Closing summary: Greece re-opens banks and pays off some debts

Our main story tonight: Greece has taken a step back to normality after its banks reopened following three weeks of closures and receipt of a €7.2bn (£5bn) loan, with almost all of it spent on repaying debts.

After a quieter day by recent eurozone standards, a closing summary before we go:

Bank branches across Greece have reopened today, as the financial restrictions that have constrained the country for the last three weeks are relaxed, a little, following last week’s bailout deal.

Queues formed early at branches in Athens and Thessaloniki, but there were no reports of panic. In Athens, our correspondent Helena Smith reports that bank officials were, in fact, surprised at how quiet it was.

The banking sector is still subject to capital controls, which mean people can’t withdraw more than €420 per week from their accounts, or transfer money overseas. Here’s a list of the restrictions.

Greek shareholders aren’t allowed to buy or sell stock today, as the Athens exchange remains closed. It may open later this week.

The European Commission sent a $7.2bn bridge loan to Greece today; the money was used to repay a maturing debt repayment owed to the ECB, and to cover outstanding bills to the IMF. The IMF confirmed Greece has now cleared its arrears with the fund.

Last week’s austerity measures are already hitting Greeks, who are now paying higher VAT rates on many basic goods.

The IMF has announced that Maurice Obstfeld, an expert on optimal currency unions, will take over from retiring chief economist Olivier Blanchard.

On financial markets, European share indices have risen as Greek worries recede, yields on Italian, Portuguese and Spanish government bonds have fallen and safe-haven favourite gold has sold off sharply.

Thanks for reading and all the comments. We will be back in the morning with the latest economic and business news from the UK, the eurozone and beyond.

On a day when the Greek banks opened their doors for the first time inthree weeks, the debate about future funding needs seems far away.But our economics correspondent Phillip Inman asks what lies ahead for Greece’s battered financial sector.

He writes:

Plenty of dangers lie in wait for Greek banks. Already short of cash, they may need lots more when stress tests of their solvency are carried out in a month or two.

And unable to access the international money markets, they will be in a similar position to the Greek god Telephus, who was wounded by Achilles and yet needed Achilles to return as a doctor before he could be healed. The Greek banks, stripped of many of their assets by the European Central Bank, will need the ECB to make a re-appearance in Athens to aid their recovery...

A couple of months from now, the story could take a grim turn. Not only will hundreds of millions of deposits have been withdrawn in that time, the weakening effects of a broader economic slowdown will have taken their toll.

The full analysis from Phillip:

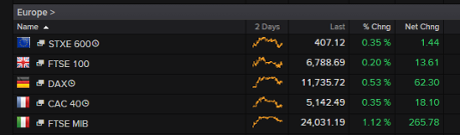

European stock markets have closed higher as worries about Greece recede.

The main share indices have not managed to hold on to all their early gains but are still well within positive territory.

The Italian FTSE MIB has lead the way, up more than 1.1%:

On government bond markets, the ebbing away of Grexit fears has also helped bring down yields in Southern Europe. Yields on Portuguese, Spanish and Italian 10-year government bonds are all lower.

Of course, the big move on financial markets today, as reported earlier, has been in the old safe-haven favourite: gold.

The gold price fell to its lowest for more than five years as the precious metal was buffeted by the deal to avert a Greek bankruptcy, a potential US interest rate increase and a sharp sell-off in China. It has since rebounded from a low of $1,088.05.

Laith Khalaf, senior analyst at Hargreaves Lansdown comments:

Gold has struggled against a backdrop of global economic recovery and a strengthening dollar, and the recent sell-off appears to have come on the back of the Chinese central bank reporting its gold holdings, which disappointed analyst’s expectations.

The yellow metal is traditionally seen as a store of value and a protection policy against catastrophe, both attractive features in recent years given the depth of the financial crisis and the devaluation of fiat currencies by central bankers cranking the printing presses. However those worries have receded, and with them so has the gold price.”

Here is our news story on today’s sharp moves for gold:

Helena Smith has also been in the vaults of the Bank of Greece talking to Ioannis Zafeiropoulos, who has oversight of some 7,500 safety deposit boxes – held behind iron bars and huge steel doors. She reports:

An official at the bank for the past 31 years,Zafeiropoulos had spent 10 days drawing up a contingency plan. His worry: that once the banks reopened, the vaults might be stormed by savers fearing the country’s enforced ejection from the euro zone.

