Closing summary

Before we close up, here is a summary of the day’s main events.

- Greece has vowed to meet Thursday’s debt repayment deadline. It is scheduled to pay the IMF €450m (£330m)

- The UK services sector was booming in March according to the latest PMI survey, potentially handing George Osborne a pre-election advantage

- Greek PM Alexis Tsipras is hoping to agree a three-year plan of action when he meets Putin in Moscow on Wednesday, officials said.

That’s all for today. Thank you for reading and commenting and please join us again tomorrow on a key day for Greece, as Alexis Tsipras heads to Moscow to meet Vladimir Putin. AM

European markets have also built on earlier gains, boosted by a strong set of PMI surveys from the UK and eurozone this morning.

- FTSE 100: +1.6% at 6,944.39

- Germany’s DAX: +1.1% at 12,104.24

- France’s CAC: +1.5% at 5,150.27

- Italy’s FTSE MIB: +1.6% at 23,673.18

- Spain’s IBEX: +1% at 11,745.2

US markets open higher

US markets have opened up.

- Dow Jones: +0.4% at 17,945.48

- S&P 500: +0.3% at 2,086.28

- Nasdaq: +0.3% at 4,365.08

IMF: governments must do more to stimulate growth

The International Monetary Fund has published part of its spring outlook this afternoon, ahead of the full publication next week.

It says t world’s major economies risk a long period of low growth unless governments do more to overcome the after-effects of the financial crisis and the longer term problem of ageing populations.

The Guardian’s economics correspondent Phillip Inman reports:

Highlighting Germany, Canada and Japan as three of the worst affected countries, the IMF said that only by adopting a list of policy reforms that include greater spending on research and development, infrastructure projects and workers’ skills could potential output be raised to nearer levels seen before the 2008 crash.

It said governments should also consider action that also includes “better designed tax and expenditure policies to boost labour force participation, particularly for women and older workers”.

Looking forward, the IMF said potential growth in advanced economies was expected to increase slightly from an average of about 1.3% a year in the last six years to 1.6% until 2020, but not reach the 2.25% average seen between 2001 and 2007.

Germany: we want to help Greece but it's not clear how

Germany’s economy minister has said his country is ready to help Greece and stay within the eurozone but it wasn’t clear how Germany could help further.

Speaking at the economy ministry in Berlin, Sigmar Gabriel said:

This country is ready to help Greece get back on its feet - moreover in my firm opinion in the euro and not outside the euro.

How one can do that, does still not appear to me to be very clear.

He also criticised Greece’s claim that it is owed €279bn by Germany in war reparations, saying it had nothing to do with negotiations on Greece’s current debt crisis.

#Greece a lot of wary western diplomats in Athens on eve of #AlexisTsipras visit to the kremlin for talks with #vladimirputin

— Helena Smith (@HelenaSmithGDN) April 7, 2015

Syriza: meeting with Russia will be 'politically friendly'

Helena Smith, the Guardian’s correspondent in Athens, has more details on the agenda for the Moscow meeting between Putin and Tsipras on Wednesday.

Helena reports:

The Greek government has announced that prime minister Alexis Tsipras will fly to Moscow, accompanied by a delegation of officials, at 4pm today.

The far-left leader will meet president Vladimir Putin at 1pm local time, followed by a working lunch between the two men at 2pm.

“The signing of documents takes place at 3:15pm,” a government statement said.

Senior officials are saying that “a three-year plan of action” in the fields of economy, commerce, research and technology are among the accords that are likely to be signed.

A press conference by both leaders will be held at 3:30pm.Senior Syriza insiders are describing the visit as “diplomatically defined, politically friendly and economically promising”.

“The Greek prime minister will go wherever it is beneficial for Greece,” one official was quoted as saying today.

Updated

Greece: IMF willing to show 'utmost flexibility'

The Greek finance ministry has given a few more details following Yanis Varoufakis’s meeting with IMF boss in Washington.

Apparently Lagarde told the Greek finance minister the IMF was willing to be flexible over Greek reform proposals.

