PPS: James Galbraith, the US economist who advised the new Greek government, has written a stirring defense of last Friday’s deal.

It’s online here:

PS..... Greek finance minister Yanis Varoufakis has just told CNN that Athens can’t be blamed for the delay:

#Varoufakis tells live on #CNN that GR delivered reform letter today & it was Eurozone finance ministers who asked delay. #Greece #Eurogroup

— Siegfried Muresan (@SMuresan) February 23, 2015

I’m going to wrap up now, as we don’t get this list until Tuesday morning. I’ll pop back if there are any major developments.

If you’re looking for something else to read on Greece, check out Paul Mason’s piece today on how a parallel currency could help Greece recover:

Can a Bitcoin-style virtual currency solve the Greek financial crisis?

And for balance, here’s a response by City asset manager Toby Nangle (always worth listening to). It’s all about the nature of money....

A quick Ello on @paulmasonnews @guardian comments today ... https://t.co/COiZboTdUT

— Toby Nangle (@toby_n) February 23, 2015

Greek journalist tweets summary of draft proposals

Now this is interesting... Greek TV journalist Sofia Dimtsa has the inside line on the Greek reform programme, and tweeted a photo of her notes [NOTE: THIS IS NOT THE ACTUAL LIST]

I'll say it before anyone else does: It's all Greek to me. A photo of the list of #Greek pledges @SofiaDimtsa pic.twitter.com/G20C9a0Mms

— Luke Baker (@LukeReuters) February 23, 2015

Yannis Koutsomitis has rapidly rattled out a translation. And it appears to show the new government trying to tread the line between its creditors demands, and the anti-austerity “Thessaloniki proposals” presented by Alexis Tsipras last autumn.

Yannis explains:

- 6 pages - 12 fields of reforms - no actual figures

- Incentives for tax arrears up 100 installments - provisions to avoid moral hazard

- Plan for NPLs (non-performing loans) - Banks capital protection - social justice - protection of primary residences from foreclosures

- Labor law: Reforms according to EU ‘best practices’

- Pension funds: Measures for viability of pension funds without strict timetables - no commitments for no deficits

- Privatizations: Respect of done deals - Protection of national key interests

- Enhancing competition: Adaptation of OECD proposals

- Reforms in state institutions - no rehires of layd-offs

- Measures for the poor according to the Thessaloniki proposals

- Reform tax collection authority

Here is a draft translation of the major bullet points of the Greek proposal as reported by @SofiaDimtsa: · 6 pa… http://t.co/sNOwHvLz3g

— Yannis Koutsomitis (@YanniKouts) February 23, 2015

This → RT @SofiaDimtsa: @YanniKouts Just to make It clear to your followers. My notes on what is on the draft.

— Yannis Koutsomitis (@YanniKouts) February 23, 2015

Updated

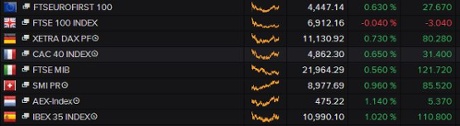

Eurozone stock markets closed at their highest level in seven years tonight, before the first rumours of a delay to the Greek reforms plan.

The main indices all finished higher (unlike the Footsie, of course), as investors reacted to Friday night’s bailout deal.

Perhaps Greece didn’t want a repeat of last week’s scenes – when Germany’s finance minister rejected its proposal before it has even been discussed!

James Wilkins of Thessaloniki, a regular reader of this blog, suggests:

The Greek government probably want to give people a chance to discuss their proposals before Wolfgang Schäuble can say “NEIN!” at two minutes past eleven tomorrow.

The reform plan is apparently longer, as well as later:

Greek media now report reform list will be 6 pages long (not 3) &will be sent Tues (not Mon) morning #Greece

— Loukia Gyftopoulou (@loukia_g) February 23, 2015

Simon Nixon of the Wall Street Journal isn’t impressed by the delay:

Worrying Greece to miss deadline for its list of reforms. More evidence it lacks serious policies. Also reduces time for Troika to reject?

— Simon Nixon (@Simon_Nixon) February 23, 2015

To add to the confusion, Greece has been discussing its reform programme with Brussels officials today:

Baffled by reports that Greek proposal will not be presented till Tuesday. Athens sent it to Declan Costello at EC mid-day Monday

— A Evans-Pritchard (@AmbroseEP) February 23, 2015

Alexis Tsipras’s government will hold a cabinet meeting tomorrow....