“How was I going to cope when no more than four people can be in a vault at the same time?” he asked. “I had to devise a plan but instead of 3,000 people turning up as I had thought we’ve had less than a hundred. We’ve been joking about how disappointing it’s been.”

All morning, he said, he had been asking himself why.

“People have behaved so responsibly, so maturely today,” said Zafeiropoulos. “And I think that’s because they have probably said ‘now that the banks have opened, they are not going to close again and what on earth will I do with the contents of a safety box? Where will I hide my money or my jewels if I do take them out?’” he murmured.

“This crisis is never going to end. Do the sums, see how much they say we owe them,” he said referring to the EU, ECB and IMF that have kept the country afloat “and you’ll understand it will not be ending anytime soon.”

The reopening of Greek banks may have been highly symbolic for the crisis-hit country’s economy but in many ways today has defied expectations. Our correspondent Helena Smith reports from Athens.

The opening of Greek banks on Monday was not without symbolism. After 21 days of being firmly closed, the sight of their shutters going up was uplifting both for Greeks and their debt-stricken economy - an economy that with the added restriction of capital controls has suffered immeasurable damage in the meantime.

“What economy can work without its banks?” asked Spyros Kouroumbiotis, a pensioner in the queue at the Bank of Greece waiting to pay his taxes. “As an economist I still help family with their business and I can tell you it’s been a huge ordeal. Exports have stopped, imports have stopped, nothing has worked because it’s been impossible to pay anyone.”

But on Monday it was the manner of their re-opening that surprised officials most. Quite quickly it became evident that the panic-stricken deluge of branches many had feared was simply not happening. Greeks, who have spent the best part of five years internalising the crisis – of getting used to bad news – had reacted with their feet: they had stayed home. And those who hadn’t were willing to stand in neat orderly queues, motivated to large degree by the desire to keep up with annual taxes and utility bills.

More from Helena later

Updated

Sticking with the IMF, the fund has just announced the successor to retiring chief economist Olivier Blanchard. Professor Maurice Obstfeld takes over the role of economic counsellor and director of the IMF’s research department in September, IMF managing director Christine Lagarde announces.

Describing Blanchard’s successor, the IMF says: “A Professor of Economics (and former Chair of the Department of Economics) at the University of California, Berkeley, Obstfeld has advised many governments and consulted at central banks all over the world. He is currently serving as a member of President Obama’s Council of Economic Advisers, on leave from Berkeley.”

Obstfeld is the co-author of two textbooks on international economics—Foundations of International Macroeconomics with former IMF Economic Counsellor Kenneth Rogoff, and International Economics with Paul Krugman and Marc Melitz.

Lagarde comments in a statement:

“I am thrilled to have Maurice join us at the Fund. His outstanding academic credentials and extensive international experience make him exceptionally well placed to provide intellectual leadership to the IMF at this important juncture. He is known around the globe for his work on international economics and is considered one of the most influential macroeconomists in the world.”

“The position of Economic Counsellor is of fundamental importance to the IMF’s ability to provide its global membership with the best possible independent analysis and policy advice. I am confident that we have found an exceptional candidate in Maurice to take this work forward.”

Ferdinando Giugliano at the Financial Times notes that Obstfeld is an expert on optimal currency areas. The eurozone will give him plenty to get his teeth into

Maurice Obstfeld,the IMF's new chief economist, is an expert of optimal currency areas.His 2013 views on the eurozone pic.twitter.com/PEghuNUOjL

— Ferdinando Giugliano (@FerdiGiugliano) July 20, 2015

You can read more about Obstfeld on his homepage, where there are links to his recent papers, including on the eurozone, like this one on “some lessons of the euro crisis”.

Updated

Further to that statement from the IMF on Greece no longer being in arrears to the Fund, as a refresher when the country missed a €1.6bn payment on 30 June it became the first developed country to default to the IMF. It joined a club that includes Zimbabwe, Somalia and Sudan, which have all fallen into arrears with the fund.

Until that point no missed payment had been more than £890m (€1.3bn). So Greece’s missed payment of €1.6bn was bigger than any previous case of arrears.

But it was short-lived and Greek officials had already said earlier today that a €2.05bn payment to the Washington-based fund was underway, representing two missed payments – that €1.6bn and another smaller one that followed in July. As just reported, the IMF says the money has now been paid back.

