And finally... Europe’s stock markets shrugged off their early weakness, to finish the day with gains across the board:

The Athens exchange also rose, finishing the day 0.5% higher.

Although there were some jitters in the bond market, it ended the day calmly too.

Tony Cross, market analyst at Trustnet Direct, reckons markets are in limbo until they know when the Federal Reserve starts to raise borrowing costs:

The reality is that rate hikes are inevitable, but with so much concern that the Fed will jump too soon, the market is understandably skittish. The problem is that any overreaction here could initiate a sell-off that would be nothing short of panicked.

And that’s all for today. Thanks, and goodnight. GW

A sign that Greece is compromising?

Economy Minister George Stathakis told Bloomberg earlier today that the government is cracking on with the privatisation of privatize the country’s largest port, at Piraeus, and regional airports.

Greece to privatize port, airports in concession to creditors http://t.co/cyJjuK026m pic.twitter.com/vsxHxZLXxg

— Bloomberg Business (@business) May 14, 2015

Missed this earlier, sorry, but the latest budget figures for Greece were released earlier today - showing that Athens has now squirrelled together €2.5bn in funds this year.

It’s achieved this primary surplus deficit by cutting its spending to the bone - expenditure is almost €2bn less than expected.

New data: #Greece govt again hoarding cash thru strong tax collex & miserly spending. €2.5bn to stave off bankruptcy pic.twitter.com/wnNFXC5nyH

— Peter Spiegel (@SpiegelPeter) May 14, 2015

It’s not exactly the Syriza dream of no more austerity; but it does show that the government could last for longer than some commentators have claimed.

Higher tax revenue and lower spending: Syriza are doing everything their creditors demand http://t.co/DHNbOzkTWX pic.twitter.com/pJaKv5ZSmC

— Telegraph Finance (@TeleFinance) May 14, 2015

Updated

And that’s the end of the conversation. Some interesting insights into Draghi’s view of the world; a shame that Christine Lagarde didn’t seek his views on the Greek bailout talks. Still, she’s not auditioning for Newsnight.

Draghi and Lagarde are now heading off for talks about the situation in Europe -- Greece will surely be on the top of the agenda....

What will the ECB’s policy response be like in 2020, asks Olivier Blanchard (he gets a question as a special treat to mark his retirement)

Not an easy question, Draghi replies.

He explains that the ECB has created a range of new tools since the financial crisis started. In five years time, we will be closer to what central banks are like in “ordinary places” -- but still with a broader set of tools than before.

Draghi explains that when people questioned recent policy measures, he would explain that the ECB needed more firepower to address its particular challenges.

We still have the same mandate as before...but in a very different situation, handling different economies in different countries.

Updated

Lagarde turns to the role of macro-prudential tools -- are they the first line of defence?

Monetary policy has one objective - price stability. And that’s a pre-requisite for financial stability, says Draghi.

So macro-prudential tools have to be used. However, the toolbox isn’t finished yet.

[macro-prudential tools are, for example, rules telling banks how much capital they have to hold].

Updated

Tackling the fragmented mortgage market across Europe would help enhance the power of monetary policy, says Draghi.

Mario Draghi and Christine Lagarde are now enjoying a conversation about monetary policy issues.

It’s not exactly Frost/Nixon, based on the opening gambit:

What other policy reforms would complement your “couragous” actions, Mario?

One of the lessons of the crisis is that our monetary policy transmission was impaired because many banks held too many bad loans, says Draghi.

That, and the fragmentation of the banking sector, made it harder to get credit flowing again.

So when the ECB pumped almost €1trn into the banking sector through its Long Term Refinancing Operations in 2011 and 2012, the banks used the cash to buy government bonds rather than lending to the real economy.

So the lesson is that two sets of reforms are needed:

1) a supervisory mechanism that ensures bank balances sheets are healthy, and can ensure closer harmony between banks across Europe.

2) Reforms to expand the capital market, to make it easier for capital to flow across borders.

