Closing summary: Greece inching towards bridging loan deal

And that’s all for tonight. Just a quick recap:

The finance ministry is also considering proposing 10 new reforms at the Eurogroup meeting on Wednesday night.

It’s a sign that Athens may be softening its position, but there’s nothing official yet.

So the Eurogroup meeting will be about finding a legal way to make an exception for a bridge loan under some conditions. Can't wait.

— Frederik Ducrozet (@fwred) February 9, 2015

Speaking to the Guardian, Varoufakis said:

“Allowing [the single currency] to fragment would be catastrophic … it is the moral duty of the critics of the Euro Zone to fix it, to make sure it doesn’t collapse because if it does the cost will be immense not just for the Greeks but the Brits, everyone.”

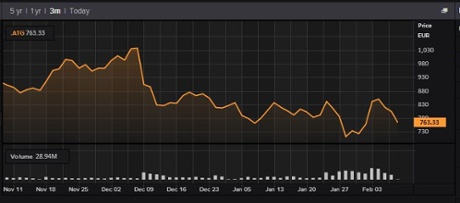

The Greek stock market suffered another selloff, down almost 5%, after Alexis Tsipras’s speech to parliament last night - in which he ruled out implementing Greece’s old austerity programme.

But Germany remains implacable; Angela Merkel said tonight it is up to Greece to produce substantive plans for the way ahead.

Merkel makes it pretty clear that the onus is on Greece -- and not to expect Germany or EU to come up with another plan.

— Scott Wapner (@ScottWapnerCNBC) February 9, 2015

That was Merkel's "Talk to the Hand" moment on Greece

— Scott Wapner (@ScottWapnerCNBC) February 9, 2015

Fears over the strength of Greece’s financial sector prompted Moody’s to downgrade five banks.

And as covered in the lunchtime summary, Britain has started preparing emergency plans for a Grexit:

Given uncertainty around Greece & the Euro, it was important I chair a meeting to ensure the Government is prepared for all eventualities.

— David Cameron (@David_Cameron) February 9, 2015

I’ll be back tomorrow. Goodnight, and thanks for all the comments. GW

You’d think there was an election coming up....

At #G20 in Istanbul where stronger economic growth in UK and US singled out, but risks from Greece and Ukraine dominates

— George Osborne (@George_Osborne) February 9, 2015

Updated

The AFP newswire has also heard that the Greek government is planning to ask the eurogroup for bridging funding until the end of August, while it hammers out a new long-term plan.

Greece wants a new economic deal with its EU creditors to enter into force from September 1, a Finance Ministry source said Monday.

“It is in our interest to have the deal running from September 1, the source said, ahead of crucial talks with eurozone finance ministers on Wednesday.

Updated

#Merkel: “This program is the foundation of what we’ve discussed,” “But I’m waiting for Greece to come forward with a viable recommendation”

— Francine Lacqua (@flacqua) February 9, 2015

Over in Washington DC, Angela Merkel has told reporters that “what counts” is the plan that Greece brings to the eurogroup meeting on Wednesday night.

The German chancellor declined to speculate on Greece’s plans until Athens has come up with a sustainable proposal.

So, no indication whether she’d be amenable to a bridging loan until the end of August, tied to various (as yet unspecified) new reform measures, as we understand the Greek government is considering (see earlier post).

Rating agency Moody’s just cut the credit rating on five major Greek banks, as fears over the country’s future in the eurozone continue to swirl.

Moody's downgrades 5 Greek Banks; Ratings On Review For Further Downgrade. Downgrades Piraeus, National Bank of Greece, Alpha to Caa2.

— Holger Zschaepitz (@Schuldensuehner) February 9, 2015

Moody's downgrades Eurobank Ergasias SA to Caa3 from Caa2, Attica Bank SA to Caa3 from Caa2.

— Holger Zschaepitz (@Schuldensuehner) February 9, 2015

Last Friday night, Moody’s put Greece’s sovereign debt rating on review for a possible downgrade.

Mujtaba Rahman of Eurasia Group reckons Athens will probably execute a “dirty exit” from its bailout at the end of the month, but it’s not a given.

- Although the Greek government’s policy manifesto includes a number of important concessions to European creditors, it does not go far enough to create the basis for a deal.

- Therefore, we remain of the view that Greece will undertake a “dirty exit” of its bailout on 28 February with no agreed backstop in place but this is a very close call.

- Economic and financial stress will increase over the next few weeks, but supportive public opinion means the risk of government collapse over the next few weeks is unlikely (45%).

After another day of heavy selling, Greece’s stock market closed down almost 5% tonight.

Bank shares were, again, hit by the growing fears that Greece could be ejected from the eurozone.

The euro was pretty calm, though. It’s currently up 0.15% against the US dollar.

