European markets close higher on Greek deal hopes

Deal or no deal - markets went for the former, and moved higher on hopes that Greece was about to come to an arrangement with its creditors. Whether that was the case or not, investors decided to push shares higher anyway. The closing scores showed:

- The FTSE 100 ended up 84.34 or 1.21% at 7033/33

- Germany’s Dax added 1.26% to 11,771.13

- France’s Cac closed 1.95% better at 5182.53

- Italy’s FTSE MIB rose 2.29% to 23,861.07

- Spain’s Ibex ended 1.7% better at 11,431.1

- The Athens market jumped 3.55 % to 851.81

In the US, the Dow Jones Industrial Average is currently up 114 points or 0.s6%.

On that note, it’s time to close up for the evening. Thanks for all your comments, and we’ll be back tomorrow.

Greek deal pic.twitter.com/QUw9XAyLVr

— Morris Cabrioli (@insidegame) May 27, 2015

As so often, journalists in Brussels are getting a more pessimistic picture than those in Athens:

Like lots of other people are reporting, the line I'm getting from creditor side of #Greece negotiations is that no deal is imminent.

— Peter Spiegel (@SpiegelPeter) May 27, 2015

Intriguing.....

#Greece FinMin Varoufakis' notebook caught by a photographer's zoom lens today. pic.twitter.com/x4pfkkqDkn

— Yannis Koutsomitis (@YanniKouts) May 27, 2015

#Greece PM Tsipras says "calm and decisiveness needed now that we're on the final stretch to an agreement" ► https://t.co/6MXNy2XM4P

— Yannis Koutsomitis (@YanniKouts) May 27, 2015

European Commission insiders are insisting that Greece is NOT, repeat NOT, on the brink of a deal, despite Tsipras’s optimistic comments.

One official has told Reuters that the remarks coming out of Athens are “nonsense”.

Another said: “I wish it were true.”

Reuters also has the full rebuttal from European Commission Vice President Valdis Dombrovskis. He said:

“We are working very intensively to ensure a staff-level agreement. We are still not there yet.”

Greek optimism is driving Europe’s stock markets higher and higher.

The FTSE 100 index is flirting with a triple-digit jump, despite Brussels officials pouring cold water on talk of an imminent deal.

Would you believe it?

An EU official has denied that Greece and its creditors are working on a staff-level agreement, as that Athens official claimed an hour ago.

EU Official: Greek creditors not yet drafting final accord. Greece, creditors always working toward agreement. (BBG) pic.twitter.com/AxBiT5re8D

— Holger Zschaepitz (@Schuldensuehner) May 27, 2015

Here’s the moment that Greece’s prime minister declared that the long, long awaited deal might be close....

PM Tsipras: We are close to deal that will be "positive for the Greek economy" #Greece pic.twitter.com/bGVxbVDOY2

— Derek Gatopoulos (@dgatopoulos) May 27, 2015

Tsipras: We are on the final stretch to a deal

It’s official! Greece believes that it is close to a deal with its lenders.

Prime minister Alexis Tsipras has just announced that the details will be presented ‘soon’, and insisted there is no danger that wages and pensions won’t be paid.

But Tsipras also said that Greece’s creditors are divided over some issues, which surely means a deal cannot be imminent.

Here are the newsflashes from Reuters:

- GREEK PRIME MINISTER TSIPRAS SAYS WE HAVE MADE MANY STEPS, WE ARE ON FINAL STRETCH TOWARDS POSITIVE DEAL

- GREEK PRIME MINISTER TSIPRAS SAYS WE WILL PRESENT DETAILS ON DEAL SOON

- GREEK PRIME MINISTER TSIPRAS SAYS THERE ARE STILL DIFFERENT APPROACHES AMONG LENDERS

- GREEK PRIME MINISTER TSIPRAS SAYS WAGES AND PENSIONS WILL BE PAID NORMALLY THIS WEEK

- GREEK PRIME MINISTER TSIPRAS SAYS THERE IS NO RISK TO BANK DEPOSITS

Updated

Now this may be significant.... Tom Nuttall, who write the Economist’s Charlemagne column from Brussels, has heard that eurozone finance minister could meet next week to sign off a Greek deal.

