PS: Greek MPs will get their say when the deal is reached:

Varoufakis "If we reach an agreement it will be approved by parliament"

— Lorcan Roche Kelly (@LorcanRK) April 16, 2015

And finally, asked exactly what he’ll do to reach a deal, Varoufakis repeats that Greece will “compromise, compromise, compromise without being compromised”.

Asked for more details of Greece’s plans, Varoufakis criticises the way in which Greece was forced to cut down its plans into increasingly narrow, granular ways by its creditors, only to them be accused by the international media for not having any proposals.

Sorry about that, Yanis. But I can’t help noticing that you didn’t actually outline those policies.....

Clear from questions that even "sympathetic" DC audience frustrated by varoufakis lack of specificity. Think he's lost this crowd.

— Simon Nixon (@Simon_Nixon) April 16, 2015

Varoufakis: "you asked about policies but I didn't have time to go into them" - after an hour of windy waffle!

— Simon Nixon (@Simon_Nixon) April 16, 2015

There could be a huge burst of optimism if Greece and its creditors can agree a new programme of reforms, says Varoufakis.

He paints a picture of a new export-driven model, with canny investors rushing in to take advantage.

Varoufakis has said it finally: "We wish to merge the current review with the June agreement." #Greece #GreekEconomy

— Yannis Koutsomitis (@YanniKouts) April 16, 2015

Varoufakis "Greece will be such a field for bargain-hunting [in the event of a deal]"

— Lorcan Roche Kelly (@LorcanRK) April 16, 2015

Varoufakis adds that he is greatly encouraged by Wolfgang Schauble’s comments earlier (I missed this, but apparently he predicted that Greece will not quit the eurozone)

Varoufakis: "We will never slip back to a primary deficit" #Greece #GreekEconomy HT @BrookingsEcon pic.twitter.com/54RinmuptL

— Derek Gatopoulos (@dgatopoulos) April 16, 2015

What about the immediate issue facing Greece, its bailout extension which expires in June?

Another lengthy answer, in which Varoufakis accuses the New Democracy government of sparking Greece’s liquidity squeeze by predicting a bank run if Syriza won power.

Varoufakis "The previous government tried to start a bank run in order to stay in power"

— Lorcan Roche Kelly (@LorcanRK) April 16, 2015

And he then cites the ECB’s decision to stop accepting Greek debt as collateral, in February:

Varoufakis complains abt ECB removing waiver on Grk debt in Feb. Doesn’t mention it was prompted by him publicly saying Greece was insolvent

— Ed Conway (@EdConwaySky) April 16, 2015

Varoufakis repeats that he is prepared to give ground, but not be crushed:

We will compromise, and compromise, and compromise to reach a speedy agreement, but we will not be compromised.

And he refuses to even consider a Grexit, saying no-one knows the impact of such a move.

Varoufakis is now arguing that the European Investment Bank should fund a massive new investment plan, to stimulate the European economy, funded by new bonds issued by the EIB -- with the ECB ready to buy them if yields rose too high.

Varoufakis "Why can't the @EIBtheEUbank fund a 'New Deal' for Europe, with the @ecb backing bond issuance in secondary market?"

— Lorcan Roche Kelly (@LorcanRK) April 16, 2015

Do you accept that as a member of a single currency union, you don’t have a mandate to do whatever you want?

Absolutely, Varoufakis replies. But we do have a right to be heard, and a right to challenge.

Varoufakis isn’t rolling over to creditors’ demands, though:

We'll compromise on few important structural reforms, says Greek FinMin, defending stance on labor law/privitizations pic.twitter.com/F9sllWa53d

— Katerina Sokou (@KaterinaSokou) April 16, 2015

OK, here’s the key line from Varoufakis. Greece is determined to reach a deal by the end of June, and quite prepared to compromise to get there (while not accepting measures that will further damage the economy and extend those mistakes of the past).

Varoufakis: "We are perfectly prepared to compromise" #Greece #EuroFuture HT @BrookingsEcon

— Derek Gatopoulos (@dgatopoulos) April 16, 2015

Onto questions, although as usual with this particular finance minister the answers are rather lengthy....

He points to mistakes of the past with Greece’s bailouts, and also sounds rather alarmed about the state of the country’s pension system:

More Varoufakis: Greek privatizations were "disasters" #Greece #EuroFuture HT @BrookingsEcon pic.twitter.com/i1sffkmYvR

— Derek Gatopoulos (@dgatopoulos) April 16, 2015

Varoufakis says there is no doubt that Greek pension system is in deep trouble. #Greece #GreekEconomy #understatement

— Yannis Koutsomitis (@YanniKouts) April 16, 2015

Varoufakis can still draw the crowds:

Here's the pictures that prove it... pic.twitter.com/UsDXfaXHSH

— Katerina Sokou (@KaterinaSokou) April 16, 2015

This negotiation must succeed, Varoufakis concludes. And we this quirky left-wing government is determined that it will.

Varoufakis talked for 25 minutes, not a single sentence on how he thinks Greece should address "malignancies".

— Simon Nixon (@Simon_Nixon) April 16, 2015

Varoufakis: We want time for reach new agreement with our partners

Varoufakis is now turning to the immediate challenge, of Greece’s debt talks.

He says that Greece want time... to persuade our partners, especially in Northern europe, that this government does not want to go back to the profligacy of recent years. And they need to persuade us that they do not want to impose a programme.... that has failed.

He then quotes Mario Draghi, who said that the eurozone can only succeed anywhere if it succeeds everywhere. We want to part of everywhere, Varoufakis smiles.

