And that, I think, is all for another day. G’night all! GW

Capital Economics: US interest rate rise is coming.....

A September interest rate hike is still on the cards, says Steve Murphy of Capital Economics.

Here’s his take on the Federal Reserve’s statement:

In its latest FOMC policy statement, the Fed did not provide any clear hints that a September rate hike is coming. Nevertheless, this doesn’t mean that it won’t happen, especially since the statement sounded a bit more upbeat on the economy.

The policy statement was largely unchanged, with only some minor tweaks to acknowledge the improvement in the economic data. The housing sector is described as showing “additional” rather than “some” improvement, jobs gains are now thought to be “solid” and the unemployment rate is “declining” rather than “remained steady” as before.

These tweaks fall well short of a clear hint that a rate hike is coming at the next meeting in September. Note the Fed flagged up a hike at the meeting before the first rise in the tightening cycle in 2004. Nonetheless, Yellen has recently stressed that each meeting is “live” and “data dependent” so this was always unlikely. The more positive tone of the statement is a sign that the first rate hike is coming closer.

Given that in June 15 of 17 officials expected rates to rise this year and 10 of 17 anticipated two 25 basis-point increases, there’s a good change that rates will rise at two of the three meetings left this year. September is very much in play, especially if international risks continue to recede and core inflation continues to strengthen.

Our view is that the Fed will raise rates at the September meeting and to 0.50-0.75% at year-end. Perhaps more importantly, stronger wage growth and core inflation will prompt rates to rise by more than currently anticipated by the markets, taking them to 2.25-2.50% by end-2016.

Tom Porcelli, chief U.S. economist at RBC Capital Markets, says the Fed will want to ensure that the two employment reports between the July and September meetings aren’t “duds” before signalling that they’re ready to raise borrowing costs.

Janet Yellen and colleagues will also be watching for any global risks flaring up, which could knock a rate rise off course. That’s via Marketwatch:

The Fed didn't shed any light on the timing of an interest-rate hike: http://t.co/cDARs3ldt6 pic.twitter.com/V5EKX5axaX

— MarketWatch (@MarketWatch) July 29, 2015

Analysts at BNP Paribas, the French bank, say the Fed has left its options open with today’s little-changed statement on monetary policy:

Here’s a flavour of BNP’s new note to clients:

- Before lift-off the Fed also wants to be reasonably confident in its forecast for inflation to return to target over the medium-term; crude oil prices falling 17% and the dollar appreciating further probably did not increase their confidence, but there was no explicit sign in the statement that the Fed is losing confidence on its inflation outlook – we will get more intel on this when the June meeting minutes are released.

- We think the Fed will continue to assess rate hikes on a meeting-by-meeting basis. In Yellen’s testimony before Congress two weeks ago, we heard that the Fed wants to see a bit more labor market improvement before lift-off – this is exactly what the statement said.

- With two payrolls reports before the September FOMC, the Fed does not know when it will have that improvement in the bag and wants to keep its options open. The majority of market forecasters think we could be there before September. We think December. The Fed is confident we’ll get there before year-end.

Here’s all you really need to know about the Federal Reserve’s announcement:

Fed says the labor market and housing have improved, moving closer to rate hike - without providing a clear signal on the timing of liftoff.

— Francine Lacqua (@flacqua) July 29, 2015

Fed committee kept its description of risks to the outlook for the economy and labor market as “nearly balanced.” Decision was unanimous.

— Francine Lacqua (@flacqua) July 29, 2015

Updated

The US stock market had a brief fluctuation at Fed o’clock, but it didn’t last long.

Dow Jones pares most of the gains after the FOMC statement as investors have no clue what to do w/ the statement. pic.twitter.com/SM8TReNQFS

— Holger Zschaepitz (@Schuldensuehner) July 29, 2015

The immediate reaction is that today’s Fed statement makes a September rate hike a little less likely.

But there’s not much in it, given there’s no radical change between the new statement and the last one.

Basically, Janet Yellen and colleagues aren’t quite ready to pull the lever to raise borrowing costs - and want to see more data from the US jobs market over the summer.

USD weaker as #Fed headlines not dovish, just less hawkish in the immediate term. Swing-o-meter from Sept to Dec hike just moved a tad right

— Joshua Raymond (@Josh_RaymondUK) July 29, 2015

At the margin, Fed statement is dovish, because June dot plot points to 2 hikes, but this does not lay clear groundwork for Sept move.

