railings that have “protected” Greek MPs from the public are being removed today, reports Yannis Karagiorgas of Euronews.

No more railings outside the Greek Parliament @euronewsgr @euronews http://t.co/yNZgXVLWvb pic.twitter.com/dDx5M8ZIG3

— Yannis Karagiorgas (@IKaragiorgas) January 28, 2015

Updated

Photo of the day?

It’s the cleaning staff who lost their jobs at the Greek finance ministry as part of its austerity programme -- they applauded as they watched Yanis Varoufakis announce they would be rehired.

Such a relief to see then smiling, after many months of tireless protests

Updated

The rout is turning into a crash:

Greek Banking stocks having their worst day ever. National Bank Of Greece (-28%), Eurobank (-22%), Alpha Bank (-22%), Piraeus Bank (-28%)

— Guy Harding (@GuyHardingSky) January 28, 2015

Alexis Tsipras has spooked the Athens market, and holders of Greek bonds, by his early moves as PM, says Felix Herrmann, a market strategist at DZ Bank.

Herrmann told Reuters:

Tsipras has announced his new cabinet and his new finance minister seems to be a rough guy from the very far left of the political spectrum,”

“This is raising fears that there’s a clash coming up between Athens and its lenders. The fact that he joined a coalition with the far right is not helping either.”

That’s the Independent Greeks, with whom Syriza have virtually no common ground apart from their shared determination to end the current Greek bailout terms.

Updated

Over in Berlin, Angela Merkel’s spokesman has told reporters that the chancellor expects to hear Greece’s new economic strategy soon.....

....and despite the new Greek government’s pledge to renegotiate its debts, Germany expects (or hopes?) Greece will stick to its obligations.

Steffen Seibert said:

“I expect, as do all European partners, that the new Greek government will present its overarching economic and financial strategy imminently, and its clear ideas on how things proceed regarding the continuation of the current programme and how to fulfil Greece’s obligations,”

“It will then be for European partners to discuss matters on the basis of these concrete suggestions,”

Updated

Varoufakis pledged to re-hire ministry cleaners, iconically protesting since Sep. 2013 http://t.co/AaQyXqdbEF pic.twitter.com/IvVemd6CRB

— reported.ly (@reportedly) January 28, 2015

Back to finance minister Yanis Varoufakis’s press conference... and he reveals he’s going to visit his counterparts in France (Michel Sapin) and Italy (Pier Carlo Padoan) soon.

No mention of a trip to Berlin, though.....

But not Schauble? Strategic mistake? MT @ManosGiakoumis: #Greece FinMin @yanisvaroufakis to meet #France & #Italy FinMins in coming days

— Peter Spiegel (@SpiegelPeter) January 28, 2015

The Athens stock market may be falling out of bed, but outside life continues as normal, reports crisis-watcher @teacherdude .

BTW the sky hasn't fallen in, Greeks going about their business same as usual

— Teacher Dude (@teacherdude) January 28, 2015

Greek cleaners to be rehired!

Varoufakis says that he is planning to cut costs at the finance ministry by cutting the number of advisers.

And he’s also planning to rehire the ministry cleaners who have been fighting a legal battle since they lost their jobs. Those ladies came to symbolise Greece’s battle against its creditors, spending months protesting outside government buildings.

#Varoufakis will immediately reinstate sacked cleaners at Ministry of Finance. #Greece

— Andrew McC Crawford (@andymccc) January 28, 2015

Varoufakis also said there'll be less consultants in finance ministry to rehire sacked cleaners #Greece

— Loukia Gyftopoulou (@loukia_g) January 28, 2015

Finance minister Varoufakis insists that Greece will seek a new deal with its creditors.....

Greek Fin Min: Creditors Gave More Money Than They Ought, But It Has Been Thrown Into a Black Hole

— Katie Martin (@katie_martin_FX) January 28, 2015

Finance minister Varoufakis gives press conference

Breaking: Greece’s new finance minister, Yanis Varoufakis, is giving a press conference in the finance ministry.

Varoufakis is saying that Greece is “turning a page on the mistake of the bailout”.

He also reveals that he’s spoken to Jeroen Dijsselbloom, who hopes to find some common ground

- GREEK FINANCE MINISTER VAROUFAKIS SAYS TOLD EUROGROUP CHIEF WANTED A NEW AGREEMENT WITH LENDERS THAT EXITS BAILOUT LOGIC

- GREEK FINANCE MINISTER VAROUFAKIS SAYS WAS TOLD BY EUROGROUP CHIEF THAT COMMON GROUND CAN BE FOUND THROUGH DIALOGUE

He’s sitting alongside the former finance minister, Gikas Hardouvelis, who has warned that Greece faces “acute financing needs in March”.

