A late newsflash: The European Central Bank has reportedly decided to increase the emergency liquidity it provides offer to Greece, but only by €200m.

That takes the ELA limit to €80.2bn.

European Central Bank raises emergency funding cap for Greek banks by €200M to €80.2B - DJ

— CNBC Now (@CNBCnow) May 20, 2015

That’s a surprisingly small increase. But one source has told Reuters that Greece hasn’t hit the €80bn limit yet; it now has a €3bn buffer to cope with capital withdrawals.

In short, it leaves plenty of pressure on Athens to come to a deal with its creditors, before facing that €305m repayment to the IMF on June 5.

Tsipras and Merkel to discuss Greek crisis on Thursday night

And finally, some important news from Greece as it strives to reach a deal with its creditors.

Speaking to the Guardian in Athens tonight, government spokesman Gavriel Sakellarides said the Greek prime minister Alexis Tsipras would be meeting Angela Merkel on Thursday night, after EU leaders had attended an official summit dinner in Riga, Latvia.

Sakellarides told us:

“We know that decisive decisions ultimately are taken at the level of finance ministers in the Euro Group but at this critical moment a meeting between Tsipras and Merkel can only be helpful.”

Talks would focus on the headway negotiators had made since the two leaders last met, said Sakellarides.

They will also cover the urgency of Greece’s liquidity problem, and issues such as VAT, pensions and labour deregulation which continue to be the major stumbling blocks between the two sides.

But Sakellarides, who is among Tsipras’ closest allies, denied that the leftist-led government now faced the dilemma of sticking to its “red lines” or seeing the county rejected from the euro zone.

“It is not a question of red lines or the eurozone. It boils down to what everybody has understood in the last five years which is that the regime of austerity has failed.

The persistence of the architects of this regime and their insistence of keeping the country on the same track, is simply irrational. We want to stop the vicious cycle of debt and recession. It’s not about stubbornness. It’s about preserving Greece and its people.”

And that’s probably all for tonight. Back tomorrow. Thanks for reading and commenting. GW

Updated

Another bad day for the banks' reputation

Time for a recap:

Announcing the fines Loretta Lynch, US attorney general, said the banks had exhibited “breathtaking flagrancy” setting up a group they called “the cartel” to manipulate a market valued at $5trn a day.

Lynch told a press conference that:

“The penalty these banks will now pay is fitting considering the long-running and egregious nature of their anticompetitive conduct. It is commensurate with the pervasive harm done.

And it should deter competitors in the future from chasing profits without regard to fairness, to the law, or to the public welfare,”

The new fines are a second wave of punishments for fixing forex markets. Six major banks were fined £2.6bn in November 2014. This takes the total penalties to £6.3bn.

Barclays, which was hit by the UK regulator’s biggest ever fine, will fire eight employees.

RBS has dismissed three staff, with two more suspended.

RBS chairman Philip Hampton siad:

We strongly condemn the actions of those responsible and regret the control failings that allowed such misconduct to take place.

Chat room information also showed that UBS staff had used finger gestures to conspire against clients.

UBS salesmen used elaborate internal system, involving hand signals and "hoots," to trick their customers. pic.twitter.com/2OL8uxMlTs

— David Enrich (@davidenrich) May 20, 2015

Shares in Barclays and RBS both rallied today after the fines were announced, as the markets welcomed the fact the fines weren’t bigger.

The Treasury said the scale of the fines showed that financial regulation is working.

The Labour opposition, though, called for a new review to clean up the City.

Here’s the full story, by Jill Treanor:

And here’s a Q&A explaining the scandal:

Updated

Despite the concerns about bank culture voiced today, several top bank executives have been playing the “bad apple” defence.

“The conduct of a small number of employees was unacceptable and we have taken appropriate disciplinary actions,” UBS Chief Executive Officer Sergio Ermotti and Chairman Axel Weber said in a statement.

JPMorgan said in a statement that the conduct underlying the antitrust charge against the bank is “principally attributable” to a single trader, who has since been dismissed.

“The conduct described in the government’s pleadings is a great disappointment to us,” said Chairman and CEO Jamie Dimon. “We demand and expect better of our people. The lesson here is that the conduct of a small group of employees, or of even a single employee, can reflect badly on all of us.”

Bank CEOs say all that currency rigging was just the work of a few bad apples. http://t.co/lRwPtmwTgI via @ZekeFaux and @maxabelson

— Joseph Weisenthal (@TheStalwart) May 20, 2015

Here’s a handy breakdown of all today’s fines, and the previous ones announced last November, from Sky News analyst Guy Harding:

FX fines. The definitive list. Today's fines shaded green. #forexscandal pic.twitter.com/6OD50jNxBx

— Guy Harding (@GuyHardingSky) May 20, 2015

[Incidentally, there are different ways of calculating the total , depending if you use today’s $/£ exchange rate or last November’s one]

Chris Leslie MP, Labour’s Shadow Chancellor, is alarmed that bank staff were conspiring to fix foreign exchange rates as late as 2013.

“Surely the time has come for fundamental reform and tougher penalties for banking misconduct.

“If ever there was an example of appalling collusion between bankers putting their own interests ahead of customers, then this is it.

“Ministers refused to act in 2012 when we pressed for broader regulation of financial benchmarks such as those in foreign exchange.

“We need to rebuild the reputation of British banking, which plays such a crucial role in our economy.”

