PPS: President Obama has weighed in on the crisis. Here’s what he told reporters in Washington (during a press conference with Italy’s PM)

Greece needs to initiate reforms; they need to collect taxes; they need to reduce their bureaucracy.

When the new PM (Alexis Tsipras) came in, I called him and recognised you need to show your people that there’s hope, that you can grow, but you have to show those who are extending credit, who are supporting your financial system that you’re trying to help yourself; that requires making the tough decisions.

Obama says Greece needs to made "tough decisions" http://t.co/6N7uyYcpMO

— fastFT (@fastFT) April 17, 2015

PS: Keep an eye on Paris this weekend for Greek developments:

Greece and institutions overseeing bailout to hold technical talks in Paris this weekend, a finance ministry official says - DJ

— CNBC Now (@CNBCnow) April 17, 2015

Closing summary: Another day of Greek drama

OK, it’s been a long week, so let’s nail the lid down with a particularly brisk catch-up.

Greece has been given until May 11 to satisfy its creditors. EU commissioner Pierre Moscovici identified a eurogroup meeting that day as the final chance to reach agreement about economic reforms, to unlock €7bn of bailout funds.

UK chancellor George Osborne has warned that the mood at this year’s IMF Spring Meeting is notably gloomy; Greece hangs over every meeting, he claimed.

Germany finance chief Wolfgang Schauble added to the gloom, saying there is no sign of a deal in the weeks ahead.

But some of Greece’s largest creditors will go “a long way” to keep it in the euro, says Bloomberg.

Greek fears send shares down sharply in Europe today.

The financial world has been disrupted by a major systems outage at Bloomberg.

City workers say they were unable to trade for hours.

While in the UK, the unemployment rate has hit its lowest since July 2008. Full coverage of that starts here.

Have a good weekend all. GW

Bloomberg are reporting tonight that some of Greece’s largest creditors are unwilling to allow it to exit the eurozone.

Here’s a flavour

Greece’s major creditors are not ready to let the country drop out of the euro as long as Prime Minister Alexis Tsipras shows willingness to meet at least some key demands, according to two people familiar with the discussions.

Chancellor Angela Merkel will go a long way to prevent a Greek exit from the single currency, though only so far, one of the people said. Every possibility is being considered in Berlin to pull Greece back from the brink and keep it in the 19-nation euro, the person said.

For all the foot-dragging in Athens, some creditors are willing to show Greece more flexibility in negotiations over its finances to prevent a euro exit, the second person said. The red line is that the Syriza-led government shows readiness to commit to at least some economic reform measures, said both people, who asked not to be named discussing strategy.

“Our view is that Greece is not going to exit the euro,” Stephen Macklow-Smith, head of European equity strategy at JPMorgan Asset Management in London, said in a Bloomberg Television interview on Friday. While both sides have “very entrenched positions” in the negotiations, “if you look at the way the euro-zone crisis has developed, in every case what you’ve seen is in return for firm action you get concessions.”

Full story: Greece’s Main Creditors Said to Be Unwilling to Allow Euro Exit

Stop me if you’ve heard this one before about Greece http://t.co/l1inlSr0Py pic.twitter.com/XEsf3F1dcJ

— Matt O'Brien (@ObsoleteDogma) April 17, 2015

And I guess we shouldn’t be surprised that those who are who are owed a lot of money by Greece don’t want to risk a default.

*GREECE'S MAIN CREDITORS SAID TO BE UNWILLING TO ALLOW EURO EXIT You surprised? Natch they'd like their money back and pref the EU to sub it

— Polemic Paine (@PolemicTMM) April 17, 2015

Greece feels familiar. Done "about to run out cash", "may miss payment" & "will Russia step in?" and are at the "red lines" stage. Again.

— Duncan Weldon (@DuncanWeldon) April 17, 2015

And here’s one reason that Greece might have more funds at its disposal than some thing:

Greek gov't is about to pass a bill that will make it mandatory for state entities & pension funds to place their assets with the state.

— Yannis Koutsomitis (@YanniKouts) April 17, 2015

Remember that claim that Greece was scraping the bottom of the barrel to meet its obligations? It’s just been denied:

- GREECE DENIES REPORT THAT IT NEEDS TO TAP ALL REMAINING CASH RESERVES TO PAY PENSIONS AND WAGES - FINANCE MINISTRY

Updated

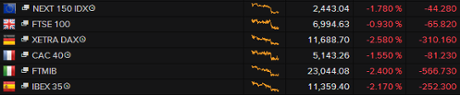

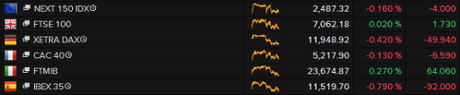

European markets post heavy falls

After a day of heavy selling, European stock markets have all closed deep in the red tonight.

The German DAX, Spanish IBEX and Italian FTSE MIB all tumbled more than 2%, as fears over Greece stalked the trading floors. The French CAC wasn’t far behind, down 1.6%.

In London, Grexit fears helped to blow the FTSE 100 index of top shares back below the 7,000 point mark. It lost fell 65 points, or almost 1%, to finish the day at 6994.