The ministry said:

Mrs Lagarde ... stressed that, in Greece’s case, the Fund is willing to show utmost flexibility in the way in which the government’s reforms and fiscal proposals will be evaluated.

It added that in separate meetings, US Treasury officials who also met Varoufakis expressed the willingness of the US government to play the role of an “honest broker” in helping Greece to strike a deal with its lenders.

Russia: talks with Greece will not be limited to finance

A spokesman for Vladimir Putin, has reportedly been making comments ahead of the Russian President’s meeting with Greek PM Alexis Tsipras on Wednesday.

According to RIA Novosti, part of a state-owned news agency, Dmitry Peskov, said:

There is no need to limit everything to credit and financial issues. Russian-Greek relations are quite multifaceted.

They are much broader, and the entire range of relations will be discussed tomorrow.

Asked whether the possibility of a gas discount would be discussed, he said:

We do not rule out that these issues will also be raised.

Sticking with Greece, there has been no let up on its insistence that it is owed reparations by Germany for the Nazi occupation of Greece during the war.

Speaking on Monday, Greece’s deputy finance minister Dimitris Mardas said that Germany owes the country nearly €279bn (£205bn).

The Reuters story:

Greece’s deputy finance minister has said that Germany owes it nearly €279bn (£205bn) in reparations for the Nazi occupation of the country.

Greek governments and private citizens have pushed for war damages from Germany for decades but the Greek government has never officially quantified its reparation claims.

A parliamentary panel set up by Alexis Tsipras’s government started work last week, seeking to claim German debts, including war reparations, the repayment of a so-called occupation loan that Nazi Germany forced the Bank of Greece to make and the return of stolen archaeological treasures.

Speaking at a parliamentary committee on Monday, the deputy finance minister, Dimitris Mardas, said Berlin owed Athens €278.7bn, according to calculations by the country’s general accounting office. The occupation loan amounts to €10.3bn.

The campaign for compensation has gained momentum in the past few years as the Greeks have suffered hardship under austerity measures imposed by the European Union and International Monetary Fund in exchange for bailouts totalling €240bn to save Greece from bankruptcy.

Tsipras has frequently blamed Germany for the hardship stemming from the imposition of austerity. The Greek prime minister has angered Berlin by threatening to push for reparations in the middle of talks to unlock aid for Greece.

Germany has repeatedly rejected the country’s claims and says it has honoured its obligations, including a 115m deutschmark payment to Greece in 1960.

Over in Athens, the leading ATG share index is down 0.2% at 769.56, despite insistence from the Greek government that it is not about to default on its debt.

Finance minister Yanis Varoufakis met Christine Lagarde, head of the IMF, in Washington on Sunday to reassure her a €450m (£330m) debt repayment due on Thursday would be honoured.

This is what Lagarde said following the meeting:

Minister Varoufakis and I exchanged views on current developments and we both agreed that effective cooperation is in everyone’s interest. We noted that continuing uncertainty is not in Greece’s interest and I welcomed confirmation by the Minister that payment owing to the Fund would be forthcoming on April 9th.

I expressed my appreciation for the Minister’s commitment to improve the technical teams’ ability to work with the authorities to conduct the necessary due diligence in Athens, and to enhance the policy discussions with the teams in Brussels, both of which will resume promptly on Monday. I reiterated that the Fund remains committed to work together with the authorities to help Greece return to a sustainable path of growth and employment.”

Updated

Some more reaction now to those upbeat numbers from the UK services sector this morning.

Samuel Tombs, Capital Economics:

March’s UK Markit/CIPS report on services provides further reassurance that the economic recovery is still on a fast track despite the uncertainty created by the upcoming general election.

Martin Beck, EY Item Club:

With the MPC beginning its April meeting today, the PMI release offers food for thought for the Committee’s hawks and doves. For the former, services activity and employment continues to rise at a strong rate, while there is evidence of rising wage pressures in the sector. But for those more inclined to wait and see before hiking rates, March’s services survey also offered support, showing growth in input costs remaining historically muted and output prices rising only fractionally.