Christopher Vecchio, currency analyst at DailyFX, says it’s “pointless to peg a specific likelihood of a Grexit”, but concedes that this “tail-risk scenario is probably “shifting closer to the centre of the bell curve”.

Greek financial news website Euro2Day has also published details of Greece’s possible strategy for Wednesday night’s Eurogroup meeting.

They suggest that Athens may ask for a bridging loan to cover funding needs until September [as we flagged up at 15.47 GMT].

And they’ve also heard the rumour that Greece might propose 10 new reforms to cover the parts of the bailout programme which it is now rejecting.

#Greece to present an 'intermediate' proposal at Wednesday's Eurogroup meeting, @euro2day_gr reports: http://t.co/6YHJyevlSo

— Yannis Koutsomitis (@YanniKouts) February 9, 2015

Something's apparently moving...

— Yannis Koutsomitis (@YanniKouts) February 9, 2015

Updated

Meanwhile in Berlin...Alexis Tsipras’s demand for Germany to pay war reparations, and repay the interest-free loan extracted from Greece during world war 2, has been robustly rejected.

Sigmar Gabriel, Germany’s vice chancellor and economy minister, said there is “zero” probability of this happening.

#Germany rejects Greek claim for World War Two reparations http://t.co/3cUbgyCpzt #Greece

— Yannis Koutsomitis (@YanniKouts) February 9, 2015

Updated

Greece might push for bridge programme to run until August

Greek finance minister Yanis Varoufakis has been giving a hint of the way he’ll approach Wednesday night’s emergency eurogroup meeting.

Our correspondent Helena Smith reports that Varoufakis, who met with Athens reporters earlier, is planning to stick to his guns. He’ll push his fellow European finance ministers to accept a “bridge programme” to cover the government’s funding needs while a new debt pact can be agreed.

But the Athens government is indicating that its creditors at the EU/ECB/IMF could call such a programme whatever they like. And there’s talk that this bridging loan could run until the end of August [only this morning, Varoufakis suggested a four-month bridge -- it just keeps growing....]

This suggests it might not differ too much from the six-month extension that the eurogroup was pushing last December [but which former prime minister Samaras rejected, in favour of a two-month window].

But what about the various ‘prior actions’ that Greece agreed, but hasn’t yet implemented?

Well, Varoufakis is likely to pledge to implement around 70% of the existing bailout programme [a point he made to parliament earlier]. We’re hearing that he might give the eurogroup details of perhaps ten new measures to replace the missing 30%.

Updated

Another photo of those pro-Athens protests in Vienna today:

Financial markets, winter is coming! #tsipras in Vienna... pic.twitter.com/emRAPDLTz1

— Lukas Oberndorfer (@L_Oberndorfer) February 9, 2015

Speaking of world leaders.. Germany’s Angela Merkel has arrived at the White House for talks with president Barack Obama.

The Ukraine crisis is top of the agenda, but I suspect they’ll touch on Greece too.

German Chancellor Angela Merkel arrives at the White House; Merkel & Pres. Obama to hold news conf. at 11:40a ET. pic.twitter.com/J40vy12IPP

— CNBC Now (@CNBCnow) February 9, 2015

There were pro-Greece protests in Vienna today, as prime minister Alexis Tsipras visited Austria to meet chancellor Faymann.

As mentioned earlier, Faymnn called for compromise over the Greek debt battle:

“The question is finding a solution between the content of the framework agreed in the past and the efforts of the new [Greek] government,”

And Tsipras also sounded upbeat, telling reporters:

“We all have an interest in coming to a mutually beneficial solution.”

Those who invested in the Greek government’s failure were “playing with fire and the danger of the far right rising in Europe,” Tsipras said.

And from Athens, Helena reports that Greek TV stations seized on Tsipras’s optimistic tone:

“The prime minister’s comments were in a different vein to what we have been hearing [from within and without Greece]. It is clear he wants a solution. Perhaps he knows something that no one else does?” said Marko Deimizi, who anchors SKAI TVs popular Magazino show.

The rising tensions in Greece have rippled across to the New York stock market.

The Dow Jones industrial average and the wider S&P 500 both dipped around 0.25% at the start of trading.

Thanks for nothing, Greece. Stocks slide around the world Monday as the Greek drama continues. Dow falls 70 points. http://t.co/A9OlUXl3FI

— CNNMoney (@CNNMoney) February 9, 2015

So how could things develop from here?

Professor Hari Tsoukas of Warwick Business School fears that Greece’s creditors will refuse to alter its bailout programme, because they don’t believe Athens can implement reforms.

Tsoukas (who ran for the centrist Potami party in last month’s elections) says:

“The terms of debt relief for Greece will be decided, ultimately, by politics. Power is what matters, and power is with the creditors, not Greece. The fundamentals of the bailout programme are unlikely to change.

