And that’s all for tonight, after a day that began with the EU and creditors blaming each other for the collapse of talks last night...

....followed by Tsipsas’s claim that lenders were driven by “”political purposefulness” after years of looting....

....which preceded Mario Draghi calling for a deal very soon...

...and reports of big withdrawals at Greek banks....

...and ended up with those (denied) reports that capital controls could be forced on Greece this weekend.

All punctuated by heavy losses on the stock markets.

I’m be back on Tuesday morning for another day of drama. Thanks, as ever, for reading and commenting. Goodnight! GW

Alexis Tsipras’s pledge early this morning to resist any more looting by its creditors makes the front page of tomorrow’s FT:

Tuesday's FT: Tsipras vows to resist ‘pillaging’ of Greece in blow to deal prospects #tomorrowspaperstoday #bbcpapers pic.twitter.com/ofr4zdZ5Kh

— Nick Sutton (@suttonnick) June 15, 2015

The Daily Telegraph reports that Greece could potentially ask the European Court of Justice to protect it.....

Germany’s Suddeutsche Zeitung reported that the creditors are drawing an ultimatum to the Greeks, threatening to cut off Greek access to the European payments system and forcing capital controls on the country as soon as this weekend. The plan would lead to the temporary closure of the banks, followed by a rationing of cash withdrawals.

Syriza sources have told the Telegraph that Greece may seek an injunction from the European Court of Justice to stop the creditors and the EU institutions acting in a way that breaches Greek treaty rights. This would be an unprecedented move, greatly complicating the picture.

Syriza sources tell @AmbroseEP Greece may seek ECJ injunction to stop EU institutions breaching treaty rights http://t.co/rfllExsN9s

— Mehreen (@MehreenKhn) June 15, 2015

The FT has a rather unsympathetic quote from one of Greece’s creditors tonight:

According to a copy of Greece’s counter-proposal presented to Mr Juncker’s staff at the weekend and obtained by the FT, Athens agreed to meet the creditors’ demands on budget surplus targets for this year and next year. For 2015, Athens said it would reach a primary budget surplus of 1 per cent and 2 per cent in 2016 — something the Greek government has resisted for nearly two weeks.

But officials representing Greek creditors said many of the underlying fiscal measures — particularly the €2.4bn in savings attributed to “administrative measures” — were unlikely to be met, making the promise to achieve surplus levels meaningless.

“It’s like you saying you promise to lose 20 kilos by next June, but you keep eating the same amount of chocolate,” said one senior official from one of Greece’s bailout monitors.

A spokesman for the German government has said he could not confirm or deny Süddeutsche’s claim that eurozone governments are considering pushing Greece to implement capital controls, if there’s no deal by the weekend.

A Greek official has apparently denied that it could be bounced into implementing capital controls this weekend.

Traders chasing this headline now // GREEK GOVT OFFICIAL DENIES GERMAN REPORT ON PLAN FOR GREECE TO IMPOSE CAPITAL CONTROLS THIS WEEKEND

— Matt Weller, CMT (@MWellerFX) June 15, 2015

A majority of Greeks blame creditors, not their leaders, for the long deadlock - according to a new poll just released.

#Greece GPO/@AnatropiMegaTV poll: Who bears responsibility for prolonged talks? · 56.3% creditors · 37.4% the Greek gov't

— Yannis Koutsomitis (@YanniKouts) June 15, 2015

Top officials in Athens have roundly rejected claims made by EU officials that the Greek government agreed to measures which it then rowed back on, triggering the collapse in talks on Sunday.

The version of events leaked by insiders close to EU commissioner, Jean-Claude Juncker, was not only misleading but very “economical with the truth,” a government source told the Guardian.

“What we said at a dinner [attended by] Juncker last week was that if the whole agreement, the package of reforms, was economically viable we, in turn, could move towards their fiscal targets for 2015 and 2016,” said the official insisting that the leftist-led government never agreed to specifics such as how such targets would be met.

“We never agreed to any of their baseline scenarios, or what would be done, or that we would reduce pensions and to leak that is very misleading,” he added.

“Yes, reports that we were late by an hour are true but the rest is being very economical with the truth.”

Government insiders refused to be drawn on when negotiations would resume saying: “we don’t know when that will happen.”

“It is up to our European partners to decide whether, after six years of recession, the priority should be a strong reform programme to counter tax evasion, the power of the elites and the failings of the Greek public administration or yet more recessionary measures, yet more cuts in pensions and real wages,” said one insider.

“It is also time for a decision whether Europe can encompass a government and people that have set social and economic priorities somewhat different from the mainstream.”

The time had come, he said, to see whether pluralism, fairness and democracy “are still European values worth preserving.”

Süddeutsche: EU draws up emergency plan

German newspaper Süddeutsche Zeitung is reporting tonight that European leaders are drawing up an emergency plan for Greece, including capital controls.

They would be implemented, it claims, if a Greek deal was not agreed by the weekend.

This would effectively be an ultimatum to Greece to accept creditors demands....

Süddeutsche reports the #EU has decided on an emergency plan for #Greece: ultimatum, capital contrls & the full monty http://t.co/E9QKdS7V0E

— Yannis Koutsomitis (@YanniKouts) June 15, 2015

Updated

Evening summary: Draghi urges deal, but both sides still divided

Time for another recap of this afternoon’s developments.

Brussels insiders have revealed that Greece’s latest proposals were rebuffed on Sunday night without even being considered by its creditors, in a sign of how relations have deteriorated.

Our Brussels editor Ian Traynor has learned that a team from the creditors spent all weekend waiting in vain for a proposal that was worth considering in detail.

In the end, by Sunday evening, said Brussels officials, the talks were not only stalemated or at an impasse, but had actually suffered a reversal, with the Greeks trying to re-open issues that both sides had already agreed.

#grexit greece and eu in breakthrough agreement! both sides say that in w/e negotiations in bxl, no negotiations took place

— Ian Traynor (@traynorbrussels) June 15, 2015

The collapse of talks prompted Greek savers to withdraw funds from their bank accounts again today; €400m was taken out, according to insiders.

Mario Draghi, head of the European Central Bank, has urged both sides to work towards a strong agreement, which is now needed very soon.