Passation de pouvoir Hardouvelis/Varoufakis au ministère des Finances grec. Devinez qui est qui #Grece pic.twitter.com/kV81nbtuLU

— Odile Duperry (@oduperry) January 28, 2015

Yanis Varoufakis, the new Greek finance minister, in defiant mood. Not about austerity this time, but his blog.

Writing in his personal blog, he vowed to continue posting his thoughts, defying those who consider it “irresponsible for a finance minister to indulge in such crass forms of communication”.

Varoufakis conceded that his blog posts would be more infrequent and shorter from now on, but that he hoped to compensate his readers with juicier insights and comments.

He wrote:

For hope to be revived we must all strive to change the ways of a dismal past. Maintaining an open line with the outside world may be a small step in that direction.

So, keep watching this space!

AM

Greek shares continue to fall sharply, led by the banks.

#Greece Greek banks no-confidence vote is pretty clear... @LVDTA pic.twitter.com/Xc1UwkOMWy

— Lex van Dam (@lexvandam) January 28, 2015

Addressing his first cabinet meeting, Alexis Tsipras said the first priority of his government would be to address Greece’s humanitarian crisis.

The people demand we bleed in order to defend its dignity.

Reuters is reporting that Giorgos Katrougalos, alternate minister for administrative reform, said some planned public sector job cuts would not go ahead. Those cuts that are against the constitution and those that have not gone through any evaluation will be cancelled, he said.

New Greek PM Tsipras is right. He does need a haircut pic.twitter.com/B4bX7CkMtt

— RANsquawk (@RANsquawk) January 28, 2015

AM

Holger Schmieding, chief economist at German bank Berenberg has recently returned from Athens and is fired up over the situation in Greece.

Just back from Athens, I feel almost compelled to shout it from the rooftops: it’s not about the debt. it’s about the economy, stupid - to borrow a phrase from Bill Clinton.

In Athens, much of the discussions I had revolved around the debt: how much will Europe cut the burden now that Greek voters have asked for it? Or: wouldn’t it be cheaper for Europe to write off half its claims on Greece than to risk losing it all?

The new Greek government and its voters are in for a reality shock. The debate in Athens seems to suffer from four delusions.

My best bet remains that, facing reality, prime minister Tsipras will eventually get real. A patient Europe will offer face-saving compromises. As a wily and power-conscious operator, Tsipras could still do a Lula-style U-turn instead of ending up in history books as the prime minister who broke his country.

But it could be a close call. And it could well be a rough ride for Greece first before Syriza bows to reality. If worst came to worst in Athens, and I still believe it won’t come to that, Europe would rather cut its losses than fund the perennial basket case into which an overdose of populist policies could turn Greece. The risk of accidental Grexit is real. We put it at 35%, well below par but still serious.

Fortunately, Europe would have the defences it needs to contain the potential financial and economic contagion. The real issue to watch in Euope is the risk of political contagion. Will the likely clash between Syriza and reality deflate the allure of populists in Rome, Madrid and Paris or stoke the populist anger against the indignities of real life? We bet that reason will prevail despite the occasional hiccup.

AM

Updated

Shares are now being routed in Athens -- shares in its biggest banks, such as Piraeus and Eurobank, are down by around 20%.

Greek stocks -7% and counting pic.twitter.com/SUzan3SvOZ

— Jonathan Ferro (@FerroTV) January 28, 2015

Greek markets today. *high whistle* pic.twitter.com/cjU9v2DJLZ

— Katie Martin (@katie_martin_FX) January 28, 2015

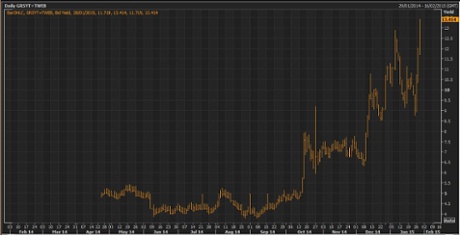

The five-year bond which Greece sold to investors last April, in its triumphant return to the markets, has hit its lowest ever level.

The yield on the debt (which moves inversely to the price) hit an all-time high of 13.5% this morning; showing a greater risk that Greece will default.

It’s remarkable to think that Greece was swamped with demand at that auction. It sold €3bn of debt, but received offers for €20bn. Investors clearly believed that the Greek debt crisis was over....