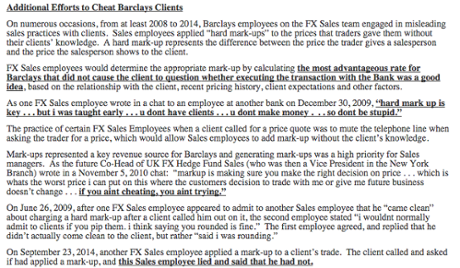

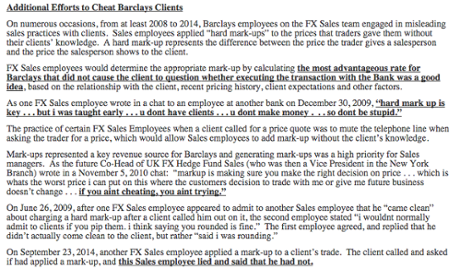

Benjamin M. Lawsky, the US Superintendent of Financial Services at the New York State Department (NYDFS), has issued a truly damning report into Barclays.

It explains how the bank conspired with rivals to trigger its clients stop-loss orders, in a “Heads I Win, Tails You Lose” approach to FX trading.

Lawsky adds bluntly:

Put simply, Barclays employees helped rig the foreign exchange market.

In one instance, a manager told his staff that their aim was to give customers the worst deal they could get away with. Another had a remarkable rallying cry: “if you ain’t cheating, you ain’t trying.”

For example:

NYDFS also explains how the collaboration between banks was crucial:

Without the active cooperation and coordination among the traders at multiple banks, via the use of chat rooms, the Barclays trader would have had neither the information to indicate that pushing the price was feasible, since there were not large contrary orders pending, nor the tools to attempt to accomplish that forced, temporary push lower.

Updated

David Hillman, spokesperson for the Robin Hood Tax campaign, argues that today’s “colossal” fines may not be enough to stamp out bad behaviour:

“It’s clear our softly softly approach to the finance industry isn’t working. Fines alone are not enough - much bolder action is needed to ensure banks work in our greater interest.”

Barclays and RBS shares rally

The London stock market just closed, with Barclays sitting proudly as the second-biggest riser on the FTSE 100 index, up almost 3.5%.

That means Barclays is worth £1.5bn more than this time yesterday, or almost exactly its total fines.

RBS was the fifth-best performer, up 1.7% - putting £715m on its value, rather more than it has been fined.

Barclays market cap up 3.4% or £1.5bn ( £1,482,099,765 ) as £1.5bn fine comes in below what was expected / provided for, which was £2.05bn

— Guy Harding (@GuyHardingSky) May 20, 2015

And Bank of America makes six....

Another bank has been fined today too -- Bank of America Merrill Lynch.

BAML has been hit with a $205m penalty by the Federal Reserve for “unsafe and unsound practices in the foreign-exchange market”.

The City must embrace a major cultural shift to avoid a repeat of the FX scandal, argues professor Mark Taylor, Dean of Warwick Business School.

He says:

Imposing heavy penalties - together with the accompanying adverse publicity - is one way of shifting that culture.

“This sort of practice strikes at the heart of business ethics and is yet another blow to the integrity of the banks. Our pension funds invest billions of pounds in the financial markets and if they are being cheated in this way it affects every one of us.

A bank’s culture is the responsibility of those at the top; Taylor wonders whether any senior executives will now resign.

Taylor is a former foreign exchange trader. He reckons that it could make sense to end the practice of taking a daily ‘fix’ of FX rates -- which proved a tempting target for some traders, so has experience of the market.

“Regulation of the forex markets would be very difficult, but one solution would be to take away the temptation to do this by taking the average over an hour - so 30 minutes either side of 4pm fix rather than 30 seconds. It’s a simple, workable solution because it would be a lot harder, if not impossible, to move a market as big as the FX market for an hour. Removing the incentive is much better than regulation because of the global, decentralised nature of the foreign exchange market.”

Cornell Law professor Robert Hockett says it’s significant that the banks have admitted guilt in criminal, not merely regulatory, investigations.

These are the first admissions of criminal guilt by large banking concerns in many, many years.

And with similar investigations into benchmark interest rate and precious metal price manipulation schemes still underway, there are likely to be more such to come.

Six banks get fined $6bn for fiddling exchange rates. Their shares go up $6.5bn as a result. So there's that.

— Stanley Pignal (@spignal) May 20, 2015

Shares in Barclays and UBS +3%, RBS +2% today. Markets clearly rattled and chastened by the FX rigging fines pic.twitter.com/pX2V0pKtey

— Jamie McGeever (@ReutersJamie) May 20, 2015

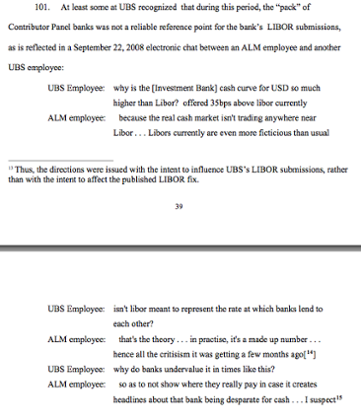

Today’s case also confirms that some traders knew very well in 2008 that the Libor rate (not to be confused with today’s FX fines) was being manipulated.

Here’s a snippet from its settlement with UBS, showing one newbie being brought up to speed by an old hand:

This really is shocking -- UBS staff were making gestures between each other to mark up the prices that they offered customers, in the hope of making illicit profits.

UBS salesmen used elaborate internal system, involving hand signals and "hoots," to trick their customers. pic.twitter.com/2OL8uxMlTs

— David Enrich (@davidenrich) May 20, 2015

Literally giving two fingers to their own clients....

Updated

Wall Street is also taking today’s fines in its stride:

Stock prices of today's punished banks either rose or were basically flat. http://t.co/OA3lNIPcmx pic.twitter.com/jgoa9rPClC

— David Enrich (@davidenrich) May 20, 2015

Here’s the press release from the Department of Justice:

Five Major Banks Agree to Parent-Level Guilty Pleas

It includes links to the five separate pleas, from Barclays, Royal Bank of Scotland, JP Morgan, Citigroup and UBS.