Varoufakis: We are asking for 2 things: 1) to be heard 2) an investment program. #GreekEconomy #Greece

— Yannis Koutsomitis (@YanniKouts) April 16, 2015

Followed by a curious line from the finance minister, that many ordinary Greeks “may have been micro-parasitic…” but not as bad as the big players.

Varoufakis delivers a good line: #Greece took a hit for Europe. #GreekEurope

— Yannis Koutsomitis (@YanniKouts) April 16, 2015

Good line from Varoufakis: Greece went from a Ponzi scheme of unsustainable borrowing before the crisis to a scheme of Ponzi austerity after it.

And our failings meant we “took one for the team” by swallowing more fiscal consolidation than anyone else.

Updated

Varoufakis: Keener than anyone to get a deal

We are extremely keen to reach a deal, Varoufakis insists, but it must be the right one.

Nothing would be easier than to simply sign on the dotted line to get seven billion euros, but it would be wrong.

Varoufakis: Our gov't is keener than anyone to bring negotiations to a conclusion. #GreekEconomy #Greece

— Yannis Koutsomitis (@YanniKouts) April 16, 2015

Varoufakis says that if Greek gov't accepts creditors demands it would be wrong. #GreekEconomy #Greece

— Yannis Koutsomitis (@YanniKouts) April 16, 2015

Varoufakis maybe over-playing the global significance of the Greek negotiations a little here.

— Lorcan Roche Kelly (@LorcanRK) April 16, 2015

The outcome of Greece’s negotiations with its creditors will play a major role in deciding if Europe aids or impedes the rest of the world in putting 2008 crash behind it, Varoufakis continues.

Varoufakis is arguing that Greece’s seven year depression cannot simply be blamed on the country’s “unique chronic malignancies”.

Instead, fundamental problems within the eurozone’s structure are to blame.

He’s accusing Europe of embarking on a Beggar Your Neighbour policy last seen in the 1930s, before Bretton Woods.

The current policy mix is increasingly turning Europe into a mercantilist force that is an exporter of idle savings, and deflation.

There is a good cause to think that Europe is bigger threat to the global economy than China was perceived to be a few years ago, he adds.

Varoufakis: Greek debt negotiations will determine Europe's future

Varoufakis says he’s delighted to be at the Brookings Institute at such an important time, as the Greek government shoulders the task of reaching a deal with its creditors.

He quickly turns to the big issue of the day, the Greek debt talks.

The Greek 2010 debt crisis was a harbinger of much of what happened afterwards, he says.The same is true this time. The outcome of our negotiations will influence how Europe handles vital issues in the years ahead.

Updated

Back in Washington, Yanis Varoufakis is taking the stage at the Brookings Institution.

#Varoufakis is up, Live here http://t.co/3GnTIl7n1e

— Lorcan Roche Kelly (@LorcanRK) April 16, 2015

Today’s surge in Greek bond yields takes us closer to the levels seen in 2011 and early 2012, before Greece’s creditors agreed to take a haircut on their loans:

Greek government bond prices plunged today. Default fears are back: http://t.co/kJTx7KsOjC pic.twitter.com/dx6A8UvgHA

— Bradley Davis (@bradleydaviswsj) April 16, 2015

Hello again. A couple more points from Wolfgang Schäuble’s session in Washington via our old ally Yannis Koutsomis:

Schäuble about #Greece: If you find someone else in Beijing, Moscow etc who is willing to lend you money, we are OK, take it. #eurofuture

— Yannis Koutsomitis (@YanniKouts) April 16, 2015

Schäuble: Greek debt not a problem in the next 6 yrs. Now challenge is growth. Minimum wage is highr than in other countries ~@GuntramWolff

— Yannis Koutsomitis (@YanniKouts) April 16, 2015

Schäuble: If #Greece wants 7.2bn tranche than it has to delivr. Otherwise they don't hv to take the money. They'll hv to find othr solutions

— Yannis Koutsomitis (@YanniKouts) April 16, 2015

So no obvious change in Germany’s position on Greece.

Onto Greece, and Schauble’s message is that Athens can’t expect any bailout funds until its lenders are broadly satisfied:

#Schauble repeats: the 3 institutions have to say "Greece has [done] BROADLY - NOT 100%, we never ask for 100%"- what is asked. #eurofuture

— The Greek Analyst (@GreekAnalyst) April 16, 2015

Schauble is hammering home the importance of credible, accountable decision-making in the eurozone.

Schäuble's ideas on the economy & monetary policy may be controversial but his ideas on governance are paramount. #eurofuture

— Yannis Koutsomitis (@YanniKouts) April 16, 2015

Updated

Schauble says he doesn’t want borrowing costs to remain so low for an extended period:

German FinMin Schäuble, one of the biggest beneficiaries of low or negative rates says: Not in favor of long-term negative interest rates.

— Holger Zschaepitz (@Schuldensuehner) April 16, 2015

Ah, Wolfgang Schauble is making some familiar points, hailing the recovery in Europe’s periphery:

FinMin #Schäuble: European countries that have already implemented real reforms are starting to see their efforts bear fruit. #EuroFuture

— BMF (@BMF_Bund) April 16, 2015

Heads-up. Germany’s finance minister is speaking in Washington now. Here’s a link:

LIVE WEBCAST: Tune in now to our live discussion with #Germany's Finance Minister Wolfgang #Schäuble #EuroFuture → http://t.co/t7K0xYFSe6

— Brookings Global (@BrookingsGlobal) April 16, 2015

I’m not able to watch it, alas, but will try to post some quotes off the wires/Twitter.

