PS: about that Bild stunt:...

German tabloid Bild today called on Germans to 'say no to greedy Greeks'. Their response is #NeinZurBild 'No to Bild' pic.twitter.com/TPgDo8LK3K

— JubileeDebtCampaign (@dropthedebt) February 26, 2015

And finally, our Europe editor Ian Traynor has filed this analysis on Friday’s vote, and beyond...

The German parliament is expected to agree to extend the eurozone’s bailout of Greece on Friday, capping a tumultuous first four weeks in office for the anti-austerity government in Athens. The next four months will be crueller yet.

That will be clear from the debate in the Bundestag in Berlin. Although Chancellor Angela Merkel has never been outvoted in five years of policy decisions on the euro crisis and need not fear defeat on Friday, the endorsement will be grudging and will reek of suspicion of the Greek prime minister, Alexis Tsipras.

At least 25 of Merkel’s 311 MPs will oppose or abstain on the Greek rescue vote, in the largest act of dissent on Greece that Merkel has seen from her backbenchers.

Patience with Greece is running out in Berlin. It is also turning to exasperation because of what is seen as the intemperate tone of Tsipras and his team.

“There can be no reward for cheek,” said the bestselling Bildzeitung tabloid on Thursday under a one-word banner headline of “Nein, no more billions for greedy Greeks.”

More here:

Greece bailout saga strains German patience http://t.co/74gxVNP7Xj

— JPmartinez-finance (@JPMFIN) February 26, 2015

That might be all for tonight. See you tomorrow for the vote! GW

Updated

Greece’s Ta Nea newspaper is reporting tonight that Greece could need a third bailout of some 30 billion euros, when its existing programme ends. It is attributed to eurozone sources, Helena flags up. The MNI newswire had the story earlier.

See http://www.tanea.gr for more.

This might come up in tomorrow’s debate over the Greek bailout extension in the German parliament.

Updated

Greek PM vows swift clampdown on tax evasion

Tax evasion is also a big theme in Greece today.

Athens prime minister Alexis Tsipras has been addressing his radical left Syriza party’s political secretariat in a meeting that cadres described as “very heavy.”

Helena Smith has the story:

The young leader, clearly attempting to quash displeasure over last week’s “bridge agreement,” said the government was poised for a “daily fight over the next four months.”

Tsipras vowed:

“We will move quickly to apply swingeing reforms to clamp down on tax evasion and corruption and reforming the public administration, “

He added that the leftist-led coalition would also move to effect “the basic body” of commitments made to the working class.

Greece, he said, would also exploit “the country’s geopolitical strength as part of the government’s negotiating power.”

Successive Greek governments have made much of the country’s location as the European Union’s only Balkan state at the cross-roads of East and West (one increasingly used as a transit route by immigrants and refugees). Similar emphasis has been placed on Greece’s role as a NATO member in an increasingly dangerous neighbourhood.

Doubts expressed over the agreement by John Milios, Syriza’s chief economist and the man in charge of the party’s economic policies, had cast a shadow over the meeting with MPs meeting, cadres said.

Milios spoke of a “big climbdown” in his blog today - prompting minister of state Alekos Flampourari to say he didn’t think it was opportune for such statements to be made “by someone who is still responsible for the economic policy of the party.”

“There are a lot of questions, a lot of unclear things about the agreement,” a Syriza MP has just told me asking that he not be named “lest my comments be misunderstood.”

“We are coming round to accepting that the agreement was the best we could do but it still hurts.”

The BBC has more details about the proposed sale of Coutts’ international arm:

Last year RBS appointed Goldman Sachs to find a buyer for Coutts’ international operations, as part of its drive to focus on the UK business.

Coutts International employs 1,200 people, has some £21.5bn of assets under management and has an estimated value of up £800m .

A buyer would have to find a new name for the international operation as RBS intends to keep the Coutts brand for the UK business.