That’s only if their deputies report that there is progress, after their conference call tomorrow.

EWG conference call 2mo afternoon, if institutions give "positive verdict" on progress in Greece, cd b "decisive" Eurogroup next wk - source

— Tom Nuttall (@tom_nuttall) May 27, 2015

Oh look! A denial, from European Commission vice-president Valdis Dombrovskis:

*DOMBROVSKIS SAYS `WE ARE STILL NOT THERE' ON GREECE TALKS

— Michael Hewson (@mhewson_CMC) May 27, 2015

The IMF is declining to comment on Greece’s claims....

Over to Reuters for full details of these rumours of a deal that sent shares rallying in Athens.

Greece says has begun drawing up agreement with creditors

Greece and its creditors are starting to draft a technical-level agreement that will include no more wage or pension cuts, a government official said on Wednesday.

The official said:

“At the Brussels Group today procedures to draw up a staff-level agreement are beginning.”

The statement appeared to suggest significant progress in talks with EU and IMF creditors that form the Brussels Group, though sources close to the lenders have so far not indicated any such progress to merit drawing up an agreement.

The official also cited differences between the EU and IMF as holding up an overall deal.

“There remains a problem with the differing stance among the institutions. If an agreement by the IMF was not needed, the deal would have closed by now.”

Updated

Markets rally on talk of a Greek deal

Greek bond yields fell sharply as soon as investors heard that Greece and her creditors have, apparently, started drawing up the terms of a deal.

According to this one official, the proposed agreement includes overhauling Greece’s VAT tax, but avoids ‘recessionary measures’ and also confirms lower primary surplus targets.

This sent the yield, or interest rate, on Greece’s 10-year debt fell from 11.9% to 11.4%, meaning traders see it as less risky.

Greek10yr yields drop like a stone as #Greece, Creditors start crafting staff level accord. pic.twitter.com/X8fQsnCSde

— Holger Zschaepitz (@Schuldensuehner) May 27, 2015

The Athens stock market also jumped in the last few minutes of trading; bank shares gained 3.4%.

Quite a reaction, given these comments only come from one unnamed Greek official. Especially as this official has apparently also cautioned that the IMF is holding progress up.

So, this is "let's gang up on the IMF", then, isn't it? #Greece

— Frances Coppola (@Frances_Coppola) May 27, 2015

Those upbeat comments from Athens also drove the German stock market higher.....

This is how #German market DAX reacted to a headline from Greece pic.twitter.com/fqnbXmXkyn

— *Russian Market (@russian_market) May 27, 2015

But this optimism might not last long; let’s see what Brussels makes of this talk of a deal.....

Curious.... Bloomberg is quoting a Greek official saying that the two sides have started drafting a staff-level agreement; basically a deal that could be approved by eurozone ministers.

*GREECE, CREDITORS STARTED CRAFTING STAFF LEVEL ACCORD: OFFICIAL - what??

— Michael Hewson (@mhewson_CMC) May 27, 2015

*GREEK BANK DEPOSITS ARE SAFE, GOVT OFFICIAL SAYS

— Michael Hewson (@mhewson_CMC) May 27, 2015

*GREECE DEAL TO INCLUDE LOWER PRIMARY SURPLUSES: GOVT OFFICIAL

— Michael Hewson (@mhewson_CMC) May 27, 2015

However, here comes the snag....

*GREECE SAYS DISAGREEMENTS AMONG CREDITORS A PROBLEM: OFFICIAL

— Michael Hewson (@mhewson_CMC) May 27, 2015

The reports are pushing shares higher in Europe; the FTSE 100 has now gained 80 points, or 1.1%, to 7031.