Testifying at the European Parliament, he told MEPs that:

We need a strong, and comprehensive agreement with Greece. And we need it very soon....

While all actors will now need to go the extra mile, the ball lies squarely in the camp of the Greek government to take the necessary steps”

The Greek government, though, said it is waiting for an invitation from creditors, as both sides become entrenched.

In a sometimes tetchy hearing, Draghi told MEPs that the ECB will keep providing funding for Greece’s banks as long as they are solvent. He also rejected claims that the ECN is letting Greece down, pointing out that it has provided around €118bn of liquidity support.

Draghi warned that a Greek default would be ‘uncharted waters’.

And he also flagged up that Greece’s institutions are concerned about its funding needs once its current bailout ends (one way or another). Member states must tackle this issue, he warned, in a signal to Europe’s leaders to face reality.

The crisis sent shares down across Europe today, driving the London market to a three month low.

Back in Greece tonight, social security minister Dimitris Stratoulis says the cuts being demanded of Greece in pensions amount to €1.8bn -- the equivalent of a 20% drop in earnings for pensioners (our own Helena Smith reports)

Stratoulis, a Syriza hardliner, added:

“They are also demanding €1.8bn in revenues from increasing VAT. These measures are measures of annihilation and will lead to the enslavement of the Greek people. They are unacceptable and therefore to be rejected.”

“There are no high pensions. Pensions have already been cut by 50%, a new reduction would leader to even greater recession.”

And for a deeper understanding of the issue, check out this post by our data blog, Alberto Nardelli:

Updated

Video: Here’s a few highlights from Mario Draghi’s appearance at Europe’s Economic and Monetary Affairs Committee:

Although Mario Draghi made some interesting points to MEPs, he “failed to ignite much hope in the Eurozone this afternoon” about Greece.

So says Connor Campbell, financial analyst at Spreadex.com:

Stating that the region needs a ‘strong deal’, Draghi failed to clarify how much progress has been made on such a solution, likely because there hasn’t been any, whilst also refusing to speculate on the consequences of any potential Greek ECB repayment failures.

The DAX has now effectively lost all of the ground it had made back across last Wednesday and Thursday, and looks like it could return to the 4 month lows it saw last Tuesday, especially with what is looking like it will be another damp squib of a Eurogroup meeting on the 18th.

That photo of the “Come home drachma, all is forgiven” sign has prompted our correspondent, Helena Smith, to send another photo of the same patch of graffiti.

It shows Tom, the resident Irishman of Plaka (the district beneath the ancient Acropolis), who painted the billboards standing with a can of local Greek brew: fix beer.

Helena, who also lives in Plaka, explains:

Tom, who is perhaps the most colourful character in Plaka - where he has lived for decades - believes he has come up with the best solution yet for Greece. “We all need to drink Fix beer to fix it,” he tells passersby (of which there are many).

The Irishman regularly paints the billboards that enclose the property on which he lives. The pithy observations accompanying his artwork often snapped by the gang of professional photographers who now roam the streets of Athens.

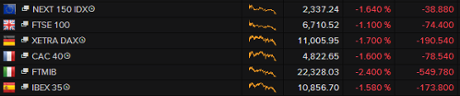

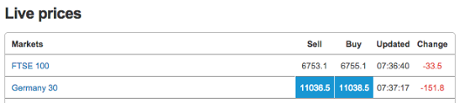

A bad day in Europe’s stock markets has ended with the FTSE 100 hitting its lowest level in over three months.

Greek woes push FTSE 100 down 1.1% to 6710, lowest close since 10 March

— Nick Fletcher (@nickfletchergdn) June 15, 2015

And London got off pretty lightly compared to the rest of Europe - the Italian FTSE MIB slid almost 2.5%.

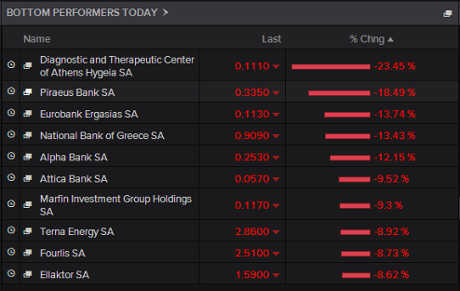

And in Greece, the Athens market finished the day down 4.6%, with Piraeus Bank tumbling 12%.

Mario Draghi concludes his appearance at the European Parliament’s Economic and Monetary Affairs committee by reiterating that Europe needs a Greek deal very soon.

Both parties are now being called to their capacity to find a compromise that yields...a strong agreement that generates growth with social fairness, with fiscal sustainability and addresses some potential financial stability issues.

And lets not forget my earlier point to Mr Weizsäcker (about Greece’s future funding needs), the ECB president adds.

We need two elements. One that concerns the substance of the policy agreement, and one that addresses the financing issues.

And that’s the end of the hearing. The committee chair says he hopes everyone will heeds Draghi’s wise words.

Draghi smiles modestly (ish).

Draghi: gender equality can boost eurozone economies

Back to Brussels, where Mario Draghi is being asked whether more gender equality would help the eurozone economy.

I completely, totally, agree with you, Draghi replies

All evidence shows that where we have gender equality objectives, productivity is higher, labour participation is higher, aggregate demand is higher.

EU committee on econ affairs grilling of Draghi closes with Q on whether more gender equality would resolve Eurozone woes. Draghi agrees

— Axel Merk (@AxelMerk) June 15, 2015

This may not fall under a central bank governor’s remit, he muses, but sometimes a central banker has to take a wider view.

Between 2000 and 2005, he continues, the regulation on financial stability in some important jurisdictions was being destroyed.

Then, we were not thinking that financial stability would fall into the jurisdictions of central banks,

But with hindsight, wouldn’t it have been better for central banks in those jurisdictions to have spoken up about financial stability, Draghi asks.

So yes, on the issue of gender equality, Draghi “fully agrees that we should have it in mind when we consider structural reforms” and ways of stimulating the eurozone economy.

Reuters: €400m taken out of Greek banks today

Breaking away from Mario Draghi’s testimony (which is being streamed here). Reuters is reporting that Greek savers have taken out around €400m today.