Now Greece has cleared its arrears at the IMF, it is entitled to more loans from the fund.

IMF confirms Greek repayment

The International Monetary Fund (IMF) has just issued a brief statement confirming Greece has repaid its arrears to the fund, as had been expected after Greece got a bridging loan to cover its most pressing debts.

Gerry Rice, the IMF’s director of communications says:

“I can confirm that Greece today repaid the totality of its arrears to the IMF, equivalent to SDR 1.6 billion (about €2.0bn). Greece is therefore no longer in arrears to the IMF.

“As we have said, the Fund stands ready to continue assisting Greece in its efforts to return to financial stability and growth.”

Back to the main events in the eurozone now and our reporter in Brussels, Jennifer Rankin, has been looking at Greece’s ‘now you see it, now you don’t’ bridging loan.

She reports:

The Greek money merry-go-round carries on in full swing as Athens received a €7.2bn (£5bn) loan from the EU and immediately spent almost all of it on repaying debts.

Greek officials confirmed on Monday they had begun paying back international lenders, not long after the emergency bridging loan arrived in the Greek government’s bank account.

The EU agreed the loan on Friday to enable Athens to meet urgent debt repayments and clear arrears, both necessary hurdles if the Greek government is to get a three-year bailout worth up to €86bn.

Greece’s bank branches are open for the first time in three weeks, but capital controls still stop people from withdrawing more than €420/week.

The full story:

Jennifer also shares a possible hint of missing all those eurogroup meetings. Be careful what you wish for....

Just realised this is my fifth week in Brussels, but only the first w/o a eurogroup.

— Jennifer Rankin (@JenniferMerode) July 20, 2015

Updated

FT up for sale?

Regular readers of this blog will have become very familiar with the Financial Times’ excellent reporters in the field who have covered the Greek crisis tirelessly in recent months. News is just breaking that their pink paper could be moving to new owners.

Bloomberg reports that owner of the FT, UK-listed Pearson, is “exploring a sale of the Financial Times after receiving interest from potential buyers, according to people familiar with the matter.”

Bloomberg says Pearson is sounding out possible bidders and a sale may value the business at as much as £1bn.

The full Bloomberg story is here.

Meanwhile the FT’s Brussels bureau chief Peter Spiegel has this take on report.

For an extra couple million, I'll throw in my troika report collection https://t.co/LlV4b60X3g

— Peter Spiegel (@SpiegelPeter) July 20, 2015

That £1bn price in the Bloomberg story, incidentally, is the same the number speculated on by analysts back in 2012 when talk swirled of a FT sale by Pearson.

Turning to the UK briefly, the wave of rate hike remarks from Bank of England policymakers last week, have kept the pound strong today.

After BoE governor Mark Carney signalled that the first rise in interest rates since the global financial crash could take place around the turn of the year, traders have been re-positioning themselves to price in the chances of a hike before 2016.

That is good news for British holidaymakers jetting off abroad, whose pounds will now stretch further. It is not so welcome, however, for UK exporters given they had already been reporting pressure from a strong pound, given it makes UK goods more expensive to overseas buyers.

Today the pound is weaker against the euro but at €1.4338 still not far off a seven-and-a-half year high hit on Friday.

Against a trade-weighted basket used by the BoE, the pound is also near last week’s seven-and-a-half year high.

Summary: Greece takes a step towards normality

A quick recap.

Bank branches across Greece have reopened today, as the financial restrictions that have constrained the country for the last three weeks are relaxed, a little, following last week’s bailout deal.

Queues formed early at branches in Athens and Thessaloniki, but there were no reports of panic.

That’s partly because the banking sector is still subject to capital controls, which mean people can’t withdraw more than €420 per week from their accounts, or transfer money overseas. Here’s a list of the restrictions.

Greek shareholders aren’t allowed to buy or sell stock today, as the Athens exchange remains closed. It may open later this week.

The European Commission is sending a $7.2bn bridge loan to Greece today; the money is being used to repay a maturing debt repayment owed to the ECB, and to cover outstanding bills to the IMF.

Last week’s austerity measures are already hitting Greeks, who are now paying higher VAT rates on many basic goods.

Many goods and services become more expensive on Monday as a result of a rise in Value Added Tax approved by Parliament last week, among the first batch of austerity measures demanded by Greece’s creditors. Photograph: Thanassis Stavrakis/AP

European stock markets have risen this morning, with the main indices up around 1% in a fairly quiet trading session. Greek fears have receded, for the moment at least.