Alexis Tsipras’s determination to renegotiate Greece’s borrowings will alarm many in the eurozone, particularly the north.

But as HSBC’s well-respected chief economist, Stephen King, explains, it takes two to create a debt crisis:

It's amazing to think that creditors believe they are in no way responsible for the €zone crisis.

— Stephen King (@KingEconomist) January 28, 2015

1/2 Germans struggle to understand that a large BoP surplus means their savings are used to acquire foreign rather than domestic assets...

— Stephen King (@KingEconomist) January 28, 2015

(BOP=Balance of Payments)

2/2 ....and that those foreign assets may, at times, offer the wrong mix of risk & reward. Creditors and debtors two sides of same coin.

— Stephen King (@KingEconomist) January 28, 2015

Updated

And here’s finance minister Yanis Varoufakis attending the first cabinet meeting, where PM Tsipras warned the government faces a very difficult task.

Photos: Tsipras's first cabinet meeting

Greek bonds have weakened sharply since Greece froze its privatisation plans and vowed to seek debt relief.

That has driven up the yield, or interest rate, further into dangerous levels.

- GREEK 3-YEAR GOVT BOND YIELD RISES 183 BPS TO 16.03%, HIGHEST IN THREE WEEKS - TRADEWEB

- GREEK 10-YEAR GOVT BOND YIELD RISES 50 BPS TO 10.30% - TRADEWEB

- GREEK 5-YEAR GOVT BOND YIELD HITS RECORD HIGH OF 13.11% - TRADEWEB

Updated

Greek banking stocks have shed a third (!) of their value this week:

Update: Greek bank stocks not liking Syriza's victory, -32% so far this week, on for 2nd biggest weekly fall ever: pic.twitter.com/qSlURYFLao

— Jamie McGeever (@ReutersJamie) January 28, 2015

Alexis Tsipras then told his cabinet that the international mood towards Greece is changing.

He predicts positive talks with Jeroen Dijsselbloem, who heads up the eurogroup of finance ministers, in Athens on Friday.

And the prime minister reiterates that ministers must deliver on their pre-election pledges, declaring:

We must not disappoint the voters who gave us a mandate.

Updated

*GREEK GOVT SIGNALS BEGINNING OF NEW ERA, TSIPRAS SAYS

— Michael Hewson (@mhewson_CMC) January 28, 2015

Tsipras tells cabinet: We must negotiate debt relief

Alexis Tsipras has just held his first cabinet meeting in Athen, and details are hitting the wires now.

He told ministers that they face an extremely difficult task, with the people expecting radical changes from their government. He vowed to restore national sovereignty and dignity to Greece.

And the new prime minister insisted that he will push for a debt renegotiation deal, saying:

We are a government of national salvation. Our aim is to negotiate debt relief.

Tsipras also pledged not to pursue destructive clashes with creditors. And he told ministers that they must tackle unemployment, and seek “balanced budgets” but not unrealistic surpluses.

And he vowed to fight vested interests and end “clientelism” in Greek society; we are responsible only to the people.

(quotes via Reuters)

"This gov't has no other dependencies or bosses than the people," Greek PM Tsipras tells his cabinet in its first meeting #Greece

— Nick Malkoutzis (@NickMalkoutzis) January 28, 2015

Oh. Tsipras already lowering expectations... *TSIPRAS: GREEKS DON'T EXPECT TO CHANGE ECONOMY IN ONE DAY

— Joseph Weisenthal (@TheStalwart) January 28, 2015

Economist Megan Greene of Manulife Asset Management (a eurozone-crisis expert) says Tsipras’s government is ready for a fight with its lenders:

All indications so far (coalition w Indy Greeks, Varoufakis as finmin) point to new Greek govt going into talks w the troika w guns blazing.

— Megan Greene (@economistmeg) January 28, 2015

The sell-off is accelerating:

#Greece Athens stock exchange -3.81%, Banks -10%, PPC -7.74, OLP -8.9%

— Efthimia Efthimiou (@EfiEfthimiou) January 28, 2015

Greece’s new foreign minister, Nikos Kotzias, has insisted this morning that Athens still wants to play a full part in European affairs.

#Greece ForMin:Anyone who thinks that in the name of the debt, Gr will resign its sovereignty &its active counsel in EU politics is mistaken

— Efthimia Efthimiou (@EfiEfthimiou) January 28, 2015

Greek bank shares are also falling again, sending the main ATG index into the red for the third day running.