It also includes this stinging rebuke, from Assistant Attorney General Bill Baer:

The charged conspiracy fixed the U.S. dollar – euro exchange rate, affecting currencies that are at the heart of international commerce and undermining the integrity and the competitiveness of foreign currency exchange markets which account for hundreds of billions of dollars worth of transactions every day.

“The seriousness of the crime warrants the parent-level guilty pleas by Citicorp, Barclays, JPMorgan and RBS.”

Lynch: Banks showed "Breathtaking flagrancy" Er. Yer. http://t.co/zj6dtBkwgJ pic.twitter.com/ZGpVbQ4QSc

— dominic rushe (@dominicru) May 20, 2015

DoJ: Banks guilty of breathtaking flagrancy

US attorney general Loretta Lynch has said the banks were guilty of “breathtaking flagrancy”, at a press conference taking place now.

Lynch said the Department of Justice was still investigating the cartel and declined to comment on whether individuals would eventually be charged.

The investigation entailed the assessment of 680,000 pages of financial documents and a terabyte of complex bank trading data/. The issues were “so systemic” that prosecutors said the parent companies had to be sanctioned at the highest levels.

Updated

Today’s fines are proof that the City is being regulated properly, according to The Treasury.

A spokesman says:

“The integrity of the City matters to the economy of Britain, which is why the government took action to deal with the abuses and unacceptable behaviour by implementing the key recommendations of the Parliamentary Commission on Banking Standards and setting up the Fair and Effective Markets Review, to ensure that Britain’s financial markets are working as they should and similar scandals cannot happen again.”

Shares in Royal Bank of Scotland have risen by 2%. It says that today’s fines are fully covered in existing provisions.

So, like Barclays, there is relief that the penalties aren’t worse.

Updated

Barclays’ share price has jumped by 3%!

That’s not the reaction you might expect, given the bank has been fined a record £284m by UK regulators and chastised over its failings.

But it makes sense - Barclays had set aside more in provisions than it’s actually being fined by global regulators. This could free up £500m in spare cash....

BARC Fined £1.534m but already made provisions of £2.05bn. £500m write-back for Q2?

— Mike van Dulken (@Accendo_Mike) May 20, 2015

Updated

The FX market is huge, with over $5 trillion of currency deals taking place each day.

And today’s evidence shows that traders didn’t always succeed in rigging the rate at which currencies were changing hands.

On one occasion, a Barclays trader spent £10m trying to drive the pound higher, and trigger a client’s stop-loss order, only to see the attempt fizzle out and leave them nursing a loss.

I. Love. Transcripts. http://t.co/30y6nCZm49 #fooooooooooookkkkk pic.twitter.com/C5Z5nDJAHY

— Katie Martin (@katie_martin_fx) May 20, 2015

This is the second time that regulators have announced fines over the Forex-rigging scandal. They take the total penalties up to $10bn.

A big number, but one that is dwarfed by the profits of the banks involved:

Total fines for 7 banks in global FX scandal = $10 bln Total net profit of those 7 banks from 2013 to now = $132 bln

— Jamie McGeever (@ReutersJamie) May 20, 2015

RBS fires three staff over FX scandal

Royal Bank of Scotland has dismissed three employees, and suspended two more, following its role in the manipulation of the foreign exchange markets.

Philip Hampton, chairman of the bank - bailed out by the UK taxpayer in 2009 - says it fully accepts today’s penalties.

Hampton added:

We strongly condemn the actions of those responsible and regret the control failings that allowed such misconduct to take place.

“This episode has exposed serious shortcomings at both individual and collective levels from which we continue to learn. As part of this effort we are committed to implementing further improvements to systems and controls.

RBS is paying $395 million to the DoJ and $274 million to the Federal Reserve to resolve the investigations.

Updated

As well as fining Barclays a record £284m, the FCA is damning about the conduct of the traders who rigged the foreign exchange rates.

It says they formed secret groups with names such as “The Three Musketeers” -- and actually tried to trigger their clients’ own stop-loss orders; costing their clients money, but making money for the traders.

Barclays engaged in collusive behaviour in which traders from different banks, including Barclays, formed tight knit groups and communicated through electronic messaging systems including chat rooms. Certain groups described themselves or were described by others using phrases such as“the players” – one chat room participant referred to himself and others in the chat room as “the 3 musketeers” and commented “we all die together”.

The information obtained through these groups helped traders determine their trading strategies. They then attempted to manipulate fix rates and trigger client “stop loss” orders (which are designed to limit the losses a client could face if exposed to adverse currency rate movements).

This involved traders attempting to manipulate the relevant currency rate in the market, for example, to ensure that the rate at which the bank had agreed to sell a particular currency to its clients was higher than the average rate at which it had bought that currency in the market to ensure a profit for Barclays.

Barclays hit with biggest ever UK fine

Today’s fines include the biggest ever penalty imposed by Britain’s financial watchdog, £284m, against Barclays.

The Financial Conduct Authority says Barclays failed to control its foreign-exchange trading operations properly. This means its traders could collude with employees at rival banks, to share market-sensitive information.

The scale of the wrong-doing undermined confidence in the UK financial system and putting its integrity at risk.

Georgina Philippou, the FCA’s acting director of enforcement and market oversight, says::

“This is another example of a firm allowing unacceptable practices to flourish on the trading floor. Instead of addressing the obvious risks associated with its business Barclays allowed a culture to develop which put the firm’s interests ahead of those of its clients and which undermined the reputation and integrity of the UK financial system.

Firms should scrutinise their own systems and cultures to ensure that they make good on their promises to deliver change.”

Updated

Five banks fined over foreign exchange scandal

BREAKING: Barclays, JP Morgan, Citigroup, Royal Bank of Scotland and UBS have been fined a total of $5.7bn for their role in manipulating the foreign exchange markets.