Tax barrister Jolyon Maugham QC, who has worked on several important tax cases recently, tweets that other banks may face similar investigations:

@jamesrbuk if Coutts is the last I'll eat my (horsehair) wig.

— Jolyon Maugham QC (@JolyonMaugham) February 26, 2015

You can see our news story about the German probe into Coutts here:

Coutts’ Swiss operation faces German investigation over tax evasion claims

The US investigation into possible tax evasion have already hit RBS’s efforts to sell Coutts International, according to the Financial Times.

The FT reported last week that:

Bidders for Coutts International have tried to use the recent scandal over tax evasion by clients of HSBC’s Swiss arm to lower the price of the private banking assets being sold by Royal Bank of Scotland, said people familiar with the situation.

This new investigation by German authorities may not make the sale any easier.

Although the FT does point out that RBS has been pro-actively addressing the issue:

Bidders for Coutts International have been given a detailed breakdown of the bank’s client portfolio in an attempt to reassure them that it does not include any potential problem cases of either tax-dodging or money-laundering.

My colleague Juliette Garside flags up the help that Coutts offers its clients:

Coutts website offers advice on "how to structure your wealth to take maximum advantage of the Swiss taxation system" http://t.co/RyH62FCfrQ

— Juliette Garside (@JulietteGarside) February 26, 2015

Advice from the Queen's bank on how to shelter wealth in Switzerland #Coutts pic.twitter.com/I87m9DNUou

— Juliette Garside (@JulietteGarside) February 26, 2015

RBS CEO pledges tough action over tax probe

Ross McEwan, chief executive of RBS discussed the tax evasion probe into Coutts’ Swiss arm by German authorities at a press conference in London.

Our City editor Jill Treanor was there, and reports:

McEwan explained the Coutts International business was being sold because it did not make money and that private banks had taken too long to clean up their activities.

McEwan said.

“I want to be very clear if we find anything that has evidence of wrong doing we will come down incredibly hard on any of those issues.”

”Any situation like this we take seriously… it if the reputation of our business. This is what has tarnished the banking industry and in my view private banks have taken far too long to catch up with the public’s expectations.”

Coutts was founded in the late 17th century, and acquired Zurich-based Bank von Ernst & Cie in 2003.

As covered earlier, McEwan has also waived a £1m ‘allowance’, on top of his basic salary, after reporting that RBS posted a £3.5bn loss this morning.

McEwan, who is a New Zealander, has also explains that he is non-domiciled for tax purposes, and doesn’t have a Swiss account himself.

Ross McEwan says he is a resident non-dom. "I'm a proud Kiwi but I work here and I pay taxes here".

— Joel Hills (@ITVJoel) February 26, 2015

Ross McEwan says he has bank accounts in the UK, New Zealand (he was born there) and in Australia (he worked there) but not Switzerland.

— Joel Hills (@ITVJoel) February 26, 2015

Yesterday, MPs on the Treasury committee grilled HSBC chief Stuart Gulliver over his decision to use a Swiss account through a company based in Panama.

Updated

Coutts probe: the official statement

Back to the news that Coutts bank is being investigated by German authorities over whether its Swiss banking arm helped customers evade tax.

RBS discloses the probe on page 120 of its 2014 financial results, released this morning.

It says:

German prosecutor investigation into Coutts & Co Ltd

A prosecuting authority in Germany is undertaking an investigation into Coutts & Co Ltd in Switzerland, and current and former employees, for alleged aiding and abetting of tax evasion by certain Coutts & Co Ltd clients. Coutts & Co Ltd is cooperating with the authority.

RBS says German authorities looking at its Coutts private bank in its legal warnings

— Jill Treanor (@jilltreanor) February 26, 2015

Coutts has also been investigated by the US Department of Justice, over “the possibility that some of its clients may not have declared their assets in compliance with US tax laws.”

It presented the results of its own investigation to the DoJ last summer, and expects to reach “a resolution” during 2015.