Yanis Varoufakis is due up later as well, at 2.45pm EST / 7.45pm BST / 9.45pm Athens. Will try to be online for that....

Updated

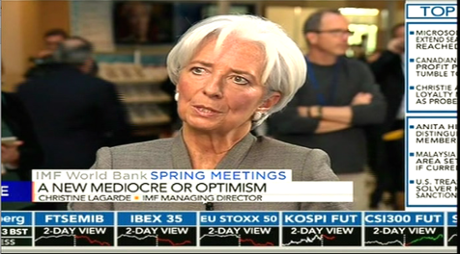

Afternoon summary: IMF chief won't support Greek repayment delay

Time for a brief recap.

Greece has been given a strong warning against asking to delay its repayments to the International Monetary Fund, as concern grows that it may fail to reach an agreement with its creditors.

IMF chief Christine Lagarde told a press conference in Washington that such a move would be unwelcome, and unprecedented.

“It’s clearly not a course of action that would actually fit....We have never had an advanced economy ask for payment delays.”

Lagarde also warned that such a policy would be unfair to poorer countries.

And in an interview with Bloomberg TV, Lagarde also said she hopes “very much” that Greece does not seek a delay.

@Lagarde answers #Greece #IMF2015 prayers: "NO," says Christine... pic.twitter.com/kiqgBIkF36

— MARK GILBERT (@ScouseView) April 16, 2015

She was speaking after the Financial Times reported that Greece has informally floated the idea; later denied by finance minister Yanis Varoufakis. Lagarde, though, said the FT’s Chris Giles was “very well informed”.....

Greece’s prime minister, Alexis Tsipras, says he’s still ‘firmly optimistic’ of a deal with month. He said:

“Despite the cacophony and erratic leaks and statements in recent days from the other side, I remain firmly optimistic that there will be an agreement by the end of the month.

“Because I know that Europe has learned to live through its disagreements, to combine its parts and move forward.”

Greek bonds have suffered a widespread selloff today, sending yields (interest rates) up to their highest levels since the current crisis began.

The yields on two-year Greek bonds spiked from 24% to over 27%, suggesting a very high risk of default.

And the 10-year bond yield is up almost 1% at over 12.7%

Greek 10-year yield at the highest levels since March 2013: 12.7% pic.twitter.com/7w4YYTJaaa

— Charlie Bilello, CMT (@MktOutperform) April 16, 2015

Data firm Markit says investors are pricing a 77% risk of Greece defaulting over the next five years.

And Capital Economics fears that the Greek crisis is finally heading to a climax.

Jennifer McKeown explains:

The upshot is that Greece desperately needs to receive bailout money very soon. If an agreement is not reached next week, the Government might resort to emergency measures to avoid an immediate default and euro-zone exit. But Greece will still need the remaining funds from its current bailout, a new third bailout and ultimately some kind of debt write-off if its future in the currency union is to be assured.

And note that any emergency measures put in place to keep the economy afloat in the meantime could conversely put the wheels in motion to facilitate a euro-zone exit.

And with bookmaker William Hill refusing to take any bets on Greece leaving the eurozone this year, it does feel as if we’re heading towards a crunch.....

There are reports of clashes involving Greek riot police at the Athens university tonight, where anarchists have been holding an occupation for several days.

Clashes outside Athens University, footage live on state TV #Greece HT @neritnetwork pic.twitter.com/xeIHs9pwOE

— Derek Gatopoulos (@dgatopoulos) April 16, 2015

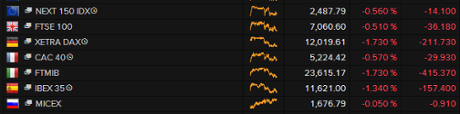

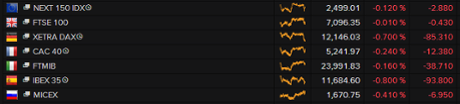

European stock markets are continuing to fall as trading grinds to a close, with Greece’s debt woes weighing on traders.

The German DAX is the biggest faller, down 1.5%. That reflects the fact the euro has rallied against the US dollar following underwhelming American housing and jobless data. A stronger euro is not great news for Germany’s export base.

Jasper Lawler of CMC Markets says the thorny issue of Greece’s IMF debts is worrying investors:

Sentiment in Europe dropped on Thursday amidst heightened concerns of a Grexit after Greece reportedly asked for extension from the IMF over its next debt payment, and got declined. Neither the desperation from Greece in asking for an extension, nor the hard-line approach from the IMF in denying it bode well for a resolution.

These latest concerns follow Greece’s debt downgrade and suggestions from German finance minister Schauble that no deal will be reached in next week’s Eurogroup meeting.

Adding to woes in European equities was a rebound in the euro, caused by nothing new from the ECB’s monetary policy meeting yesterday, and poor data from the United States sending the US dollar lower.

The IMF chief is taking her message to Twitter:

We need policy action to prevent the “new mediocre” from becoming the “new reality”. pic.twitter.com/J4HFNW25XT

— Christine Lagarde (@Lagarde) April 16, 2015

It’s worth noting that the question about potential Greek payment delays came from Chris Giles, who co-wrote the Financial Times’s story about Greece officials making informal inquiries, and being rebuffed.

Christine Lagarde could have taken the opportunity to dispute the FT’s line, but instead she described Giles as “very well informed”. An endorsement of the story?...

.@Lagarde calls @ChrisGiles_ "very well informed".