Barclays will also fire eight people, as part of a deal with regulators.

Here are the snaps from Reuters:

- FIVE BANKS TO PAY ABOUT $5.7 BLN IN FOREX SETTLEMENT WITH AUTHORITIES – U.S. DEPT OF JUSTICE

- JPMORGAN, CITIGROUP, ROYAL BANK OF SCOTLAND, BARCLAYS TO PLEAD GUILTY TO CRIMINAL CHARGES OVER FOREX RIGGING – US DOJ

- UBS PLEADS GUILTY TO CRIMINAL CHARGE OVER LIBOR RATE MANIPULATION - DOJ

- JPMORGAN TO PAY JUSTICE DEPARTMENT $550 MLN, CITIGROUP $925 MLN IN CRIMINAL FINES - DOJ

- ROYAL BANK OF SCOTLAND TO PAY $395 MLN CRIMINAL FINE, BARCLAYS $650 MILLION IN CRIMINAL FINE ALONE OVER FOREX

- UBS TO PAY $203 MLN CRIMINAL PENALTY OVER LIBOR – DOJ

- FIVE BANKS ALSO TO PAY FINES OF OVER $1.6 BILLION TO U.S. FEDERAL RESERVE - DOJ

- FEDERAL RESERVE SEPARATELY FINES BANK OF AMERICA $205 MILLION OVER FOREX

- BARCLAYS SETTLES RELATED CLAIMS WITH NEW YORK REGULATOR, CFTC AND UK REGULATOR FCA FOR ADDITIONAL $1.3 BILLION PENALTY - DOJ

- BARCLAYS ALSO TO FIRE 8 EMPLOYEES OVER FOREX MISCONDUCT IN DEAL WITH NEW YORK REGULATOR

- BARCLAYS’ OVERALL FINES TOTAL $2.4 BILLION - NEW YORK BANKING REGULATOR

Updated

Our City editor, Jill Treanor, has helpfully written a Q&A about the forex scandal, to help explain today’s fines.

And here it is:

What are the foreign exchange markets?

Each day, £3.5tn changes hands in the foreign exchange markets. Each week, the equivalent of a year’s global trade in physical goods takes place. The markets are open 24 hours a day, although 40% of the activity takes place in London. This is because of the city’s central position in time zones. Hong Kong dealers pass their trading to London, which in turn transfers to New York before slipping back to the Asian time zone.

Where does it trade?

There is no equivalent of a stock exchange for currencies. Dealers trade between each other, and prices flash up on trading terminals in a wide range of currencies. A price of any currency has to be set against another, say the pound, and they are known as pairs. The most commonly traded pairs are the euro against the dollar, the dollar against the yen, and sterling against the dollar.

Many of them have nicknames. “Cable” is sterling-dollar because of cable laid under the Atlantic ocean in 1858 to improve communications between the US and the UK. The “loonie” is the Canadian dollar, named after the bird.

Such is the size of the market, dealers trade in millions, and often billions (known as yards).

Why does it matter?

The prices of currencies have an impact on everyone, from holidaymakers to companies manufacturing cars or selling clothes.

How did the traders rig it?

As the markets never close, there is no single closing price in the currency markets. But when the Financial Conduct Authority fined five banks in November 2014, it outlined two points in the day – at 1.15pm and 4pm – when the prices for currencies are “fixed”. Most of the focus has been on the 4pm fix which is set on the basis of a 60-second trading period each side of the hour.

Customers give banks orders to trade at 4pm and if banks know the trading positions of their rivals they are able to work out at what price the “fix” will take place. Through chatrooms, traders shared information about their client orders and were able to influence the price.

The FCA found the traders at rival banks formed groups through which they shared information and referred to their teams using names like “the players”, “the 3 musketeers”, “1 team, 1 dream”, “a co-operative” and “the A-team”.

Is this like the Libor scandal?

To a certain extent. The interest rate rigging scandal increased scrutiny on other markets, although the process of manipulation was different.

Libor was set using estimates submitted by banks about what rate of interest they expected to be charged for borrowing. The currency fixes are based on actual trades.

Preamble: FX fines due very soon

OK. Financial regulators are about to announce fines against some of the world’s largest banks, over their role in the foreign exchange-rigging scandal.

We believe thats several banks will be penalised, with fines possibly running to £3bn. They could also plead guilty to offences relating to manipulating foreign exchange markets.

As Bloomberg’s Max Colchester tweeted earlier, we’re probably also going to receive transcripts of conversations between traders, discussing their activities.

So, roughly one hour to go before we get the latest installment of "dumb things traders said on chat" #fx

— Max Colchester (@MaximColch) May 20, 2015

Summary: Capital control fears grow

Time for a recap of the main Greek developments today.

Concern is growing that Greece will miss its next repayment to the International Monetary Fund, triggering a new phase of the crisis.

With fellow spokesman Thanassis Petrakos reiterating this point, it’s clear that Greece has barely two weeks to get a deal.

Fears over Greece have knocked the euro today, and left Europe’s financial markets nervous.

Euro slides as Greek spokesman warns June 5 will be "the moment of truth" http://t.co/MbynMbkYw5 pic.twitter.com/z1ari6WWP8” #morningjoe #tcot

— jaazee (@jaazee1) May 20, 2015

Moody’s added to the gloom, warning that there is a high risk that capital controls could be imposed in Greece, meaning bank accounts could be frozen.

Lawyers fear that Greece could be plunged into chaos if it missed an IMF payment, potentially triggering a default and possibly leading to a parallel currency.

Anti-austerity protesters have marched through Athens; it began with pensioners, and was followed by healthcare workers.