Greece wasn’t the only factor hitting shares, as Jasper Lawler of CMC Markets explains:

Europe’s stock markets extended a week of heavy losses on Friday, spooked by changes in Chinese trading regulations, an outage in Bloomberg terminals and Greece drifting closer to the brink.

Having failed to hold onto new record highs yesterday, Britain’s FTSE 100 joined in on the selling frenzy and headed back below 7000, its lowest in over a week.

Chinese regulators altered rules to encourage institutional short selling and banned trading on over the counter or non-exchange-listed securities using leverage. The rules were aimed at adding a bit more two-sidedness, but given Chinese equities have been going almost vertically up, that second side could only be down.

The Bloomberg terminal outage delayed a UK treasury auction and no doubt delayed, if not prevented numerous other bond deals. The modern way of getting a trade done is through Bloomberg chat, so without it, traders were a bit at a loss. Of course there is always a telephone if the deal is urgent.

What is this thing on my desk? A *phone*, you say? How does it work? http://t.co/LbOaiAdaIM #BloomiesOutage pic.twitter.com/0BsF2QMg4L

— Katie Martin (@katie_martin_FX) April 17, 2015

Another flurry of newsflashes from Washington.

This time, from Yanis Varoufakis following his meeting with ECB president, Mario Draghi.

Greek FinMin Varoufakis: Draghi meeting lasted an hour, he said he wants a resolution soon to help #Greece grow. /via @livesquawk #ECB

— Yannis Koutsomitis (@YanniKouts) April 17, 2015

Bloomberg has denied that today’s system wipeout was caused by a can of Coke being spilled on a server, as was rumoured earlier today:

@Bloomberg has stressed that Coke was not to blame for the outage today not was cyber crime.They're in talks with customers re compensation

— Joe Lynam BBC Biz (@BBC_Joe_Lynam) April 17, 2015

A weak end to the trading week:

Stocks selling off as global jitters grip the market: http://t.co/cmlRpNTB3q pic.twitter.com/4UDJR4CKPw

— MarketWatch (@MarketWatch) April 17, 2015

Service has been fully restored. We apologize to our customers for the disruption.

— Bloomberg LP (@Bloomberg) April 17, 2015

The selloff is accelerating in late trading; Germany’s DAX is now down almost 2.5%, or 290 points.

The Greek crisis is partly to blame. R.J. Grant, associate director of equity trading at KBW, has told WSJ that:

“Obviously Greece is back in focus today, and there’s a little bit of trepidation heading into the weekend.”

Earlier today, the European Commission revealed that technical officials involved with the negotiations will meet on Saturday.

The "Brussels Group" of #Greece bailout negotiators to meet tomorrow (Saturday), according to @EU_Commission spokeswoman

— Peter Spiegel (@SpiegelPeter) April 17, 2015

Just in: Bloomberg has said that its service is now “fully restored” after today’s global wipe-out.

It’s not clear that Greece has enough funds to reach this new May 11 deadline, without any funds from its creditors.

The government must pay public sector wages and pensions at the end of this month; Reuters is hearing that this will pretty much clear Athens’ cash reserves out.

***Greece needs to tap all remaining cash reserves of 2 bln Euros to pay salaries, wages at end-April - finance ministry sources - RTRS

— Fabrizio Goria (@FGoria) April 17, 2015

That will make it tricky to meet €900m of IMF repayments due in May, but Greece could potentially tap other reserves, such as state pension funds.

Updated

The Greek stock market has just posted a 3% tumble, as growing anxiety over Greece’s future in the eurozone hit shares in Athens.

Bank shares led the selloff, finishing the day down 5.5%.

Here are George Osborne’s full quotes on Greece’s debt negotiations today, via our man in Washington, Phillip Inman:

I would say that the situation in Greece is the one that at the moment is the most worrying for the global economy, and the discussions about Greece have pervaded every meeting. The mood is notably more gloomy than at the last international gathering and it’s clear now to me that a misstep or a miscalculation on either side could easily return European economies to the kind of perilous situation we saw three to four years ago.

The crunch appears now to be coming in May, and it would be a mistake to think that the UK would be immune to a return to this instability in European financial systems and the European economy, and of course it would be therefore the very worst moment for there to be any confusion about the direction of British economic policy or for a change of direction from the plan that we have pursued. That plan in the UK is building up resilience, and we need resilience for moments like this.

Osborne also spoke about the UK:

It’s important to help countries affected by Ebola and I’m proud that the UK is the largest contributor to the IMF trust. You will have heard the very positive comments about the British economy, and British economic policy, from the managing director of the IMF, Christine Lagarde and indeed from my German opposite number Wolfgang Schauble.

And I agree with them that the British economy is one of the brighter spots in the world economy at the moment, and that’s confirmed by the IMF forecasts which show the UK as the second fastest growing economy in the G7 in the next two years, having been the fastest growing in 2014.

Which brought him onto today’s unemployment data.