— Peter Spiegel (@SpiegelPeter) April 16, 2015

Lagarde: I couldn't support payment delay for Greece

Christine Lagarde is now being interviewed by Bloomberg.

Asked about the Greek payment delay issue, she reiterated that such a course of action couldn’t be recommended, adding that she would not be able to support it.

IMF's Lagarde to @tomkeene: "We've never had an advanced country [Greece] ask for a delayed payment. I myself would not support it."

— Vonnie Quinn (@VonnieQuinn) April 16, 2015

It’s a pretty clear message to Athens:

"Forget it Yanis".

— Yannis Koutsomitis (@YanniKouts) April 16, 2015

Updated

Lagarde concludes her press conference by, again, urging America to ratify reforms to the way the IMF runs.

These reforms would give the IMF more financial resources, and also give more power to other nations such as China -- something Congress has baulked at.

Asked about Russia, Christine Lagarde says she’d be very pleased if the IMF’s economic forecasts are too pessimistic. Russia is an important partner, she adds.

What is your advice for Greece?

Lagarde: Our advice is the same, to get on with the work of improving the short and medium-term economic prospects.

We want to restore the stability of the Greek economy...and I hope everyone involved can continue the work at a faster pace.

Actually, maybe Christine Lagarde wasn’t quite as emphatic as I initially thought about Greece.

Sky News’s Ed Conway tries to get a definitive answer - are you absolutely ruling out a payment delay, and are you worried that the IMF’s reputation for always getting its funding back is at risk?

Lagarde replies that the Fund’s management will do everything it can to ensure that lending to the Fund is the safest route that anyone can adopt.

I ask @lagarde (twice) if she will rule out agreeing to any kind of loan repayment delay for Greece. She refuses to answer.

— Ed Conway (@EdConwaySky) April 16, 2015

Updated

Lagarde says IMF payment delay by Greece tantamount to demand for more money from much poorer countries in worse state than Greece itself

— A Evans-Pritchard (@AmbroseEP) April 16, 2015

Lagarde says that the IMF has concerns over Greece’s liquidity situation:

#Lagarde says #IMF concerned about liquidity situation in #Greece- photo via @mignatiou pic.twitter.com/KxrgR9CnGs

— EfiKoutsokosta (@Efkouts) April 16, 2015

Updated

Greece’s government, incidentally, is adamant that it has not inquired about a delay -- despite the Financial Times’s report today.

"media reports are outright lies" I make that Varoufakis 2 - FT 0 pic.twitter.com/PUkX14g3kU

— Credit Macro PM (@lebullmarche) April 16, 2015

Lagarde: Greek payment delay can't be recommended

Christine Lagarde has just all-but ruled out giving Greece more time to repay its IMF loans .

She tells the press conference in Washington that:

Payment delays have not been granted by the board of the IMF in the last 30 years.

They have been granted to a couple of developing countries... and that was not followed by very productive results.

The IMF is a rules-based institution, Lagarde says. And while all options are available, “it’s clearly not a course of action that could be recommendable in the current situation”.

We have never had an advanced economy asking for repayment delay.

And one reason, she explains, is that such a delay would actually be classed as “additional financing” for the country in question.

And that financing would come from some countries who are in “an even worse situation” than the countries seeking the delays.

Punchy from @lagarde on Greece: “Payment delays have not been granted by IMF in last 30yrs. Never had advanced economy asking for delay.”

— Ed Conway (@EdConwaySky) April 16, 2015

Updated

Onto questions, and Lagarde denies that the world economy is in a bad way.

The US economy has shown decent growth. In Europe, the UK is holding up strongly and the eurozone is improving. Japan is also on the rise.

IMF's Lagarde: U.S. economy is bright spot in world; Euro area showing signs of recovery.

— DailyFXTeamMember (@DailyFXTeam) April 16, 2015

But it’s true that emerging markets are not performing as well as we hoped, or as well as last year. China is slowing.

And financial stability risks are on the rise. It’s not armageddeon, though, she insists.

Updated

Christine Lagarde says that the global economy’s growth potential won’t be realised unless policy makers take new steps to stimulate demand.

She outlines a familiar cocktail:

- Accommodative monetary policy where needed

- Tightened monetary policy where possible

- Smart fiscal policies, adjusted to each countries.

- Ways of dealing with the financial risks created by record low interest rates, volatile commodity prices and exchange rates, and the possibility that the US raises interest rates.

But we also need labour market reforms, and international collaboration “to raise today’s growth, and tomorrow’s growth” and to fight inequality, she adds.

To get good enough it needs to get better, and we can only do it together-Lagarde on global recovery #188Together http://t.co/Zq5rywkqHC

— IMF (@IMFNews) April 16, 2015

And we're off with @Lagarde pic.twitter.com/Sha3AJq9gz

— Peter Spiegel (@SpiegelPeter) April 16, 2015

Christine Lagarde press conference - watch here

IMF chief Christine Lagarde is about to speak to the press in Washington, at the start of the Spring Meeting.

It’s being streamed live here (right-click to open in a new tab)

Starts now: IMF Managing Director Christine Lagarde address the press during the 2015 Spring Meetings http://t.co/9Ew5AMtmp1

— IMF (@IMFNews) April 16, 2015

Moscovici also warned, though, that Europe doesn’t have the political will to agree another haircut on Greece’s debt pile.

EU Finance Commissioner @pierremoscovici: #Greece leaving € zone would not be an accident, would be catastrophic. #SpringMeetings @euronews

— Stefan Grobe (@StefanGrobe1) April 16, 2015

Pierre Moscovici added that it would be a “catastrophe” if Greece were to leave the euro.