Greece’s finance minister, Euclid Tsakalotos, has said farewell to one deputy this lunchtime, and welcomed another.

Nadia Valavani (the outgoing deputy fin. min.) resigned last week in protest at Greece’s new bailout programme, and is being replaced by Tryfon Alexiadis:

Alexiadis had better hit the ground running, as the Greek government must pass a second set of austerity measures later this week (probably on Wednesday night).

Updated

Here’s a technical explanation of how Greece’s new bridge loan will work (thanks to Katy Lee of AFP)

European Commission confirms $7.16 bn loan paid to Greece so they can now pay ECB & IMF (see gif for explanation) pic.twitter.com/3xxPq6pU1F

— Katy Lee (@kjalee) July 20, 2015

Updated

The EC’s chief spokesman, Margaritis Schinas, is fielding a few questions on Greece:

Asked about troika v institutions, commission spokesman says he wouldn't like "to become lost in terminology". #Greece

— Jennifer Rankin (@JenniferMerode) July 20, 2015

@Elbarbie Just referendums, I guess

— Peter Spiegel (@SpiegelPeter) July 20, 2015

Greece gets bridge loan, and immediately spends it

Greece won’t have much time to enjoy the €7bn bridge loan organised by the European Union last week.

EU officials have just announced that this financing has been sent to Athens today, following several days of work by Brussels officials.

The €7.16bn bridge loan just sent to #Greece, says @Mina_Andreeva

— Peter Spiegel (@SpiegelPeter) July 20, 2015

But over in the Greek capital, the money is already being spent to address Greece’s latest debt demands.

Government officials have confirmed that the process of repaying $4.2bn to the European Central Bank today has begun. That means Greece will avoid defaulting on its obligations to the ECB, which would have had very serious consequences.

Greece also plans to clear its arrears to the International Monetary Fund, by sending €2.05bn over to Washington. That will cover the €1.6bn repayments due in June, which was missed as Greece staggered out of its previous bailout, plus a second payment due last week.

So in short, Greece’s creditors have loaned it more money, so it can repay its creditors.

The cash spends hardly any time in Athens at all, before being yanked back out again. Maybe it should be renamed a bungee loan.....

Commission confirms #Greece has received €7.2 bn bridge loan. Now money can go straight out the door to repay @ecb and other creditors.

— Jennifer Rankin (@JenniferMerode) July 20, 2015

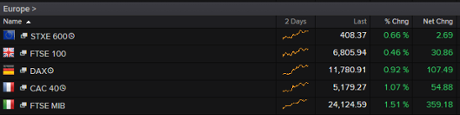

But while shares rally, the price of gold has hit its lowest level since early 2010:

Europe’s stock markets are all up this morning, as worries over Greece recede.

The Italian FTSE MIB is leading the way, up 1.5%, followed by Spain, France and Germany:

City experts appreciate that the Greek crisis isn’t over.

Connor Campbell, financial analyst at SpreadEx, explains:

After a weekend (mercifully) free of big Eurozone drama, the semblance of normality returned this morning as the Greek banks opened for the first time in 3 weeks.

But there is a reason why these re-openings merely provide a surface level simulation of a working economy, not the real thing; capital controls remain in place, with the Greek public allowed only €420 a week (a marginal adjustment of the previous €60 a day) alongside a host of other restrictions.

But rather than watching Athens and Brussels again, many traders are concentrating on events up at St Andrews:

I blame #British weather for light newsflow, #TheOpen continues on Mon for first time since 1988, traders watching instead of trading #Golf

— RANsquawk (@RANsquawk) July 20, 2015

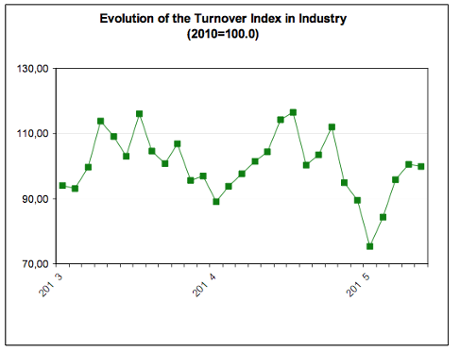

Greece’s factories was struggling even before capital controls were imposed at the end of June, new data shows.