Bankers said that the pace of withdrawals picked up from last week, after talks collapsed over the weekend, but it’s not a bank run.

One said:

“There is worry but the outflows were rather contained, not as bad as feared in the context of a bad climate after negotiations hit an impasse.

“For the system as a whole, Monday’s outflow is estimated at around 400 million euros.”

In April, Greek banks lost €4.9bn of deposits, or around €163m per day (or €220m excluding weekends).

Every withdrawal leaves Greece’s banks even more dependent on the ECB’s emergency liquidity support, and potentially needing a further injection this week.

Updated

Asked about European integration, Draghi says it’s more important to expend energy strengthening the eurozone rather than adding more members.

Draghi: Strengthening the monetary union is more urgent than enlarging it

— ECB (@ecb) June 15, 2015

Updated

Draghi: Institutions believe Greece needs further financing

Mario Draghi then makes an important point about the Greek crisis -- the International Monetary Fund believes that Greece needs further financing to cover its needs beyond June 30th (when the eurozone bailout expires).

And this view is shared by other institutions, he adds.

So the IMF cannot hand over its portion of Greece’s bailout loans, worth around €16bn over the next year, without some breakthrough on this issue.

Member states must give an answer.....It is not easy, but it is essential.

[The eurozone, though, says it won’t discuss a third bailout until the current programme is resolved].

German MEP Jakob von Weizsäcker asks Draghi what would happen if Greece fails to meet its repayments to creditors this summer? And what would it take to prompt the ECB to end the emergency liquidity it is providing?

I don’t want to speculate about possible missed payments, Draghi replies. We know from the Greek leaders that these comments will be made fully, and in a timely manner.

And on the ELA, Draghi confirms that it would take a two-thirds majority at the governing council to veto an extension of emergency liquidity.

Updated

Draghi: Our policy is best contribution we can make to reduction of inequality

— ECB (@ecb) June 15, 2015

Another MEP asks why the ECB is driving up asset prices by its QE scheme, thus helping the wealthy, but not doing more to help the poor in Greece.

Whether we like it or not, banks and markets exist and are the only way of transmitting monetary policy, Draghi replies.

And what’s the biggest cause of poverty? Unemployment. Are you suggesting we should raise interest rates now, Draghi asks, rhetorically.

And then he switches into Italian (his mother tongue, of course), to declare that the ECB is aware of the criticism over its polities, but it is doing its best.

And if we fails, at least we tried.

Another MEP asks Draghi why he won’t include Greece in his QE stimulus programme.

Why are you blackmailing Athens, at a time when millions are in poverty and many children cannot even access basic healthcare?

We are simply following the rules, Draghi replies. We are not a political player.

"You're trying to portray the @ECB as a political entity. We're not a political entity," says #Draghi. Hmmm.

— Peter Spiegel (@SpiegelPeter) June 15, 2015

And the rules state that:

- The ECB can’t buy the bonds of a eurozone government which is currently being reviewed by the International Monetary Fund

- It can’t buy bonds below a certain credit rating (and Greece’s ratings are only a few notches above default)

- There’s a limit to the share of any eurozone government’s debt the ECB can hold.

Updated

Dramatic scenes in Brussels!

Greek MEP Notis Marias challenges Draghi about the dire state of the Greek economy, and the unfolding humanitarian crisis. He wants the ECB to do more to help Greece, by assisting with its payments to the IMF.

The situation in the Greek is dramatic, Draghi agrees. But the ECB cannot undertake any monetary financing.

He then outlines that Greece has received €223bn of bilateral loans from Europe, plus the ECB’s liquidity support (€118bn so far), plus the IMF loans, plus the debt haircuts in 2012 (a 53.5% cut in the face value of €200m of debt).

I don’t want to overplay the significance of these numbers, but the responsibility does not lie only with the institutions who have provided this help.

At this point, Marias thumps the table and waves a document, which he claims shows Mario Draghi assisted with such financing when he was governor of the Bank of Italy.

Draghi says he’s not clear what this is about (me neither, sorry), but will discuss it afterwards.

You must read the law and not speculate on an answer, shoots back Marias.

Draghi getting shouted down by Greek MEP. Shakes his head despairingly like a man whose had enough of this

— Mehreen (@MehreenKhn) June 15, 2015

Draghi: Greek default would be 'uncharted waters'

MEPs are asking Draghi about how much contagion would be created in the eurozone if Greece doesn’t get a deal with its creditors and defaults.

I don’t think it’s productive to speculate about possible outcomes, Draghi replies.

We would be entering into “uncharted waters”, but he believes policymakers have all the tools to manage the situation.

Draghi: In case of default, "we will enter into uncharttered waters, we have all the tools to manage the situation at best" #Greece

— Jorge Valero (@europressos) June 15, 2015

It is quite clear that our union is an unfinished construction, he concludes. And we need a “quantum leap” to complete monetary union.

#Draghi: To conclude EMU, we need a quantum leap forward, we need to put our institutional structure on more solid basis

— Jarno Hartikainen (@JarnoHa) June 15, 2015

The Greek government doesn’t agree that the ball is in its court!

Alexis Tsipras’s office just released a statement, saying it is waiting to be invited back to the negotiating table:

“We are awaiting the invitation of the institutions and we will respond, at any time, to resume the negotiations.”

Draghi: We need a strong Greek deal, very soon

Mario Draghi now turns to Greece, and defends the European Central Bank’s handling of the crisis.

We will continue to take our decisions with full independence, he vows.

This rules-based approach is what is required from us. This is what we have been following, and will continue to follow.

Our current liquidity support now totally €118bn, says Draghi. That’s 66% of Greek GDP. The highest level of any eurozone country.

We will support Greek banks for as long as they are solvent, and have enough collateral.

But, we cannot raise the cap preventing Greek banks from buying more Greek government debt, until there are clear signs that the current ongoing review of its bailout will be successfully concluded (meaning the €7.2bn of bailout funds can be unlocked).

Draghi adds:

We need a strong, and comprehensive agreement with Greece. And we need it very soon.

Such a “strong” deal would generates growth, has social fairness, addresses competitiveness, and the remaining sources of financial instability.

And Draghi concludes that Greece must now take new steps to break the deadlock.