The European Central Bank has been deliberating whether to continue providing emergency liquidity to the Greek banking sector. We expect a decision later today. According to Bloomberg, Athens has asked for more help:

#Greece’s c-bank to ask #ECB for increase of 1.1 bln euro to emergency funding it can provide to banks @business says http://t.co/mKqNxdZunq

— cep (@CEP_EU) May 20, 2015

The New York Times has run a long profile of Greek finance minister Yanis Varoufakis, in which he says he would rather resign than accept a deal that extends Greece’s misery.

And here’s Larry Elliott’s news story, with all the latest details:

Updated

A group of protesters have broken into the Athens headquarters of Allianz, the German financial services group, according to Greek newspaper Enikos.

They say:

According to reports the demonstrators, without using violence, asked all employees to leave the building.

Leftists occupy #Allianz’s #Athens headquarters Greece- http://t.co/G3moin8uEl pic.twitter.com/lXvVW2mH1B

— enikos_en (@enikos_en) May 20, 2015

Updated

Health workers have now marched through Athens, to mark a 24-hour strike calling for more funding and extra staff for the sector.

Over in Athens, the speaker of the Greek parliament has gone toe-to-toe with police officers, insisting they stop restricting today’s anti-austerity protesters [see earlier photos]

#Syriza House Speaker Konstantopoulou demanding from the police to open the road for marching of protesters. #Greece https://t.co/J3WLJGEXua

— The Greek Analyst (@GreekAnalyst) May 20, 2015

Greece would enter a legal minefield if it were to default on its IMF repayments, as it is now threatening.

Benedict James, a partner at law firm Linklaters, explains:

“With a number of repayment deadlines for Greece in the coming weeks, if a bailout package isn’t agreed, the government seems likely to run progressively out of euros. This may lead to the imposition of capital controls and issuance of government IOUs as a sort of quasi-currency (as happened in Argentina and California).

That may or may not be a precursor to a full exit of the euro.

The legality of capital controls is complicated under the EU treaties and the IMF framework, the imposition of a quasi-currency may be in breach of the eurozone rules, and there is no mechanics in the relevant EU treaties for a legal departure from the eurozone. This would all therefore be a highly complex legal situation, both for the relevant countries, and for businesses and financiers trying to work out whether their contracts are enforceable, and if so in what currency.”

When we profiled Yanis Varoufakis in February, Greece’s new finance minister told us that “If I weren’t scared, I’d be awfully dangerous.”

Today’s NYT profile shows that he’s now even more worried about the situation.

Updated

Reuters is reporting that Greece has suggested bringing in a transaction tax on bank customers:

- GREEK GOVERNMENT HAS PROPOSED IMPOSING A BANKING TRANSACTION TAX IN TALKS WITH EU/IMF LENDERS - SOURCES

There were reports earlier this month that Greece could impose a small levy when people accessed their accounts, to deter a bank run and to raise funds.

NYT publishes profile of Yanis Varoufakis

The New York Times has just published a profile of Yanis Varoufakis today, which gives a detailed, sympathetic picture of the challenges facing Greece’s finance minister.

I think it’s appearing in next Saturday’s NYT magazine; but we can read it now.

Here’s a flavour:

Imagine that President Obama had, instead of picking Timothy Geithner to be his Treasury secretary in the midst of the financial crisis, appointed a progressive academic economist like Paul Krugman or Joseph Stiglitz, only edgier and funnier, someone who had spoken out scathingly against bank bailouts, freely expressing himself however he wanted on television and in public debates because he wasn’t running for office....

NYT: Tsipras' appointing Varoufakis as a Greek Finance Minister is like Obama appointing Stiglitz or Krugman. http://t.co/Nv5vGWEJc5

— Joseph Stiglitz (@stiglitzian) May 20, 2015

The interview begins with Varoufakis showing frustration with his European colleagues over their refusal to cut a new deal:

The Greek finance minister had just returned to Athens from a hopscotch tour of European capitals, during which he warned his fellow European leaders that they faced a Continental crisis: If they didn’t lend money to his ailing country soon, Greece might end up forced to leave the eurozone. And yet Greece wouldn’t accept many of the conditions they were demanding in return. He sounded angry. “I’ll be damned if I will accept another package of economic policies that perpetuate this same crisis. This is not what I was elected for.”

He would resign, he said, rather than push the Greek people deeper into economic despair: “It’s not good for Europe, and it’s not good for Greece.”

And the Marxist professor (surprisingly?) even compared his challenge to Conservative PM Margaret Thatcher:

From the European point of view, Greece has no right at all to argue about reforms, so utterly did previous governments, after torpedoing their own economy, fail to implement them over the past five years. But Varoufakis and Syriza regard their election as a sort of “Day Zero” for Greece. “We are the guys who spent all our lives in Syntagma Square outside my office protesting what the people inside my office were doing,” Varoufakis said. “We were being bombarded with gas, because we didn’t see how we could repay a loan under the circumstances.”

He compared himself to Margaret Thatcher, elected in 1979 in opposition to the welfare state. “How intelligent is it to blame Margaret Thatcher for the postwar corporatism that came before her?” he asked. “Not much. So what we have here is a serious case of deeply rooted racism that all Greeks are the same, that whether or not they protested the bailout, they are still responsible for it.”

Worth a read:

A Finance Minister Fit for a Greek Tragedy?

Greek PM could face left-wing mutiny

Over in Athens there is mounting speculation that prime minister Alexis Tsipras is struggling to control his increasingly fractious far left Syriza party.

Helena Smith reports

There are growing suggestions in Athens this morning that Alexis Tsipras may soon be dealing with a full-scale mutiny within the ranks of his radical left party.

Last night, John Milios, the party’s chief economist who played a leading role in drawing up Syriza’s manifesto, spoke excoriatingly of the concessions the government was now making to strike a deal with lenders.