And of course all of that has been more than reinforced by the employment figures we saw this morning, which show a record number of people in work. They show the claimant count at its lowest level since 1975 and they confirm that under this government two million jobs have been created. So the British economy is a job creating machine, and we have set out, as the Conservative Party, plans today to go on creating jobs – two million further jobs – in the next Parliament.

Updated

IMF's Poul Thomsen says Grexit risks should not be underestimated, would like to simplify/ slim down the Greek program further

— Katerina Sokou (@KaterinaSokou) April 17, 2015

The International Monetary Fund is adding its weight to the pressure on Greece to produce credible reforms soon.

But crucially, one of its top officials - Poul Thomsen - has said that the programme also needs to be changed. Thomsen, as regular readers will remember, used to be the IMF’s top man in the Troika:

IMF Economist: Greek Bailout Talks Need to Gain Momentum Now >>> get. on. with it.

— Katie Martin (@katie_martin_FX) April 17, 2015

At presser, #IMF European dept chief Poul Thomsen acknowledges #Greece programme should be "simplified" and "slimmed down".

— Peter Spiegel (@SpiegelPeter) April 17, 2015

The IMF is also worried about the consequences if Greece doesn’t have new financial support in place by the end of June (when its current bailout expires)

#IMF official: June-August period has significant rise in Greek payments; important to reach deal before payments rise. #Greece

— Yannis Koutsomitis (@YanniKouts) April 17, 2015

Shares are falling sharply on Wall Street in early trading, matching the selloff in Europe today.

ALERT: Dow slides 260+ points » http://t.co/f2CBNqo0Jy pic.twitter.com/ry3tflenwd

— CNBC Now (@CNBCnow) April 17, 2015

Moscovici: We need a Greek deal by May 11

European Commissioner Pierre Moscovici has thrown down a challenge to Greece; you must produce a concrete set of reforms by May 11.

Moscovici told the Financial Times that Athens must speed up its work, and deliver acceptable plans by the time finance ministers gather next month. There’s not chance of a deal next week, he confirmed.

In intw w/@FT econ editor @ChrisGiles_, @PierreMoscovici sez May 11 #eurogroup will be the "decisive" one for #Greece http://t.co/9gVWSWY7ol

— Peter Spiegel (@SpiegelPeter) April 17, 2015

Moscovici, the European commissioner for economic and financial affairs said:

We’ve got two meetings which are important. The April 24 meeting in Riga must not be a wasted moment; it must be a useful moment in which we see concrete progress in catching up with those reforms, and then the next meeting on May 11, which certainly must be decisive”.

The former French finance minister has been relatively optimistic about the Greek crisis in recent months. But he makes it clear that Athens has still not been “precise enough” in its reform plans.

“We are not talking about nothing. We are talking about things, but now we need to make progress”.

Moscovici warns Greece to agree to reforms or face default

Over in Athens, meanwhile, the Greek media is full of accounts of Yanis Varoufakis’s meeting with US president Barack Obama at the White House last night.

Our correspondent Helena Smith reports:

Though stand up and barely 12 minutes long, Yanis Varoufakis’ meeting with the US president at a reception to mark Greek Independence Day, is being heartily played up by the media in Athens this morning. The two men exchanged views “in a good climate” with Barack Obama reportedly conveying his concerns of “an accident” occurring if flexibility wasn’t shown by all sides – and Athens in particular.

Varoufakis – giving credence to statements made by his German counterpart Wolfgang Schauble earlier this week - announced that it was highly unlikely that any deal would be sealed at next week’s euro group meeting of finance ministers in Riga. Developments had to be seen cumulatively, he insisted.

The Greek finance minister was quoted as saying:

“There has never been a key date. We have to see everything in combination and cumulatively. On the 24th there will not be a solution, there will be progress,”

That also squares with Wolfgang’s Schäuble’s comments this morning....

Highlighting the role played by the debt-stricken country’s creditors, Varoufakis added:

“We have to be absolutely committed to our goal and absolutely integrated in the process in which we are participating with the IMF, ECB and EU.”

Varoufakis also highlighted the importance Athens’ Syriza-led government was giving to the “post-June” period when Greece’s current bailout program (extended by four months in February) finally expires. “The issue is what we do in the post- June period. Our goal is a good agreement [after that date], an agreement with a different take on the situation from previous agreements which only prolonged the problem.”

Athens would not “leave any stone unturned” to get to it, he said.

Updated

Wolfgang Schäuble also argued that the Greece’s problem is the weak state of its economy, not its huge debt pile.

He also downplayed the dangers posed by a potential Grexit:

- GERMANY’S SCHAUBLE SAYS CANNOT SEE ANY CONTAGION IN THE MARKET FROM GREECE TROUBLES, MARKETS HAVE PRICED IN ALL POSSIBILITIES

- 15-Apr-2015 13:58 - GERMANY’S SCHAUBLE SAYS PROBLEM WITH GREECE IS NOT ITS LOANS BUT LACK OF COMPETITIVENESS

Schäuble: Nobody has any idea how to solve Greek deadlock

More gloom on Greece. Germany’s finance minister, Wolfgang Schäuble, has just warned that there is “no expectation” of a solution to the Greek situation soon.