“My sense is that Alexis Tsipras will not back off, for if he does, he knows he will incur the fate of his predecessor – sticking with austerity will cost him dearly. Besides, he may hope that by putting up a fight, he may ultimately force creditors to change their view, since a Greek exit will be potentially disastrous for the Euro zone.

“Unless there is compromise - which for the time being I see as difficult to be achieved - a likely scenario is for Tsipras to put whatever deal he cuts with the creditors to a referendum or call fresh elections. That will complicate things enormously, especially since, most likely, there will be a bank run and the banking system will collapse.

The growing popularity of Spain’s new Podemos party highlights why European leaders are unwilling to cut Greece a deal, for fear of vindicating the anti-austerity movement.

Latest polls in Spain: Podemos way in front at 28%. pic.twitter.com/1uoN4KYx4D

— ian bremmer (@ianbremmer) February 9, 2015

(Europe’s weak growth and near-record unemployment could be all the vindication we need, mind you....)

Schäuble: Don't know how markets will react

Germany’s finance minister is maintaining an uncompromising attitude on Greece today.

Attending the G20 ministers meeting in Istanbul, Wolfgang Schäuble declared that he didn’t know how the markets would react if Greece abandoned its bailout, adding:

“We’ve never forced anyone into a programme.

I’m ready for any kind of help, but if my help is not wanted, that’s fine.”

So there! Maybe Herr Schäuble is sore that The Economist has dubbed him “Europe’s foremost ayatollah of austerity”

"I wouldn't know how markets will handle it w/out a programme, but maybe he knows better." #Schauble on @atsipras http://t.co/Jjsk034Smi

— Peter Spiegel (@SpiegelPeter) February 9, 2015

Updated

Associate Press has the full quote from Yanis Varoufakis to the Athens parliament:

“The time has come to say what officials admit when the microphones are turned off and say out in the open. ... At some point someone has to say ‘No’ and that role has fallen to us, little Greece,”

After speaking to the Guardian, Varoufakis went on to address the Athens parliament, as the debate ahead of Tuesday night’s confidence vote picks up.

The Greek finance minister got a standing ovation as he said: “someone has to say No and that is Greece!”.

But he also tried not to sound too confrontational, saying the new government would implement around 70% of the current Memorandum of Understanding agreed with the Troika.

#Greece Varoufakis: We are not "yes-man" nor "no-man", we are just European citizens

— Efthimia Efthimiou (@EfiEfthimiou) February 9, 2015

Greek Finance Minister Varoufakis "At Eurogroup, I will not be a yes man but I will say "yes" to proposals that makes sense" #Greece

— Kathimerini English (@ekathimerini) February 9, 2015

Updated

Back to Athens, and Yanis Varoufakis has outlined how Greece and its lenders can find a mutually agreed face-saving solution.

The key, he told our Helena Smith, is Greece’s proposal of a bridging program for two, or three, or four months “to which we make some undertakings to our partners”.

During that time the new government would forge ahead with crucial reforms that could be mutually agreed while ensuring the budget is not derailed.

“And why do we want this to have the time and the space to sit down and deliberate? We just want a little bit of time....”

The prime minister tweets..

Given uncertainty around Greece & the Euro, it was important I chair a meeting to ensure the Government is prepared for all eventualities.

— David Cameron (@David_Cameron) February 9, 2015

Varoufakis: Eurozone collapse would have 'immense cost'

Over in Greece our correspondent Helena Smith can confirm that Yanis Varoufakis is in fighting form – and optimistic about the future.

Helena writes:

I had a long sit-down with the Greek finance minister this morning, and he did not disappoint.

Varoufakis’s reaction to George Osborne’s revelations on Sunday that Britain is stepping up contingency plans in preparation of a possible Greek exit from the euro zone was one of slight mystification.

He had, he said, had very friendly discussions with the chancellor in London last week.

“Anybody can compile contingency plans but I don’t know what that means,” he told me in his sixth floor office overlooking Syntagma square, adding:

“I can’t even begin to imagine what preparation he [Osborne] is putting in. Maybe he has aces up his sleeve that I am not familiar with.”

As for the Alan Greenspan’s predicting Greece’s exit from the currency bloc, Varoufakis was emphatic. The former head of the US federal reserve belonged to the school of thought that the euro zone was untenable – a view that, he himself, had been loud and clear about back in the 1990s.

“Greenspan is part of the tradition of Anglo Saxon financiers, economists and central bankers who never believed in the Eurozone construction. I happened to be one of them … back in the 1990s I was writing articles that argued that the way the euro zone was constructed was like removing the shock absorbers from the system [the single currency] and ensuring that when the shock comes it is of maximum [strength].

“However, having said that, allowing it to fragment would be catastrophic … it is the moral duty of the critics of the Euro Zone to fix it, to make sure it doesn’t collapse because if it does the cost will be immense not just for the Greeks but the Brits, everyone.”

The rest of the world would instantly go into recession, he said, if the eurozone collapsed.