— Carl Riccadonna (@Riccanomix) July 29, 2015

The markets aren’t quite sure what to make of the Fed statement.

The dollar plunged when the first newsflashes came up, but has now bounced back.

that was a heckuva knee-jerk move in the dollar/euro exchange rate pic.twitter.com/6DwWsOVASb

— Alexandra Scaggs (@alexandrascaggs) July 29, 2015

Changes to the Fed statement

There are two significant changes in today’s statement from the Federal Reserve.

1) It has added a reference to the labor market ‘continuing to improve’, and slightly hardened its language about the underutilisation of resources diminishing (ie, fewer people working less than they want)

2) It has removed a reference to energy prices stabilising:

CNBC has helpfully highlighted the statement:

Here's what changed in the new Fed statement: http://t.co/PI5ytJe3BE pic.twitter.com/pP1QU1Nz0j

— CNBC (@CNBC) July 29, 2015

Today’s decision was unanimous, the Fed adds.

BREAKING: FED LEAVES IN THE WORD "NEARLY" http://t.co/7FzmnLlJCO

— Joseph Weisenthal (@TheStalwart) July 29, 2015

Federal Reserve leaves rates unchanged

Here we go!

The Federal Reserve has resisted raising interest rates from their current record low, of 0% to 0.25%.

The US central bank says that it will raise interest rates when it has seen “some further improvement” in the labour market (or the labor market, I guess). Is that a hint of a rise in September?

The Fed also repeats that the risks to the economy and the jobs market are “nearly balanced”, showing that it hasn’t - yet - been pushed into a rate hike.

OK, nearly time for the Federal Reserve’s interest rate decision....

Nervous

— Joseph Weisenthal (@TheStalwart) July 29, 2015

Come on Janet, I have gin to drink

— World First (@World_First) July 29, 2015

Afternoon summary: Greek debt relief back in the spotlight

Time for a recap:

The issue of Greece’s unsustainable debt burden has moved back up the agenda, as top officials from the country’s creditors prepare to begin talks on a third bailout.

Lagarde also wants to see “sensible fiscal targets” (which must take account of the recent economic turmoil), “structural measures” to reform the Greek economy, and enough funding to cover Athens’ medium-term financing needs.

Lagarde at online press conference in Washington today pic.twitter.com/eH2L6RPmEU

— IMF (@IMFNews) July 29, 2015

Greek prime minister Alexis Tsipras has also put debt relief front-and-centre, telling a radio interview that Greece should get help in November.

Tsipras also warned that Greece’s eurozone membership is still up in the air until the third bailout is agreed.

And he threw down the gauntlet to rebels in his party, saying they must either support the government or resign. Ratcheting up the pressure, Tsipras also suggested that he could be forced to call early elections if he doesn’t have Syriza’s support.

Tsipras warned:

“I’m the last person who would want elections....If I don’t have a parliamentary majority, though, we will be forced to head to a snap vote.”

Tsipras Challenges Party Rebels With Threat of Snap Greek Ballot http://t.co/JZIPpaAKO9 pic.twitter.com/mPN90Yciwc

— Bloomberg Markets (@markets) July 29, 2015

Speculation is growing that former Greek finance minister Yanis Varoufakis could ultimately face charges over his plan to develop a parallel payment system. The country’s top prosecutor has asked parliament to examine complaints over the issue.

Greece is preparing for tough negotiations with its creditors over a third bailout - with IMF negotiator Delia Velculescu arriving tomorrow.

While European Commissioner Pierre Moscovici insists that Grexit is off the table, the prime minister of Bavaria is less sure - he fears ‘utter chaos’ if Greece fails to reform and leaves the eurozone.

And the financial markets remain calm, as investors await the Federal Reserve’s decision on interest rates at 7pm BST (or 2pm East Coast time)

Asked about the prospect of a US rate rise, Christine Lagarde predicts “a variation of monetary policy in the not-too-distant future”.

And she ends her first online press conference by telling reporters that she hopes they’re comfy, with their feet on the desk and a cup of coffee (or watching the Ashes, perhaps....)

Takeaways from Lagarde's online presser: She's not sweating China's stock rout too much. More prodding of Europe to give Greece debt relief

— Andrew Mayeda (@amayeda) July 29, 2015

Four legs good.....