Speaking in Washington, Schäuble said Greece was in a “very difficult situation”, and criticised the new government for hurting its economy (by demanding a new deal with its creditors)

That suggests we should give up on hoping for a breakthrough at the next meeting of eurozone finance ministers in Riga, a week today. It also backs up George Osborne’s gloomy tone.

Schaeuble says all quiet on the Greek front

— Todd Buell (@ToddBuell) April 17, 2015

Reuters has snapped the key points:

- GERMANY’S SCHAUBLE SAYS GREECE IS IN A VERY DIFFICULT SITUATION

- GERMANY’S SCHAUBLE SAYS NOBODY HAS AN IDEA HOW TO GET TO AN AGREEMENT ON AN AMBITIOUS PROGRAM FOR GREECE

- GERMANY’S SCHAUBLE SAYS THERE IS NO EXPECTATION FOR A SOLUTION TO GREEK FINANCIAL ISSUES IN THE NEXT WEEKS

- GERMANY’S SCHAUBLE SAYS NEW GREEK GOVERNMENT HAS DAMAGED IMPROVING ECONOMIC TREND IN COUNTRY

Nice to see Schaeuble being conciliatory and uncontroversial

— Michael Hewson (@mhewson_CMC) April 17, 2015

Another line from Osborne:

- OSBORNE SAYS NOW IS NOT THE TIME FOR ANY CONFUSION ABOUT BRITISH ECONOMIC POLICIES OR POSSIBLE CHANGE IN DIRECTION

A cynic might quietly suspect the chancellor was using the Greek crisis as a reason to vote Conservative next month

George Osborne also told reporters in Washington that the UK would not be immune from the problems caused by a worsening in the Greek crisis.

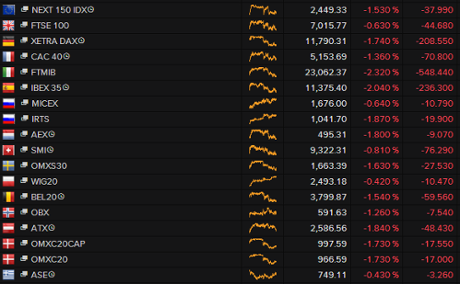

European stock markets remains deep in the red this afternoon, with Germany’s DAX down 2% and the FTSE 100 off 0.9%, or 60 points.

Arnaud Masset, market analyst at Swissquote, says Greece is to blame:

Investors are worried that Greece may default after rumors spread that Greece asked to delay its next debt payment to the IMF.

If you’re just tuning in, our opening post explains the state of play with Greece (no deal, not much optimism)

George Osborne: Greek misstep could reignite eurozone crisis

Breaking: George Osborne has warned that the deadlock over Greece’s bailout programme could trigger a repeat of the crisis which gripped the eurozone in 2011 and 2012.

Speaking in Washington, at the IMF/G20 Spring Meeting, the UK chancellor declared that the mood is much more gloomy than last year, adding that one “misstep” by either side could cause calamity.

Greece’s problems are pervading every discussion at this year’s meeting, he claims.

George Osborne: “Situation in Greece is most worrying for global economy. Discussions have pervaded every meeting. Mood notably more gloomy”

— Ed Conway (@EdConwaySky) April 17, 2015

Here are the snaps off Reuters:

- UK FINANCE MINISTER OSBORNE SAYS MOOD AT IMF MEETINGS IS “NOTABLY MORE GLOOMY” THAN AT THE LAST INTERNATIONAL GATHERING

- OSBORNE SAYS GREECE IS MOST WORRYING ASPECT FOR GLOBAL ECONOMY

- OSBORNE: MISSTEP ON EITHER SIDE ON GREEK ISSUE COULD RETURN EUROPEAN ECONOMIES TO PERILOUS STATE OF 3-4 YEARS AGO

- OSBORNE: WOULD BE MISTAKE TO THINK UK WOULD BE IMMUNE FROM EUROPEAN PROBLEMS FROM ANY GREEK FALLOUT

Osborne also touched on Greece’s repayments to the IMF -- yesterday, Christine Lagarde was adamant that Athens should not be granted a delay.

- OSBORNE SAYS HE IS CONFIDENT THAT THE IMF, AS HIGHEST-TIER LENDER TO GREECE, CAN BE BETTER PROTECTED THAN OTHER POTENTIAL CREDITORS TO GREECE

- OSBORNE - IMF EXISTS TO HELP COUNTRIES IN TROUBLE, BUT GREECE’S BIGGEST TROUBLE IS NOT ITS RELATIONSHIP WITH IMF BUT RELATIONSHIP WITH EURO ZONE

Updated

The Financial Conduct Authority, which regulates the City, says it is monitoring the effect of the Bloomberg crash.

A spokesman says:

“We are aware of the issue and are monitoring the impact on our firms.”

Bloomberg outage was 'worst in a decade'

I just chatted with Steve Collins, global head of dealing at asset management firm London & Capital, about the Bloomberg crash.

He says the outage was the worst he’s seen in the City in over a decade.