Overall, short of a marked rise in pay growth, we think that the MPC’s doves will continue to win out over the hawks for the foreseeable future, with no hike in [interest rates] likely in 2015.

Nick Beecroft, Saxo Bank:

This morning’s [composite PMI] for March will be extremely welcome news for the ruling Conservative party and Prime Minister Cameron. At 58.8, the figure beat expectations, (56.7), and is the highest reading since last August.

The detail behind the headline number was also encouraging, with the driving force for the increase being a surge in the services PMI to 58.9 from 56.7, beating expectations for a reading of 57.0.

As the services sector accounts for roughly 70% of the economy, and is sensitive to consumer confidence and behaviour, it appears that increases in living standards may finally be having a beneficial effect.

Eurozone factory gate deflation slows in February

Producer prices fell at an annual rate of 2.8% in February, a slower pace of decline than January when prices fell by 3.5%.

Economists polled by Reuters had forecast annual factory gate deflation of 3%.

On a monthly basis, producer prices actually rose by 0.5%, following a 1.1% fall in January. Economists had predicted a smaller rise of 0.1%. The increase was driven by a 2% rise in energy prices, and a 0.1% increase in consumer goods prices according to Eurostat, the eurozone’s statistics agency.

On a monthly basis, prices rose at the fastest pace in Greece, up 3.5%, and fell at the fastest rate in Slovakia, down 2.2%.

Howard Archer, chief UK and European economist at IHS Global Insight, said the data was the latest sign that eurozone deflation might be easing:

The marked weakening in the euro, improving eurozone growth and a limited firming in oil prices from their January lows currently looks to be diluting the risk of prolonged eurozone deflation. Indeed, the eurozone could possibly exit deflation in April.

Even if the eurozone does imminently exit deflation, it may still prove to be a hard slog to get eurozone consumer price inflation back up to the ECB’s target rate of “close to, but just below 2%.”

Despite improving eurozone growth, underlying inflationary pressures across the region look set to be limited for some considerable time to come.

The European Central Bank began a €1.1 trillion programme of quantitative easing last month, in an effort to boost growth and ward off the threat of a dangerous deflationary spiral. Inflation in the single currency bloc has been negative since December last year.

Markit: UK economy grew by 0.7% in Q1

Chris Williamson, chief economist at Markit, said the PMI suggested the UK economy “moved up a gear in March”.

Combining the services PMI with the equivalent surveys from the manufacturing and construction sectors published last week, Markit says the UK economy probably grew by 0.7% in the first quarter of 2015. That would be a slight improvement on the fourth quarter of 2014, when the economy grew by 0.6%.

We will have to wait until 28 March for the first official confirmation of Q1 GDP from the Office for National Statistics. Any improvement on Q4 2015 would hand the chancellor George Osborne a crucial advantage just one week before the polls open for the general election.

Markit’s Williamson:

The three PMI surveys collectively indicate that the economy grew by 0.7% in the first quarter, reviving from the slowdown seen late last year.

Faster growth of new business and improved expectations of prospects for the year ahead also bode well for the upturn to retain strong momentum as we move through the spring.

While the data support the view that the next move interest rates will be upward, the lack of inflationary pressures suggests the first hike remains some way off, and probably not this year unless we see some significant upturn in wage growth.

UK services sector booming in March

The headline Markit/CIPS services PMI has beaten expectations, rising to 58.9 in March from 56.7 in February.

It was the strongest since August 2014, and economists had forecast a lesser improvement to 57.

New business growth was behind the jump in overall UK services sector activity in March. Confidence about the outlook meanwhile was the strongest in 10 months.

Updated

So all in all, a broadly positive set of eurozone services PMI surveys has boosted the outlook for the broader economy. And certainly no nasty shocks.

The UK services sector data is due at 9.30am so we’ll bring you that very soon.

Here is how the private sector in individual eurozone countries performed in March, combining the manufacturing and services sector PMIs.