Fiscal policies, structural reforms, financing & debt restructuring are four key legs for a Greek solution - Lagarde pic.twitter.com/eVYeShcwLn

— IMF (@IMFNews) July 29, 2015

Lagarde: Greece needs 'significant' debt relief

Christine Lagarde has warned that Greece needs “significant” debt relief - laying down the conditions for the IMF to take part in the third bailout.

She told today’s virtual press conference that any rescue plan for Greece will be unworkable without some form of debt relief.

“For any programme to fly, a significant debt restructuring should take place.”

Lagarde added that a rescue plan would have to involve “four legs”:

- sensible fiscal targets, that are delivered

- structural measures to open up the Greek economy

- sufficient financing to make the programme workable

- debt restructuring

Lagarde added that the IMF would be looking at what the Greek government does, not what it says, promising to disregard what she called political “noise”, and focus on “deeds, not creeds”.

IMF's @Lagarde on Greece: "for any programme to fly, a significant debt restructuring should take place".

— Heather Stewart (@heatherstewart3) July 29, 2015

Lagarde on Greece: what matters are actions. “It’s deeds, not creeds.”

— IMF (@IMFNews) July 29, 2015

Updated

IMF Lagarde notes trepidations in Greece but notes Eurozone recovery finally taking shape Admits questions on cohesion will shape its future

— Katerina Sokou (@KaterinaSokou) July 29, 2015

Lagarde: The global recovery is tepid and fragile

IMF chief Christine Lagarde is holding her first ever virtual press conference with reporters.

Top spokesman Gerry Rice is putting the questions (don’t go easy on the boss, Gerry!)

Online Press Conference with IMF Managing Director Christine @Lagarde pic.twitter.com/hvBM4diQnY

— Thanasis Koukakis (@nasoskook) July 29, 2015

The event started with Lagarde joking that she was trying to imagine us all behind the little computer screen *waves*.

And then to business, with a warning that the global recovery is “a little bit too tepid” and fragile for her liking.

On the eurozone, Lagarde says it appears to be ‘turning the corner’.

And on China, she’s believes that the current stock market volatility isn’t a reason to panic.

IMF's @Lagarde in online chat: "We believe that the Chinese economy is resilient"; can withstand "significant variations" in stock markets.

— Heather Stewart (@heatherstewart3) July 29, 2015

Updated

The ECB has maintained its current support for the Greek banking sector today, at almost €91bn.

Why no increase? Apparently the Bank of Greece didn’t ask for one - suggesting that the outflow of deposits has stabilised (and with capital controls in force, that’s understandable).

Greek MP: Varoufakis could face charges over Plan B

In a drama fast unraveling in Athens the scene has been set for possible criminal charges to be brought against former finance minister Yanis Varoufakis following revelations of his secret plan to establish an alternative currency in the event of Greece’s euro ejection.

Helena Smith reports:

Amid cries of high treason, the country’s most senior state prosecutor, Efterpi Koutzamani, ordered the Greek parliament to examine an array of complaints brought by private citizens against Varoufakis.

The Supreme Court prosecutor, who played a leading role in putting the far right Golden Dawn on trial, also asked a magistrate to investigate whether criminal charges should be brought against non-political figures, following Varoufakis’s admission of a plan to hack Greece’s tax service to set up the parallel payment system.

“I would not want to be in Varoufakis’ shoes,” the conservative MP and shadow finance minister Anna Asimakopoulou told the Guardian.

“I think that it is highly likely he will end up in a courtroom.”

As a sitting MP, the maverick economist enjoys immunity from prosecution. But the prosecutor’s move now opens the way to criminal charges being bought against him if parliament determines there are grounds to establish a special congressional committee to probe the allegations.

Judicial sources said the charges could range from dereliction of duty to overseeing the formation of a criminal gang – the central accusation brought against Golden Dawn whose leaders are currently on trial.

The five-member team tasked with organizing the alternative currency – described by the former finance minister as a form of parallel liquidity - could also face accusations of participating in a criminal organization. The working group was headed by the well-known US economist, James K Galbraith, who was seconded to help Varoufakis until the politician’s resignation earlier this month.

In five separate suits brought against him, the academic-turned-MP has also been accused him of high treason although legal experts said the charge would be very hard to prove. His perceived mishandling of highly fraught negotiations with the EU and International Monetary Fund – the bodies keeping debt-stricken Greece afloat – has been blamed for the tough measures imposed on Athens in exchange for a third bailout of emergency loans from international creditors.