“I haven’t seen it go down like this for ten or fifteen years. Bloomberg is usually the one stable thing; it’s the thing that everyone can’t live without.”

Traders on Steve’s desk were left “twiddling their thumbs” after their Bloomberg terminals went down. Calls to the Bloomberg helpline (apparently not terribly helpful on a good day) went unanswered, he said.

“Big banks will pump thousands of orders across Bloomberg, so the outage had quite an effect on the market.”

Stop trading! pic.twitter.com/LSsc305Uo4

— *Russian Market (@russian_market) April 17, 2015

It was still possible to place orders by telephone, as in the days before computerisation reshaped the City, but is a more cumbersome, time-consuming process. As Steve explains.

“It was annoying that we lost the facility to trade bonds across the Bloomberg platform. Price discovery took longer, as we had to phone Deutsche Bank and Bank of America and say “make me an offer”.”

Bloomberg appears to be back now <crosses fingers>, but the cause of the outage isn’t known. A rumour is sweeping the City that it was caused by a carelessly spilled can of fizzy pop:

A SPILLED CAN of coke is apparently to blame for Bloomberg outage http://t.co/K62xaUcnfJ

— Lianna Brinded (@LiannaBrinded) April 17, 2015

Here’s my colleague Julia Kollewe’s story on the crash:

Updated

It’s business as usual at the Bank of England despite the Bloomberg outage:

- 17-Apr-2015 12:28 - BANK OF ENGLAND SAYS CORE OPERATIONS HAVE BEEN UNAFFECTED BY BLOOMBERG OUTAGE

- 17-Apr-2015 12:28 - BANK OF ENGLAND SAYS RETAINS ALL TOOLS NEEDED TO CARRY OUT RESPONSIBILITIES FOR FINANCIAL STABILITY, AND TO PROVIDE MARKET LIQUIDITY IF NEEDED

And the bond sale that was halted this morning will take place this afternoon, according to the Debt Management Office; a sign that the City is getting back to normal.

European stock markets fall

Back in the financial markets, a chunky selloff is breaking out across the main European bourses.

Germany’s DAX has slipped by over 1.7%, while Spain’s IBEX shed 2%. The FTSE 100 of leading blue-chip shares has also been hit, down 0.6%.

Not immediately clear what’s caused the selloff.

Some traders are blaming rumours that Chinese stock market regulators are planning to clamp down on speculative trading. It could also be due to a rise in the euro against the US dollar, which is bad news for European exporters.

And the crash at Bloomberg may be contributing, meaning there is less liquidity in the market today.

There is action in the bond markets too. Spanish and Italian government debt is weakening, pushing up bond yields.

* Spain, Italy 10-year bond yields rise 13 bps to 1.48 and 1.50 percent, respectively - Tradeweb

— Fabrizio Goria (@FGoria) April 17, 2015

Traders are scrambling to get hold of German debt, though, driving the yield on 10-year bonds closer to zero [at which point investors would be accepting NO interest at all]

Don’t miss economic editor Larry Elliott’s analysis on the jobs data:

Why the British jobs recovery has not brought bulging pay packets

The Bloomberg system crash I mentioned earlier has forced the UK’s debt management agency to suspend a £3bn debt sale. Here’s the full story.

UK halts £3bn debt sale after Bloomberg terminals crash worldwide http://t.co/XLwAATT7Gv

— Julia Kollewe (@JuliaKollewe) April 17, 2015

Updated

UK unemployment falls: read the full story here

My colleague Katie Allen writes:

Britain’s unemployment rate has dropped to its lowest level since 2008 but earnings growth has slowed, according to the final official labour market figures to be published before the election.

The Office for National Statistics said the jobless rate dropped to 5.6% in the three months to February, down from 5.8% in the previous three months. That was the lowest rate since the onset of the financial crisis in July 2008....

And here’s her full story, complete with charts and expert reaction:

UK jobless rate falls to 5.6%, lowest since 2008, but pay still sluggish

PS: apologies that the charts in today’s blog are quite blurry. I must have done something wrong

Updated

The CBI, which represents British firms, is also notably cool about raising wages faster.

Neil Carberry, CBI Director for Employment and Skills argues that firms need to become more productive first:

“It’s great to see 248,000 more people in work, the fastest rise in employment in just under a year – thanks to our flexible jobs market.

“With real wage growth rising people have a little more money in their pockets. But we need to see a recovery in productivity before wages can rise faster.”

Britain’s bosses aren’t keen to open up their wallets, it appears.

James Sproule, chief economist at the Institute of Directors, argues that:

“While many people would like to see greater pay increases, wages are now rising in line with historic productivity growth, making them sustainable in the long term and allowing UK companies to remain competitive.”

Curiously, the remuneration packages of FTSE 100 executives doesn’t seem to be rigidly tied to productivity growth. Their total pay jumped 50% last year, the Financial Times reports.

Ian Stewart, chief economist at Deloitte, predicts that workers may finally see larger pay rises soon:

“Despite these buoyant job numbers earnings growth has drifted up only slowly from last year’s lows. But with skills shortages emerging, and the jobless rate set to fall further, we see earnings growth accelerating through this year and next.”