Describing himself as an “internationalist” Varoufakis insisted that Greece’s fate was inextricably bound up with that of Europe. But he was also clear-headedly optimistic.

“I cannot possibly separate the fate of Greece from the fate of Europe… We are perfectly capable as Europeans to mess things up unnecessarily. We can find the accommodation between Greece and our creditors, our partners, the EU, ECB and IMF,” he said before adding that in a depressed economy it was simply impossible for the policies of “contractionary contraction” to work.

“There is no economist I know in the world who thinks this program has worked, or will work … it couldn’t work. It’s not a question of willpower or intelligence, it simply cannot be done in a depressed economy that has no viable banking system that is properly functioning and giving out loans.”

At the same time Greece’s new government recognised that a loan agreement had been signed and that Athens had entered into a “legal framework” with its international creditors.

Varoufakis concluded:

“There has to be continuity but at the same time the argument that the elections don’t change anything and that the government has to adopt a program it was elected to challenge the logic of, is absurd.”

Updated

The leader of Austria, Werner Faymann, has offered Greece some support after a meeting with prime minister Alexis Tsipras today.

Chancellor Faymann told reporters in Athens that both sides must compromise:

Faymann: "Greece must stay in euro and we have to find mutually acceptable solutions" #Greece #Austria

— Kathimerini English (@ekathimerini) February 9, 2015

Faymann "There must be compromise between previous program and plans that current gov't has" #Greece #Austria

— Kathimerini English (@ekathimerini) February 9, 2015

Tsipras sounds upbeat too:

Tsipras "Very satisfied by today's discussion. I have a new friend that can help us find viable solution for common European future" #Greece

— Kathimerini English (@ekathimerini) February 9, 2015

Lunchtime summary: Greek crisis escalates

Time for a quick recap, before we hear from the Greek finance minister in under an hour’s time (3pm EET/1pm GMT).

Greece’s escalating debt crisis has sent shares sliding across Europe, and triggered a new selloff in Greek bonds. The Athens market is down 6%, as bank shares suffer new double-digit falls. In London the FTSE 100 has lost 54 points.

Fears that Greece might default also drove yields high into dangerous territory; the three-year Greek bond hit levels not seen since its 2012 restructuring.

The selloff was sparked by last night’s speech by prime minister Alexis Tsipras; he laid out a comprehensive plan to end austerity, and also pledged not to extend the country’s bailout programme [see last night’s story].

Although Greece insists it can reach a deal with its creditors, there are signs that the crisis is sending shivers through the global community.

-

UK prime minister David Cameron held a briefing on Britain’s plan if Greece leaves the eurozone, this morning. Genuine concern, or a politically-motivated move, some wonder....

Dare I say it, letting it be known he's prepared for eurocrisis isn't unhelpful for a PM keen to hammer in that he has a long-term econ plan

— Ed Conway (@EdConwaySky) February 9, 2015

-

European Commission president Jean-Claude Juncker warned Tsipras that he can’t expect Europe to simply accept his proposals.

-

Canada’s finance minister urged both sides to make compromises.

- And Timothy Adams of the Institute of International Finance warned that time is running out.

City analysts are also increasingly concerned. Gary Jenkins of LNG Capital said Tsipras’s speech had raised the chance of Greece leaving the eurozone, to 50%.

But Greece’s finance minister, Yanis Varoufakis, has insisted that there’s no conflict with the rest of Europe -- even though fellow nations have shown little support for his attempt to re-engineer the debt mountain.

However, Varoufakis’s claim yesterday that Italy also faces unsustainable debts may not have helped his cause, suggests the FT’s editor....

Greece just lost Italy ahead of this week's euro group meeting #varoufakis shooting from the lip #berlin

— Lionel Barber (@lionelbarber) February 9, 2015

Updated

#Cameron: “We need to be prepared to deal with instability in the markets”; Foreign Office updated PM on political situation in #Greece

— Francine Lacqua (@flacqua) February 9, 2015

UK officials have dug into their filing cabinets to find the Grexit plan pulled together at the height of the eurozone crisis, tweets Sky’s economics editor Ed Conway.

HMT & @bankofengland have had detailed contingency plans for #Grexit since 2011/12. They were dusted off when Syriza won the election. (1/2)

— Ed Conway (@EdConwaySky) February 9, 2015

(that’s Her Majesty’s Treasury)

Lobby has been briefed on a No 10 meeting on Greece/euro today - though the key work has been going on behind the scenes at Bank/HMT (2/2)

— Ed Conway (@EdConwaySky) February 9, 2015

But insiders still reckon a compromise will be hammered out...

My govt sources still convinced everyone in euro (inc Germany) will do all they can to prevent #Grexit. They stared into precipice in 2012

— Ed Conway (@EdConwaySky) February 9, 2015

Updated

Here’s a summary of the headlines in today’s Greek newspapers, via Enikos.gr.