“We have to help Syriza stay with its pre-election commitments,” he told a gathering of leftist dissidents in Athens before exerting heavy criticism of the strategy pursued by finance minister Yanis Varoufakis.

“The party can’t have its feet in two boats.”

Default, he added, would be preferable and would not have any bearing on Greece’s place in the euro zone.

Tsipras was forced to address his parliamentary group for over five hours yesterday with increasingly divisive MPs arguing that a split from the eurozone, and a return to the drachma, would be infinitely more sensible than years of “dead-end austerity.”

The infighting is such that even if a deal is eventually reached with creditors there are real – and growing questions - over the ability of the government to enforce it.

“If he can’t get it through [parliament], and his people don’t vote for it, we will have a serious crisis,” the New Democracy MP Anna Assimakopoulou told me.

“Failure to support it will bring up questions of implementation and the stability of the political system. I don’t think lenders are going to give up money if they think the government is going to fall,” added Assimakopoulou, a shadow finance minister for the main opposition New Democracy.

“The big question is can Tsipras strike a deal inside his own party when so many are now speaking openly about the benefits of going back to the drachma? Personally, I seriously doubt that they can find an internal, workable compromise.”

Syriza’s militant Left Platform, lead by energy minister Panagiotis Lafazanis, has also been racheting up the pressure.

On Tuesday, the radicals’ news portal, ISKRA, lashed out at the concessions being made in a story headlined “lenders are preparing plans for the unprecedented submission of the country.”

“They are preparing ultimatums of the kind “take it or leave it,” it said, adding that the debt-stricken country was being economically asphyxiated to force its hand.

It added:

“An agreement with the “institutions will either comply with the government’s programme or it can’t happen, and it that case it won’t happen.”

Updated

Moody's: Risk of Greek capital controls has risen

The risk of Greece freezing bank accounts and imposing restrictions on the movement of money has “materially increased” in the last few weeks, rating agency Moody’s has just warned.

Moody’s fears that the outlook for the Greek banking sector is “negative”, due to the “significant deterioration in banks’ funding and liquidity”.

Moody’s says:

The outlook for the Greek banking system is negative, primarily reflecting the acute deterioration in Greek banks’ funding and liquidity, says Moody’s Investors Service in a new report published recently.

These pressures are unlikely to ease over the next 12-18 months and there is a high likelihood of an imposition of capital controls and a deposit freeze.

They also warns that Greece’s banks will remain dependent on central bank help for some time:

Moody’s notes that significant deposit outflows of more than €30 billion since December 2014 have increased banks’ dependence on central bank funding. In our view, the banks are likely to remain highly dependent on central bank funding, as ongoing uncertainty regarding Greece’s support programme continues to compromise depositors’ confidence.

*MOODY'S: PRESSURES ON GREEK BANKING UNLIKELY TO EASE 12-18 MOS

— Michael Hewson (@mhewson_CMC) May 20, 2015

Updated

Greek finance minister Yanis Varoufakis has now published a transcript of his interview with Die Zeit (see earlier post).

It shows Varoufakis described Wolfgang Schauble as a “legendary” figure...although one whose view of the crisis should be challenged.

And although he does believe the German finance minister makes mistakes, Varoufakis had the grace to admit the feeling is mutual.

1. If you would explain to a teenager, maybe your own daughter, what your relationship to the German Finance Minister Wolfgang Schäuble looks like – what would you tell her?

YV: I would tell my daughter that it is, from my perspective, a multi-layered relationship. There is a sense of awe that I feel from meeting with a legendary figure whose work I have been following critically for decades. Then there is a strong urge to counter his overarching approach to common problems regarding Europe. Additionally, there is some frustration at not having the opportunity to discuss in a different setting; to stage these meetings in a proper federal, democratic context in which arguments, rather than relative power, would play a more prominent role.

2. What are the European topics you probably could agree on with Mr Schäuble?

YV: That Europe needs a political union and that, without it, our monetary union is problematic.

3. Do you think Mr Schäuble makes mistakes in his analysis of the Greek situation? If yes, which ones?

YV: Yes I do (as I am sure he thinks that I err in my analysis). Primarily, he associates past Greek governments with the Greek people; as if the former reflect the character of the latter. And he does not appreciate how helpful it would be for mainstream Northern Europe to find a modus vivendi with a movement (like SYRIZA in Greece) which may be very critical of European institutions but which is profoundly pro-European and eager to help bring Europe closer together.

My answers (verbatim) to Die Zeit on Dr Schäuble http://t.co/l4kOBFGqhT

— Yanis Varoufakis (@yanisvaroufakis) May 20, 2015

Updated

Investors just paid for the privilege of lending money to Portugal, suggesting investors aren’t panicking about an anti-austerity government winning power this autumn.

The Lisbon debt agency just sold €300m of six-month Treasury bills at an average yield of -.002%.

That means buyers will make a tiny loss when the bonds mature in November -- unless they manage to sell them to the European Central Bank’s QE programme, of course.

Portugal joining the party. *PORTUGAL SELLS 6-MONTH BILLS AT NEGATIVE YIELD FOR 1ST TIME

— Frederik Ducrozet (@fwred) May 20, 2015

Portugal sells 6 month T-Bills at a negative yield. Is this the same Portugal that might be electing an anti austerity gov't in October?

— Michael Hewson (@mhewson_CMC) May 20, 2015

In another sign of rising tensions, Greek pensioners are holding an anti-austerity protest in Athens, against cuts to welfare and healthcare.

The demonstration, which looks peaceful, could be a taste of what’s to come if Greece is forced to implement more cutbacks by its lenders.