Official: #Greece to send reforms to EZ FinMin in morning, greek cabinet mtg at 11am local. Eurogroup teleconference in afternoon

— Nathalie (@savaricas) February 23, 2015

Updated

Greek government spokesman: Reforms will be sent tomorrow

Sounds like it’s official. A Greek government spokesman has told Reuters that the list of proposed reforms will be sent to Brussels tomorrow morning, not tonight.

That chimes with the rumours we heard an hour ago (details).

Still no firm details on the plan, but apparently it will include measures to fight tax evasion and corruption, and to reform the public sector....

- GREECE WILL SUBMIT LIST OF REFORMS TO EUROGROUP ON TUESDAY MORNING - GREEK GOVT OFFICIAL

- LIST WILL INCLUDE REFORMS TO FIGHT TAX EVASION, CORRUPTION - GREEK GOVT OFFICIAL

- LIST WILL INCLUDE MEASURES TO REFORM PUBLIC SECTOR, CUT BUREAUCRACY - GREEK GOVT OFFICIAL

- LIST WILL INCLUDE REFORMS TO REGULATE TAX ARREARS AND BAD LOANS - GREEK GOVT OFFICIAL

Although government insiders insisted earlier that there’s ‘no obstacle’, this is not a great development.

Gah, deadlines... RT @FGoria: ***Greece will submit list of reforms to Eurogroup on Tuesday morning - Greek government official - RTRS

— Ed Conway (@EdConwaySky) February 23, 2015

Oh dear...

— Yannis Koutsomitis (@YanniKouts) February 23, 2015

Lagarde: Grexit is off the cards

Christine Lagarde, head of the IMF, has insisted that Greece will not quit the eurozone.

In an interview with the Huffington Post this afternoon, Lagarde says:

This is not on the cards, and it is not being discussed.

Last week was a triggering point where there was a collective determination to listen, to build trust, and to do the best to stay together.

Lagarde also urged Greece’s new government to implement reforms, to tackle “vested interests, protected professions, rigidity in some markets”. Those measure can “unleash productivity” and lead to sustainable growth, she argued..

“I hope that the structural reforms that are so needed in the country can be implemented. There’s been a lot of talk about it, but now it’s time to get on with the work.”

LAGARDE SAYS SHE HOPES GREEK TALKS RECOGNIZE PLIGHT OF GREEKS

— Jonathan Ferro (@FerroTV) February 23, 2015

LAGARDE: GREECE NEEDS PRO-GROWTH, FISCALLY SENSIBLE POLICIES

— Jonathan Ferro (@FerroTV) February 23, 2015

Updated

Back in Athens, Helena Smith has been speaking to government sources, who tell her that the list of economic reforms may even be sent on Tuesday morning rather than by the deadline of midnight tonight.

One says:

“The good news is that no obstacle has emerged in discussions (with creditors today) but there is a possibility the list will be sent tomorrow now that the teleconference (between the Greek finance minister and his euro group counterparts) is assured.”

That’s just a possibility, of course. I’m sure the euro group would rather see these reforms tonight, so they’ve got time to digest them before that call.

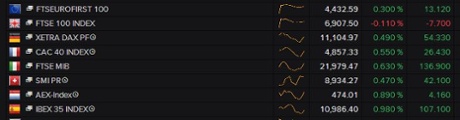

Predictions that Britain’s blue-chip index of leading shares would hit a record high today were dashed, by disappointing results from HSBC.

The FTSE 100 just closed for the day at 6912, a drop of 3 points or 0.04%, having scooted to a 15-year high in early trading.

HSBC did the damage, falling 4.6%. Standard Chartered suffered a similar decline.

David Madden, market analyst at IG, explains:

British banks that weathered the credit crisis relatively well have lost the most ground today. HSBC kicked off reporting season for the UK banks and the poor results triggered a wave of selling of Standard Chartered shares as it also has a big dependency on Asia.

*DIJSSELBLOEM: GREEK REFORMS LETTER SHOULD BE `STRONG ENOUGH'

— lemasabachthani (@lemasabachthani) February 23, 2015

DIJSSELBLOEM SAYS HE IS `OPTIMISTIC' ON GREEK REFORMS LETTER

— Jonathan Ferro (@FerroTV) February 23, 2015

Some of us are merely impatient. Or maybe the eurogroup chief is optimistic that it’ll turn up eventually....