“Alexis message to the Germans: Hand over the money you owe us from WWII” is the main story in Kontranews.

Ethnos says that the Greek PM adopts a tough line in the negotiations with the lenders.

Eleftheros Typos reckons that Tsipras is set for a head-on conflict with the troika whereas at the same time is looking for a bridging agreement.

Ta Nea reveals that 85 names are missing from the ‘Lagarde list’ [of suspected tax avoiders]

I Efimerida ton Syntakton quotes Tsipras: ‘Our dignity is non-negotiable’

Right-wing Eleftheri Ora says that Alexis Tsipras is Greece’s Che Guevara!

Updated

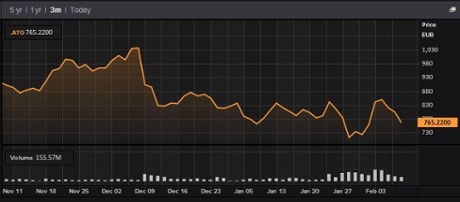

The selloff in Athens is picking up pace, sending the main ATG index down almost 6% today.

It’s heading back towards the lows plumbed immediately after Syriza won last month’s election.

The word from Westminster is that David Cameron chaired a meeting with officials from the finance ministry and the Bank of England this morning, to plan for a possible Greek exit from the euro zone.

We’ll have more details very soon. In the meantime, one Treasury source has told Reuters that:

“It is not saying that anyone thinks it is going to happen, but it is right that they have a look at the risk of Greece leaving the euro zone. That would create real instability.”

Just what the UK government doesn’t want, three months before the general election.

Contingency planning; would be more newsworthy if they hadn’t. MT @Peston PM held meeting to plan for+protect UK from poss Grexit. #Greece

— Mehran Khalili (@mkhalili) February 9, 2015

If the Bank of England did not have plans ready for #Grexit before today there should be a national enquiry as to why not?! #BoE

— Shaun Richards (@notayesmansecon) February 9, 2015

Heads-up: Greece’s finance minister, Yanis Varoufakis, is expected to hold a press conference this afternoon, around 3pm local time or 1pm GMT.

Canada’s finance minister has urged Greece and its international creditors to find a compromise.

Joe Oliver (in Istanbul for the G20 meeting) told Reuters that both sides need to give ground:

“There has to be compromise. It’s clear that Greece has got to be prepared to make some changes, and I think a wholesale repudiation of their debt is not on the cards.

But other countries, creditors will have to work with Greece to arrive at a compromise solution.”

What Tsipras pledged last night

Alexis Tsipras outlined a broad range of measures last night, to unravel the austerity programme that Greece has endured since 2010.

Teneo Intelligence has helpfully rounded up the key commitments, which MPs will vote on tomorrow night:

- Abolish the single property tax (ENFIA) and replace it with another tax targeting large real estate properties.

- Re-increase the tax-free threshold to €12k (from its current €5K).

- Restore the 13th pension for gross monthly pensions below €700 from end 2015.

- Introduce subsidized meals for families living below the poverty line.

- Rehire 3,500 civil servants who lost their jobs as a result of the mobility scheme introduced by the previous government in the public sector. However, this number would be subtracted from the 15,000 recruitments scheduled for this year.

- Raise the monthly minimum wage in the private sector from €586 (or €510 for under-25s) to its 2011 level of €751 by 2016.

- Restore collective wages bargaining with the advice of the International Labor Organization (ILO).

- Extend the existing ban on foreclosures of primary residences.

- Stop new privatizations, but extend concessions when in the national interest.

- Introduce legislation enabling the Hellenic Financial Stability Fund (HFSF) to exercise its full voting rights with no restrictions in recapitalized banks.

- Repel legislation providing immunity to the members of the boards of the HFSF, the Hellenic Republic Asset Development Fund (HRADF) and the Bank of Greece.

- Introduce a new ‘stable, simple and fair’ tax system and fight corruption and tax evasion.

- Introduce a comprehensive reform of Greece’s public sector.

Updated

BBC: UK government holds talks over Grexit risk

It’s 2012 all over again - the BBC has learned that David Cameron has met with officials at the Treasury and the Bank of England to discuss the risk that Greece leaves the single currency.

Prime Minister held meeting with Treasury and Bank of England to plan for and protect UK from possible Greek exit from euro, I have learned

— Robert Peston (@Peston) February 9, 2015

Updated

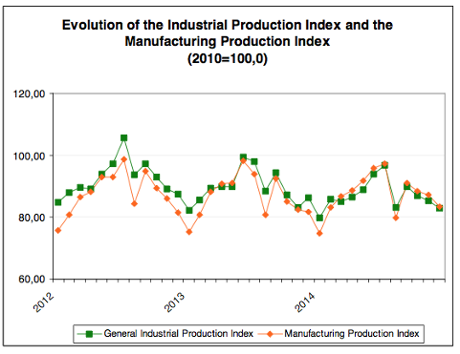

Greece’s factory sector was already weakening before the current crisis erupted, new data shows.