The charts from Mario Draghi’s speech https://t.co/ARMxbdLHRe (speech text here https://t.co/88qDNAbmWh) pic.twitter.com/BnaQ9JuVdm

— ECB (@ecb) May 14, 2015

Draghi: Stimulus will continue for some time

Draghi has also tried to sink the suggestion that the ECB might wind up its QE scheme early:

After almost 7 years of a debilitating sequence of crises, firms and households are very hesitant to take on economic risk. For this reason quite some time is needed before we can declare success, and our monetary policy stimulus will stay in place as long as needed for its objective to be fully achieved on a truly sustained basis.

Updated

Draghi: We must watch for undesirable consequences

Towards the end of his lecture, Mario Draghi does admit that the unprecedented stimulus launched by the ECB could have negative consequences:

That being said, we have to be mindful that too prolonged a period of very low real rates can have undesirable consequences in the context of ageing societies, where many households save not just to smooth consumption over the cycle, but to smooth consumption over their lifetime. For pensioners, and for those saving ahead of retirement, low interest rates may not be an inducement to bring consumption forward. They may on the contrary become an inducement to save more, to compensate for a slower rate of accumulation of pension assets.

However, he argues that those savers wouldn’t benefit if the central bank simply gave up on its mandate:

On the contrary, the interest of long-term savers is that output be raised to potential without undue delay. This is because their financial assets are always, in the final analysis, a claim on the wealth generated by the productive part of the economy. So it is in their interest that output growth remains on a robust path as this maximises the likelihood that their claims are honoured in full. At the same time, the more monetary policy is able to encourage investment, the faster interest rates will return into more normal territory.

Updated

Central banks are often criticised for boosting the wealth of the richest though their asset purchase schemes.

Mario Draghi, though, is arguing that younger Europeans would have suffered disproportionately if the eurozone had been left to fallen into protracted deflation

Draghi: Yes, monetary policy has distributional impact. So does inaction. There is no neutral distribution pic.twitter.com/sH0PotsFil

— Mike Bird (@Birdyword) May 14, 2015

Mario Draghi is now giving the Michel Camdessus lecture. His theme is “The ECB’s Recent Monetary Policy Measures: Effectiveness and Challenges”.

He’s outlining how the ECB has responded to the crisis, particularly since the start of 2014 -- by cutting interest rates to record lows, imposing negative yields on deposits, offering cheap loans to banks, and eventually launching its on QE asset purchase scheme.

Helpfully, the speech is online, complete with charts, so I suggest you read it here:

The ECB’s Recent Monetary Policy Measures: Effectiveness and Challenges

Or you could digest Draghi’s conclusion:

Faced with an environment of unprecedented complexity, the ECB has taken a series of unconventional measures to prevent a too prolonged period of low inflation and deliver its mandate. Those measures have proven so far to be potent, more so than many observers anticipated. But their potency is also because they have interacted with other policies that have put the economy and the financial sector in a better position to respond to our monetary impulses.

This includes the Comprehensive Assessment of euro area banks. And it includes structural reforms where they have been implemented. By the same token, structural reforms that increase confidence in economic prospects and encourage entrepreneurs to capitalise on today’s extremely accommodative financing conditions will make our policy commensurately more powerful.

Policymakers in the euro area are independent, but the effects of their policies are interdependent. This is why it is ultimately only a combination of policies, that are complementary and mutually consistent, that will allow our policy to reap its full effects – and to bring about a lasting return of both prosperity and stability for the whole euro area.

Draghi has screwed up his Between Two Ferns appearance. pic.twitter.com/RscaWIIgy5

— Mike Bird (@Birdyword) May 14, 2015

Christine Lagarde also pays tribute to Mario Draghi, and the leadership he has shown.

Mario—and I cannot emphasize this enough—your job is one of the most difficult. It is in part because it is a very influential one, and you have used that influence to move the euro area in the right direction. Those who know you understand that you are a man of outstanding insight, fierce determination, and above all, courage.

So far so good....

You can call a spade a spade without putting any of your cards on the table.

We have no idea what that means.