Markets getting a boost at the moment as the latest comments regarding #Greece suggest a deal could be forthcoming

— RANsquawk (@RANsquawk) May 27, 2015

Algos see 'Greece', 'accord' and 'crafting' and have gone for it

— World First (@World_First) May 27, 2015

(that’s a reference to algorithmic, or high-speed computer trading)

Benedict James, banking partner at global law firm Linklaters, has warned that Greece could trigger a meltdown in its banking sector if it fails to repay the IMF €1.6bn next month:

“The Greek government and Greek banks are trapped in a death embrace, with the government only appearing solvent because the Greek banks agree to roll over Greek government bonds as they mature, and the Greek banks only do that because they can use the bonds as collateral with the ECB under a facility which only works as long as the Greek government looks solvent.

But if the Greek government defaults to the IMF, then the ECB will probably have withdraw the current collateralised liquidity facility, whereupon the Greek banks will be very bust. This takes us into the world of the Single Resolution Mechanism which would probably involve a massive good -bank/bad-bank split, and a huge resolution of the bad banks’ assets.”

Summary: America turns up the heat over Greek crisis

Time for a recap.

Speaking at the London School of Economics, Treasury secretary Jack Lew said both sides need to drop the rhetoric, avoid brinksmanship and reach a deal quickly before an accident occurs.

He warned:

You have moments that come up with all too much frequency when a miscalculation could lead to the crisis that would be potentially very damaging.

and also cautioned against thinking that a Greek default would be easily manageable.

The notion that there is no contagion ....I think it’s a mistake to think that a failure is no consequences outside of Greece.

Lew is now heading to Dresden, to meet with finance ministers and central bank chiefs. Greece isn’t officially on the G7 agenda, but behind the scenes it seems likely that Lew will be pushing for a resolution.

In other news....

Greece has insisted that it did not seek fresh liquidity help from the European Central Bank today, because deposit outflows have stabilises.

Banking insiders, though, have claimed that €300m was withdrawn on Tuesday alone, driven by fears of looming capital controls.

But a meeting between Greek officials and creditors was delayed by air traffic problems in Belgium. Instead of Brussels, they’ve ended up in Dusseldorf.

Greek negotiating team stuck in Dusseldorf - PHOTOS - http://t.co/pYXo2Z5SDZ

— enikos_en (@enikos_en) May 27, 2015

Euro officials have warned that little progress has been made in recent days, meaning no chance of a deal before the weekend. There goes another deadline....

And economists fear that time is running out. As Christian Schulz of Berenberg bank warned:

Every day of delay deepens the recession, destroys international trust, reduces bank deposits, hurts companies and increases job losses.

Updated

Greece’s prime minister has begun holding a meeting with his top financial advisers over the bailout crisis:

Ξεκίνησε η σύσκεψη στο υπουργείο Οικονομικών pic.twitter.com/91MFtUJoKA

— Giannis Politis (@GiannisPolitis) May 27, 2015

The meeting at the MinFin has begun. Love those smiley cheekbones on #Varoufakis and #Tsipras. All is dandy! #Greece https://t.co/GDdQAEQbVO

— The Greek Analyst (@GreekAnalyst) May 27, 2015

Over in Dresden, the police are out in force ready for the start of the G7 meeting of finance ministers and central bank chiefs:

Campaign group ONE has brought along balloons showing the faces of world leaders including David Cameron (left), Shinzo Abe (centre) and Angela Merkel (right)

Those leaders aren’t due in Dresden for another two weeks; the main G7 summit is on 7 and 8 June.

Updated

The Greek government has announced that the European Central Bank left the emergency liquidity limit unchanged today because Greek banks did not request any more money.

That could calm fears that the ECB was playing hardball today, to drive Greece into a deal.

Helena Smith reports from Athens:

The leftist-led government announced in a statement that:

“The ECB did not increase ELA because the Bank of Greece did not request an increase, as it was considered that the threshold of €80.2bn was adequate.”