While all actors must go the extra mile, the ball lies firmly in the camp of the Greek government to take the necessary steps.

Updated

Mario Draghi turns to the impact ECB’s QE programme:

A large-scale asset purchase programme is “not without risks”, Draghi says, and we monitor them very closely.

In particular, we manage credit risks by only buying assets of sufficient quality.

And we also decided the government bond purchases will not be ‘risk-shared’ (ie, each central bank is on the hook for purchases of its own sovereign bonds).

We see financial stability risks as relatively contained right now, Draghi continues. There are no signs of overheating in the eurozone housing market.

And he then turns to the distributional impact of the QE’s huge stimulus package, acknowledging that it results in changes in asset prices, and wealth gains for investors.

(in other words, if you’re rich enough to own shares or bonds, you benefit)

But this lies at the heart of monetary policy. Interest rate changes always change the attractiveness of saving vs spending.

In the long run, stimulus will help everyone, including those who are relatively poor or out of work, he argues.

Draghi tells MEPs that the ECB won’t be panicked by the recent volatility in the bond markets.

We must keep a steady monetary course and firmly implement measures, including our asset purchase scheme, Draghi declares firmly, reiterating comments made at the ECB’s press conference earlier this month.

He reaffirms that the ECB will keep buying €60bn of assets each month until September 2016, and at any rate until inflation is back on target.

Updated

After apologising for being late (please don’t mention it, Mario), Draghi begins giving his statement to the committee:

The latest economic indicators and survey data broadly confirm that the economic recovery is proceeding, at a moderate rate, he says.

There are encouraging signs that private investment is picking up, he says, suggesting the recovery should broaden. Our monetary policy measures are working their way through to the real economy.

And he confirms that the ECB expects inflation to remain low for some months, before rising towards its targets close to, but below, 2%.

Mario Draghi will mainly be testifying on his new asset-purchase scheme, the QE programme which was announced in January.

But he will “certainly” give his view on the negotiations between Greece and its creditors, says the committee chairman, Roberto Gualtieri.

Gualtieri says that those talks have reached a critical point.

Mario Draghi testifies to European Parliament

#Draghi in the @EP_Economics house pic.twitter.com/0dVpN1GN9S

— Peter Spiegel (@SpiegelPeter) June 15, 2015

Updated

Mario Draghi has just arrived at the European Parliament, around 15 minutes late. Perhaps his working lunch with Jean-Claude Juncker overran.....

The first link I provided may require a plug-in; if so, you could try watching on EbS instead

The FT has also published details of Greece’s latest proposals (which, as you now know, was swiftly rebuffed before actually reaching the Troika).

They confirm that Athens did accept the creditors demand of a 1% budget surplus this year, but its method of getting there was inadequate (as explained at 12.41pm)

Our friends & rivals at @kathimerini_gr got it 1st, but we also got our hands on #Greece's weekend counterproposal: http://t.co/DZCVJWLwr3

— Peter Spiegel (@SpiegelPeter) June 15, 2015

European Central Bank president Mario Draghi is about to testify before the European Parliament’s Economic and Monetary Affairs committee.

Over in Athens the political opposition has accused prime minister Alexis Tsipras’ leftist-led government of attempting to take debt-stricken Greece back to the drachma.

Our correspondent Helena Smith reports:

The breakdown of talks with creditors has unleashed a welter of criticism from the Syriza-led government’s political foes, with the main opposition centre right New Democracy party accusing the radical leftists of wanting to remove Greece from the euro zone.

Lashing out at the Greek finance minister Yanis Varoufakis, New Democracy’s parliamentary spokesman, Kyriakos Mitsotakis, said it was now clear that the academic-turned-politician “has bankruptcy in the back of his mind.”

“It may be a very fine day for Mr Varoufakis but it not a fine day for the rest of Greeks who, even at this very last moment, want an honourable compromise with Europe and cannot imagine Greece outside the Eurozone,” he told the radio station, Focus 103,6.

“If the government chooses rupture [from Europe] it means a return to the drachma in conditions of absolute chaos with a loss of income of around 30 % and more impoverishment of the Greek people.”

Speaking to the leftist radio station stokokkino.gr earlier today, the Greek finance minister called the breakdown in talks “a moment of clarity.”

“Today is a very fine day,” Varoufakis said, adding.

“Finally we have arrived at the moment of clarity, yesterday Greece said enough is enough, now the Europeans have to take decisions.”

Seen “from a positive angle” things were now crystal clear, Varoufakis insisted, adding that it was impossible to have “real convergence” with creditors if the focus of the discussions was only on fiscal adjustments and not debt restructuring.

He told the station.

“If there was no discussion of debt relief and only the fiscal [reforms] that they want, [we] can’t move forward. Finally, we have arrived at the moment of clarity where the opposite side, and specifically, the German chancellor, has to take decisions.”

The finance minister’s remarks earned this retort from Mitsotakis.

“Mr Varoufakis is clearly picturesque and dangerous. Unfortunately, Mr Tsipras didn’t have the … courage to sideline him.”

Revealed: How the Greek talks went backwards yesterday

EU officials have signalled their utter disenchantment with the Greek negotiations, by supplying unusual detail on how a weekend of talks in Brussels actually amounted to no negotiations at all.

Our Europe editor, Ian Traynor, reports:

On Saturday and Sunday, a team from the creditors, the International Monetary Fund, the European Central Bank, and the European Stability Mechanism bailout fund, waited in a separate room at the European Commission’s headquarters, while Martin Selmayr, chief of staff to Jean-Claude Juncker, president of the European Commission, assessed whether there was enough of a basis for negotiations to begin.

In the end, by Sunday evening, said Brussels officials, the talks were not only stalemated or at an impasse, but had actually suffered a reversal, with the Greeks trying to re-open issues that both sides had already agreed.

The creditors had been promised new Greek proposals from the team that rushed to Brussels on Saturday morning. According to the account in Brussels, they failed to produce a paper. There was nothing to negotiate and the Greeks were asked to produce new figures on their fiscal targets by 10pm on Saturday evening. They delivered by 11pm. The offer was viewed as inadequate. The troika of creditors kept to their separate room and failed to meet the aides to Alexis Tsipras.