Back in Greece, the Syriza party is putting on a brave face after yesterday’s marathon, record-breaking 12-hour session to discuss the bailout situation, writes Helena Smith in Athens.

A phalanx of Syriza cadres appearing on TV chat shows this morning said the deal was essentially “not an agreement” but the key that would unlock the door to new negotiations.

Syriza MEP Kostas Chrysogonos declared:

“The next four months are what is critical....There is no agreement as such.”

Christos Mantas, who is secretary of Syriza’s parliamentary group, said “every MP had the chance to speak” at yesterday’s marathon session.

He told Star TV that:

“We have taken a small step that is only the beginning. Things will be judged on how we govern....Next week you will see that parliament will begin operating and a lot of legislation will be pushed through,”

Mantas added that the bills would include protective measures for austerity-hit Greeks, concluding.

“Why is (German finance minister Wolfgang) Schauble so angry, if we are such good guys?”

Updated

German authorities probe Coutts over tax evasion allegations

Royal Bank of Scotland has revealed that Coutts, its private banking arm, is being investigated by German authorities.

They are examining whether it helped clients to evade tax by using Swiss bank accounts – a hot topic, following revelations around HSBC in recent weeks.

German prosecutor investigating #RBS (Coutts) in #Switzerland for aiding and abetting tax evasion by customers pic.twitter.com/PXaamVML2p

— Dominic Lindley (@DominicLindley) February 26, 2015

Coutts, one of the world’s oldest banks, is famous for handling the Queen’s financial affairs.

RBS CEO Ross McEwan has been questioned about the probe, and pledged to take “severe action” if wrongdoing is discovered.

ITV News business editor Joel Hills has tweeted the key points:

Ross McEwan reveals RBS's private bank now being investigated in Germany (as well as US) for allegedly helping wealthy clients evade tax

— Joel Hills (@ITVJoel) February 26, 2015

Ross McEwan on @CouttsandCo and alleged tax evasion "if we find anything that's gone wrong in that business...we will take severe action."

— Joel Hills (@ITVJoel) February 26, 2015

Ross McEwan tells @itvnews that decision to sell @CouttsandCo was moral as well as commercial.

— Joel Hills (@ITVJoel) February 26, 2015

Updated

Hmmm. The €700m that flowed back into Greek banks on Tuesday may be related to pension payments by the government, reckons Kathimerini newspaper -- More here.

So, maybe the tide hasn’t turned quite as much as Varoufakis suggested.

Still, a senior banker has told Reuters that another €150m came in on Wednesday.

Updated

The German Association of Journalists has called on Bild to ditch its anti-Greek campaign.

They argue that Bild has crossed the line into political campaigning, by urging readers to pose with their “Nein” poster ahead of tomorrow’s Bundestag vote [see earlier post].

They added that it is ethically questionable to vilify a whole nation for the fiscal mistakes of their politicians.

Updated

The governor of Greece’s central bank has predicted that the country’s economy will grow this year, unless the fragile recovery is derailed by bailout deadlock.

Yannis Stournaras (the former finance minister) told an audience in Athens that it was vital that Greece reaches a final agreement with its creditors to cover future funding needs.

Delivering his annual report, Stournaras urged the government to pursue talks with its creditors in a spirit of co-operation.

There is no room for complacency, he added, given the strain that Greek banks have come under and the fragility of the recovery.

But the worst could be over, Stournaras said:

“In the past few years, we have covered some very rough ground at high cost to the whole of Greek society.

“If we can address the relatively few issues still pending and complete the first phase of the effort launched in 2010, we will then be able to move on to the next phase, in which the growth potential of the economy will be considerably enhanced.”