Updated

Shares in PPC and Piraeus Port tumble

Shares in energy firm PCC and Piraeus Port have both tumbled by around 7% at the start of trading in Athens, after the government halted plans to sell its majority stake in both firms.

- GREEK ATG STOCK INDEX FALLS 0.8% AT OPEN

- GREEK BANKING SECTOR INDEX FALLS 3.7%

- SHARES IN GREEK UTILITY PPC FALL 7.2% AFTER GOVT PLANS TO FREEZE PRIVATISATION PROCESS

- SHARES IN PIRAEUS PORT FALL 6.6% AFTER GOVT PLANS TO STOP PLANNED SALE OF 67% STAKE IN COMPANY

Syriza is also planning to help poorer Greeks by raising the minimum wage:

New Greek gov't has crossed off Piraeus port & energy privatisations. SYRIZA wants raising of minimum wage to be 1st bill #Greece

— Nick Malkoutzis (@NickMalkoutzis) January 28, 2015

Greece’s lenders had forced the previous government to cut wages to boost competitiveness, one factor that has driven so many people into poverty. Devaluation, that traditional way of making a country more competitive - and lowering the real value of its debt - was obviously not an option in the eurozone.

Germany’s biggest newspaper isn’t showing much sympathy for a Greek debt deal, flags up ING analyst Carsten Brzeski:

Asking for the Grexit by accident? This morning's Bild lists earlier German statements ruling out debt forgiveness for Greece.

— Carsten Brzeski (@carstenbrzeski) January 28, 2015

European stock markets have inched higher, despite events in Greece.

The FTSE 100 has gained18 points or 0.3% in early trading to 6830. Investors are cheered by Apple, which smashed profit forecasts last night.

They’re also waiting for the Federal Reserve’s monthly statement on monetary policy, due at 7pm tonight, which will show how close it is to raising interest rates. Gerald Lyons, who advises the Mayor of London on economic policy, reckons the Fed can be wait....

FOMC policy statement today Patience the buzz But tightening via dollar strength & balance of external risks strengthen case for later hike.

— Gerard Lyons (@DrGerardLyons) January 28, 2015

The new Greek government has also pledged to reverse the unpopular ‘mobility scheme’ which was used to lay off thousands of public sector workers, rolling back another key bailout measure.

George Katrougkalos told Mega TV:

“It will be one of the first pieces of legislation that I will bring in as a minister.”

Day 1, potential major stand-offs: privatisations(Piraeus Port, Public Power Co.), public sector layoffs/re-hires, Russia sanctions #Greece

— Yiannis Mouzakis (@YiannisMouzakis) January 28, 2015

Greek government halts privatisations

Good morning, and welcome to our rolling coverage of the financial markets, the world economy, business and the eurozone.

Greece’s new anti-austerity government is making a dramatic start today, starting to unravel key parts of the country’s bailout deal.

Alexis Tsipras’s administration is making good on the promises it made during the campaign, just hours after being sworn in.

Energy minister Panagiotis Lafazanis has announced this morning that he will freeze plans to privatise the country’s dominant power utility PPC (in which the government holds a majority stake).

Lafazanis told Greek TV that:

“We will halt immediately any privatisation of PPC.”

#Greece Productive Reconstruction Min Lafazanis said PPC will 'return to the state', its privatisation will be halted imminently. #economy

— Manos Giakoumis (@ManosGiakoumis) January 28, 2015

Greece’s lenders had forced the country to liberalise its energy market, as a condition of its €240bn bailout.

Tsipras’s government has also pulled the plug on the sale of a stake in the country’s largest port.

Reuters has the story:

One of the first decisions announced by the new government was stopping the planned sale of a 67% stake in the Piraeus Port Authority, agreed under its international bailout deal for which China’s Cosco Group and four other suitors had been shortlisted.

“The Cosco deal will be reviewed to the benefit of the Greek people,” Thodoris Dritsas, the deputy minister in charge of the shipping portfolio, told Reuters.

Tsipras is clearly waving a few red rags (or possibly red flags?) at Brussels and the IMF; an early skirmish in the battle over Greece’s debts.

And that’s before the radical finance minister,Yanis Varoufakis, gets to work. He’ll receive the keys to the finance ministry at 2pm local time (noon GMT).

Handover ceremony at Finance Ministry to take place tomorrow at 2 p.m. #Greece

— Kathimerini English (@ekathimerini) January 27, 2015

We’ll be tracking all the key events in Greece, and beyond, though the day.

Updated