Updated

European Commissioner Pierre Moscovici has weighed in, telling an audience in Washington that it’s time for Greece “to deliver” on the reforms its creditors are seeking.

Taking part in a roundtable at the @gmfus in #Washington: "The recovery in Europe – the way forward" #GMFEurope pic.twitter.com/XbTqYOavIX

— Pierre Moscovici (@pierremoscovici) April 16, 2015

The IMF/G20 meeting is getting underway in Washington, with staff determined to avoid a repeat of yesterday’s antics in Frankfurt.

Staff here at IMF/World Bank meetings are on high alert for protesters masquerading as journalists, following yday’s Draghi “episode”

— Ed Conway (@EdConwaySky) April 16, 2015

Greek PM "firmly optimistic" of deal this month

Alexis Tsipras, Greece’s prime minister, has just declared that he’s “firmly optimistic” that Greece will reach a deal with its creditors in time.

With default fears growing, Tsipras told Reuters that disagreements over major issues such as pension and labour reform would be overcome in time.

Tsipras said:

“Despite the cacophony and erratic leaks and statements in recent days from the other side, I remain firmly optimistic that there will be an agreement by the end of the month.

“Because I know that Europe has learned to live through its disagreements, to combine its parts and move forward.” <end>

I’m not sure that taking a pop at Greece’s creditors for leaking information is going to mend many fences between the two sides.

And it’s hard to see how a deal can be reach without some serious concessions being made. Analysts at Nomura bank don’t share Tsipras’s optimism:

Nomura: Tsipras seems to find himself trapped btwn promises made to voters, the hardliners in his party & the demands of #Greece’s creditors

— Efthimia Efthimiou (@EfiEfthimiou) April 16, 2015

Incidentally, Tsipras just tweeted a photo of a meeting with former Greek PM George Papandreou today:

Συνάντηση νωρίτερα με τον κ. Παπανδρέου & ενημέρωση σχετικά με τις τρέχουσες εξελίξεις. #Greece pic.twitter.com/ana43Fpa1c

— PrimeMinisterGR (@PrimeministerGR) April 16, 2015

Updated

Greece denies asking to skip IMF repayment

Newsflash from Washington: Yanis Varoufakis has insisted he has not asked for a delay from the International Monetary Fund.

Greek FinMin says never asked IMF to skip payment

— NTMarkets (@NTMarketscom) April 16, 2015

So the Financial Times is wrong? Not so fast! The FT story says that Greek officials “made an informal approach” to the Fund, and were “persuaded not to make a specific request” (because it would be turned down).

The euro just hit a one-week high against the dollar after two pieces of US economic data hit the wires.

The number of Americans filing new unemployment claims rose unexpectedly, by 12,000, last week to 294,000.

And the number of new house-building projects begun in March only rose by 2% year-on-year. Economists expected a much larger bounceback after February’s slowdown (blamed on bad weather).

Housing Starts by Region: pic.twitter.com/SyiFlwuqdF

— Michael McDonough (@M_McDonough) April 16, 2015

That sent the euro up to $1.074, half a cent higher today.

Capital Economics: Greek crisis coming to a head?

A research note from Capital Economics just landed, warning that the situation in Greece may finally be escalating into a major crisis.

I’ve taken the liberty of pasting it below. It’s by Jennifer McKeown:

- The Greek crisis has reached a new crunch point amid signs that the Eurogroup will not grant desperately needed financial aid after next week’s meeting. Greece might resort to IOUs and/or capital controls to avoid a disorderly default and keep the banks afloat for now. But such measures would offer a temporary solution at best and could be the first steps towards a euro-zone exit.

- Things had gone comparatively quiet on the subject of Greece as the Government worked on a fourth version of its reform list ahead of the Eurogroup meeting on 24th-25th April. It had expressed confidence that this would secure payment of at least part of the final €7.2bn remaining from its second bailout.

- However, yesterday’s statement by German Finance Minister Wolfgang Schäuble that “nobody expects that there will be a solution” at the meeting certainly poured cold water on those hopes. The Vice President of the European Commission, Valdis Dombrovskis, also said yesterday that imminent cash disbursement was highly unlikely and suggested that reforms would have to be implemented first.

- The Greek Government, which had already warned that without more bailout money it might fail to meet its obligations next month, has reportedly now asked the IMF for an extension to loan repayments of almost €1bn due in May. But the Fund has refused, leaving open the possibility of a disorderly default. If Greece failed to make scheduled repayments to the IMF, it would be the first developed economy ever to do so and there is a chance that this would lead to its expulsion from the euro-zone.

- Assuming that a deal is not reached next week, there are a couple of routes that the Greek Government might take to avert disaster in the short term. First, it could issue IOUs to pay public sector workers and pensioners and free up money to repay its debts. But this could cause economic chaos if fears that the IOUs would never be paid sparked riots or public sector employees simply refused to work.

- Even if Greek people accepted IOUs, they could only function for a very short period. Before long, those receiving incomes in IOUs could only afford to pay their taxes through the same medium. And given that the Government’s international creditors would not accept IOUs as repayment, this would still lead to a debt default. Effectively, the IOUs would become a parallel currency whose value was deemed lower than that of a normal euro. This would be akin to a euro-zone exit.

- Another necessary stopgap may be the introduction of capital controls. For now, the Bank of Greece is keeping commercial banks afloat with Emergency Liquidity Assistance (ELA). But the ECB imposes a limit on this which it reviews every week. So far, the limit has been gradually increased and President Draghi said yesterday that there was no specific red line beyond which the ECB would refuse to condone support. But only solvent banks are eligible and the more likely a Greek government default becomes, the more questionable is the solvency of Greek banks.