By failing to agree on a cash-for-reform programme earlier, the crisis-plagued country was forced to sign up to a deal outlining €12bn of savings rather than €8bn as originally thought. The closure of banks and imposition of capital controls – implemented under Varoufakis’ stewardship – are said to have wrought at least €3bn worth of damage on the economy with prolonged recession now predicted for a country that has experienced record levels of unemployment and poverty since the eruption of the debt crisis five years ago.

In recent days even senior members of prime minister Alexis Tsipras’ radical left Syriza party have joined in the criticism, attributing the tough stance of lenders to the outspoken politician’s handling of the talks.

Syriza MP and vice president of the 300-seat House Alexis Mitropoulos told Mega TV that:

“With his loquaciousness, with his naivety, with his zeal to prove his ideas more than anything else, it seems that he hurt the Greek issue.”

Varoufakis, who has retreated to his island home, has openly admitted resorting to “unconventional methods” to come up with a contingency plan that would have paved the way to the re-embrace of the drachma if Greece was forced out of the euro zone.

But he also argued yesterday that it would have been “remiss” of him if his ministry had not also devised a Plan B.

Something is rotten with the eurozone’s hideous restrictions on sovereignty (Plus the Plan against liquidity crunch) http://t.co/uERxy9qOIp

— Yanis Varoufakis (@yanisvaroufakis) July 28, 2015

On Tuesday the European Union waded in slamming Varoufakis for suggesting that he was forced to hack his ministry’s computer systems because the nation’s “troika” of creditors had exclusive control of the country’s tax agency. A commission spokeswoman described the claims as “false and unfounded.”

But the self-styled “erratic Marxist” also has friends in high places with many saying he has been turned into a scapegoat.

Writing in the New York Times this week, the Nobel prize winning US economics professor Paul Krugman argued that it would have been highly irresponsible of Varoufakis had he not had a plan.

“The issue now becomes whether Tsipras was right to decide not to invoke this plan in the face of what amounted to extortion from the creditors,” he wrote.

“I think he called it wrong, but God knows it was an awesome responsibility — and we may never know who was right.”

Varoufakis responded with his usual aplomb today tweeting:

Have you not heard Paul? Drawing up contingency plans vs the troika unapproved by the troika = High Treason https://t.co/6tPWL8ojja

— Yanis Varoufakis (@yanisvaroufakis) July 29, 2015

Updated

Tsipras has also warned that Greece could face fresh snap elections, if he cannot maintain the support of his party:

Tsipras: I am the last to want elections, if we have parliamentary majority. If not, forced to go to elections

— Chrisostomos (@LoukasChris) July 29, 2015

Tsipras appears to be challenging the 30-or so rebellious government MPs to either shuffle back into line, or shuffle off:

#Tsipras on Syriza defectors:You can't say you disagree with govt decisions but back the government. That's taking surrealism to a new level

— NikiKitsantonis (@NikiKitsantonis) July 29, 2015

That sets the tone for a meeting of Syriza’s central committee on Thursday. That committee could decide to call a new party congress – either in September or straight away.

Let’s get back to Alexis Tsipras’s radio interview, where the Greek PM has warned rebels in his Syriza party to support him or clear off:

Tsipras: collective decisions must be followed by all MPs or hand back their seat

— Chrisostomos (@LoukasChris) July 29, 2015

#Greece PM Tsipras says there cannot be à la carte support to the government.

— Yannis Koutsomitis (@YanniKouts) July 29, 2015

Some analysts suspect that Syriza will soon split, with the rebellious Left Platform breaking away from the rest of the party. That would allow Tsipras to take a more centrist approach.

However, he’s also just ruled out turning Syriza into a social democratic party.

Bank of England fears impact of Fed rate hike

Breaking away from Greece, and the Bank of England’s deputy governor for financial stability has revealed his worries about the consequences of a US interest rate rise.

Speaking to the Guardian, Sir Jon Cunliffe warned that markets are still ‘quite fragile’. So we can’t assume that a Fed rate hike won’t cause problems.

As Cunliffe put it:

“If and when US interest rates go up ... there are concerns about how the market will adjust. This must be the most advertised, well signalled change in monetary policy in the history of man.

Nonetheless you don’t know. These are different sorts of markets to the ones we had before.”

Cunliffe also warned that new rules to regulate banks should not be watered down, despite pressure from the industry....

Tsipras: Grexit is still a risk

Alexis Tsipras has warned radio listeners that Greece could still be forced out of the eurozone.