Industrial production across Greece shrank by 3.8% in December, compared to the previous year, according to statistics body ELSTAT.

The only good news is that manufacturing picked up. Here’s the details:

- Mining and quarrying production decreased by 13.2%.

- Manufacturing production increased by 2.1%.

- Electricity production decreased by 18.6%.

- Water supply production increased by 4.3%.

Updated

Yanis Varoufakis: No conflict between Greece and Europe

Greece’s finance minister is playing good cop this morning, denying that there’s any dispute between Athens and its creditors.

Yanis Varoufakis told reporters gathered outside the finance ministry that:

“There is no conflict, there is discussion and consultation as always happens in the European family.”

And Varoufakis shot back “Don’t be so hasty”, when asked if Greece should hold a referendum on the debt crisis.

Updated

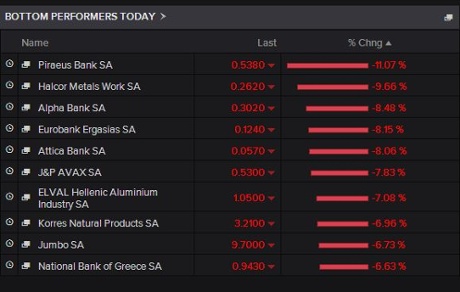

The never-ending decline of #Greek banks: -25% in 3 days and 99.15% below 2007 highs... pic.twitter.com/NsMcGk2wsb

— Mark Barton (@markbartontv) February 9, 2015

European Commission chief Jean-Claude Juncker has warned Greece this morning that the eurozone can’t simply accept all of Syriza’s programme.

Juncker told reporters in Germany that Tsipras’s speech last night had “only partly addressed” Brussels’ concerns about his plans.

Updated

The BBC’s esteemed economics editor is many things, but thick is certainly not one of them....

I am obviously being thick but I can't see deal between Athens/Syriza and Berlin/Brussels http://t.co/QOqrqTfIF8

— Robert Peston (@Peston) February 9, 2015

This chart shows how Grexit worries drove Greek bond yields higher at the start of trading:

Doesn't seem the bond market too happy w/@atsipras speech yesterday. Yield on 10-year back about 11%. pic.twitter.com/vtN3rFkYLy

— Peter Spiegel (@SpiegelPeter) February 9, 2015

Another bad morning for Greek bank shares:

The Greek parliament is starting to debate the programme that was outlined by Alexis Tsipras last night.

Twitter user Diane Shugart is watching, and reports that it’s a slow - and confusing - start.

first speaker is ND's kyriakos mitsotakis. wants to know if there will be a lunch break. (the answer is yes: 4-6 pm, for prep.)

— Diane Shugart (@dianalizia) February 9, 2015

did kasidiaris just ask for a referendum on the euro? (i honestly have trouble following his rambling.)

— Diane Shugart (@dianalizia) February 9, 2015

Updated

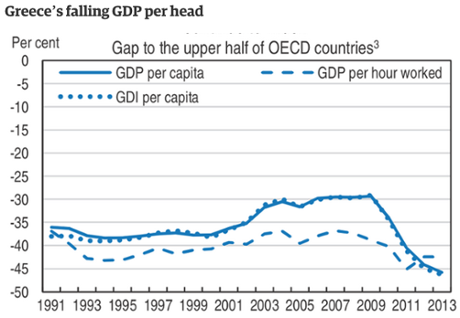

The OECD has also highlighted how Greece’s wealth tumbled, relative to rich countries, since the financial crisis began.

The OECD report highlights large increases in income inequality and poverty in Greece, alongside other countries hit hardest by the crisis: Iceland, Ireland and Spain.

Updated

The OECD is making another attempt to get finance ministers to take inequality seriously.

The thinktank told the G20 finance ministers’ meeting in Istanbul to prioritise growth-friendly measures such as educating low-skilled workers and getting more women into work.

Katie Allen has the full story: OECD: changes must cut inequality, not just boost economic growth

Tsipras’s speech marked a hardening of tone from the Greek government, points out analyst Wolf Piccoli:

Tsipras & Varoufakis alternating between the roles of good/bad cop. Not sure it will be enough to confuse #Greece’s creditors

— wolf piccoli (@wolfpiccoli) February 9, 2015

Updated

The Greek stock market has fallen back to a near one-week low this morning:

#Grèce : l'indice #ASE perd plus de 4% #Greece pic.twitter.com/Xc96XgAjfC

— IG France (@IG_France_) February 9, 2015

The selloff across European stock markets is picking up pace, sending the main indices deeper into the red.