Varoufakis: Schäuble make mistakes, and it's frustrating

Greek finance minister Yanis Varoufakis has apparently told a German newspaper that his counterpart, Wolfgang Schäuble, makes mistakes in his analysis of Greece.

Reuters reports:

The left-wing economist, asked by Die Zeit in excerpts of an interview to be published on Thursday whether the conservative finance German minister commits such mistakes, answered: “Yes, he does.”

Varoufakis added:

“It is frustrating that we are not able to speak with each other in a context where arguments count more than relative power.”

That’s the difference between politics and academia, I guess.

It’s not clear which particularly errors Varoufakis has in mind. These comments may not improve relations between Athens and Berlin at this critical time.

In case a Greek deal wasn't hard enough @yanisvaroufakis gives interview: *SCHAEUBLE'S ANALYSIS OF GREECE IS FLAWED, VAROUFAKIS TELLS ZEIT

— HansNichols (@HansNichols) May 20, 2015

This @yanisvaroufakis interview with Die Zeit is something else. Quite personal. *VAROUFAKIS SAYS SCHAEUBLE EMPHASIZING POWER OVER ARGUMENT:

— HansNichols (@HansNichols) May 20, 2015

Updated

A second Greek government representative has now declared that Athens will miss its €305m repayment to the IMF early next month, unless a deal is reached.

Thanassis Petrakos, Syriza’s parliamentary spokesman, echoed Nikos Filis’s comments this morning, on Star TV.

Petrakos also argued that Greece wouldn’t suffer if it failed to pay up, according to Twitter user The Greek Analyst who tweeted the key points:

Both parliamentary spokesmen of #Syriza, Filis & Petrakos, repeated this morning (different shows) that govt might actually not pay IMF.

— The Greek Analyst (@GreekAnalyst) May 20, 2015

#Syriza spox Petrakos replies: "What can happen to us [if we don't pay the IMF]? Nothing is going to happen to us!" #Greece

— The Greek Analyst (@GreekAnalyst) May 20, 2015

These. People. Are. Dangerously. Foolish. #Greece

— The Greek Analyst (@GreekAnalyst) May 20, 2015

Updated

Britain’s central bank can’t agree whether wage are going to rise strongly, or not.

This is the key bit of the MPC minutes. Pay growth & inflation might pick up quickly... Or they might not... pic.twitter.com/8FyR96ZeQW

— Duncan Weldon (@DuncanWeldon) May 20, 2015

The Bank of England also believes UK economic growth will accelerate this quarter, after slowing to just 0.3% in the first three months of 2015.

The minutes say:

The Committee judged that GDP growth would pick up in Q2 to close to its historical average rate, supported by the boost to real incomes from the fall in food, energy and other import prices, and would continue to grow at, or just a little below, historical average rates throughout the forecast period.

Bank of England minutes released

The Bank of England’s monetary policy committee was unanimous in voting to leave interest rates unchanged this month, according to the minutes of the meeting which were just released.

However, the decision of whether to hold or raise Bank Rate was “finely balanced” for two MPC members.

That’s probably Martin Weale and Ian McCafferty, who recently stopped voting for a rate rise once they realised that inflation was falling really quite sharply (to -0.1% last month).

The minutes also show that the MPC is confident that borrowing costs will rise in the medium term, having been pegged at 0.5% since March 2009:

While there was a range of views over the most likely future path for Bank Rate, all members agreed that it was more likely than not that Bank Rate would rise over the three-year forecast period.

Minutes of the MPC Meeting held on 7 and 8 May http://t.co/23rf87VcTR

— Bank of England (@bankofengland) May 20, 2015

Updated

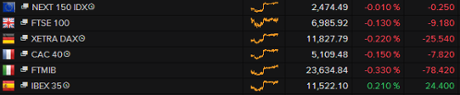

Europe’s stock markets are rather becalmed this morning, as the Greek crisis continues to worry traders.

Most of the major indices are slightly in the red:

The Athens stock market has also dipped, down 0.2% in early trading.

Stan Shamu of IG says:

Unfortunately Greece remained a thorn with no positive developments and reduced expectations of a swift solution.

In London, Burberry’s share have slid 4% after the fashion chain cut its profit forecasts for 2016 and blamed currency fluctuations.

It was a better day in Japan, where the Nikkei touched a 15-year high. That followed the news that the Japanese economy grew by 0.6% in the last quarter (an annualised rate of 2.4%). That beat expectations, and also outperformed the US, the UK and the eurozone.

Moscovici: Still big gaps to close with Greece

We’re making progress with Greece, but we’re not there yet.

That’s the message from Pierre Moscovici, European commissioner for Economic and Monetary Affairs, this morning.

Speaking in Paris a few moments ago, Moscovici said that negotiations are advancing, but they need to accelerate.

Worryingly, he also warns that pensions and labour market issues remain unresolved -- those are the red lines which Greece is sticking to.

- EU’S MOSCOVICI SAYS TALKS OVER GREECE HAVE PRODUCED MORE RESULTS OVER THE PAST THREE WEEKS THAN THE PREVIOUS MONTHS

- EU’S MOSCOVICI SAYS THERE IS IMPORTANT PROGRESS ON GREECE BUT WE ARE NOT THERE YET, STILL BIG GAPS ON PENSION AND LABOUR ISSUES

- EU’S MOSCOVICI SAYS WE MUST ACCELERATE TALKS ON GREECE, NEED TO REACH DEAL IN NEXT FEW WEEKS, IT’S POSSIBLE TO DO IT

- EU’S MOSCOVICI SAYS THERE IS NO PLAN B ON GREECE, MUST STAY IN EURO ZONE

Greece’s governing Syriza party has called a rally in Paris tonight, to show support for Athens in its battle with its creditors.

The event, at 18:30 in Republic Square, will call on Greece’s lenders to respect its “red lines”; the promises on pensions and labour market reforms, ahead of an EU summit tomorrow in Riga, Latvia.