- And capital controls may be deemed necessary as well as ELA if a deal is not made at next week’s meeting. Such an outcome would heighten speculation of default and exit, threatening to exacerbate greatly deposit outflows and capital controls might be required as damage limitation.

- On the face of it, the Cypriot experience with capital controls is encouraging. Controls implemented there in 2013 halted deposit outflows and were removed entirely last week without much ado. But note that deposits have not yet returned to Cyprus and banks there remain reliant on bailout funds. So capital controls alone will not be enough to save Greek banks: more money will be needed either in the form of bailout funds or the reinstatement of a waiver allowing them access to unlimited ECB loans.

- The upshot is that Greece desperately needs to receive bailout money very soon. If an agreement is not reached next week, the Government might resort to emergency measures to avoid an immediate default and euro-zone exit. But Greece will still need the remaining funds from its current bailout, a new third bailout and ultimately some kind of debt write-off if its future in the currency union is to be assured. And note that any emergency measures put in place to keep the economy afloat in the meantime could conversely put the wheels in motion to facilitate a euro-zone exit.

ECB protester Josephine Witt has been talking to our Berlin correspondent, Kate Connolly, this morning about yesterday’s events.

Asked why she registered as a journalist, got into the press room and then jumped Draghi with leaflets and confetti, Witt says:

”What I wanted to demonstrate is that economics are not just some god-given thing that we have to accept and go along with. We can try to change our economy.

If the ECB was a democratically elected institution we could use it far more for the better.”

Witt also reckons that Draghi’s shocked reaction show that he “clearly hasn’t had much [plastic surgery] done”.

Here’s the full interview:

Updated

Eurozone crisis veteran Yiannis Mouzakis fears we’re on the edge of something rather nasty....

#Greece, in the last few weeks of calm before the storm that one side thinks will never come and the other believes it can control

— Yiannis Mouzakis (@YiannisMouzakis) April 16, 2015

Protest marches are taking place in Athens today, in favour of a controversial gold mine project in northern Greece.

According to AP, around 4,000 workers are taking part in the protest. Dressed in safety vests and helmets, they are waving flags which read “Yes to mines, yes to growth.”

The protesters want the Syriza-led government to reverse its decision to revoke a permit for a key ore enrichment plant at the Skouries mine.

That site is hugely unpopular with environmental activists, who are expected to hold their own protest march in Athens tonight.

Many commentators have criticised Greece’s new government for demanding a new deal from its creditors. But it’s worth noting that Greece’s reform programme was already slipping even before Syriza took power:

Joan Hoey, Senior Analyst, Europe at the Economist Intelligence Unit, explains:

The previous New Democracy-Pasok government collapsed not because of a technical failure to elect a new president, but because it became politically impossible to implement reforms tied to Greece’s bailout programme.

In its final six months in office, the government failed to pass any significant reforms. It therefore failed to complete the fifth and final review of the bailout programme, exit from which would have brought some relief from the austerity squeeze of the past six years.

Now a radical left government elected on a mandate to reverse bailout reforms is expected to accomplish what its centre-right predecessor could not.

Here’s another view of Greece’s looming debt repayments:

Greek bond yields have been soaring this morning: View Greece’s debt repayment timetable http://t.co/7ax3rEb2qV pic.twitter.com/McrtSwZFvr

— The Economist (@TheEconomist) April 16, 2015

Note the sizeable IMF repayments in May, June and July, and the heftier sums owed to the European Central Bank in July, August and September.

(T-bills are short-term debt, typically three-month bonds, which are held by Greek banks and regularly rolled over)

The selloff in Greece’s bonds is accelerating, following the FT’s report that Athens had asked the IMF about possibly delaying some loan repayments.

#Greece's 3yr yields jump to almost 28% as #IMF knocks Greek debt rescheduling hopes. http://t.co/XhbUgg5B4p pic.twitter.com/jQ1qloWVHc

— Holger Zschaepitz (@Schuldensuehner) April 16, 2015

The message from Brussels today is depressingly familiar -- the EU wants to see more progress from Greece, fast:

We are not satisfied with level of progress made so far -says #EU spokes re. #Greece Work needs to intensify b4 informal #Eurogroup 24 April

— Méabh (@Brusselsness) April 16, 2015

Updated

William Hill closes Grexit book

I missed this earlier, but bookmaker William Hill is now refusing to take any more bets on Greece leaving the eurozone this year.

It’s seen a surge of interest, as the crisis continues to build.

NO MORE BETS http://t.co/sWAAMIoTIP pic.twitter.com/57wgLLrh2g

— Joseph Weisenthal (@TheStalwart) April 16, 2015

Updated

Regular blog readers may remember that a year ago this week, Greece made a stunning return to the financial markets.

On 9 April 2014, Athens put its toe in the water by trying to sell €3bn of five-year bonds, and was promptly swamped with €20bn-worth of bids from investors desperate for a decent return.

That bond was sold at an interest rate, or yield, of nearly 5%. A much chunkier return than you’d have got from other eurozone debt. But taking part in the auction wasn’t the brightest idea - the bond has slumped since, losing more than a third of its value.