Updated

It wld be much better for the Greek banking system & stock mrkt if tomorrow's #Eurogroup teleconf is held is the early am hrs. But it won't.

— Yannis Koutsomitis (@YanniKouts) February 23, 2015

Mood music on #Greece increasingly positive today, after shaky Sun. Sounds like #eurogroup teleconference tomorrow rather than meeting.

— Peter Spiegel (@SpiegelPeter) February 23, 2015

Teleconference confirmed for tomorrow

Some news in from Greece, reports Athens correspondent Helena Smith.

The Greek finance ministry has announced in a two line statement that “tomorrow, Tuesday, a teleconference will take place between the finance minister and euro group.”

They didn’t give a time, though. And there’s no news about that list of proposed reforms....

Updated

The clock is still ticking towards Greece’s midnight deadline to get its reforms plan to its creditors....

cinderella has just six hours to get its reform proposals to the princes in brussels before it turns into a pumpkin. #greece

— Diane Shugart (@dianalizia) February 23, 2015

Updated

Eurogroup president Jeroen Dijsselbloem, who let the negotiations with Greece, is due before the European Parliament’s Economic Affairs Committee on Tuesday morning.

The state of play in Eurogroup talks with Greece is set to dominate the Economic and Monetary Affairs Committee’s regular debate on euro zone economic indicators with Eurogroup President Jeroen Dijsselbloem on Tuesday morning.

#grexit before eurogroup finmins teleconf tues on greek package, @J_Dijsselbloem appears before @Europarl_EN committee #lookingforclues

— Ian Traynor (@traynorbrussels) February 23, 2015

Updated

The easing of the Greek crisis (for the moment at least) pushed European stock markets hit seven year highs today.

Analysts at private bank Coutts says investors are putting geopolitical fears behind them

European equities have extended their year-to-date outperformance, seeming to put geopolitical fears behind them following agreement on a ceasefire in Ukraine earlier this month and a deal this past week to avert a renewed debt crisis in Greece. While neither problem has been fully resolved, we have remained overweight in European equities throughout these crises, in the belief that they wouldn’t derail economic recovery in the region.

Last week’s news reinforced our sanguine view as Greece and its eurozone counterparts hashed out a last minute deal to extend its €172bn bailout programme, just days before the programme was set to run out on 28 February. While it leaves some key issues unresolved, the breakthrough removes the risk of Greece running out of money next month, provides some reassurance for financial markets and should help stem the flow of withdrawals of deposits from Greek banks

Here’s our news story on the state of play, from Helena and Europe editor Ian Traynor:

Greece drafts menu of reforms to appease eurozone

More news on when we should expect the proposals to arrive in Brussels, from Helena Smith in Athens:

One well-briefed source has just told me that the government has until midnight to deliver the reform package “and may well use every hour.”

“It will be put over this evening although when exactly that will be we just don’t know. Right now they are drawing up and crossing out [proposals],” he said.

Reports that the list would run to five pages could not be confirmed. “It is changing all the time,” he said.

Updated

Lunchtime summary

A quick recap.

Greece’s government is putting the finishing touches to its proposed economic reforms, which must be submitted to Brussels by the end of the day.

Insiders say the plan will be ‘broad brush’, but may include a general pledge to stick with state asset sales, along with a clampdown on tax evasion to bring in billions of euros.

If it is accepted by the eurozone, it will pave the way for Greece’s bailout to be extended by four months.

The risk of Greece exiting the euro has now fallen, to 25%, according to Berenberg Bank.

But political tensions in Athens are rising. Several left-wingers have gone public with their concerns that Greece has agreed to stick with most of its former bailout.

Difficult hours for Greek govt, having to draw up reforms to satisfy EU/IMF and growing dissent at home over failure to ease austerity.

— Gavin Hewitt (@BBCGavinHewitt) February 23, 2015

European stock markets are mostly higher today, on relief that the immediate crisis has eased a little. Earlier, the Japanese Nikkei hit a 15-year high.

However, the FTSE 100 has dropped back after hitting its highest level since 1999. It has been dragged down by HSBC, which reported a 17% drop in profits this morning.