The risk of Grexit won’t be removed until a third bailout deal, and debt relief, is secured, he says.

Tsipras: capital controls damage reversible. Grexit still on the table until a debt forgiveness comes

— Chrisostomos (@LoukasChris) July 29, 2015

As reported earlier, Bavaria’s prime minister has warned that Grexit is still a risk.

Horst Seehofer said:

On top of that there would be utter chaos. If Greece were not prepared to reform, a path like that would have to be accepted but one shouldn’t strive for it oneself or organise it.”

What defeat?!

Tsipras: I have no regrets over the past few months. Greece is front page news with positive light.totally worth it

— Chrisostomos (@LoukasChris) July 29, 2015

In defeat, unbeatable?

Tsipras: deal on greece was Pyrrhic victory for EU partners

— Chrisostomos (@LoukasChris) July 29, 2015

#Tsipras: it was a Pyrrhic victory for lenders, a big moral victory for #Greece

— Kathimerini English (@ekathimerini) July 29, 2015

#Tsipras on July 12 e/z summit:If I had done what my heart told me, + left talks, wd have been chaos w Greek banks, global markets, savings.

— NikiKitsantonis (@NikiKitsantonis) July 29, 2015

Updated

Tsipras has returned to defending the deal he signed up to at the all-night negotiations in Brussels:

Tsipras: if I left the 17hs negotiations, chaos with Greek banks and world markets, peoples' savings lost

— Chrisostomos (@LoukasChris) July 29, 2015

But what about your referendum, Alexis?

A. Tsipras: referendum was not for a Grexit but for strengthening negotiating position

— Chrisostomos (@LoukasChris) July 29, 2015

Greek PM: debt relief in November

Another nugget from Alexis Tsipras’s interview with Sto Konnino 105,5 - he says Greece’s creditors will tackle its debt sustainability in November:

RT @ThePressProject: #Tsipras on radio: We will have debt relief in November #Greece #GreekCrisis

— Janine Louloudi (@janinel83) July 29, 2015

*TSIPRAS: GREECE CAN'T RETURN TO MARKETS WITH CURRENT DEBT LEVEL

— Nour E. Al-Hammoury (@NourHammoury) July 29, 2015

For that to happen, Greece would need to agree a third bailout, and then show its lenders that it is sticking to the plan.

Updated

Alexis Tsipras is denying that Greece could have breezed out of its bailouts if Syriza hadn’t won January’s election:

A. Tsipras. Samaras, Venizelos on exit from memoranda were fairy tales

— Chrisostomos (@LoukasChris) July 29, 2015

Chris Loukas of radio station Sto Kokkino 105,5 is tweeting the key points from their interview with the PM:

Tsipras. Our mandate was to stop the people's bleeding. I never said memoranda can be torn with just one law

— Chrisostomos (@LoukasChris) July 29, 2015

Tsipras: we have been implementing our policies for the past 6 months whilst negotiating in asphyxiation conditions

— Chrisostomos (@LoukasChris) July 29, 2015

A. Tsipras: (on referendum) I had no choice but to decide on a referendum. U have to see what kind of deal we were offered.

— Chrisostomos (@LoukasChris) July 29, 2015

A. Tsipras: France, Italy other, different views than Germany

— Chrisostomos (@LoukasChris) July 29, 2015

Updated

Kathimerini are also translating Alexis Tsipras’s radio interview (thanks guys!).

The Greek PM is (once again) defending the bailout deal he agreed to this month:

PM #Tsipras interview with Sto Kokkino FM: For the first time, there was a tough negotiation. Conflicting strategies on the table #Greece

— Kathimerini English (@ekathimerini) July 29, 2015

#Tsipras: we never said negotiations would be a walk in the park #Greece

— Kathimerini English (@ekathimerini) July 29, 2015

#Tsipras: We did not say, before the elections, that bailout agreements would be annulled with a single piece of legislation #Greece

— Kathimerini English (@ekathimerini) July 29, 2015

Tsipras: Last six months have seen 'great conflict'

Here are some early highlights from Alexis Tsipras’s radio interview, via Enikos.

The institutions were not independent or neutral.

We should be proud of the battle we have given.

The last 6 months has been a period of great conflict.