The Greeks were asked to return to the table on Sunday afternoon with a revised proposal. The 3pm deadline passed. At 4pm the Greeks arrived with their proposals. An informed official described what then took place.

“Selmayr asked ‘are these the pages you sent today?’ ‘Yes’, was the answer. ‘Are the figures any different from yesterday?’ ‘No’.”

The conclusion: ‘There was no basis for discussion”. The Sunday talks broke up after 45 minutes. The troika team never met the Greeks all weekend.

[PS: this latest Greek proposals was published by Kathimerini this morning]

Updated

Lunchtime summary: Greece and its creditors blame each other

Time for a recap, as we await Mario Draghi’s appearance at the European Parliament this afternoon.

The Greek government and the European Commission have blamed each other for the collapse of negotiations over its bailout programme last night, amid rising concern that Greece could soon run out of cash to service its debts.

Government spokesman Gabriel Sakellardis told reporters in Athens that Greece will keep working towards a deal, but insisted that it will not accept fresh cuts:

The Greek government has only one plan and that is to reach a deal.....

We will not adopt measures which will cut pensions, raise the value added tax on basic goods or measures which exacerbate the vicious circle of austerity.

While in Brussels, the EC criticised Greece for producing numbers that didn’t “add up”.

Spokeswoman Annika Breidthardt said the package proposed by the institutions was substantial, valid and made full economic sense.

“The proposals meet the needs of the Greek people, the Greek government, but also of the other 18 (euro zone) member states.....

“The targets have already been significantly lowered... It’s not a one-way street.”

The EC also denied that it is pushing for pensions to be cut, but does want the overall cost of the system to be lowered by 1% of GDP.

Germany’s EU Commissioner Guenther Oettinger has dramatically raised the tensions today, telling MPs in Germany that Freece

“We should work out an emergency plan because Greece would fall into a state of emergency,” said Oettinger, the EU Commissioner for Digital Economy and Society who is also a senior member of Merkel’s CDU in unusually strong comments.

“Energy supplies, pay for police officials, medical supplies, and pharmaceutical products and much more” needed to be ensured, he said.

He noted that the EU has “proven mechanisms” that can help states to fulfil essential duties such as with police protection and healthcare.

Greek prime minister Alexis Tsipras remains steadfastly opposed to compromise, telling a Greek newspaper that the days of allowing creditors to loot the country are over.

If anyone thought @atsipras would back down, think again: day after talks break down, he comes out swinging pic.twitter.com/PwlOL6v2dx

— Peter Spiegel (@SpiegelPeter) June 15, 2015

Tsipras has been meeting with senior ministers today discuss the crisis.

Greek government debt has slumped in value today, as traders see a higher danger that it will default on its loans.

That drove the yield on Greek two-year bonds soaring to 29.6%, up from below 25% on Friday night.

European stock markets have been hit hard by the crisis today too. The FTSE 100 has shed 70 points or 1.1%, to 6714 points - that’s a three-month low.

And there are steeper losses in other markets; Athens has slumped by over 5%.

And there was no escape from the Greek crisis for Francois Hollande as he visited the Paris Air Show.

France’s president urged Greece to resume talks soon, in an attempt to get a deal before Greece’s bailout expires on 30 June, when it also owes €1.5bn to the IMF.

AFP has the details:

“This message is for Greece,” Hollande told reporters at the Paris Air Show.

“It should not wait and should restart discussions with the institutions... Let’s not waste time.”

Updated

I’d recommend getting your lunch breaks in soon, gang

One hour to go until Draghi takes the stage in Brussels at EP. Interesting to see to what extent Greece is mentioned in opening remarks.

— Todd Buell (@ToddBuell) June 15, 2015

Despite the deterioration in relations between the two sides, some analysts believe a deal will be reached in time.

One is Salman Ahmed of Lombard Odier, the Swiss private bank, who reckons Greece’s lenders can force Alexis Tsipras’s government to make new concessions.

Here’s his take:

“The Greek banking sector is now totally dependent on the ELA provided by the ECB, which gives the European authorities a very strong bargaining chip as any reduction of this support will very quickly push Greece towards capital controls and extended bank holidays, which in turn will make the ruling Greek government very unpopular.

“We expect noise on the Greek front to continue over the short-term (or even escalate), but expect a deal of some form to happen before the end of the month, given how damaging the alternative is for both sides.”

Leaked! The latest Greek proposal

Greek newspaper Kathimerini has now published Greece’s latest offer to its lenders, which was rejected last night.

And it shows that Greece proposed imposing a special windfall tax on corporate profits over €1m, and also hiking corporate income tax from 26% to 29%, to claw in additional revenue.

The report also confirms that Greece proposed just €71m of pension savings next year (and nothing this year); that’s the 0.04% of GDP figure which the Commission cited as inadequate this morning.

And Greece also refused to abolish its lowest VAT rate, as lenders want. Instead, it would actually cut that entry-level rate from 6.5% to 6%, for medicine, books, and theatres.

Despite that, Athens still reckons it can bring in €680m of extra funds this year, and €1.36bn in 2016, by VAT reforms.

The eight-page list also included cuts to defence spending, new taxes on TV adverts and new luxury taxes on private boats and yachts.

Together, the measures show Greece hitting the primary surplus targets set by creditors, of 1% of GDP this year and 2% in 2016.

#Greek media has revealed "shock" list of tax hikes & other measures proposed by gov to creditors http://t.co/tn3BvZE4JV (in Greek)

— Helena Smith (@HelenaSmithGDN) June 15, 2015

Updated

Greek coalition partner: We won't surrender

Over in Athens there’s been fighting talk this morning from the man who leads the government’s junior partner, the stridently anti-austerian right wing populist Independent Greeks party.

Helena Smith reports:

Speaking to state-run TV this morning, the defence minister Panos Kammenos, who also heads the government’s coalition partner, Anel, dug in his heels.

According to Kammenos, Greece’s foreign lenders must choose whether “they want a solution” or whether they want “to impoverish and humiliate a country.”

“The position of Greece and the Greek government is clear. For so many years Greeks have been forced to endure misery because of the failed policies that lenders imposed.