Greek left-wingers unhappy about bailout deal

Dissent within Syriza over the bailout agreement is growing, our correspondent Helena Smith reports.

One after the other expressions of disquiet are coming in. The celebrated composer Mikis Thedorakis waded in earlier today appealing to the government, even at this late hour, to resist the pressure being exerted by Greece’s euro zone creditors.

“There is hope. And that is for the leaders of Syriza to find the strength to say, even now, OXI [NO] to Schauble’s NEIN,” the award-winning composer said in a statement, invoking the time Greeks rejected Mussolini’s request to align with the Axis powers and in so doing entered the second world war.

Now Costas Lapavitsas, the Syriza MP and noted economics professor at London University’s School of Oriental and African Studies, has also made his discomfort known.

Taking to the blogosphere today he writes:

“The Euro group agreement has not been completed partly because we still don’t know what reforms the government will propose today and what will be accepted. But those of us who have been elected based on Syriza’s program, and consider the announcements made in Thessaloniki [where Tsipras outlined his economic policies] as a commitment that we have undertaken towards the Greek people, have deep worries. It is our duty to register them.”

Lapavitsas, who belongs to Syriza’s hard-left faction, follows Greece’s veteran leftist Manolis Glezos who called for action yesterday.

Helena says she is hearing rumblings from the far left that they are not being consulted and are essentially being ridden rough shod over.

“This is an absolutely critical time for society, the nation and naturally the left,“ Lapavitsas wrote.

“The democratic legitimisaton of the government is founded in the program of Syriza. The least that is called for is to have an open discussion in the party apparatus and [Syriza’s] parliamentary group.”

And last night, Syriza MEP Sophia Sakorafa tweeted her concerns:

The people gave a mandate to cancel the memorandum. We don’t have any political legitimacy to act otherwise.

Ο λαός έδωσε εντολή για ακύρωση του μνημονίου. Δεν έχουμε καμία πολιτική νομιμοποίηση για να πράξουμε το αντίθετο.

— Σοφία Σακοράφα (@SofiaSakorafa) February 22, 2015

Updated

Bloomberg has rounded up the analyst reaction to Friday night’s Greek deal, and concluded that Athens came off second best.

Economists declare Greece the loser of the bailout negotiations. http://t.co/dEwSPiYXJT

— Bloomberg Markets (@markets) February 23, 2015

Here’s a flavour:

A “complete political surrender to the world of reality” was how Erik Nielsen, London-based global chief economist of UniCredit Bank AG, put it.

Societe Generale SA and Berenberg Bank both labeled it a “u-turn” by Alexis Tsipras, who won election on January 25 promising an end to budget cutting.

However, let’s see what reforms Athens proposes, shall we?

As Commerzbank AG chief economist Joerg Kraemer suggests, Tsipras may well manage to alter Greece’s bailout programme.

“Nominally, at least, the creditors have won, but reality is likely to be different,” said Kraemer.

Plus ça change?

A copy of The Guardian’s City pages from October 1962 has been discovered; the top news of the day included fighting deflation, and a Greek debt deal.

Brilliant. Nothing changes? Guardian page on deflation and Greek debt deal from Oct 1962 unearthed by a colleague pic.twitter.com/gBXI9Awhyl

— Katie Allen (@KatieAllenGdn) February 23, 2015

Hopefully such fears will be history when someone stumbles upon this liveblog in 2068....

Updated

There’s no financial reaction from Greece yet. The Athens stock market is closed today, to mark “Clean Monday”.

Traditional #Greece Lent Monday seafood. pic.twitter.com/CFlQCSSBbw

— Manos Giakoumis (@ManosGiakoumis) February 23, 2015

Updated

Ambrose hears that the Greek reform plan might run to five pages....

Am reliably informed that Greek reform list is 5 pages, including labour reform with ILO, and minimum wage (which will irk Berlin)

— A Evans-Pritchard (@AmbroseEP) February 23, 2015

Greek reform plan will include firm-level "smart" collective bargaining. Syriza's Left Platform not happy, but won't kibosh (apparently)

— A Evans-Pritchard (@AmbroseEP) February 23, 2015

Updated

The Greek bailout extension deal will put strains on Alexis Tsipras’s coalition government, predicts Mujtaba Rahman of Eurasia Group:

The real crunch time for Tsipras will come when the measures will actually need to be implemented. Syriza’s coalition partner, the Independent Greeks (ANEL) was created on the basis of its members’ antithesis to the bailout and austerity. Combined with opposition from his left, it will be difficult for Tsipras to keep his government together without any defections as he implements reforms that backtrack on the government’s promises and ideology.