Updated

Greek PM Alexis Tsipras is giving a radio interview now. It’s live here (in Greek, obviously)

My interview on @stokokkino1055 has begun. Listen to it live here: http://t.co/5uX09Q7D53 #Greece pic.twitter.com/MTolC63vz5

— Alexis Tsipras (@tsipras_eu) July 29, 2015

Britain’s City watchdog has fired a warning shot at the banking sector, warning that some firms haven’t done enough to prevent financial benchmarks being manipulated.

Following a series of scandals, the FCA is pushing banks to ensure that they are properly overseeing their staff. However:

....the application of the lessons learned from the LIBOR, Forex and Gold cases to other benchmarks had been uneven across the industry and often lacked the urgency required given the severity of recent failings.

Updated

IMF top negotiator won't arrive in Athens until Thursday

After getting off to a bumpy start yesterday, negotiations with mission chiefs representing Greece’s creditor institutions will begin today minus one, we have just been told.

From Athens our correspondent Helena Smith reports

The hotly-anticipated arrival of all four mission chiefs representing the EU, ESM, ECB and IMF will have to wait until tomorrow, the Guardian has just been told.

After much confusion, a finance ministry official has confirmed that the Rumanian economist Delia Velculescu, who will be heading the IMF team to Greece, will not be flying in until tomorrow.

The well-placed source told me

“There’s no particular reason for the delay.

But I can confirm she won’t be coming in today, she’ll be arriving tomorrow.”

The official rejected suggestions that the delay was directly linked to difficulties with the IMF, which of all the creditor bodies has taken the toughest stand with Greece.

“There’s absolutely no mystery to it,” said the official adding that it remained unclear how long the inspection tour would last.

Velculescu comes with a reputation. The Rumanian economist who will be reporting to former mission chief Poul Thomsen (now head of the IMF’s European department) was previously appointed mission chief for Cyprus where her demanding stance earned her the nickname Dracula.

US-trained, she will be tough with Athens applying prior actions in the coming weeks.

@deliavelculescu new @IMFNews delegation chief to #Greece in #Greecrisis - a cool "Draculescu" http://t.co/2qzrapJlAZ pic.twitter.com/Xk5xuOJysc

— Proto Thema English (@eprotothema) July 27, 2015

Already the talks are mired in dispute amid speculation that the Greek government will have to pass more restrictive measures through parliament to qualify for bailout funds.

Rumour has been rife that creditors will demand further prior actions not least pension cuts and tax hikes on profits made by farmers – neuralgic issues bound to trigger further anger in Syriza.

In a statement the Greek finance minister rejected any suggestion that the government might be forced to impose further prior actions.

“As far as reports of prior actions are concerned it should be noted that neither in the agreement of the European summit on the 12 of July nor in the two letters that the Finance Minister Euclid Tsakalotos sent to the ESM was there the slightest hint of a third package of prior actions.”

The latest talks, the ministry said, would focus on changes to the Greek pension system labour reform, fiscal policy and market regulation.

Updated

Here’s a few gems from the deluge of corporate news this morning:

Strong spring selling boosts Taylor Wimpey sales http://t.co/N2PVqyRoWX

— fastFT (@fastFT) July 29, 2015

Antofagasta lowers full year copper guidance http://t.co/a9yzZ72aFy

— fastFT (@fastFT) July 29, 2015

And if you want more, check out FastFT’s full summary of this morning’s results:

UK stocks: the morning’s movers and shakers

Greek stock market investors need to stay patient.

The Athens exchange won’t open today, because the government hasn’t issued a ministerial decree to allow trading to resume.

It could open on Thursday, more than a month after capital controls were introduced.

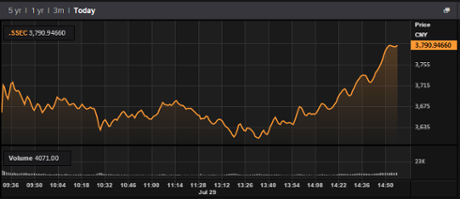

You need nerves of steel to play the Chinese stock market right now.

The Shanghai composite index ended the day up 3.5%, after a late surge of buying drove many shares up 10% - the maximum allowed in one day.

Earlier, the market had been heading for another fall, before a rush of optimism swept brokerages. Beijing’s latest steps to stabilise the markets by buying shares and injecting liquidity may be paying off.

That still leaves traders nursing big losses after Monday’s 8.5% plunge”

Believe it or not: #China regulators manages to get stocks into the green. Shanghai Composite ends up 3.5%. pic.twitter.com/UBDScuPKKl

— Holger Zschaepitz (@Schuldensuehner) July 29, 2015

Updated

For all the talk of clean-ups and fresh starts, Britain’s banks are still paying for the mistakes of the past.