Almost exactly 1 year ago there were €20bn of orders for €3bn Greece 5yr bond yielding 4.95%. Has since fallen almost 40% and yields 19%

— Bond Vigilantes (@bondvigilantes) April 16, 2015

Updated

Financial news service Ransquawk has rounded up the next series of debt repayments which Greece faces:

Key Greek Dates 17Apr €1b redemption 24Apr runs out of cash Apr end - €1.7b payment due for public wages&pensions 8May €1.4b redemption 1/2

— RANsquawk (@RANsquawk) April 16, 2015

Key Greek Dates: 12May €779m IMF repayment 11May Eurogroup meeting 15May €1.4b bill redemption 20July €3.5b bond redemption due 2/2

— RANsquawk (@RANsquawk) April 16, 2015

European stock markets are edging down this morning, with the Greek crisis giving little reason for optimism:

The Athens market has also dipped, by just 0.2%.

It’s not ALL doom and gloom this morning. European car industry is reviving, with sales across the EU jumping by 10.6% year-on-year in March.

Sales in Spain, Portugal and Ireland all led the way:

That last chart from Pantheon Macro - country by country breakdown here. +40% in Portugal too, +32% in Ireland. pic.twitter.com/N4GQmjxDlD

— Mike Bird (@Birdyword) April 16, 2015

Greece’s prime minister needs to make concessions to creditors soon, before the situation deteriorates further, argues Janis Emmanouilidis of the European Policy Centre, a think tank.

High time for #Tsipras government to compromise. Negative economic & political consequences too high if developments spiral out of control.

— Janis Emmanouilidis (@jaemmanouilidis) April 16, 2015

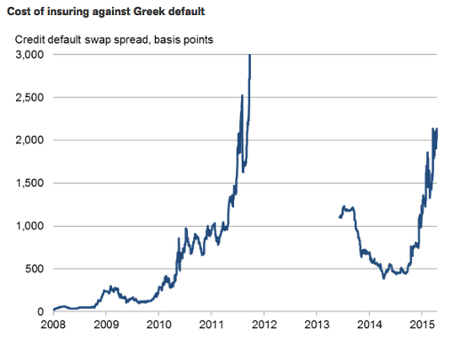

Markets price in higher risk of Greek default

The financial markets are now pricing in a 77% chance that Greece will default in the next five years, data firm Markit says.

Markit’s chief economist, Chris Williamson, explains:

The cost of insuring against a default by the Greek government has spiked sharply higher as worries about the ability to meet debt repayments have intensified.

Credit default swap prices, which provide investors with protection to insure against debt default have surged higher. The CDS market is now implying a 77% probability of default by the Greek government in the next five years, according to Markit data.

FT: Greece asked IMF about delaying debt repayments

This looks worrying. The Financial Times is reporting that Greek officials have made an “informal approach” to the International Monetary Fund to delay repayments of loans to the international lender, but were rebuffed.

It’s another sign that Athens is running perilously short of funds, and is worrying how it will meet next month’s bills (both €900m+ owed to the IMF, and its public sector wages and pensions).

Here’s the full story: IMF knocks Greek rescheduling hopes

And here’s a flavour:

According to officials briefed on the talks by both sides, Athens was persuaded not to make a specific request for a delay to the Fund, which is owed almost a €1bn in two separate payments due in May.

Although Athens was rebuffed, the discussions, which occurred in private earlier this month, are a sign that the Greek government is finding it increasingly difficult to scrape together enough money to continue to pay wages and pensions while meeting its debt payments to external lenders.

Officials representing Greece’s creditors are unsure whether Athens will be able to make the payments in May. Even if they do, they are certain that the matter will come to a head by June, before much larger payments on bonds held by the ECB start coming due.

Delaying payments to the IMF would be unprecedented for a eurozone member, and a rare event for any advanced economy.

Greece went ahead and (quietly) asked IMF if it could delay loan repayments. Quite a moment. The fund said no http://t.co/Zm5nisLmRF

— Joseph Cotterill (@jsphctrl) April 16, 2015

And the report is driving Greek bond yields even higher:

#Greece 10Y yield soars as GrGov seeks #IMF installment delay pic.twitter.com/RYeUGl3Oqv

— acheron (@acheron112) April 16, 2015

Two-year Greek bonds are now at their weakest level since last summer:

* Greek two-year bond yields rise 230 bps to 26.14 percent, highest since issue in July 2014 - Tradeweb

— Fabrizio Goria (@FGoria) April 16, 2015

Another sign of growing Greek concern:

*GREEK THREE-YEAR BOND YIELD CLIMBS TO 26.09%, MOST SINCE 2012

— lemasabachthani (@lemasabachthani) April 16, 2015

Greek bond yields surge as default fears grow

Greek government bonds are weakening this morning as concern grows that Athens and its creditors are nowhere close to a deal.

Last night’s credit downgrade from S&P is also helping to drive Greece’s bond yields higher.

The yield on 10-year Greek bonds has jumped to 12.5%, having closed at 11.9% last night. And the two-year bond yield has also spiked, up to 25.2% from 23.8% last night.

That suggests a high, and growing, risk of default.

Overnight, Greece’s largest opposition party, New Democracy, hit out at reports (since denied) that a referendum could be called:

New Democracy spokesman Costas Karagounis said:

“Just the thought of holding a referendum is an admission of an impasse. If they move forward with such an idea, they turn this impasse into a tragedy.”

The Kathimerini newspaper also reports that New Democracy now thinks Greece could be forced out of the eurozone.

ND believes #Grexit is possible. #Greece's 2yr yields jump to almost 25%. http://t.co/qizVYfkQue pic.twitter.com/3WkLK0qL58

— Holger Zschaepitz (@Schuldensuehner) April 16, 2015

The Greek crisis will be centre-stage in Washington as G20 finance ministers and central bankers gather for the IMF’s spring conference, says Mike Peacock of Reuters.