Even if this were to happen, the bills would still likely pass through parliament with the help of pro-bailout parties (New Democracy, Potami and PASOK).

But this would call into question the leadership of this government, and could trigger a government reshuffle or new elections, potentially in the middle of discussions on a new bailout.

Eurozone finance ministers will discuss Greece’s list of reforms on a telephone conference call tomorrow.

That’s according to Germany finance ministry spokesman Martin Jaeger. He told reporters in Berlin that:

“The institutions (ECB, European Commission and IMF) will look at this list first, as agreed on Friday, and then give their opinion on it and on this basis there will be a discussion among the Eurogroup ministers and according to current plans, this will be in the form of a telephone conference.”

(quote via Reuters)

The plan must then be approved by national parliaments across the eurozone; German MPs could vote as early as Friday:

Bundestag Greece Vote On Feb. 27 Would Be Early Enough: Jaeger

— Steve Collins (@TradeDesk_Steve) February 23, 2015

Updated

Helena is also hearing that among the proposals being considered by Greece is a broad-based plan for privatisations of state assets to go ahead.

This will not sit well with far left radicals in the ruling Syriza party who have made state asset-stripping a “red line” they are not willing to cross.

Helena explains:

The Energy Minister Panagiotis Lafazanis, who heads the party’s Left Platform, has ruled out any sort of privatisation - in stark contrast to the finance minister Yanis Varoufakis who says he will “not be dogmatic” about denationalisations.

Over the weekend Lafazanis said: “Red lines won’t be violated. That’s why they are called red.”

Insiders: Greek list will be broad-brush

Our correspondent Helena Smith has been calling her sources in Athens, and can get no confirmation that the much-anticipated list of reforms has actually been sent to Brussels.

What she is hearing is that the list will be no longer than three-pages in total. It will be “broad-brush” and light of details, as the government is keen to get a steer on reaction to its proposals first.

Updated

It’s official - Greece’s proposals haven’t reached Brussels yet. And Athens has some time yet...

.@YanniKouts @minefornothing We have not received a list. Deadline is close of business tonight. We are in talks with #Greek authorities.

— Mina Andreeva (@Mina_Andreeva) February 23, 2015

Updated

Hmmmm. A European Commission spokeswoman says they’ve not received a copy of Greece’s proposals yet....

Now reports frm Commission that it is yet to receive #Greece reform list - wouldn't fit with the past 10 days if there wasn't a bit of drama

— Open Europe (@OpenEurope) February 23, 2015

The AFP news agency is reporting that Greece’s official programme of economic reforms has arrived at EU headquarters.

Afp Reporting That Greek Reform List Has Been Received In Brussels

— Live Squawk (@livesquawk) February 23, 2015

Now we just wait for the first leak. #Greece

— Yannis Koutsomitis (@YanniKouts) February 23, 2015

All eyes on Brussels for a reaction. If the eurozone isn’t impressed, there’s a possibility of more emergency meetings this week.

Nour Al-Hammoury, chief market strategist at ADS Securities, says:

If the Troika rejects the approach then another emergency meeting will be held with the Eurogroup tomorrow, but time is running out. The drama continues, but we still believe that they will come up with a deal....

Updated

The edgy peace between Greece and the EU could also be threatened by political instability in both Athens and Berlin.

I mentioned earlier that veteran Greek left-winger Manolis Glezos had lambasted the agreement yesterday. But Marc Ostwald, analyst at ADM Investor Services, points out that critics in Germany could also shake things up:

He writes:

That the Greece “deal” is the usual Euro area/EU can-kicking fudge goes without saying, the question is whether:

a) Syriza’s more restive radical elements can be kept in check by Messrs Tsipras and Varoufakis, and

b) the extent to which the “even more hardline than Schaeuble” elements of the CDU/CSU can be persuaded to bite their tongues, perhaps the more so given the blatant schism in the grand coalition, with the SPD taking a rather more conciliatory tone.