John Hawksworth, PwC’s chief economist, points out that while employment has grown rapidly since 2010, wage growth has not. That’s not a coincidence either:

“Looking back over the past five years, average real earnings are around 4.4% lower, but employment has risen by around 6.5% over the same period. In this way, the pain of recession has been spread more widely than in past downturns in the early 1980s and early 1990s, with more jobs being created but at lower average rates of pay.”

The pound has jumped almost a cent against the US dollar to a four week high of $1.5028 on the back of the jobs data.

Here’s Rachel Reeves, Labour’s Shadow Work and Pensions Secretary, responding to today’s Labour Market Statistics:

“Today’s fall in overall unemployment is welcome, but with working people earning on average £1,600 less a year since 2010 and the biggest fall in wages over a parliament since 1874, it’s clear the Tory plan is failing.

“Labour has a better plan to reward hard work, share prosperity and build a better Britain. A Labour government will raise the minimum wage to more than £8 an hour by October 2019 and give tax rebates to firms who pay a Living Wage. We will protect the tax credits that millions of families rely on, get at least 200,000 homes a year built by 2020, extend free childcare from 15 to 25 hours for working parents of three and four-year-olds and guarantee apprenticeships for everyone who gets the grades.”

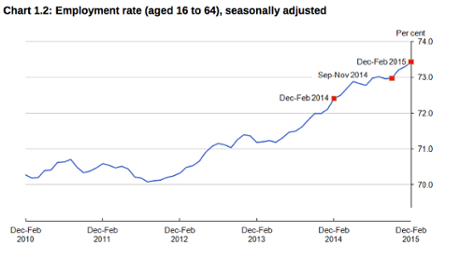

UK unemployment: the key charts

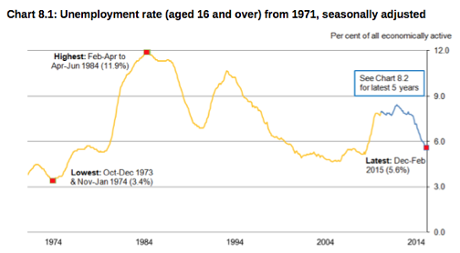

This chart confirms that the unemployment rate is now at its lowest since July 2008, the quarter before the financial crisis erupted.

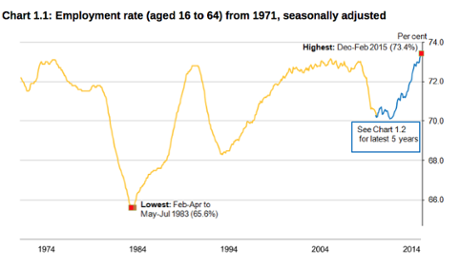

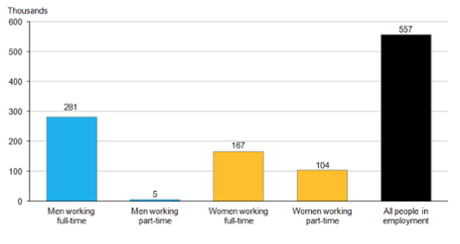

These two show that Britain’s employment rate, at 73.4%, is the highest since records began in 1971:

The number of people in work rose by 557,000 over the last year; more than half were men taking full-time jobs.

At 5.6%, Britain’s unemployment rate is almost as low as America’s (which hit 5.5% in February).

And it’s half the rate in the eurozone, where 11.3% of adults are out of work. Across the whole EU, the rate is 9.8%.

Probably one of the best charts for Coalition: jobless record detached from Europe now as good as US pic.twitter.com/ineFmmvgf0

— Faisal Islam (@faisalislam) April 17, 2015

Paul Kenny, general secretary of the GMB union, questions the quality of the jobs being created in the UK today:

“Most of these new jobs are mainly low-skilled, low-paid and zero hours.....

“Most workers have seen little or no evidence of any recovery in living standards due to the Tories not promoting real economic growth based on investment and productivity gains.”

The prime minister tweets that today’s employment report shows his economic plan is delivering:

More strong jobs figures show our plan is working - helping put Britain back to work: http://t.co/j7y4s67KxU pic.twitter.com/V5m2yfYjIY

— David Cameron (@David_Cameron) April 17, 2015

You can see the jobs report yourself, here on the ONS website:

PA: Record numbers of people in work

Here’s the Press Association’s first take on the jobs data:

Unemployment has continued to fall and a record 31 million people are in work, the last jobless figures before the general election have shown.

The jobless total fell by 76,000 to 1.84 million in the quarter to February, the lowest for almost seven years.

The number of people claiming jobseeker’s allowance fell by 20,700 in March to 772,400, the 29th consecutive monthly cut.

Other data from the Office for National Statistics (ONS) showed that more than 31 million people were in work after an increase of more than half a million in the past year, the biggest total since records began in 1971.

The UK’s unemployment rate is now 5.6%, a fall of 1.3% since a year ago. The rate was 7.9% in May 2010, when the last general election was held.

Around 1.3 million people were in part-time jobs when they wanted full-time work, up by 29,000 in the latest quarter, while self-employment was little changed at 4.5 million.