These policies aren’t going to continue, we are not going to surrender democracy, nor our parents, the Greek men and women pensioners who are now living under the poverty line. We have made a huge effort to find a solution. It is now up to them.”

Kammenos, whose popularity ratings like that of the governing radical left Syriza party have also improved since elections in January, insisted that the government didn’t have the mandate “to surrender either our national sovereignty or the dignity of the country and that is what we are going to stick by.”

Jean-Claude Juncker has invited Mario Draghi to a working lunch today, before Draghi’s appearance at the European Parliament this afternoon.

They plan to discuss the Four President’s report on strengthening the eurozone, rather than the Greek crisis, the Commission says.

COM spokesperson Schinas: Juncker will have working lunch with #Draghi today but on four presidents report, not #Greece

— Open Europe (@OpenEurope) June 15, 2015

Is there time to conclude the Greek programme by the end of June if eurozone ministers don’t reach an agreement at their eurogroup meeting on Thursday?

The only deadline is the 30 June when the Greek bailout programme expires, Schinas replies. Thursday’s Eurogroup meeting would have been a good opportunity to assess any progress made over the weekend.

Earlier today, EU Commissioner Guenther Oettinger warned that Greece will face a “state of emergency” unless it has a bailout deal by the end of June.

What plans is the EC taking to handle this?

EC spokesman Margaritis Schinas says that the Commission is very busy negotiating an agreement.

Updated

Over in Brussels, the European Commission is holding its own press briefing and defending its position.

Spokeswoman Annika Briedthardt is explaining that the Institutions have already significantly lowered their budget targets in recent months, down from a surplus of 3.5% of GDP to 1%.

It is up to the Greek government to make fresh proposals, she says, saying negotiations are not a “one-way street”.

We want the numbers to add up....

According to Briedthardt, Greece’s pensions reforms only added up to 0.04% of GDP, not the 1% that its lenders are looking for.

She also firmly denies that that creditors are demanding that individual pensions are cut.

EU Commission: "Gross misrepresentation to say creditors want cuts to individual pensions"

— Mehreen (@MehreenKhn) June 15, 2015

At midday presser, @MargSchinas says @EU_Commission's doors "open 24/7" if #Greece comes back w/another proposal.

— Peter Spiegel (@SpiegelPeter) June 15, 2015

Updated

Some more highlights from Greek government spokesman Gabriel Sakellaridis’s briefing:

#Greece govt spox Sakellaridis: "WE BELIEVE THERE WILL BE AN AGREEMENT & WON'T BE ANY PROBLEM WITH REPAYING THE IMF AT THE END OF JUNE."

— The Greek Analyst (@GreekAnalyst) June 15, 2015

#Greece govt spox Sakellaridis then says that the GR people's collectedness is the best weapon against any kind of blackmailing.

— The Greek Analyst (@GreekAnalyst) June 15, 2015

GR people are cool Sakellaridis: "I want to express the gratitude of the GR govt to the GR people for its amazing coolness it exemplifies

— Dimitris Galanis (@dimitrigalanis) June 15, 2015

The Greek government press briefing is being broadcast live here (no English translation, though).

Gabriel Sakellaridis also blamed Greece’s creditors for the collapse in talks last night, saying they didn’t actually have a mandate to negotiate with them.

That echoes what the top negotiator, Euclid Tsakalotos, told my colleague Helena Smith last night.

#Greece spokesman repeats what chief negotiator @euclidtsakalotos told me tt EU officials had "no mandate" 2 negotiate hence breakdown

— Helena Smith (@HelenaSmithGDN) June 15, 2015

Updated

Greek spokesman: Elections aren't on the table

Greece’s main government spokesman, Gabriel Sakellaridis, is fielding questions in Athens now.

Sakellaridis is insisting that Greece will keep working towards a deal, but on its terms rather than accepting the pension cuts, VAT rises and tougher budget surplus targets its lenders demand (reminder, there is a €2bn gap between the two sides).

Sakellaridis also denied that Greece might be forced to call early elections -- we have a mandate to govern until 2019, he says.

Gov spo @gabriel_athens "We are not at an impasse" #Greece pic.twitter.com/3RYiDs6Raa

— Derek Gatopoulos (@dgatopoulos) June 15, 2015

Reuters has snapped the key points:

- GREEK GOVERNMENT SPOKESMAN SAYS WE WILL CONTINUE EFFORTS TO REACH A DEAL

- GREEK GOVERNMENT SPOKESMAN SAYS OUR PARTNERS DON’T WANT DEBT RESTRUCTURING BUT A CONTINUATION OF AUSTERITY

- GREEK GOVERNMENT SPOKESMAN SAYS GREEK GOVERNMENT’S ONLY PLAN AT THE MOMENT IS TO REACH A DEAL

- GREEK GOVERNMENT SPOKESMAN, ASKED ABOUT EARLY ELECTIONS, SAYS THIS GOVT HAS A MANDATE TO RULE FOR FOUR-YEAR TERM

- GREEK GOVERNMENT SPOKESMAN SAYS SCENARIOS FOR ELECTIONS OR REFERENDUM ARE NOT ON THE TABLE

The president of Portugal, Aníbal Cavaco Silva, has also urged Greece and her creditors to resume talks quickly, echoing Francois Hollande’s concern.

But he is also unwilling to see Greece cut much slack.

- SOFIA - PORTUGAL PRESIDENT SAYS AGREEMENT BETWEEN GREECE AND TROIKA SHOULD BE REACHED AS FAST AS POSSIBLE, THIS WEEK IF POSSIBLE

- PORTUGAL PRESIDENT SAYS THERE ARE RULES AND PROCEDURES FOR ALL AND EXCEPTIONS COULD NOT BE MADE FOR ANY COUNTRY

Germany isn’t buckling this morning -- the Berlin government says they want Greece to stay in the single currency, but Athens must offer new proposals first.

- 10:31:30: GERMAN GOVT SPOKESMAN SAYS GERMAN GOVT WANTS GREECE TO STAY IN THE EURO ZONE

- 10:33:55: GERMAN FINMIN SPOKESMAN SAYS BALL IS IN GREECE’S COURT

French president Francois Hollande warned reporters at the Paris Air Show that Europe will suffer turbulence unless Greece and her creditors reach a deal.