That was because outflows had been “stabilised,” it added (which would not seem to chime with earlier reports about outflows accelerating).

The statement also confirmed that a travel hitch delayed the 2pm start of talks by the Brussels Group, meaning the Greek team ended up 200km away in Dusseldorf:

“The Brussels group work session was due to start at 2 PM. It will be delayed however because of a problem at Brussels airport which forced the plane carrying members of the Greek mission to land in Dusseldorf.

The Brussels Group is important because it will handle the last things still outstanding from the agreement.”

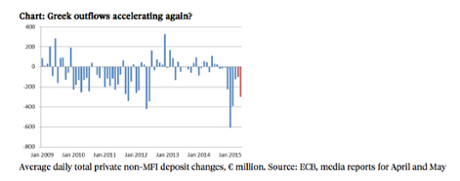

Reuters: Greek bank outflows accelerated in May

Sources in the Greek banking sector have told Reuters that savers pulled more money out of Greek banks in the last week.

One said:

“The past week in May was more challenging compared to the previous ones in the month, with daily outflows of 200 to 300 million euros in the last few days,”

They also reckon around €5bn was withdrawn from Greek banks during April, up from below €2bn in March, as fears of a default grow.

We get official figures from the Bank of Greece tomorrow.

Updated

At the north of the eurozone, Finland’s new coalition government is taking shape.

Former prime minister Alex Stubb has been given the job of finance minister, meaning the right-winger will be attending eurogroup meetings where Greece’s bailout is discussed.

There had been speculation that eurosceptic Timo Soini would get the finance brief; instead, he’s been rewarded with the foreign office.

Alex Stubb is Finland's new finance minister. Timo Soini, leader of True Finns, is foreign minister.

— Richard Milne (@rmilneNordic) May 27, 2015

Soini is implacably opposed to any more Greek bailouts, and has called for Greece to quit the eurozone..

Interesting new Finnish govt has Stubb as Fin Min & Soini as For Min, might have been other way. Means no Soini v Varoufakis at #Eurogroup

— Open Europe (@OpenEurope) May 27, 2015

Here’s another sign that Alexis Tsipras is taking personal responsibility for the bailout talks:

PM Alexis #Tsipras to hold meeting with Greek negotiating team at Fin Min HQ at 3 p.m. #Greece

— Kathimerini English (@ekathimerini) May 27, 2015

Today’s meeting between Greece and its creditors has apparently been delayed, because the Greek team has suffered transport problems:

Brussels Group meeting to be delayed following Greek flight delay, local media report #Greece

— Kathimerini English (@ekathimerini) May 27, 2015

That must be due to the closure of Belgian airspace this morning, after an air traffic control failure.

PHOTO Close to chaos inside terminal at @BrusselsAirport due to airspace closed (@TeleBXLActu) http://t.co/jG2NfZLwT1 pic.twitter.com/NAK1w1lQgw

— AirLive.net (@airlivenet) May 27, 2015

German bank Berenberg has published a scathing assessment of Greece’s situation today, warning that the new government has been an “unequivocal disaster”.

Every day of deadlock brings more pain to the Greek economy, warns senior economist Christian Schulz, who writes:

Anyone following the Greek situation must be wondering, what Prime Minister Tsipras is holding out for. While the Greek economy and its financial system are increasingly at peril of a major collapse, Syriza has achieved virtually nothing in the negotiations with the troika. The key conditions for remaining €7.2bn disbursement from the second bail-out remain the same. Worse, a follow-on package is inevitable come July, and with Eurozone and IMF trust shattered, the conditions will have to be tough and the monitoring of the implementation is going to be very tight. Compared to what a hypothetically re-elected Samaras would probably have achieved, Tsipras has been an unequivocal disaster.