Of course, the whole exercise underlines that the resistance to addressing any of the Eurozone’s deep seated governance flaws remains sky high, and thus the next crisis is and will always be just around the corner.

Another example of Europe muddling through. The Telegraph’s Ambrose Evans-Pritchard sees more trouble ahead:

As dust settles, clearer that Friday Greek deal resolves nothing. EMU leaders not remotely off hook, face simmering crisis ad aeternum

— A Evans-Pritchard (@AmbroseEP) February 23, 2015

Updated

How nervous did Greek bank depositors get last week, as negotiations with the rest of the eurozone threatened to flounder?

Well. JP Morgan has estimated that deposit outflows from Greece’s banks accelerated to around €3bn during the week, up from €2bn in the previous seven days.

At that rate, Greek banks would have been unable to keep functioning in mid-April.

The 50% increase in outflows from the prior wk meant Greek banks were on track to run out of collateral for new loans in 8 weeks- JP Morgan

— cigolo (@cigolo) February 23, 2015

Credit Agricole economist Fred Ducrozet predicts several tense months as Greece and its creditors haggle over a long-term deal:

Overall implementation risks remain elevated, negotiations will go on for several months while the Greek state cash position remains tight ahead of large summer redemptions.

On the bright side, the interim agreement will buy Greece four more months to address the long-term issues and work out the details of a comprehensive deal including new fiscal targets and NPV debt reduction measures.

We still expect a politically-acceptable arrangement to be found eventually – the Eurogroup statement should be used as an important basis for this purpose.

That’s from his latest research note, which also shows how Greece faces hefty debt repayment over the next six months, how bank deposits are falling, and how its financial sector is dependent on emergency funding from the ECB:

The 3 key charts from my reaction piece on Greece - 4 more months of hope and risks. http://t.co/hj2le2YlP0 pic.twitter.com/FediTcqQGJ

— Frederik Ducrozet (@fwred) February 23, 2015

The relief rally is also pushing down the yields (the interest rates) on eurozone government debt.

That means Portugal’s sovereign bonds can now borrow at a lower rate than the United States:

Topsy Turvy World... “@YanniKouts: #Portugal 10-year bond yield drops below US', first time since 2007. /via @lemasabachthani #euro”

— Sony Kapoor (@SonyKapoor) February 23, 2015

Updated

The FTSE 100 has dropped back from its record levels, thanks to HSBC’s falling share price (still down 5%).

The other European markets are still benefitting from Greek relief....

....even though Greece’s debt problems aren’t fixed. As Gary Jenkins of LNG Capital writes:

The interim agreement was not really a victory for anyone.

At some stage the Greek debt pile will need restructuring, whether that be amended to include bonds linked to growth or the maturities extended further or even a real actual write down as there is very little chance of Greece repaying its debt as things currently stand. In 2011 I said that a 65% write down was required to give Greece a fighting change. Even after the private debt restructuring that percentage is probably still not far from what is required.

One wonders if some of the Eurozone finance ministers now wish they had been slightly more proactive 6 months ago and offered the then Greek PM Mr Samaras an amendment to lower the primary surplus target.

Greece is also planning to raise its minimum wage “gradually”, the spokesman added.

And he’s also pledging that pensions – another ‘red line’ for the new government – will not be cut

Note that #Greece raising minimum wage won't affect the budget surplus. BUT it's a violation of the program formerly know as "the program"

— HansNichols (@HansNichols) February 23, 2015

Greek Govt spox says will not cut pensions, red lines continue to apply.

— Steve Collins (@TradeDesk_Steve) February 23, 2015

Greece’s government spokesman has confirmed that will send its list of economic reforms to Brussels before the end of the day.

- GREEK GOVT SPOKESMAN SAYS GREEK REFORMS LIST WILL BE SENT TO EU PARTNERS WITHIN THE DAY

- GREEK GOVT SPOKESMAN SAYS LIST WILL INCLUDE REFORMS AGAINST TAX EVASION AND CORRUPTION

- GREEK GOVT SPOKESMAN SAYS WE ARE DISCUSSING WITH PARTNERS TO ENSURE LIST IS ACCEPTED

Berenberg: Grexit risk cut to 25%

The odds of Greece quitting the eurozone has fallen, says German bank Berenberg this morning.