The higher the number above 50, the stronger the growth:

- Ireland: 59.8 (nine-month low)

- Spain: 56.9 (two-month high)

- Germany: 55.4 (eight-month high)

- Italy: 52.4 (eight-month high)

- France: 51.5 (two-month low)

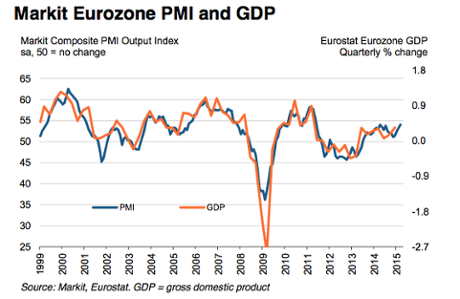

And here is how Markit’s composite PMI survey’s have tracked official GDP:

Eurozone's private sector boosts economy in March

Taken together, the services and manufacturing sector PMI data suggest the private sector boosted the eurozone economy in March, with the two sectors combined growing at the fastest rate in 11 months.

The eurozone composite index climbed to 54 in March from 53.7 in February, putting the single currency bloc on course for 0.3% growth in the first quarter according to Markit - the same pace as the fourth quarter of 2014.

The services index increased to 54.2 last month from 53.7 in February.

Improvement was broad-based across services and manufacturing, but in terms of country performance, former bailout countries Ireland and Spain led the way.

Chris Williamson, chief economist at Markit :

Whether the eurozone economy has achieved escape velocity to enjoy a return to a strong and sustainable recovery remains uncertain, but the region is certainly seeing its best growth momentum since 2011.

The PMIs are indicating somewhat sluggish GDP growth of 0.3% for the first quarter. However, the important message from the survey data is that the pace of expansion looks set to gather pace in coming months.

Encouragingly, with France returning to growth, all of the four largest euro nations are now back in expansion, indicating a broad-based upturn which should therefore be more self-sustaining.

An ongoing recovery is no one-way bet, however, with the Greek crisis remaining a critical threat to stability in the region.

Growth in German services sector accelerates

The headline services PMI rose to a six-month high of 55.4 in March from 54.7 in February.

Rising new orders and employment boosted the sector in Europe’s largest economy.

Oliver Kolodseike, economist at Markit:

Germany’s service providers signalled a pick-up in activity growth at the end of the first quarter, with the headline index improving for the third month running. New business flooded in at the strongest rate since September of last year, with companies benefitted from an improving economic environment, which in turn encouraged them to further add to their payrolls.

Survey data suggest that positive sentiment towards the 12-month outlook for business activity hit a four-year high in March, and companies were able to raise their charges to the greatest extent for nine months.

PMI data also showed that the upturn in economic activity was broad-based, with manufacturers and service providers experiencing similarly strong rates of output growth.

Growth slows in French services sector

The French services PMI indicated slowing growth in March, with the headline index falling to 52.4 from 53.4 in February.

It reflected a slowdown in new business growth. Employment in the sector grew for the first time in 17 months in March, albeit at a modest level.

Jack Kennedy, senior economist at Markit:

The French service sector maintained its expansion in March, with activity and new business continuing to rise, albeit at slower rates. This offset a continued contraction of the manufacturing sector.

PMI data suggest that private sector activity is likely to have made a small positive contribution to first-quarter GDP. Yet there remains little to suggest any sort of convincing recovery lies around the corner, as highlighted by service providers’ business expectations dipping to a three-month low in the latest survey period.

Italy services PMI creeps higher

The headline index rose to 51.6 in March from the no-change level of 50 in February.

New work rose at the fastest rate in eight months, ending four months of decline.

Phil Smith, economist at Markit, said the latest survey was good news for the Italian economy overall:

Although not quite the growth seen in manufacturing, the rise in business activity in the service sector is at least another sign that Italy’s private sector economy is expanding. Furthermore, stronger inflows of new business bode well for the upturn being sustained.