This morning, Barclays has set aside £1.8bn to cover the cost of compensating customers caught up in a string of scandals. It took the shine off a 25% jump in profits.

Our City editor Jill Treanor reports:

The figure was revealed as John McFarlane, the chairman who is standing in as chief executive following the ousting of Antony Jenkins earlier this month, pledged to accelerate the disposal of risky businesses, cut costs at the scandal-hit bank and change the dividend policy.

Included in the provision is a further £600m for the payment protection insurance mis-selling scandal and £250m to compensate customers with packaged bank accounts that had other products, such as insurance, attached to them.

Shareholders seem happy, though - Barclays shares are up 2.6% in early trading.

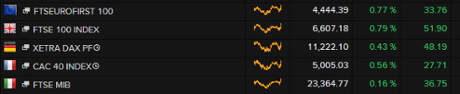

There’s not much sign of Greek angst in the European stock markets this morning.

Shares are higher across the board, helped by the news that China’s stock market surged by over 3% in late trading:

Investors are poised to hear the Federal Reserve’s decision on interest rates tonight, and to digest the accompanying statement.

FXTM Chief Market Analyst Jameel Ahmad explains:

What everyone wants to know from tonight’s FOMC announcement is clear guidance on the likely time frame to expect an US interest rate increase.

We have repeatedly been told that US interest rates will rise at some point later this year, but the timing on when this will occur still remains largely unclear.

Bavarian PM: Grexit would be 'utter chaos'

The prime minister of Bavaria, one of Angela Merkel’s allies, has warned that there would be ‘utter chaos’ if Greece were to leave the eurozone.

However, it might also be inevitable, if Athens can’t implement the reforms that creditor demand, Horst Seehofer added.

Seehofer made the comments in an interview with German newspaper Die Welt, published in today’s edition.

Reuters has the key quotes:

“No one can predict the consequences of a Grexit other than that a lot of Greece’s debts would have to be written off and at the same time monetary help would be necessary.”

“On top of that there would be utter chaos. If Greece were not prepared to reform, a path like that would have to be accepted but one shouldn’t strive for it oneself or organise it.”

Moscovici optimistic on bailout talks

Negotiations over the third Greek bailout deal are going well, European commissioner Pierre Moscovici told French radio listeners this morning.

Interviewed on Europe 1 radio, Moscovici said talks were taking place in “good conditions”, declaring that:

“Grexit is behind us.”

The priority now, he added, is to create closer integration in the eurozone and drive through economic reforms to lower unemployment.

Le #Grexit est derrière nous. Nous avons besoin d'une #zoneeuro plus intégrée. Il faut aller de l'avant @EU_Commission #Grèce

— Pierre Moscovici (@pierremoscovici) July 29, 2015

Poursuivre les efforts pour réduire le chômage, nécessité de réformes pour la #croissance et l'#emploi en #Europe @EU_Commission #E1Matin

— Pierre Moscovici (@pierremoscovici) July 29, 2015

Updated

Introduction: Greek negotiators 'predict deep recession'

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

Coming up.....

Technical talks between the Greek government and its creditors will continue today, as Athens tries to secure a third bailout by mid-August.

Top officials from the European Commission, European Central Bank and European Stability Mechanism should all in the capital by the end of the day, ready to take over negotiations by Friday. Delia Velculescu, the IMF’s lead negotiator, arrives tomorrow.

Technical teams have been assessing the state of the Greek economy so they can draw up plausible new fiscal targets.

Greek media report that they now expect a deep recession in 2015, given the severe damage caused by a month of capital controls:

#Greece and the Institutions agree 2015 GDP forecast at -3.3%. ~@in_gr

— Yannis Koutsomitis (@YanniKouts) July 29, 2015

In October 2014 there was consensus that #Greece 2015 GDP would land at minimum +2%. Now forecast lies at -3.3%. Syriza mission accomplished

— Yannis Koutsomitis (@YanniKouts) July 29, 2015

Also coming up....

Tonight, the Federal Reserve will announce its latest decision on interest rates. They’re very likely to hold them at 0.25% - but for how much longer? Speculation of a September rate hike have already helped to drive emerging market currencies down to a 15-year low.

And there’s also a flurry of corporate news, as companies clear the decks before the August break - including Barclays, Sky, Antofagasta and Foxtons.