Turnover across the industrial sector shrank by 4.2% year-on year in May, according to stats body Elstat.

That follows a 4% annual decline in April, and a very serious slide at the start of the year:

Elstat reports that mining and quarrying turnover slumped by 8.3%, while manufacturing turnover dropped by 4.2%.

Krugman: I may have overestimated the competence of the Greek government.....

Quote of the Day goes to Paul Krugman, the Nobel Prize-winning economist.

He’s admitted to CNN’s Fareed Zakaria that he didn’t anticipate that Alexis Tsipras wouldn’t have a Plan B, in case Greece’s creditors didn’t fold.

Krugman on assuming that Greece had an exit plan from the Euro:

“…it didn’t even occur to me that they would be prepared to make a stand without having done any contingency planning ...amazingly - they thought they could simply demand better terms without having any backup plan. So certainly this is a shock. But, you know, in some sense, it’s hopeless in any case. …it’s not as if the terms that they were being offered before were feasible. I mean, the new terms are even worse, but the terms they were being offered before were still not going to work. So I, you know, I may have overestimated the competence of the Greek government.”

Krugman also believes that Greece will eventually leave the eurozone, unless it is granted “enormous” debt relief.

Paul Krugman on CNN: "I may have overestimated the competence of the Greek government" http://t.co/fwE2YZHpLU

— Jennifer Rankin (@JenniferMerode) July 20, 2015

The re-opening of Greece’s banks appears to be operating smoothly, judging by this photo from a National Bank branch in Athens:

Today’s Greek VAT rise is the third since the country’s austerity programme began, five years ago:

VAT on basic foodstuffs 2005: 8% 2006: 9% 2010: 11% 2011: 13% 2015: 23% Sharing the burden fairly & proportionately. https://t.co/zqlGhVSuGh

— Theodora Oikonomides (@IrateGreek) July 20, 2015

Greece's VAT rise hits customers

Greek consumers are facing higher prices today, as the sales tax hike demanded by its creditors is applied.

Sweeping VAT changes mean some food stuffs, restaurant meals and education services cost more. And even death (life’s other certainty alongside those taxes) will be more expensive:

Associated Press has the details:

The VAT rose from 13% to 23%, making some meats, cooking oils other than olive oil, cocoa, vinegar, salt, flowers, firewood, fertilizer, insecticides, sanitary towels and other basics all more expensive.

Services hit by the new VAT increases include restaurants and cafes, funeral parlors, taxis, cramming and tutorial schools very popular with Greek students seeking to make up for the deficiencies of the school system language institutes and computer learning centers. Public transport fares are expected to rise early next month.

Greece 'gives order to repay ECB and IMF'

Bloomberg is reporting that Greece has spent almost all of the €7bn bridge loan hammered out by the eurozone on Friday.

*GREECE SAID TO GIVE PAYMENT ORDER FOR EU 6.8BN TO CREDITORS, COVERS ECB, IMF, CENTRAL BANKS: FIN MIN OFFICIAL (Bloomberg)

— Alberto Gallo (@macrocredit) July 20, 2015

If so, Greece would have met today’s repayment to the European Central Bank, and covered its arrears to the International Monetary Fund (having missed two payments in recent weeks)

A bridge financing that'd be quickly spent. *GREECE SAID TO GIVE ORDER FOR EU6.8 BLN PAYMENTS TO CREDITORS; ECB, IMF, CEN BANK

— Frederik Ducrozet (@fwred) July 20, 2015

More to follow....

Customers at this National Bank branch in Athens received little numbered tickets to allocate places in the queue:

But heated conversations with the branch manager were on a strictly ‘first-come, first-served’ basis.....

Updated

Across central Athens, customers waited patiently at this Alpha Bank branch:

Although Greece’s banks are reopening, customers will find that many services are still off limits.

Macropolis, the news and analysis site, has compiled a list of the current restrictions, on top of the €420/week limit on cash withdrawals.

Here’s some highlights:

- Cashing-in of checks or payments via letters of guarantees are allowed only if the money is credited in a bank account.

- Withdrawals from credit or prepaid cards in Greece or abroad are forbidden.

- Money transfers abroad are forbidden including use of credit, prepaid or debit cards for cross country payments.

- The use of credit or debit cards abroad is allowed only for goods or services purchases without cash and up to the limit set by each bank.

- New sight or savings accounts cannot be opened, while dormant accounts cannot be reactivated.