Are things coming to a head now? Today, the ECB apparently left the ELA limit unchanged at €80.2bn. This was only the second time since February that it did so and it comes as a surprise. Deposit outflows have re-accelerated according to some Greek media reports to €300m per day from €100m as recently as last week. This may not threaten the immediate liquidity position of Greek banks, who last week were said to have an ELA buffer of €3bn. But there are two reasons for concern. (1) The minority in the ECB who are openly worried about the impact of the deepening Greek recession on Greek banks solvency seems to be growing and putting pressure on the majority to limit the risks to the institution. (2) With no clear data about banks’ liquidity position available, the unchanged ELA limit could trigger more concerns by Greek households and companies about potential capital controls and thus trigger accelerated withdrawals.

Greek finance minister Varoufakis may increasingly worry Greeks, too. Not just has he become a disturbing factor in the negotiations with the troika. His – swiftly denied - toying with a tax on ATM withdrawals may get people additionally worried about capital controls. In the current uncertain environment, many may believe that where there is smoke, there is also a fire.

Given that a very strong minority of their governing party openly sympathise with euro exit and given that the government has made little progress in the negotiations while at the same time sinking the Greek economy back into recession, Greeks have remained remarkably sanguine about their bank deposits. After a brief spike just after the January elections, deposit outflows had normalised to relatively small amounts. However, the apparent re-acceleration of outflows could herald new depositor nervousness, potentially aggravated by the ECB and Varoufakis. That would be one way of forcing the Greek issue, alongside the government running out of money.

Prime Minister Tsipras is in a very difficult situation. On the one hand, the Eurozone and the IMF will not help him deliver his impossible election promises. On the other hand, large parts of his party are not yet pragmatic enough to water down these promises and put the interest of the country above ideology. Tsipras depends on the left-wingers around energy minister Lafazanis for his job. The opposition might help him get the approval for the necessary laws in parliament to keep Greece afloat, but will demand conditions that could eventually spell the end of the Tsipras government and even his political career. It is a tough decision which Tsipras is understandably putting off. But every day of delay deepens the recession, destroys international trust, reduces bank deposits, hurts companies and increases job losses.

Updated

Jack Lew has spoken with Greece’s prime minister, Alexis Tsipras, by phone, according to journalist Michail Ignatiou.

Είχαμε νέο τηλεφωνική επικοινωνία του Αμερικανού υπουργού Οικονομικών και του κ. Τσίπρα. Οι Αμερικανοί ανέλαβαν τη διαπραγμάτευση;

— Michail Ignatiou (@mignatiou) May 27, 2015

That’s another sign that America is taking a more prominent role in the crisis.

As flagged up this morning, Washington wants to calm the Greek situation to avoid the risk that Athens seeks help from Moscow, which would have a destabilising effect on Europe and the NATO alliance.

While Jack Lew was urging Greece and her creditors to treat the next deadline as the last one, Bloomberg was reporting that, well, the next deadline is about to be clattered.

They say:

Greece will likely miss a deadline for a deal with creditors by the end of the week as the two sides have made little progress during talks in recent days, four international officials familiar with the matter said.

Greece is nowhere close to an agreement with the European Commission and International Monetary Fund over the terms of a continued bailout for the country, said the people, who asked not to be identified discussing private negotiations. German Chancellor Angela Merkel and French President Francois Hollande last week set a target to reach a deal by the end of May.

Greece Likely to Miss May Deal Deadline as Talks Go Nowhere http://t.co/rp0CskJRbc

— Bloomberg Markets (@markets) May 27, 2015

Updated

Matt Klein of FT Alphaville sums up Jack Lew’s trip across the Atlantic:

Once again, Americans have to step in to solve Europe's problems.

— Matthew C. Klein (@M_C_Klein) May 27, 2015

Jack Lew is covering a range of other issues during his talk at the LSE, including trade negotiations, China, and cyber-security.