(I’ve taken the quotes via AFP)

Reuters snapped other key points:

- GREEK CENTRAL BANK GOVERNOR SAYS REACHING NEW DEAL WITH PARTNERS MAY BE NECESSARY FOR RECOVERY TO TAKE ROOT BUT GROWTH PLAN ALSO NEEDED

- GREEK CENTRAL BANK GOVERNOR SAYS GREEK BANKS ARE WELL-CAPITALISED BUT LIQUIDITY HAS COME UNDER CONSIDERABLE STRAIN IN RECENT MONTHS

- GREEK CENTRAL BANK GOVERNOR SAYS GREEK BANKING SYSTEM FACES SERIOUS CHALLENGES DUE TO HIGH LEVEL OF BAD LOANS

- GREEK CENTRAL BANK GOVERNOR URGES GOVT TO COMPLETE STRUCTURAL REFORMS, REVIEW TAX POLICY, COMPLETE MAJOR PRIVATISATIONS

Yanis Varoufakis also attended the annual meeting:

Bild’s campaign against those “Greedy Greeks” may be backfiring.

This reader has posed for a selfie, as instructed, but he’s refusing to pay for that ‘stupid’ newspaper:

Take a NEIN selfie for #Geece with @BILD ! @sechsdreinuller does it the right way pic.twitter.com/nucSWPJiqw

— The Gentle Thinker (@GentleThinker) February 26, 2015

German news magazine Spiegel confirms that CDU/CSU MPs expressed concern about the Greek loan deal, at their meeting with Wolfgang Schäuble this morning.

It also reports that CDU parliamentary leader Volker Kauder criticised the “loutish” comments made by Greek politicians -- it’s not clear exactly what he’s referring to. More here.

As mentioned earlier, 22 conservative MPs indicated they’d oppose extending Greece’s bailout, in a test ballot at the meeting.

German conservatives agree to extend #Greece aid, but FinMin #Schäuble is "stunned" by tone of Varoufakis interview in #CharlieHebdo. 1/2

— Charles Hawley (@charles_hawley) February 26, 2015

Schäuble: "If #Greece violates agreement, then it is invalid." Said that Greeks are trampling on European solidarity. http://t.co/uQjqvAfHTM

— Charles Hawley (@charles_hawley) February 26, 2015

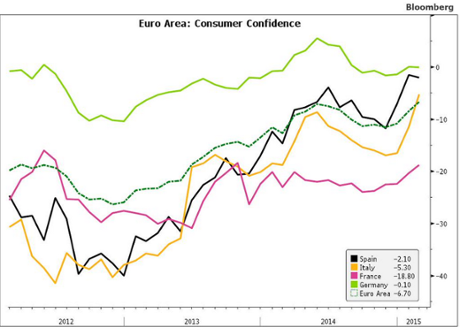

Europe’s economy may be turning the corner.

Consumer confidence has hit a seven year high this month, Eurostat just announced, with people in several eurozone nations reporting that they’re a little more optimistic:

And the M3 measure of money supply has also risen, suggesting economic activity picking up:

Eurozone M3 annual growth up to 4.1% YoY, better than expected. Old 4.5% 'target' not far off anymore.

— Frederik Ducrozet (@fwred) February 26, 2015

With Germany’s unemployment total falling again this morning, there are some encouraging signs that growth may be picking up.

Updated

ECB: €12bn withdrawn from Greek banks in January

Greek banks suffered a significant deposit flight last month, new data from the European Central Bank shows.

Around €12bn was withdrawn from Greek banks in January, the ECB says, taking deposits down to €155.4bn.

That’s close to, or possibly even below, the levels plumbed in 2012.

NEW official data: #Greece bank deposits -12bn€ in Jan, lowest level in 10 years. Was about time to reach that deal! pic.twitter.com/AygFoTnpsl

— Maxime Sbaihi (@MxSba) February 26, 2015

Analysts believe the withdrawals continued this month, as Athens clashed with its creditors over a bailout extension.

Indication of pressure on Greece during negotiations. In January deposits in Greek banks fell by 12 billion € . # Greece

— Gavin Hewitt (@BBCGavinHewitt) February 26, 2015

But the situation may be changing.