- Early, partial or full loan repayment is forbidden except repayment via cash or money transfer from abroad.

- Early, partial or full termination of a time deposit is forbidden unless the amount of the early partial termination is used for payment of tax, social security or bank loan obligations, payroll payment within the same bank, payment of hospital or educational expenses.

Greek banks open again after 3 weeks but there's really not that much you can do inside them https://t.co/cKemBkhvXE #Greece #euro

— Nick Malkoutzis (@NickMalkoutzis) July 20, 2015

After months of drama, the financial markets are now more relaxed about Greece, according to David Cumming, head of UK equities at Standard Life Investments.

He told Radio 4’s Today Programme that:

“The key question is: is the euro going to break up because of the Greek crisis, and the answer is no it isn’t. The second issue is when are we going to stop talking about it because it’s corrosive at the margin for business confidence in Europe. The answer is relatively soon.

From a market perspective it [Greece] has become less of an issue”.

(via the BBC)

Queues also formed outside National Bank branches in Athens, but it all looks calm:

Customers queued outside this National Bank branch in Thessaloniki, Greece’s second city, this morning, as it reopened for the first time since late June:

Updated

The head of Greece’s banking association, Louka Katseli, hopes that Greeks will put money back into their accounts:

She told Skai television yesterday:

“Tomorrow when the banks reopen and normality is restored, let’s all help our economy.

If we take our money out of chests and from our homes - where they are not safe in any case - and we deposit them in the banks, we will strengthen the liquidity of the economy,”

(quote via Reuters).

Adea Guillot, journalist with Le Monde, is tweeting from a bank branch in Athens:

— adea guillot (@Adea_Guillot) July 20, 2015

Yiannis,agent de securite ds une banque d'Athenes: tout se passe tres bien. Les gens sont calmes et philosophes. pic.twitter.com/UtRlFxqy15

— adea guillot (@Adea_Guillot) July 20, 2015

Athens stock market won't open today

Traders on the Greek stock market must be itching to get back to work after their three week delay. But they’ll have to be patient.

The Athens exchange will remain closed today, even though Greece’s banks are opening up to customers right now.

According to spokeswoman Alexandra Grispou, the new capital controls degree issued on Saturday “doesn’t allow us to open today.”

The exchange could open in a couple of days, according to Evangelos Charatsis, managing director of Beta Securities, a financial services firm.

He told Bloomberg TV that some staff took holidays once capital controls were imposed three weeks ago, adding:

Others worked part time, then went to the beach.

Introduction: Greek banks reopening today

Good morning, and welcome to our rolling coverage of the Greek debt crisis.

Across Greece, banks are reopening after a three-week hiatus. Customers are flocking to their local branches for the first time since Alexis Tsipras’s fateful decision to call a referendum on the country’s bailout terms.

Greek banks to reopen for first time in 3 weeks. But long queues at ATM's remain as CNBC shows http://t.co/GzCWxQxQ1d pic.twitter.com/PVD8tFb3j3

— Holger Zschaepitz (@Schuldensuehner) July 20, 2015

But the situation remains far from normal, with capital controls still in place. Customers are only allowed to take out €420 per week (a slight tweak to the €60 per day limit).

But as Associated Press explains, that’s only the start....

Bank customers will still not be able to cash checks, only deposit them into their accounts, and will not be able to get cash abroad with their credit or cash cards, only make purchases.

There are also restrictions on opening new accounts or activating dormant ones.

Here’s our latest news story explaining the situation:

Today had (until recently) been inked in as the moment when Greece’s battle against bankruptcy floundered. It is is due to make a $3.5bn bond repayment to the ECB today (plus $700m in interest), which would have been impossible before last week’s bailout deal.

Instead, the $7bn bridge loan agreed last week should arrive just in time to repay Greece’s creditors.

As Bloomberg explains:

Greece has reached the deadline it couldn’t afford to miss, for a bill it can finally afford to pay.

Greece’s Real Crisis Deadline Arrives With ECB Debt to Pay

But this crisis isn’t over.

Negotiations over Greece’s bailout are going to take several weeks, perhaps a month.

And Alexis Tsipras’s position remains precarious. Last Friday’s night’s reshuffle has sidelined several key dissenters, breaking the PM’s links to the far-left faction of Syriza and making an autumn election more likely.

We’ll be tracking all the main events through the day....

Updated