The number of people classed as economically inactive, including those looking after a relative, on long-term sick leave or who have given up looking for work, fell by 104,000 to just under nine million.

Average earnings increased by 1.7% in the year to February, 0.2% down on the previous month.

Long-term unemployment has also fallen, down by 188,000 to 623,000 for those out of work for at least a year. Youth unemployment - 16 to 24-year-olds - fell by 22,000 in the three months to February to 742,000.

The ONS also reported that 107,000 people were made redundant over the latest three months, little changed on the end of last year, but more than 200,000 fewer than the record peak of 311,000 in early 2009.

There were 743,000 job vacancies across the country in January to March, 124,000 more than a year ago and the highest since records began in 2001.

Economists are welcoming the news that Britain’s jobless rate has fallen to 5.6%, the lowest since the run-up to the financial crisis.

But there is some concern that wage growth isn’t accelerating.

Some instant reaction:

More good jobs figures - employment up nearly 250k in three months to record 73.4% of workforce; unemployment rate down to 5.6%.

— David Smith (@dsmitheconomics) April 17, 2015

Pay still relatively subdued - 1.7% including bonuses, 1.8% ex bonuses, though well ahead of inflation.

— David Smith (@dsmitheconomics) April 17, 2015

Regular pay growth at 1.8%, unemployment down, employment rate at record high - strong set of labour market stats.

— Duncan Weldon (@DuncanWeldon) April 17, 2015

Employment growth driven by full time employee positions. Labour market composition shifting towards that over last year.

— Duncan Weldon (@DuncanWeldon) April 17, 2015

UK wages growth in February alone fell to 1.3% so after 1.4% (Jan) and 2.4% (Dec) there is sadly a clear slowing evident #GBP

— Shaun Richards (@notayesmansecon) April 17, 2015

With inflation at zero, today’s data also shows that real wages continued to rise in the three months to February, after years of falling real pay.

For Dec-Feb 2015 wages including bonuses up 1.7% on a yr earlier. Wages excl bonuses up 1.8% http://t.co/XEpzd276SE pic.twitter.com/uTMW1mosfZ

— ONS (@ONS) April 17, 2015

UK unemployment rate falls again

The UK unemployment rate has fallen to 5.6%, its lowest level since July 2008.

And the number of people in employment has risen by almost a quarter of a million in the December-February quarter, to the highest rate on record. A pre-election boost to the Conservatives?

#Employment rate 73.4% for Dec-Feb 2015, highest figure on record http://t.co/zNLTsoLpHm pic.twitter.com/BHQj9x00ZD

— ONS (@ONS) April 17, 2015

But wage growth during the quarter slowed; average pay including bonuses rose by +1.7%, down from +1.8% last month.

Here’s the snaps from Reuters:

- UK MARCH JOBLESS CLAIMANT COUNT -20.7K (REUTERS POLL -29.5K) TO 0.722 MLN

- UK ILO JOBLESS -76,000 TO 1.838 MLN IN 3 MTHS THROUGH FEB, RATE 5.6 PCT (REUTERS POLL 5.6 PCT), LOWEST RATE SINCE JULY 2008

- UK LFS EMPLOYMENT +248,000 TO 31.049 MLN IN 3 MTHS THROUGH FEB, BIGGEST 3-MONTH INCREASE SINCE APRIL LAST YEAR

- UK AVG WEEKLY EARNINGS +1.7 PCT YY IN 3 MTHS THROUGH FEB (REUTERS POLL +1.8 PCT); FEB ALONE +1.3 PCT YY

- UK EARNINGS EX-BONUSES +1.8 PCT YY IN 3 MTHS THROUGH FEB (POLL +1.7 PCT), FEB ALONE +2.2 PCT YY, BIGGEST SINGLE MONTH RISE SINCE MAY 2011

- ONS LINKS RISE IN SINGLE-MONTH REGULAR PAY TO EU RULES RESTRICTING BANKER BONUSES

Updated

Heads-up: it’s nearly time for the latest UK unemployment data to be released.

Grexit talk in the analyst notes rising. Worth remembering though that faced with reality of a bank run, Greek govt compromised last time.

— Duncan Weldon (@DuncanWeldon) April 17, 2015

The Greek stock market is also calm, up 0.7% in early trading.

Fortunately my Reuters terminal is working perfectly this morning (thanks guys), so we can see that Greek bonds are trading at worryingly high levels.

The two-year Greek bond is yielding 27.2%, broadly unchanged today, suggesting a high risk of default.

And 10-year Greek debt is trading at a yield of 12.7%, down slightly from 12.8% yesterday.

Yields soared yesterday as traders reacted to the news that the IMF would not allow Athens to delay a debt repayment, making this the worst week for Greek debt since January.

CONNECTION LOST #bloomberg pic.twitter.com/RGJGMDY0No

— James Titcomb (@jamestitcomb) April 17, 2015

The technical problems at Bloomberg are a major problem for City types. There are more than 300,000 terminals around the globe, used for both news and trading.