Finance minister Yanis Varoufakis has declared that €700m flowed back into Greek banks on Tuesday.

He told Bloomberg TV that savers took confidence from the deal agreed last Friday, and signed off by Greece’s lenders on Tuesday

“There was a deposit flight back into the Greek banking sector,”

“It’s a question of direction. Once you turn the tide, you hope.”

More here: Greek bank deposits return after bailout extension

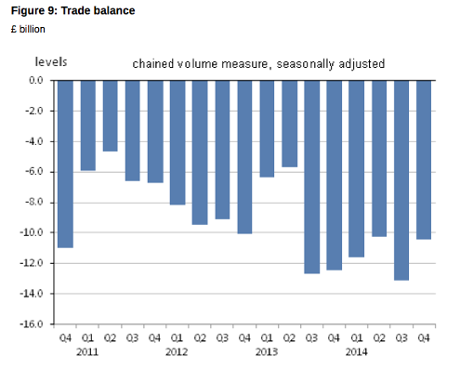

On a happier note, the ONS also reports that UK exports rose by 3.5% in the last quarter of 2014.

That reverses a 0.8% drop in the third quarter. Imports increased by 1.3%, meaning the UK’s dire trade position improved for once.

We badly need this! RT @mhewson_CMC UK Exports revised up for Q4 to 3.5%.

— Shaun Richards (@notayesmansecon) February 26, 2015

But it’s still quite bad:

There’s a worrying new fact in today’s UK GDP data; British business investment has fallen at its fastest pace in almost six years.

Business investment dropped by 1.4% in the last three months of 2014, following a 1.2% decline in July-September.

It was driven by a drop in spending in the energy sector, probably in response to falling oil and gas prices.

UK growth confirmed at +0.5%

The UK economy grew by 0.5% in the last three months of 2014, the Office for National Statistics reports. That matches the initial estimate.

Here’s Jill Treanor’s take on Royal Bank of Scotland’s results:

Royal Bank of Scotland has revealed it handed out £421m in bonuses in 2014 as it reported its seventh consecutive year of losses and appointed Sir Howard Davies as its new chairman.

Its chief executive, Ross McEwan, also warned of substantial job cuts as a result of a further retrenchment of its once-dominant investment bank. RBS said it would reduce its operations to 13 countries, compared with 38 at the end of last year and 51 in 2009, just after it was bailed out.

Announcing another overhaul of the investment bank, McEwan said: “This marks the end of a standalone investment bank at RBS.” The move is intended to focus the bank on the UK.

Davies, chairman of the airports commission and a former City regulator, is replacing Sir Philip Hampton as chairman at the 79%-taxpayer owned bank. He will join the board in June before taking over the top job in September....

Full story: RBS paid out £421m in bonuses in 2014 despite £3.5bn loss

This morning's news of far bigger drop than expected of 20k in German Feb unemployment fits with my read the world economy is picking up.

— Gerard Lyons (@DrGerardLyons) February 26, 2015

German unemployment rate at record low

Just in: Another strong month of unemployment data from Germany, backing hopes that Europe’s largest economy is picking up.

The unemployment total fell by 20,000 this month, on a seasonally-adjusted basis, twice as much as expected.

That leaves the unemployment rate at a record low of 6.5%.

GERMAN UNEMPLOYMENT FELL 20,000 IN FEB. VS EST. 10,000 DROP

— World First (@World_First) February 26, 2015

Some City bankers are too buttoned up. But not Bill Winters, the new boss of Standard Chartered!

As this video shows, he doesn’t mind loosening a few buttons for charity, and can pull off a decent falsetto at the same time.

Full story on the Wall Street Journal:

Ever Wanted to See Bankers Strip?

@katie_martin_FX he'll be so delighted he did that.