Lagarde: We need ambitious polities to boost growth

Christine Lagarde is speaking in Washington now, and warning that the task of fixing the world economy is not complete.

The IMF chief says:

I am myself very concerned that slow job growth and rising inequality will come back to haunt us. We need ambitious and decisive policies to boost today’s growth and tomorrow’s growth potential, and to build resilience to existing and emerging challenges. I am reminded of a saying by Michelangelo:

“The greater danger for most of us lies not in setting our aim too high and falling short; but in setting our aim too low, and achieving our mark.”

She also offers her “full support” to the actions taken by the European Central Bank, particularly its QE programme.

Notably, the significant further easing of monetary policy in January of this year has done much to stave off the threat of deflation and support weak demand. Monetary policy and price stability are essential for strong, sustainable, and inclusive growth.

Looking forward to my #CamdessusLecture discussion with @ecb President Mario Draghi at 10.45am ET. Watch here: http://t.co/geNKR74pKf

— Christine Lagarde (@Lagarde) May 14, 2015

The IMF are live-streaming Mario Draghi’s lecture, which starts in around 10 minutes time at 4pm BST or 11am East Coast.

It’s followed by a ‘conversation’ between Draghi and Christine Lagarde.

Here’s the livestream:

2015 Michel Camdessus Central Banking Lecture

IMF: We can look at all options for Greece

The International Monetary Fund hasn’t given up hope that Greece can complete its bailout programme, despite the months of turmoil and slow progress towards a deal with creditors.

Gerry Rice, the IMF’s chief spokesman, is briefing reporters in Washington DC now. He says that the Fund will stand by Athens, so long as it is meeting its bailout programme

“We are flexible. We are open to look at all options. But we must insist on reaching the objectives of the program.”

Rice also confirmed that Christine Lagarde and Mario Draghi will talks about ‘developments’ in Europe today, after Draghi has given his speech in Washington later today.

IMF's Rice: IMF working intensely with Greece to procure a deal, IMF head Lagarde to meet with Draghi to discuss developments in Europe: BBG

— Live Squawk (@livesquawk) May 14, 2015

#IMF repeats it is flexible in #Greece talks as long as program objectives met; working intensely to get deal soon ~spokesman /via @cigolo

— Yannis Koutsomitis (@YanniKouts) May 14, 2015

Weidmann criticises emergency Greek funding

Germany’s top central banker, Jens Weidmann, has weighed in on the Greek crisis.

The head of the Bundesbank criticised the emergency support which the European Central Bank is giving to Greece. He also raised concerns over the ECB’s quantitative easing programme, which is mopping up tens of billions of euros of government bonds each month.

Weidmann Criticizes ELA Funding of Greek Banks: Handelsblatt pic.twitter.com/lpn4H046Yx

— *Russian Market (@russian_market) May 14, 2015

Weidmann, of course, is one of the most powerful policymakers at the ECB (not as powerful as Mario Draghi, though!)

Updated

Summary

OK, time to recap.

The governor of the Bank of England has downplayed suggestions that foreign workers should be blamed for the UK’s poor productivity growth, and weak pay rises.

Mark Carney also told Radio 4’s Today Programme that a referendum on the UK’s membership of the European Union should take place ‘as soon as necessary’, before uncertainty over the result hits the economy.

He said:

“I think it’s in the interests of everybody that there is clarity about the process and the question and the decision.”

#brexit uk's central banker sounds worried bout quitting, rubbishes immigration alleged impact on jobs,wages http://t.co/qtL1lkhtRM

— Ian Traynor (@traynorbrussels) May 14, 2015

Negotiations between Greece and her creditors has resumed in Brussels today, in an attempt to accelerate progress.

Athens says:

The instructions given to the negotiating team were to move in such a way to speed up the process.”

But Greece is sticking to its ‘red lines’; with finance minister Yanis Varoufakis insisting that he couldn’t sign a deal that pushed Greece back into a death spiral.