Here’s the damage:

Traders blame the escalating Greek crisis, and also cite disappointing Chinese trade data overnight (exports fell 3.3% in January, suggesting global demand weakening.)

Ilya Spivak, currency strategist, at DailyFX, says:

“Comments from newly-minted Greek Prime Minister Alexis Tsipras rejecting his country’s EU/IMF bailout – raising the probability of so-called “Grexit” – compounded investors’ dour mood.”

Updated

Greek bond yields surge higher

Greek bonds are tumbling in value this morning, underlining how the crisis has escalated over the weekend.

This has driven the interest rate (yield) on its debt sharply higher, reflecting a greater risk of default.

The yield on Greece’s three-year bond has leapt to 19.15%, from around 18.1% on Friday night. That’s an alarmingly high level.

* Greek three-year bond yields up more than one percentage point at 19.15 pct - Tradeweb

— Fabrizio Goria (@FGoria) February 9, 2015

The yield on Greece’s 10-year bond has jumped too, from 10.4% to 11.1% this morning.

That follow’s Tsipras’s address to the Athens parliament, and also Alan Greenspan’s prediction that Greece will exit the eurozone.

Tsipras favours Greek jobless over creditors in defiant policy speech http://t.co/Gp4XqZvkR2 http://t.co/JvxTjf48ff

— Erik Wesselius (@erikwesselius) February 9, 2015

Updated

Analyst: Grexit is now a 50% chance

LNG’s Gary Jenkins adds:

In my view the possibility of Greece leaving the eurozone has increased with this speech from 35% to 50%. This Wednesday’s meeting of finance ministers will give us a good indication of whether or not Greece will remain in the eurozone.

Updated

Greek stock market falls after Tsipras speech

Over in Athens, the Greek stock market has opened with a rush of selling, sending the AGT index down over 4%.

Bank shares are leading the selloff, dropping by around 8%.

#Greece Athens stock exchange -4.15% after minutes in session, banks -8%

— Efthimia Efthimiou (@EfiEfthimiou) February 9, 2015

Greek assets seeing selling in early trade - ASE now down >4% and banking sector 8% aft PM rejected international bailout extension

— RANsquawk (@RANsquawk) February 9, 2015

The selloff is triggered by Alexis Tsipras’s no-holds-barred speech last night (see opening post for details)

His insistence that Athens will abandon its bailout programme and seek a bridging loan appear to have fanned the fears that Greece will tumble out of the eurozone.

Gary Jenkins, analyst at LNG Capital, sums up the mood:

I think it is fair to say that the speech given by the Greek Prime Minister Mr Tsipras to his parliament was a long way from being conciliatory. He said that ‘Our government’s irreversible decision is to implement in full our pre-election pledges,’ and that ‘Our government is not entitled to ask for a bailout extension. We are not entitled to ask for an extension of a mistake.’ He added that ‘We will fulfil the Eurozones’s rules but we will not agree to unreasonable budgetary primary surpluses.’

Just for good measure he added that he would ask for World War II reparations from Germany and increase the minimum wage.

Updated

While Greece flails under the yoke of austerity, Germany has exported more goods than ever before.

German seasonally-adjusted exports hit a record high in December, up by 3.4% month-on-month, data released this morning showed.

There was bad news for foreign companies looking to sell to Germany – imports dropped by 0.8% month-on-month. That helped to push Germany’s trade surplus to a record high.

German firms look well-placed to profit from the weaker euro too, now the ECB has embarked on quantitative easing......

#Germany| 2014 FULL-YEAR TRADE SURPLUS REACHES RECORD €217B pic.twitter.com/1tnoWbet29

— Ioan Smith (@moved_average) February 9, 2015

Updated

Italian Finance Minister Pier Carlo Padoan opens remarks at #G20 #IIFistanbul saying pleasure2be here "in a new capacity, same old problems"

— Harriet Torry (@HarrietTorry) February 9, 2015

The next nine days are crucial for Greece. The government must win a confidence vote on Tuesday, then sell short-term debt on Wednesday.

There are then three meetings with political leaders before next Wednesday, when the ECB decides whether to keep providing emergency liquidity to its banks.

Credit Agricole analyst Fred Ducrozet suggests this timeline could put pressure on the new government to shift its position:

Greece’s calendar: confidence vote (10); T-Bills auction (11); Eurogroup (11); EU summit (12); Eurogroup (16); ECB/ELA review (18).

— Frederik Ducrozet (@fwred) February 9, 2015

Could some Greek concessions be forced from the inside? Syriza very popular, but I guess this could always change if things go sour.

— Frederik Ducrozet (@fwred) February 9, 2015

The Mayor of London’s top economic advisor, Dr Gerard Lyons, has endorsed the Greek government’s plan to abandon the fiscal targets set by the Troika.

Varoufakis is game theorist & taking it to wire but his demand for 1.5% primary surplus reasonable. Current situation is not sustainable.