— Lady FOHF (@LadyFOHF) February 26, 2015

Updated

Reuters: Germany says Greek deal could be ditched

There are fresh signs of jitters in Germany over Greece’s bailout today.

Reuters is reporting that finance minister Wolfgang Schäuble told CDU party members that the extension could be abandoned if Athens doesn’t stick to its pledges.

Here’s the story:

Germany’s Wolfgang Schaeuble told a meeting of conservatives lawmakers on Thursday that recent remarks by the Greek finance minister had strained European solidarity and that a bailout extension for Athens could be ditched if the country failed to stick to its promises, according to participants.

The German finance minister met lawmakers from Chancellor Angela Merkel’s conservative bloc to prepare for Friday’s vote in the Bundestag on extending the Greek bailout in return for a new package of reform commitments by the new leftist-led government of Alexis Tsipras.

Lawmakers speaking on condition of anonymity said Schaeuble said Greek Finance Minister Yanis Varoufakis “strains the solidarity of European partners” in interviews where he has resurrected talk of a debt haircut for Greece and cast doubt on its ability to repay its international debts.

German Fin Min Schaeuble tells German MPs that Greek Fin Min Varoufakis ' strains the solidarity of European partners.'#Greece

— Gavin Hewitt (@BBCGavinHewitt) February 26, 2015

The Bild tabloid has also weighed in, encouraging readers to send a photo of themselves posing with a page saying ‘NO!’ to giving ‘Greedy Greeks’ more cash.

How low can they go? "No further billions 2 greedy #Greeks" screams #Bild! Says hold page up, take selfie & send it! pic.twitter.com/ccSm9wUqsM

— Sony Kapoor (@SonyKapoor) February 26, 2015

Could someone kindly remind Bild where most of Greece’s bailout money has gone?

Boardroom clearout at Standard Chartered

It’s official: Standard Chartered CEO Peter Sands is leaving the company, replaced by Bill Winters.

And he’s not alone -- the bank has also announced that chairman John Peace will depart in 2016. Jaspal Bindra, CEO for Asia, is also leaving soon, along with three other long-serving non-executives. Here’s the statement.

Report: 22 conservative German MPs oppose Greek deal

Newsflash from Germany: 22 MPs from Angela Merkel’s CDU party and their CSU allies* are planning to oppose Greece’s four-month bailout extension in Friday’s vote.

[* - tweaked, thanks readers]

*GREEK AID EXTENSION OPPOSED BY 22 MERKEL CAUCUS MEMBERS: HILLE

— Frederik Ducrozet (@fwred) February 26, 2015

That’s not enough of a rebellion to stop the legislation passing, as Merkel’s coalition has a chunky majority.

Updated

In other banking news, Sky are reporting that Standard Chartered is about to name a new chief executive:

EXCLUSIVE: Standard Chartered to name Ex-JP Morgan executive Bill Winters as new chief executive; announcement later today, I'm told.

— Mark Kleinman (@MarkKleinmanSky) February 26, 2015

If so, Peter Sands’ increasingly precarious grip on the CEO’s chair has finally been broken, after months of shareholders pressure over its falling profits.

Shares in Standard Chartered are up 3.6% in early trading, followed by RBS - up 2%.

RBS planning 'substantial' job cuts

RBS CEO Ross McEwan has announced there will be “substantial” job cuts as he continues to reshape the company.

Its investment bank is being particularly hit.

McEwan just held a conference call with reporters; Jill is tweeting the key points:

"Let me be clear, this marks the end of a standalone investment bank at RBS" says CEO McEwan as he announces further retrenchment

— Jill Treanor (@jilltreanor) February 26, 2015

RBS boss admits there will be "substantial" job cuts as a result of the latest restructuring… "unfortunately they will be substantial"

— Jill Treanor (@jilltreanor) February 26, 2015

RBS is also planning to “fully exit” its markets businesses in Central and Eastern Europe, the Middle East and Africa, and substantially cut its presence in Asia Pacific and the US.