CNBC has a good early take:

Bloomberg’s trading terminal experienced an outage on Friday morning, with some users saying they were unable to perform their usual trading activity.

The company confirmed to CNBC that its terminal was currently unavailable worldwide, with traders from the U.K. and Singapore complaining on Twitter that they had been affected by the issue.

Bloomberg is looking into the causes of the outage, the company’s spokesperson said.

Bloomberg terminals hit by global outage; "could well" affect trading volumes: http://t.co/C3gZ5a3Jx4 pic.twitter.com/wV5RbSGF5A

— CNBCWorld (@CNBCWorld) April 17, 2015

Updated

Bloomberg outage hits the City

Alarm is sweeping the City this morning as traders and analysts realise that their Bloomberg terminals have crashed.

It looks like a serious outage:

Bloomberg helpdesk not answering phones

— Steve Collins (@TradeDesk_Steve) April 17, 2015

Bloomberg problems argggghhh

— Michael Hewson (@mhewson_CMC) April 17, 2015

Come on @yanisvaroufakis and @tsipras_eu ! With Bloomberg down, this is your chance to default and exit the EMU without any repercussions.

— barnejek (@barnejek) April 17, 2015

Updated

German 10-year bund yields fall closer to zero

The Greek crisis is also helping to drive money into German government debt.

The yield (or interest rate) on 10-year bonds has fallen even closer to 0.0%. That means Berlin could effectively borrow for almost nothing and repay the money in 2025.

German 10Y yields drop to 0.076%, record low - growing concerns over Greek debt crisis pic.twitter.com/yhjnOgKjnq

— Francine Lacqua (@flacqua) April 17, 2015

Shorter-term bunds are already trading at negative yields, meaning investors are paying more than the face value of the debt. They could still make a profit, though, by selling them onto the European Central Bank’s QE scheme.

Greece’s Kathimerini newspaper is also gloomy, suggesting that a deal might not come before mid-May.

If so, we can scrap hopes of a breakthrough at the April 24th eurogroup meeting

With negotiations between Greece and its creditors effectively deadlocked, a potential deal that could unlock crucially needed funding appeared more distant than ever on Thursday with doubts appearing about whether an agreement can be reached in time for a Eurogroup planned for May 11, well after the next scheduled eurozone finance ministers’ summit in Riga next Friday, which had been the original deadline.

Darren Courtney-Cook, head of trading at Central Markets Investment Management, confirms that the Greek crisis is lingering over the City:

“I think the Greece situation will be resolved but we’ve had a massive up-turn on the stock markets so far this year, and the underlying concerns are causing some people to take a bit of money off the table.”

(quote via Reuters)

European markets have opened mixed, with Germany’s DAX extending yesterday’s falls but the FTSE 100 rising a little:

Are markets too complacent?

Investors are underplaying the risk posed by Greece, according to Chris Weston of financial spread betting firm IG this morning:

The Greek government have a mandate to stay in the European Monetary Union and they simply can’t leave. However a view from certain parts of the market is [Greece’s plans] to distance themselves from the rest of Europe and to actually be forced out.

Markets still believe Greece will stay within the union in some form, but the risks are growing and a full ‘Grexit’ won’t be pleasant. The market is not prepared at all for this.

Analysts at Citigroup also suspect markets are too relaxed:

Citi: "investors continue to bank on last minute Greek solution. This complacency likely understates tail risk for EUR"

— Katie Martin (@katie_martin_FX) April 17, 2015

Updated

The Agenda: Greek crisis rumbles on

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

It looks like another day dominated by the Greek debt crisis, which ratcheted up another notch yesterday when the IMF effectively sunk the idea that Athens could be granted a payment delay.

Both sides appear far from a deal, still. As we covered in last night’s blog, Greek finance minister Yanis Varoufakis insists that Greece won’t roll over and accept measures that would perpetuate the crisis.

He told an audience in Washington that:

“We will compromise, we will compromise and we will compromise in order to come to a speedy agreement, but we are not going to be compromised.”

Varoufakis also warned that Greece was suffering “liquidity asphyxiation”, but insisted that he wouldn’t even consider the idea that the country leaves the euro:

Toying with Grexit, or amputating Greece, is profoundly anti-European. Anybody who says they know what will happen if Greece is pushed out of the euro is deluded.....

Our only rational pro-European response is to spend every waking hour... trying to reach an honourable agreement.”

But Greece’s creditors continue to take a hard line, with German finance minister Wolfgang Schäuble warning that Athens must deliver on its pledges to receive bailout funds.

With Greece due to pay almost €1bn to the IMF next month, investors fear that the country could hit a cash crunch soon.

There’ll be more action in Washington today, where finance ministers and central bank chiefs are attending the IMF/G20 Spring Meeting.

Varoufakis is due to meet with ECB chief Mario Draghi at some point.

There’s also some data to look forward to, including the latest UK unemployment report at 9.30am BST, and the final eurozone inflation data at 10am BST.

#UK daybook: Euro Area Inflation, U.K. Unemployment

— Francine Lacqua (@flacqua) April 17, 2015

I’ll be tracking all the main events through the day.....