Fortunately Observer economics editor Heather Stewart is in the audience, tweeting all the key points:

US Treasury Sec underlines importance of new trade deals (eg. TTIP): insists they will boost labour laws, consumer standards. #LSEUS

— Heather Stewart (@heatherstewart3) May 27, 2015

Lew: confident Congress will pass delayed IMF reform. "Challenge is how to bring voices of emerging econs into existing frameworks." #LSEUS

— Heather Stewart (@heatherstewart3) May 27, 2015

Lew: trade deals will boost lab, enviro rules: "to level playing field...one needs to have some acceptance of these higher standards" #LSEUS

— Heather Stewart (@heatherstewart3) May 27, 2015

Asked biggest challenges over 5-10 years, Lew singles out "cyber risks". Must "change our trusting habits" of opening attachments. #LSEUS

— Heather Stewart (@heatherstewart3) May 27, 2015

Lew also predicted that the US economy would bounce back from its slowdown last winter:

Sec Lew: weak Q1 growth in US was "somewhat anomalous": second half should be stronger. "The core strength in the economy is clear". #LSEUS

— Heather Stewart (@heatherstewart3) May 27, 2015

But some in the audience aren’t happy:

Round of applause from ex-pats for grumpy questioner saying US financial regs make life tough for Americans living/banking overseas. #LSEUS

— Heather Stewart (@heatherstewart3) May 27, 2015

Updated

US Treasury secretary warns against brinksmanship over Greece

It’s pretty clear that Jack Lew will be banging heads together at the G7 meeting of finance ministers to get a deal on Greece.

Asked if he’s optimistic that a compromise will be found, the Treasury secretary tells his audience at the LSE that he always tries to be optimistic.

But still, this crisis needs resolving fast, he says:

Brinksmanship is a dangerous thing when it only takes one accident.

Everyone has to double down, and treat the next deadline as the last deadline and get this resolved.

The risk of going from deadline to deadline only increases the risks of an accident.

And that’s the end of the Greek questions - highlights start here.

Lew: "profoundly in the interests of the US + European economies for the accident to be avoided. Brinksmanship is a dangerous thing". #lseus

— Heather Stewart (@heatherstewart3) May 27, 2015

Updated

Jack Lew repeats his warning against being complacent about the risks if Greece were to default on its loans.

Greece is going to have to manage to draw up a credible plan, he says,...but I’ve told other parties there should be no sense that we know exactly what happens if Greece has a crisis.

The notion that there is no contagion ....I think it’s a mistake to think that a failure is no consequences outside of Greece. We don’t know the exact scope.

There is no doubt that the worst and deepest consequences would be felt in Greece, but it is “profoundly in the interest of the Europeans and the global economy” that an accident is avoided, that Greece makes the moves it must make, and the institutions move with it.

Updated

Lew: I fear a Greek accident

It sounds like Jack Lew has come to Europe to knock heads together.

I’ve been saying consistently that everyone must “park rhetoric on the side” and find a sensible place where compromise can be found, he tells his audience at the London School for Economics [livefeed]

That means Greece must to do some “very tough things which will be a challenge for the prime minister to sell at home”.

The institutions must look at what it will take to show there is a credible path forwards.

Progress has been made, but not enough for it to be resolved. And there’s always another deadline approaching.

My concern isn’t the goodwill of the parties, Lew continues - his big worry is an accident.

You have moments that come up with all too much frequency when a miscalculation could lead to the crisis that would be potentially very damaging.

Updated

Jack Lew: Greece crisis must be resolved.

Treasury Secretary Jack Lew is issuing a call to arms to resolve the Greek crisis quickly before it blows out of control.

Speaking at the LSE right now, Lew says that he’s sure that issue of Greece will come up when G7 finance ministers meet in Dresden for this week’s meeting.

Lew says that the situation is Greece is familiar, and more stable than in 2012 because more of its debt is owned by sovereigns.

But still:

No-one should have a false sense of confidence that they know what the result of a crisis in Greece would be.