Most of the protagonists in the Greek saga will there including Finance Minister Yanis Varoufakis who is due to hold talks with both President Barack Obama and ECB chief Mario Draghi. He can presumably expect some sharp words with time running very short.

The euro zone is doubtful that a deal will be struck with Greece next week on economic reforms for bailout funds. Both the Greek government and its creditors have expressed the need for an agreement, at least in outline, to be reached when euro zone finance ministers meet in the Latvian capital Riga on April 24. But Athens has yet to produce a programme of reforms that is deemed acceptable.....

Greek drama shifts to Washington http://t.co/ucW3fl9mmy via @Reuters

— The Greek Analyst (@GreekAnalyst) April 16, 2015

Britain’s economy is also suffering from political drama.

Housebuilder Persimmon has warned shareholders that it’s harder to find building sites ahead of May’s nailbiter of a general election.

Election is stalling new house building, says Persimmon http://t.co/YGYYTh8xGo

— Julia Kollewe (@JuliaKollewe) April 16, 2015

Persimmon hopes it’s a temporary factor, but the latest polling suggests we could see deadlock after May 8th:

Latest YouGov poll (14 - 15 Apr): LAB - 35% (-) CON - 34% (+1) UKIP - 13% (-) LDEM - 8% (-) GRN - 5% (-)

— Britain Elects (@britainelects) April 15, 2015

Schäuble: Greece will suffer from impossible promises

Overnight, German finance minister Wolfgang Schäuble chastised Greece’s government for making promises it can’t deliver on.

In remarks that are likely to irk Athens, Schäuble argued that Greece was doing better than expected - until the election three months ago.

Schäuble told an audience at Columbia University that:

“I have told Prime Minister [Alexis] Tsipras, if you promised to your electors in campaigning that you will get recovery and stay within the euro zone without sticking to the program, you will suffer.”

We don’t yet have official growth data for Greece, but various surveys do suggest it has stumbled since January’s election was called.

Updated

The IMF/G20 Spring meeting is the main event in the financial world today, says Michael Hewson of CMC Markets.

And with little in the economic calendar, Yanis Varoufakis’s brief meeting with president Obama will also get some attention. But it may not yield much for Greece, Hewson warns:

Unfortunately for Mr Varoufakis, sympathy is probably the only thing he will receive in the wake of yesterday’s S&P downgrade of Greece to CCC+ with a negative outlook, and last week’s meeting between Greek Prime Minister Tsipras and Russian President Vladimir Putin.

The new Greek government is slowly realising that when you’re trying to negotiate a deal with your creditors, it pays to at least try and generate some consensus and goodwill amongst some of them, and not cosy up to a Russian President who is probably not the most popular person amongst European and US officials at the moment.

Early action in the bond markets: German 10-year bunds are hitting fresh record highs again today, sending the interest rates on its debt down again.

The 10-year bund yields has just fallen below 0.1% for the first time ever:

10y Bunds at 0.099%

— Alberto Gallo (@macrocredit) April 16, 2015

Bunds are in huge demand thanks to the weak inflation outlook, market jitters, and the prospect of selling them for a profit to the ECB through its QE scheme.

Mario Draghi can take a sigh of relief.

Josephine Witt, the activist who disrupted his press conference yesterday with a shower of confetti and anti-ECB leaflets, has left Frankfurt.

Bye, Bye, #ecb pic.twitter.com/fgDfRTpT4o

— Josephine Witt (@josephine_witt) April 16, 2015

And here’s a video of the protest, for anyone who missed it yesterday (where were you?!).

Updated

The Agenda: Greek crisis looms over IMF-G20 Meeting

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

After the excitement of yesterday’s glittering of Mario Draghi, we’re back to the hard grind of worrying about Greece.

Finance chiefs from around the globe are gathering in Washington today for the International Monetary Fund/G20 Spring Meeting, with the Greek debt crisis looming.

Yanis Varoufakis, Greece’s finance minister, is in town, and due to meet with Barack Obama. But it’s probably only going to be a fleeting chat; not much time for Varoufakis to pitch his case to the US president.

The possibility of a Greek default is causing growing tension in America; last night, Treasury Secretary Jack Lew urged both sides to reach a deal fast.

Lew told Bloomberg that Grexit would be a major blow to the country:

“There’s no doubt that if this leads to a crisis such as Greece leaving the euro zone, it will cause an enormous amount of disruption and hardship in Greece,”

“Even if the contagion risk is much less now than it was, say, in 2012 and earlier, it would not be a good thing in a world economy just recovering from a deep recession to have that kind of uncertainty introduced.”

But Germany’s Wolfgang Schäuble appears to have dashed hopes of a breakthrough next week.

He told an audience in New York last night that there was almost no chance of a deal at next Friday’s eurogroup meeting in Riga.

As Schäuble put it:

“No one has a clue how we can reach agreement on an ambitious programme.

We have the next Eurogroup meeting at the end of the coming week, but nobody expects that there will be a solution.”

If he’s right, Greece is going to enter May without the bailout funds it needs to help cover public sector wages and debt repayments.

And as we covered last night, Standard & Poor’s added to the pressure on Athens by warning that there is a high risk of Greece defaulting, and cutting its credit rating to just CCC+ (deeper into junk).

Europe’s financial markets remain sanguine about the crisis; the main indices are expected to be pretty calm this morning. But Greek bonds could take another kicking on the back of the S&P downgrade.

We’ll be covering all the main events through the day.

Updated