I’ve taken the quotes from Reuters:

“We are arriving at a time that could be turbulent if we don’t reach an agreement....

Let us not waste time and let’s restart the negotiations as soon as possible.”

Updated

Newsflash from Greece: The government’s top ministers have begun holding an emergency meeting (earlier than we thought....)

Extraordinary meeting between #Greece PM #Tsipras, Dep PM Dragasakis, FinMin #Varoufakis & Interior Min Voutsis underway (via @MegaGegonota)

— Manos Giakoumis (@ManosGiakoumis) June 15, 2015

#Hollande says Greece shouldn't wait, the government should go back to talks with the European institutions

— Gráinne McCarthy (@grainnemcc) June 15, 2015

Hollande: Talks must resume soon

France’s president, Francois Hollande, has urged Greece and its institutions to resume talks as soon as possible.

* French president francois Hollande says must not waste time on Greece, need to restart talks as quickly as possible - RTRS

— Fabrizio Goria (@FGoria) June 15, 2015

I think he was speaking at the Paris Air Show.

Greek banks appear to be working normally today:

Swissquote: Odds of a Greek default have spiked

I know you’re all heard this before, but it really is a crunch week for Greece.

Its existing bailout programme expires on 30 June; if there’s not a deal by then, Greece will lose €7.2bn of outstanding loans which have been frozen for months.

The best, possibly last chance of a deal to unfreeze those funds comes in three days time when eurozone finance ministers meet.

And Europe’s stock markets will be “driven by the saga”, says Peter Rosenstreich, Head of Market Strategy at online bank Swissquote:

The deadline is approaching fast (end of June) and the Eurogroup meeting on Thursday is broadly seen as the last chance for Greece to reach an agreement that will unlock the remaining €7.2bn bailout fund. In spite of last week’s highly uncertain environment, markets remained relatively stable with most market participants consolidating their positions.

However, we expect markets will feel the heat this week as the odds of a Greek default have increased considerably.

Jens Weidmann, the head of Germany’s Bundesbank, has just warned that time is running out for Greece, Reuters reports.

Weidmann was giving a speech in Frankfurt this morning, and warning that central bank policy can’t do everything.

- BUNDESBANK CHIEF WEIDMANN SAYS MORE EXPANSIONARY MONETARY POLICY WOULD NOT ADDRESS FACTORS THAT ARE DRAGGING ON GROWTH

- BUNDESBANK CHIEF WEIDMANN SAYS HIGH PUBLIC DEBT AND RESULTING TAX BURDEN COULD DAMPEN GROWTH IN EURO ZONE

- WEIDMANN SAYS MONETARY POLICY CAN MAKE A CONTRIBUTION TO RETURNING TO SUSTAINABLE AND SOLID GROWTH

Greek media are reporting that Alexis Tsipras will meet his bailout negotiating team this afternoon, around noon BST.

Emergency Governmental Meeting to take place under Tsipras at 14:00 (local time), various local media report. #Greece

— The Greek Analyst (@GreekAnalyst) June 15, 2015

The selloff in Greek government debt is intensifying too:

#Greece's 2yr yields jump to 28.3% as default risks rise after debt talks collapsed. pic.twitter.com/EXCdYd8WM1

— Holger Zschaepitz (@Schuldensuehner) June 15, 2015

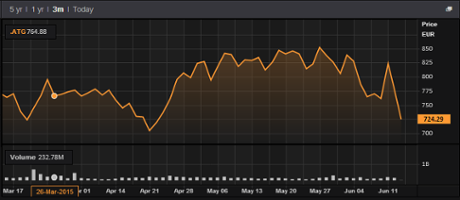

The Athens stock market has now hit its lowest point since late April, as bank shares drag it down:

Updated

Greek stock market slumps

The Greek stock market has tanked by over 6% in a panicky rush of sell orders, as trading begins in Athens.

Banking shares have slumped by over 12%, hit by fears that the Greek government could default.

Unsurprisingly, the Athens Stock Exchange is down 6.71%. #Greece

— Vincenzo Scarpetta (@LondonerVince) June 15, 2015

Greek banks are already heavily reliant on the emergency liquidity provided by the European Central Bank. It will decide on Wednesday whether to maintain that support.

Tsipras: No more bailout looting

Alexis Tsipras is implacable that Athens will not cave in to creditors’ demands.

In a defiant statement to the Ton Syntakton newspaper, the Greek prime minister said his government will wait “patiently” until lenders become realistic.

Tsipras told the paper that he would not surrender his democratic mandate, having won power in January on a pledge to end the “vicious cycle of austerity”.

“One can only see a political purposefulness in the insistence of creditors on new cuts in pensions after five years of looting under the bailouts.”

“We will await patiently until the institutions accede to realism,. We do not have the right to bury European democracy at the place where it was born.”

#BREAKING Athens ready to 'wait patiently' until creditors become 'realistic': Tsipras

— Agence France-Presse (@AFP) June 15, 2015

The unfolding Greek crisis has sent shares sliding in London, Paris, Amsterdam, Milan, Madrid and Frankfurt:

Ian Williams of Peel Hunt explains:

The tone of the reports over the weekend suggested that the other European leaders are losing patience with Greece and news that the implications of a default are under serious discussion does not suggest hopes for a compromise are high.

European markets hit by Greek fears

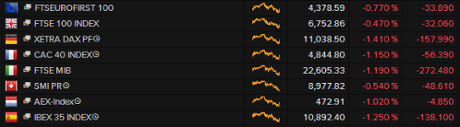

European markets are falling in early trading as fears that Greece could soon default on its loans sweep the trading floors.

As feared, the German DAX fell 1.3% at the start of trading in Frankfurt, followed by France’s CAC (down 1.1%).

In London, the FTSE 100 is down 35 points, or 0.5%, at 6750 as investors react to the collapse of talks on Sunday evening.

German MP: Greece needs to get back to reality

The parliamentary leader of Chancellor Angela Merkel’s conservative Christian Democrats (CDU) has urged Greece to “get back to reality” this morning, showing that tensions in Berlin are rattling up.