Chancellor George Osborne has flexed his muscles and decreed that RBS’s top directors should not take home a bonus this year.

In a letter to the bank, Osborne says:

I would expect that no executive directors or members of the executive committee will receive bonuses.”

Britain’s government still owns 79% of RBS, having pumped tens of billions of pounds into the bank to rescue in the financial crisis.

RBS incurred almost £2.2bn in fines, provisions and legal costs last year, for its role in a series of banking scandals and blunders.

The bank explains:

This included additional provisions for PPI redress (£650 million) in PBB, provisions relating to investigations into the foreign exchange market (£720 million) in CIB, Interest Rate Hedging Product redress (£185 million), the fine relating to the 2012 IT incident (£59 million) booked in Centre and other costs (£580 million) including provisions relating to packaged accounts and investment products.

That’s actually an improvement on 2013, when litigation and conduct costs hit £3.8bn.

#RBS takes £2.2bn hit on costs of litigation and mis-selling in 2014 accounts

— Douglas Fraser (@BBCDouglasF) February 26, 2015

Updated

RBS has also confirmed that its CEO, Ross McEwan, will not take a £1m ‘pay allowance’ [designed to avoid the EU’s bonus cap] which he was entitled to 2014, as reported last night.

Howard Davies confirmed as RBS's new chairman

RBS also has a new chairman, Sir Howard Davies (former head of the CBI, the Financial Services Authority, the London School of Economics...)

#RBS confirms Howard Davies will be its new chairman. #RBS narrows its losses to £3.5 billion in 2014 - down from £9 billion in 2013.

— Sally Bundock (@SallyBundockBBC) February 26, 2015

2014 wasn’t a vintage year for RBS’s investment bankers:

Total #RBS bonus pool £421m down 21% on last year. Bonuses for 'risky' investment bank down by half to £114m @BBCNews

— Ben Thompson (@BBCBenThompson) February 26, 2015

RBS posts £3.5bn loss

Another year, another loss at Royal Bank of Scotland.

RBS has just reported that it made an attributable loss of £3.5bn in the last financial year. That’s mainly due to writing down the value of its US business, Citizens, by £4bn and a tax charge.

That’s an improvement on last year, when the bank lost around £9bn. But the turnaround job at RBS, bailed out by the taxpayer six years ago, continues. This is the seventh loss in a row.

RBS’s bonus pool has shrunk too; bankers will share £421m this year, down from £536m a year ago.

The agenda: Greek debt talks and RBS results

Good morning, and welcome to our rolling coverage of Greece, the world economy, the financial markets and business.

Today we’ll be tracking the political tensions in Athens over its bailout agreement, as analysts fret about Greece’s ability to meet its debt repayments in the coming months.

Yesterday, Syriza MPs talked for hours behind closed doors, amid mounting angst over the government’s privatisation plans.

Energy minister Panayiotis Lafazanis is emerging as the leading voice of dissent over the decision to compromise with Greece’s lenders, declaring:

“There are parts of the letter [with reform proposals] that are reminiscent of the lenders’ language, not ours.”

We also the latest German unemployment data (9am GMT), the second estimate of UK growth in the last quarter (9.30am), and a new measure of eurozone consumer confidence (at 10am).

Today: Euro-zone consumer confidence, German unemployment; Greece’s Varoufakis says counts on ECB’s #Draghi to avoid a default next month

— Francine Lacqua (@flacqua) February 26, 2015

In the UK, Royal Bank of Scotland – bailed out in the financial crisis – is issuing its results this morning and also announcing Sir Howard Davies as its new

There’s a veritable flurry of other big-name companies reporting too:

UK companies posting results today - Capita, RBS, Ladbrokes, Interserve, RSA, Merlin Entertainment, Domino Pizza, Spirent Communications

— David Buik (@truemagic68) February 26, 2015

I’ll be tracking all the main events through the day...