It would not be a good thing to see an economy in crisis, a run on Greece’s banks, which would leave people in other countries wondering what would happen if they hit a difficult moment.

It is in everyone’s interest that this is resolved, Lew continues.

Greece must come up with a package of credible economic reforms measures, that deals with fiscal challenges and provides structural reforms.

And if it does that, the challenge for the Europeans and the IMF is to show enough flexibility to help resolve the situation safely.

US Treasury Sec Lew says at G7 he will be urging Europe and IMF to "treat every deadline as the last" on Greece. Fears an "accident". #LSEUS

— Heather Stewart (@heatherstewart3) May 27, 2015

More to follow....

Updated

Heads-up. US Treasury Secretary Jack Lew is about to begin discussing the global economy over at the London School for Economics.

He’ll be setting the scene ahead of the G7 meeting in Dresden this week. There’s a livefeed here.

Live webcast today from 10.45 : in Conversation with Secretary Lew #LSEUS http://t.co/xS9DFXXfOf #USpolitics #economy #LSEUS

— LSE Events (@LSEpublicevents) May 27, 2015

Report: ECB leaves Greek emergency liquidity unchanged

News is coming in that the European Central Bank has decided to leave Greece’s emergency liquidity limit unchanged, at its current €80.2bn.

#ECB said to leave Greek ELA ceiling unchanged

— Francine Lacqua (@flacqua) May 27, 2015

Last week the ECB raised the limit by €200m, which insiders said meant Greek banks had some €3bn of wriggle-room left.

So even after losing €300m of deposits yesterday, there’s still some emergency funding to tide them over for a bit longer...

Early ELA announcement - an easy decision for once? Moment of truth coming soon.

— Frederik Ducrozet (@fwred) May 27, 2015

Kathimerini: €300m withdrawn from Greek banks yesterday

Worried Greek savers withdrew around €300m from their accounts yesterday, more than the daily average, according to the Kathimerini newspaper.

It blames worries about the IMF repayments due in June, rumours that capital controls could be imposed over the upcoming long weekend, and a suggestion that a levy could be imposed on bank withdrawals soon (this appears to be off the agenda though).

It’s not a full-blown panic, though.

As Kathimerini puts it:

Credit sector professionals reported that deposit outflows on Tuesday alone came to 300 million euros, against about 100 million euros per day in recent days.

They said that while this amount is quite high, the situation is under control as citizens are remaining calm on the positive messages from Greek officials.

Some 300 mln left banks on Tuesday http://t.co/vqRKWUAGT5

— Kathimerini English (@ekathimerini) May 27, 2015

These withdrawals leave Greece’s banks increasingly dependent on the emergency liquidity doled out by the European Central Bank.

The Athens stock market gained almost 1% in early trading today as fears over Greece’s bailout talks recede, a little.

Bank shares are among the biggest rises, pushing the ATG index towards the two-month high recorded last week.

The rally suggests investors are less worried that Greece could suffer a default soon. It owes €1.6bn to the IMF next month, starting with €305m on June 5th.

That payment had emerged as a hard deadline for Greece, but it now appears that it could bundle all June’s obligations into a single chunky payment at the end of the month.

As the WSJ explained on Monday, that would let Athens buying a bit more time and and ‘fight to the bitter end’. But it wouldn’t help Greece meet the €6.7bn it owes to the European Central Bank in July and August.

Dresden police welcoming-committee quite enthusiastic about #G7 it seems. pic.twitter.com/9cdpjetsYx

— Jeff Black (@Jeffrey_Black) May 27, 2015

Ilya Spivak of DailyFX says traders will have an eye on the G7 meeting in Dresden, which runs from today until Friday.

“Greece is likely to feature prominently in the discussions, and traders will keep a close eye on headlines emerging from the sit-down for direction cues.”

German consumer confidence hits 13 year high

The German public don’t appear to be spooked by the Greek crisis.

Consumer confidence in Germany has jumped to its highest level since October 2001, according to market research company GfK.