Based on the recent stream of PMI data, GDP is likely to have risen for the first time in more than a year in the first quarter, albeit probably only marginally.

The survey data are also highlighting healthier trends in the labour market, with the combined rate of job creation in manufacturing and services the best seen for over four years. The unemployment rate is therefore likely to fall in coming months in a boost to the euro area’s third-largest economy.

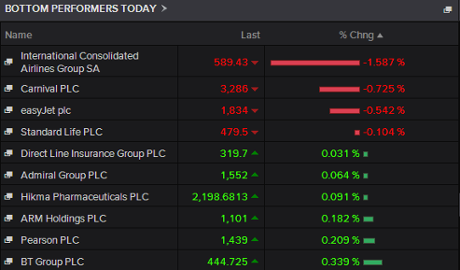

The vast majority of FTSE 100 companies are up this morning, just four are down.

Top performers:

Worst performers:

European markets rise

A quick look at the markets before we get the flurry of remaining eurozone services PMIs between 8.45am and 9am.

All the major European indices are up.

- FTSE 100: +1.3% at 6,922.5

- Germany’s DAX: +0.8% at 12,068.03

- France’s CAC: +0.7% at 5,111.79

- Italy’s FTSE MIB: +1.1% at 23,555.48

- Spain’s IBEX: +0.6% at 11,707.5

Here is how Spain’s PMI survey has tracked official GDP over the years.

#Spain Services #PMI: sharpest rise in new orders since Jul'00 and strongest rate of job creation since Nov'07 http://t.co/0bAZANsS7n

— Markit Economics (@MarkitEconomics) April 7, 2015

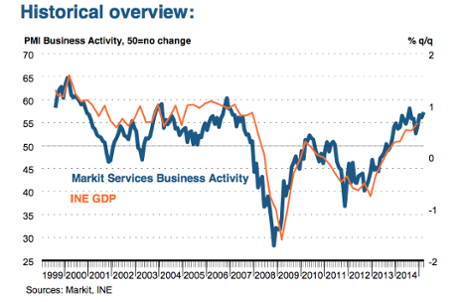

Spain's services sector grows in March

Spain’s services sector performed strongly in March, with companies witnessing the sharpest rise in new orders in 15 years. The headline index on the Markit services PMI increased to 57.3 from 56.2.

New orders rose at the sharpest pace since July 2000, and employment in the sector increased at the fastest rate since November 2007, before the financial crisis was unleashed on the global economy.

Andrew Harker, senior economist at Markit:

The highlight from the latest Spanish Services PMI is the sharpest monthly expansion in new business for almost 15 years as improving economic conditions encourage customers to commit to spending.

The labour market continues to benefit from higher workloads, with staff taken on at a pace not seen since prior to the economic crisis.

Updated

Agenda: UK and eurozone services PMIs

At 9.30 we have the closely watched Markit/CIPS services PMI for March.

Economists are expecting the survey to show improvement, with the headline index forecast to rise to 57 from 56.7 in February, where anything above 50 indicates expansion.

Britain’s recovery to date has been heavily dependent on the services sector, which accounts for about three quarters of the economy. Services is the only key sector of the economy where output has now surpassed pre-crisis levels.

The first official estimate of UK GDP for the first quarter will be published on 28 March, the week before the general election. The March services PMI will be scrutinised for signals about how the economy was doing at the end of the quarter.

We also have all the eurozone services and composite PMI’s coming up, starting with Spain at 8.15am.

Greece vows to make IMF repayment ahead of Moscow visit

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

Yanis Varoufakis, the Greek finance minister, has been in Washington DC to meet Christine Lagarde, head of the International Monetary Fund.

He told Lagarde Greece will be able to meet Thursday’s deadline for a €450m (£330m) debt repayment.

Greece is on a mission to convince its lenders that it is able to honour its debts and will not default.

Ahead of the key deadline on Thursday, the Greek prime minister Alexis Tsipras will hold talks with the Russian president, Vladimir Putin, in Moscow.

We will be bringing you all the latest Greek developments and other news as it happens.

Updated