It has cut the chances of a ‘Grexit’ to 25%, after the Athens government and its creditors reached agreement on Friday night.

Dr Holger Schmieding, chief economist, says:

The risk of Grexit falls from 35% to 25%; the chance that prime minister Tsipras completes his required Uturn and stays the reform course (“Samaras II”) rises from 45% to 50%;

the probability that his double-populist government falls apart to make way for a less populist and more pro-European government rises from 20% to 25%.

The risk of immediate capital controls in Greece has receded.

Schmieding also points out that this “new deal” is rather similar to the previous bailout agreement:

The key elements of the deal struck late on Friday are:

● Greece accepts all conditions attached to its EU/IMF bailout programme;

● Greece stays under full supervision of the “institutions” that used to be called troika;

● Greece can make adjustments within the programme but only if the changes are neutral for the immediate and long-term fiscal outlook and are approved by its external supervisors;

● Greece will receive the last tranche of support to be paid under the current programme only if it meets all conditions. Greece probably needs the money in March for €2.2bn debt service payments, of which €1.4bn are to the IMF.

Syriza gets real - but will the deal last? #Grexit risk down to 25%, but 4 risks remain http://t.co/3sCjEec264

— Berenberg Economics (@Berenberg_Econ) February 23, 2015

Updated

The next six months could be gripped with drama:

#Greece's Tsipras walks another high wire over next 24h. http://t.co/NFqYlT0CRb pic.twitter.com/sFcjUKx2eY

— Holger Zschaepitz (@Schuldensuehner) February 23, 2015

Updated

HSBC shares hit by falling profits

Back in the City, shares in banking giant HSBC are falling fast after it reported a 17% drop in pre-tax profits for the last year.

HSBC, which is leading the FTSE 100 fallers, also apologised for the conduct of its Swiss Private Bank, following a series of revelations about aggressive tax avoidance.

We deeply regret and apologise for the conduct and compliance failures highlighted which were in contravention of our own policies as well as expectations of us.

Shares fell over 2% as HSBC’s results hit the wires, and are now down 5%.

HSBC's shares down 2.3%. Douglas Flint, chairman: "We deeply regret and apologise for the conduct and compliance failure" in Switzerland

— Jill Treanor (@jilltreanor) February 23, 2015

Today, the Guardian reports that CEO Stuart Gulliver sheltered millions of pounds in a Swiss account through a Panamanian company and remains tax domiciled in Hong Kong.

Monday's Guardian front page: Swiss account secret of HSBC chief revealed #tomorrowspaperstoday #bbcpapers pic.twitter.com/pkEKRg40Ja

— Nick Sutton (@suttonnick) February 22, 2015

Excellent news. The FT’s Peter Spiegel reckons Greece may let us all see its reform programme:

Sounds like #Greece submission will indeed be much more than just "tax crackdown", and proposal may be made public. Interesting day ahead.

— Peter Spiegel (@SpiegelPeter) February 23, 2015

FTSE 100 parties like its 1999, FINALLY surpasses record closing level http://t.co/vvxQB1K5rC pic.twitter.com/SBWw3UBNna

— Robin Wigglesworth (@RobinWigg) February 23, 2015

Germany’s DAX has also hit a new record high this morning, jumping 1% in early trading.

The FTSE 100 has surpassed the record close in intra day trading, but not the intra day high of 6950 (Dec 30th 1999) @LSEplc

— Guy Harding (@GuyHardingSky) February 23, 2015

FTSE 100 hits new 15-year high

Breaking: The FTSE 100 index of leading blue-chip shares has hit its highest level in 15 years.

Optimism over Greece’s rescue deal sent the FTSE up by 0.4% at the start of trading, to 6943 points.

That’s above the closing high of 6930 hit on 31 December 1999, and only a few points away from the record intraday high of 6950 earlier on that day, as the dot-com boom began to blow up (what heady days they were, dear readers).

U.K.'S FTSE 100 SURPASSES RECORD CLOSE IN INTRADAY TRADING

— Francine Lacqua (@flacqua) February 23, 2015

Mike van Dulken, head of research at Accendo Markets, confirms that Greek fears have abated:

The positive open comes after news late Friday that Greece and the Eurogroup had reached a tentative agreement for an extension of its bailout for four months.`

But plenty of experts are warning that the Greek crisis hasn’t gone away.