That summit meeting will be “a decisive meeting in the political confrontation between austerity and social justice, between neo-liberalism and democracy in Europe”, they say. More details here.

SYRIZA calls for a "Avec les Grecs" (together with Greeks) rally today in Paris, #France in place de la République. http://t.co/ts36jIYoOS

— spyros gkelis (@northaura) May 20, 2015

It seems that SYRIZA is trying to re-ignite people's support across Europe in head of the #eurogroup negotiation #greece #previoustweet

— spyros gkelis (@northaura) May 20, 2015

Investors are bracing for Greece to miss its €305m repayment to the IMF on June 5, says Mike van Dulken of Accendo Markets.

In Europe this morning indications are that, while there has been progress in negotiations, Greece will miss its June debt payment to the IMF unless a deal is reached by the end of May.

Concessions for Greece are highly unlikely - the EU will almost certainly face a second revolt in the form of Portugal’s ascendant socialists if any are afforded to Athens.

Portugal holds a general election this autumn, and opinion polls show the opposition Socialists holding a small lead. Their leader, Antonio Costa, has vowed to reverse the austerity measures imposed since its 2011 bailout, suggesting the eurozone crisis could flare again soon.....

The foreign-exchange rigging scandal took another twist this morning.

Swiss bank UBS revealed it had dodged being prosecuted by the US Department of Justice...because it blew the whistle that traders had been conspiring to fix the rates at which currencies were changing hands.

Other banks could be hit with big fines today, as City editor Jill Treanor explains:

The announcement from UBS signals that the US DoJ is preparing to impose punishments on other banks – including Barclays and bailed-out Royal Bank of Scotland – as soon as Wednesday. Barclays is also awaiting punishment from the FCA and has already prepared the ground for penalties of as much as £2bn.

The punishments, also expected on two US banks, could result in total penalties of over £3bn and require the banks to plead guilty to offences relating to manipulating foreign exchange markets – a sanction rarely imposed by the DoJ

The euro fell sharply following the warning that Greece could miss its repayment to the IMF on June 5.

It hit a two week low against the US dollar at $1.107.

Updated

Greece will prioritise pensions and wages rather than repaying the IMF, if creditors don’t unlock some of the €7.2bn in outstanding bailout funds, added Nikos Filis.

“There is no money for the foreign (lenders) when they have not given us any funds for a year...We don’t have it to make the payment and this is part of the discussion.”

Greece: No IMF repayment without a deal

The Greek government has warned that it will miss its next repayment to the International Monetary Fund unless a deal is reached soon.

Nikos Filis, the government’s parliamentary speaker, raised the stakes in its negotiations with its lenders this morning.

He told the ANT1 TV station that the IMF won’t get the €305m due in a fortnight’s time, unless creditors have unlocked some bailout funds.

“Now is the moment that negotiations are coming to a head. Now is the moment of truth, on June 5.

“If there is no deal by then that will address the current funding problem, they won’t get any money.”

(thanks to Reuters for the quotes)

Filis’s comments could reverberate around the European Central Bank’s HQ in Frankfurt, as the governing council meets to discuss the crisis.

GREECE WILL NOT MAKE JUNE 5 IMF LOAN REPAYMENT IF NO DEAL WITH LENDERS IS REACHED BY THEN- GOVT PARLIAMENTARY SPEAKER - RTRS

— econhedge (@econhedge) May 20, 2015

This echo a warning from Greece’s Labour minister Panos Skourletis. As we covered in Tuesday’s liveblog, Skourletis warned that “things will be difficult” if Greece hits June without a deal.

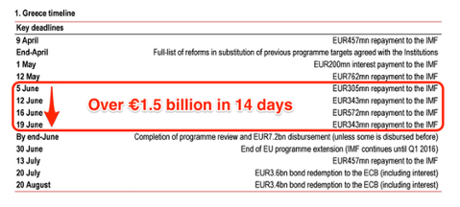

A glance at Greece’s repayment schedule confirms that June will be very sticky unless the two sides have reached agreement....

The Agenda: ECB to discuss Greek support today

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

The European Central Bank will hold the fate of Greece’s banking system in its hands today.

The 25 members of the ECB’s governing council will discuss whether to keep pumping emergency liquidity into Greek banks to keep them afloat. They might decide to impose a higher haircut on the assets provided by the Bank of Greece in return for this support.

According to the Financial Times, this is a serious possibility:

It is possible that two thirds of the council will support the move as soon as the Wednesday vote.

The haircuts were lowered last year after Greece returned to capital markets. The council is considering returning to the levels applied before the reduction, according to two people familiar with the matter.

This would lower the level of collateral held by Greek banks eligible for emergency loans from €95bn to €88bn and is viewed by insiders as a relatively incremental shift.

At the moment, Greek banks can access €80bn of liquidity.

The ECB could even cut the emergency liquidity scheme off altogether, if it reckons Greece simply poses too much risk to the rest of the eurosystem.

That would be the nuclear option, though, and take the central bank even further into political considerations. Does it really want to be responsible for the break-up of the single currency?

The decision is expected this afternoon.

ECB ensnared in politics as it faces vote on Bank of Greece loans: http://t.co/PH8k3ORqmS #FT

— AnneSylvaineChassany (@ChassNews) May 20, 2015

Also coming up today...

Some of the world’s biggest banks are expected to be fined billions of dollars, and face criminal charges, over the foreign-exchange rate rigging scandal.

In the City, investors will be digesting results from high street stalwart Marks & Spencer, fashion chain Burberry and travel firm Thomas Cook.

And we get minutes of the last meeting of the Bank of England at 9.30am BST, and then the Federal Reserve tonight (7pm BST).