It explains that:

“Very strong domestic demand in Germany and the low rate of inflation are fuelling economic expectations and consumers’ willingness to spend.”

Having said that...Greece’s future in the eurozone, the Ukraine crisis and the rise of the Islamic State could all dampen confidence this summer, GfK says.

So are Germans being resolute, or not quite paying attention to events? Carsten Brzeski, ING Germany’s chief economist, isn’t quite sure.....

Die-hard optimists or just sleepyheads? German consumer confidence climbs to highest level since October 2001.

— Carsten Brzeski (@carstenbrzeski) May 27, 2015

The Greek government has told its technical staff in Brussels to “close all issues as soon as possible but without retreating from the red lines”, the AMNA newswire reports.

Those lines are Greece’s primary surplus targets (ie, how much revenues should exceed spending, stripping out debt payments), pensions, labour market reforms, and Greek VAT rates.

US could demand action on Greece at G7 meeting

The Greek crisis is likely to dominate a meeting of finance ministers from the G7 industrialised nations in Eastern Germany, which begins tonight.

America’s Jack Lew, Germany’s Wolfgang Schauble, Britain’s George Osborne et al will gather in Dresden to discuss the global economy.

One official told Reuters that the US delegation will push for a breakthrough in the long-running talks.

“The Americans are stressing the geopolitical risks and telling us we have to find a solution, that we cannot really put the euro area and Europe at risk because of Greece.”

Washington fears that without aid soon, Athens could be forced to turn to Moscow for help, undermining the West’s efforts to keep Vladimir Putin in check.

As our unnamed official put it:

“If Greece for some reason were to turn to Russia and Moscow would get involved more, they could get too much influence inside NATO and inside the EU when it comes to policies towards Russia.”

Updated

The London stock market is clawing back some of yesterday’s losses. In early trading, the FTSE 100 has risen 29 points, after tanking by over 80 yesterday.

Other European markets are also inching higher.

Mike van Dulken of Accendo Markets says Greece’s bailout deadlock send “mild panic” through the markets on Tuesday.

As a June deadline approaches for Athens to make its next IMF repayment, both the Greek government and its creditors are scrambling to ease fears of an imminent default and potential exit from the Eurozone.

The Agenda: Greek negotiations resume as time runs short

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

Officials from Greece and her creditors will make another attempt to hammer out a deal to unlock bailout funds today, as they sit down for negotiations in Brussels.

Time is short; eurozone deputy finance ministers are due to hold a Euro Working Group teleconference on Thursday, and they’d like to hear there’s been some progress this week.

But the two sides remain divided over key issues, including labour market reform and pension rates across Greece’s battered economy. And without a breakthrough soon, it’s not clear Athens can receive fresh aid before the next wave of bills start to arrive in June.

Yesterday, shares across Europe fell as confidence was hit by the lack of Greek progress, and they could be edgy today unless we see some action.

Investors were also alarmed by the success of left-wing parties in Spain’s regional elections.

Expectations that Spain’s right-wing PP party will win this winter’s election have been dented by the surge in support for the anti-austerity Podemos movement, and the centre-right Ciudadanos party.

As Michael Hewson of CMC Markets sums up:

Yesterday’s sell off in European markets serves as a timely reminder that despite the recovery in the Spanish economy, politics has a nasty habit of reminding EU policymakers that away from their spreadsheets and flow charts of economic models, there is a human equation that adds an unpredictable element to all of their best laid plans.

With a Spanish election coming in Q4 of this year and unemployment still at an eye wateringly high level above 20%, and youth unemployment still over 50% it seems highly improbable given last weekend’s results that the incumbent government will see any benefit in the main poll later this year, unless significant inroads are made to these numbers between now and polling day.

There’s not much on the agenda today -- the ‘highlight’ is the Bank of Canada’s interest rate decision at 3pm BST.

But we’ll be tracking all the main events through the day...