Volker Kauder also warned that the Bundestag will refuse to back a Greek aid package unless the IMF is fully involved:

Kauder told the ARD TV station:

“I couldn’t vote for a further payment if the IMF says it won’t work...We’re pleased that the IMF is with us but if it says it won’t work then our parliamentary group will also say we can’t pay out further (loan) tranches.”

“We all know what’s at stake. No one else in Europe is carrying the responsibility for this except Greece itself.

“Not only Angela Merkel (wants to keep Greece in the euro), a lot of people want that....We’re saying Greece should remain. But it won’t work that Greece sets the terms and says ‘everyone else has to dance to our tune’. Greece needs to get back to reality.”

(quotes via Reuters)

Updated

And here’s another sign of alarm:

- EURO/DOLLAR 1-MONTH IMPLIED VOLATILITY RISES TO 3-1/2 YEAR HIGH OF 14.305%, TRADERS CITE GREEK WORRIES

That means investors are paying more to protect themselves against sharp swings in the value of the euro in the weeks ahead.

Updated

Money is flowing into German bonds and out of Italian, Spanish and (of course) Greek debt this morning.

That has pushed the yield (or interest rate) on German 10-year bunds down to 0.8%, from 0.85% on Friday night.

Flight to safety after Greek talks collapsed: 10yr Bunds Yield 0.80%; Down 5bps. pic.twitter.com/Psv3HmBRKg

— Holger Zschaepitz (@Schuldensuehner) June 15, 2015

The yield on two-year Greek bonds has risen to 26%, from 25.86% on Friday night, showing it’s seen as even riskier this morning.

Investors concerned by Greek deadlock

Stock market traders in Frankfurt may be reaching for the tin hats.

The German DAX is tipped to fall by around 150 points, or 1.3%, when trading begins in around 20 minutes time. Other markets are also expected to lose more ground, extending last week’s losses:

Chris Weston of IG says there is “a modest degree of concern” about Greece.

The Greek negotiating team are still optimistically pushing for continued inclusion in the Monetary Union, while at the same time pushing for debt forgiveness and maintaining government. This is simply not going to happen but it is important to note that both the Greeks and the Creditor nations have common ground, in so much that they are both agreeing on a 3.5% primary surplus by 2018.

It’s the pace and how they get there in the years leading into this that are a major point of contention.

Updated

Introduction: Greek fears grow as talks break down

Good morning, and welcome to our rolling coverage of the Greek bailout negotiations and other key events across the world economy, the financial market and business.

Fears of a Greek default are rising this morning after last-ditch talks between Athens and its creditors collapsed on Sunday night.

A meeting between the two sides broke up after under an hour, with negotiators unable to reach any agreement on pension reforms, budget targets and tax rates.

That has dashed lingering hopes that eurozone finance ministers could rubber-stamp a deal when they meet on Thursday.

Instead, Greece is careering towards the end of June, when its bailout programme expires and it owes around €1.6bn to the International Monetary Fund.

EU insiders dismissed the Greek plans as “incomplete”, while Greece’s top negotiator Euclid Tsakalotos blamed the creditors for failing to compromise.

Tsakalotos told us:

“We made huge efforts to meet them halfway but they insisted on both pension cuts and the increase in VAT on restaurants and would not accept closing the gap even partially via administrative measures to reduce tax evasion, even though this was a central plank of our electoral programme.

Moreover, they told us bluntly they had no mandate to discuss a compromise! So much for negotiating...

Here’s Helena Smith full story:

Happy (early) Monday. Not much constructive commentary being distributed about state of Greek debt negotiations from either side. $EURUSD

— Christopher Vecchio (@CVecchioFX) June 15, 2015

It tees up another “crunch week for Greece”, with Thursday’s eurogroup meeting likely to be extremely tense.

Greek talks break down, deadline approaching. Anyone else got a sense of déjà vu?

— Duncan Weldon (@DuncanWeldon) June 15, 2015

We’ll hear from the Greek government shortly, and then from European Central Bank president Mario Draghi this afternon, when he appears at the European Parliament from 3pm Brussels time (2pm BST)

Even as the talks were collapsing, the IMF was launching a blogpost by the IMF’s chief economist, Olivier Blanchard, which explained that a “credible” deal must include some debt relief for Greece.

Blanchard wrote:

On the one hand, the Greek government has to offer truly credible measures to reach the lower target budget surplus, and it has to show its commitment to the more limited set of reforms. We believe that even the lower new target cannot be credibly achieved without a comprehensive reform of the VAT – involving a widening of its base – and a further adjustment of pensions. Why insist on pensions? Pensions and wages account for about 75% of primary spending; the other 25% have already been cut to the bone. Pension expenditures account for over 16% of GDP, and transfers from the budget to the pension system are close to 10% of GDP. We believe a reduction of pension expenditures of 1% of GDP (out of 16%) is needed, and that it can be done while protecting the poorest pensioners. We are open to alternative ways for designing both the VAT and the pension reforms, but these alternatives have to add up and deliver the required fiscal adjustment.

On the other hand, the European creditors would have to agree to significant additional financing, and to debt relief sufficient to maintain debt sustainability. We believe that, under the existing proposal, debt relief can be achieved through a long rescheduling of debt payments at low interest rates. Any further decrease in the primary surplus target, now or later, would probably require, however, haircuts.

But some Greek politicians won’t settle for mere debt haircuts. According to Ambrose Evans-Pritchard in the Telegraph today:

The radical wing of Greece’s Syriza party is to table plans over coming days for an Icelandic-style default and a nationalisation of the Greek banking system.

Syriza sources say measures being drafted include capital controls and the establishment of a sovereign central bank able to stand behind a new financial system. While some form of dual currency might be possible in theory, such a structure would be incompatible with euro membership and would imply a rapid return to the drachma.

The confidential plans were circulating over the weekend and have the backing of 30 MPs from the Aristeri Platforma or ‘Left Platform’, as well as other hard-line groupings in Syriza’s spectrum. It is understood that the nationalist ANEL party in the ruling coalition is also willing to force a rupture with creditors, if need be.

With one Syriza MP vowing not to be “throttled to death by European monetary union,” it’s going to be another dramatic week....

Updated