Michael Hewson of CMC Markets writes:

While the fear of a Greek exit has been avoided for now, it is by no means off the table, and to all intents and purposes nothing much has changed, in Greece, or anywhere else for that matter.

Strains still remain with record unemployment, sluggish growth as well as low or negative inflation, confirmation of which is expected to come later this week from Germany, Italy and Spain.

Robin Bew of the Economist Intelligence Unit agrees that Greece’s problems are far from over:

#Greece deal only buys 4mths, even if reform programme approved. Hardly game changing - names changed, basic outline still the same.

— Robin Bew (@RobinBew) February 23, 2015

In other news, the UK government has trimmed its stake in Lloyds Banking Group -- more than six years after rescuing the bank. More here.

Government sells £500m of Lloyds shares in key week for bailed-out bank http://t.co/6J2XvLqsjl

— Jill Treanor (@jilltreanor) February 23, 2015

#FTSE 15 points away from record high of 6930 - now at 6915.20. @guyjohnsonTV on #ThePulse pic.twitter.com/Yx2ObE2wu2

— Francine Lacqua (@flacqua) February 23, 2015

The Financial Times reckons says the Greek reform programme may be light on specifics:

The reforms would be “mainly of a structural nature” and would not include details of projected revenue increases or spending cuts, a Greek government official said.

Still, Athens intended to spell out measures to crack down on tax evasion and fuel and cigarette smuggling that could raise about €2bn-€2.5bn this year, the official added.

If "crackdown on tax evasion" is sum total of #Greece reform proposals, we may be in for a long week. I suspect there's more, tho.

— Peter Spiegel (@SpiegelPeter) February 23, 2015

Updated

Eurozone crisis expert Yannis Koursomitis has tweeted more details of the Greek tax clampdown (and also wonders whether it’ll work):

#Greece govt's extra revenue plan: Gasoline smuggling €1.5bn, cigarette smuggling €800ml, rich ppl taxation €2.5bn, tax arrears €2.5bn ~Bild

— Yannis Koutsomitis (@YanniKouts) February 23, 2015

#pt - I'm not convinced these goals are achievable. In any case I wish the Greek gov't good luck.

— Yannis Koutsomitis (@YanniKouts) February 23, 2015

Nikkei hits 15-year high

Asian investors have driven the Japanese stock market to a 15-year high today, on relief that Greece and its creditors had agreed to extend its bailout by four months.

The Nikkei rose 0.7% to 18,466.92 points, its highest close since April 2000.

Updated

Introduction: Greece to send reform plans today

Good morning, and welcome to our rolling coverage of Greece’s bailout and other events across the global economy, the financial markets and business.

The sticking-plaster agreement hammered out in Brussels on Friday night faces its first test today, as the Greece government outlines the economic reforms it will deliver in return for its four-month bailout extension.

That plan is due to be delivered to eurozone officials today, but details have already leaked out.

According to Germany’s Bild newspaper, Athens is gunning for unpaid taxes -- including €2.5bn from powerful Greek tycoons, another €2.5bn from individuals and businesses, and €2.3bn from clamping down on illegal smuggling of petrol and cigarettes.

Greece draws up €7.3bn tax hit list aimed at oligarchs and criminals - report

Clamping down on tax dodging is a noble enterprise, of course. But will the eurogroup be convinced that it’s achievable?

There are already signs that Friday night’s compromise is creating tensions in Athens. As we wrote last night, veteran left-wing politician Manolis Glezos has blasted the Syriza government for yielding to pressure and extending its bailout, along with further oversight from the EU, ECB and IMF.

Glezos said:

“I apologise to the Greek people that I cooperated in this illusion,”

“Some claim that as part of a deal you have to back down. First of all, there can be no compromise between the oppressor and oppressed, just as there cannot between the slave and the tyrant, the only solution is freedom.”

Here’s a full translation:

I just translated the stmnt released by Manolis Glezos, #Syriza MEP & Resistance fig, slamming govt's realistic turn. pic.twitter.com/6YIciTcson

— The Greek Analyst (@GreekAnalyst) February 22, 2015

In the short-term, last week’s breakthrough is calming the financial markets. We could see Britain’s FTSE 100 hit a new all-time high today.

I’ll be tracking all the main events through the day.

Updated