— Gerard Lyons (@DrGerardLyons) February 9, 2015

Economist Paul Ormerod wrote excellent piece last week in @CityAM on Game Theory & Greek strategy. Seems like it turned up notch yesterday.

— Gerard Lyons (@DrGerardLyons) February 9, 2015

European markets fall amid Grexit fears

European stock markets have fallen at the start of trading, as Greek crisis fears eat away at confidence.

The French CAC, Spanish IBEX and Italian FTSE MIB all shed around 1% at the open, while the FTSE 100 dropped 37 points, or 0.55%, to 6817 points.

Investors will have noted the Greek finance minister’s alarming comments yesterday. Yanis Varoufakis declared that the eurozone was a ‘house of cards’ that would collapse without Greece, and went on to claim that Italy’s debt situation is “unsustainable”.

That prompted Italy’s finance minister to tweet back that the Italian debt was quite sustainable, thankyouverymuchYanis.

.@Presa_Diretta Debito italiano solido e sostenibile. Dichiarazioni @yanisvaroufakis fuori luogo.

— PCPadoan (@PCPadoan) February 8, 2015

A day of bizarre statements, but the prize goes to Greek Finance Minister announcing Italian bankruptcy

— Bruno Maçães (@MacaesBruno) February 8, 2015

Over in Istanbul, finance chiefs at the G20 summit are fretting that Greece and its creditors will fail to reach a deal.

Timothy D. Adams, the president and chief executive of the Institute of International Finance, warned that time is running out. He told CNBC that both sides must stop playing to the galleries:

“I think there is still an opportunity for all sides to have a negotiation but I think (that is) narrowing pretty quickly so let’s hope we can find a way through this,”

“I think there is a way through this crisis but it requires cooler heads to prevail, (they need to) tone down the rhetoric and roll up their sleeves and get to work on a solution. I believe there is a solution but the rhetoric doesn’t help.”

G-20 leaders plea for 'cooler heads' in Greek crisis http://t.co/VSvv9L39OG #Greece pic.twitter.com/cVkNrqC8xR

— CNBCWorld (@CNBCWorld) February 9, 2015

Greek bailout crisis intensifies as Tsipras stands firm

Good morning, and welcome to our rolling coverage of the Greek bailout crisis, the eurozone, the world economy, the financial markets and business.

The Greek debt crisis remains the biggest issue on the table this week, after Greece’s prime minister raised the stakes with its creditors by insisting it will not stick to its old bailout deal.

In a passionate address to the Athens parliament last night, Alexis Tsipras insisted that his government would deliver on its pre-election pledges, intensifying the crisis.

Athens will not seek an extension when its existing bailout expires at the end of February, he said. Instead, he will seek a new “bridge agreement” to cover Greece’s funding needs until June.

As Helena Smith wrote last night:

“We see hope, dignity and pride returning to Greek citizens. Our obligation and duty is not to disappoint them,” Tsipras told the 300-seat house. “We realise that negotiations [with foreign lenders] won’t be easy … but we have faith in our struggle, because justice is on our side.”

Declaring his administration “a government of national salvation”, Tsipras said he would also pursue claims to win back from Germany wartime loans that Greece had been forced to make to Nazi occupiers. “I can’t overlook what is an ethical duty, a duty to history … to lay claim to the wartime debt.”

Full story: Tsipras favours Greek jobless over creditors in defiant policy speech

Tsipras’s speech has blown away any expectations that the Athens government might cave in, after failing to make much obvious progress during last week’s tour of European capitals.

There’s little sign of enthusiasm for a bridging loan among Greece’s partners in the eurozone; on Friday, the head of the Eurogroup of finance ministers, Jeroen Dijsselbloem, declared “We don’t do bridging loans.”

It’s heading towards a major clash.....as Michael Hewson of CMC Markets explains:

If investors were hoping for a more emollient tone from the new Greek government in light of last week’s events, and the ECB’s intervention in removing its collateral waiver, they were in for a rude awakening as PM Tsipras reinforced his determination to end the bailout at the end of this month, insisting on some form of bridging finance, as well as a determination to “honour and fully implement our pre-election policy commitments, fully respecting the will of the people”

The speech sets the scene for another crunch week in the long-running financial crisis.

Finance ministers and central bank chiefs are gathered in Istanbul today for talks on the global economy; on Wednesday eurozone finance ministers hold an extraordinary meeting to discuss Greece, and then European leaders hold a summit on Thursday.

And with former Federal Reserve chairman Alan Greenspan predicting a Grexit, and UK chancellor George Osborne stepping up Britain’s preparations for a crisis, the situation could easily escalate again this week.

Ukraine's set to have a worse week than Greece. But it's close.

— ian bremmer (@ianbremmer) February 8, 2015

I’ll be tracking all the main developments through the day, as usual....

Updated