"As finance min I refuse to put my signature to a package .. if it proves mathematically that it doesn't add up," says #YanisVaroufakis

— Helena Smith (@HelenaSmithGDN) May 14, 2015

Varoufakis has floated the possibility that Europe’s main bailout fund could step in to cover looming repayments due to the ECB.

But he’s certainly not proposing that Greece should refuse to pay up.

Varoufakis has also claimed that Mario Draghi is afraid of upsetting Germany, saying:

“The idea of a swap between the Greek government and the ECB fills Mr. Draghi’s soul with fear. Because you know that Mr. Draghi is in a big struggle against the Bundesbank, which is fighting against QE. Mr. Weidmann in particular is opposing it.”

Varoufakis says debt swap fills Draghi's 'soul with fear' http://t.co/Wy213vwt9T #greece

— Kathimerini English (@ekathimerini) May 14, 2015

Another Greek minister has suggested that Greece could yet hold a referendum on its bailout programme, despite time and money running very short.

The European Bank for Reconstruction and Development has highlighted the dangers Greece faces; a major recession could be inevitable if a deal isn’t reached in time.

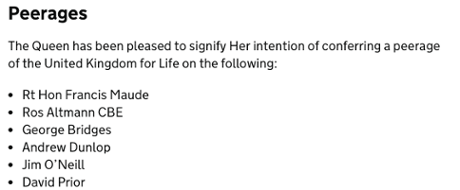

And it’s trebles all round for Jim O’Neill as he joins the government, and Thomas Piketty as he takes up a role at the London School of Economics.

Updated

It’s a real musical chairs day in the word of economics.

Olivier Blanchard, the IMF’s top economist, is retiring at the end of September, the Fund just announced.

He’s going to become C. Fred Bergsten Senior Fellow at the Peterson Institute for International Economics.

Lagarde praises Blanchard for “intellectual leadership, wise counsel, friendship, loyalty” http://t.co/a6Xo0Fx8km

— IMF (@IMFNews) May 14, 2015

Blanchard is probably most famous in the UK for warning that George Osborne was “playing with fire” with his economic plans. Britain went on to record the fastest growth in the advanced world; and also ran a rather chunkier deficit too...

Updated

And here’s a photo of the chancellor announcing his devolution plans:

Heseltine, Jim ONeill, council leaders, here to hear from Osborne on Powerhouse at ex-Warehouse Project rave location pic.twitter.com/qmnPKa2qmh

— Faisal Islam (@faisalislam) May 14, 2015

Congratulations to Jim O’Neill, the former Goldman Sachs chief economist who coined the idea of the BRICS economies.

He’s just been appointed as Commercial Secretary at the Treasury, with responsibilities for devolving powers to the UK’s regions and building a new Northern Powerhouse.

He’s also lined up for a peerage -- arise Lord O’Neill! Of BRICS? Or perhaps Old Trafford, given his love of Manchester United.

Look who’s coming to London:

Thomas Piketty is to join the London School of Economics as Centennial Professor its new International Inequalities Institute

— Greg Hurst (@GregHurstTimes) May 14, 2015

Piketty joins London School of Economics. http://t.co/2MRAJtBnbv

— Sebastian Barfort (@SBarfort) May 14, 2015

Piketty’s book Capital in the Twenty-First Century has reportedly sold more than 1.5 million copies in its combined French and English translations; the resulting royalties mean the French economist might actually be able to afford a house in the capital.

Updated

Hell hath no fury like a finance minister misquoted.

Yanis Varoufakis has now issued a statement, insisting that he did not propose a delay to repaying the ECB back (as covered earlier), and blasting those who believed he did.

#Greece MoF press release re FinMin @yanisvaroufakis refererence to SMP. #economy #ecb pic.twitter.com/vGRC87fR9n

— Manos Giakoumis (@ManosGiakoumis) May 14, 2015

Cutting through the acronyms, Yanis is talking about Europe’s main bailout vehicle (the ESM) providing assets for Greece to use to repay Greek government bonds held by the ECB (starting with the €6.7bn which mature in July and August).

This would remove the danger of default. But it’s also effectively another bailout, and the rest of the eurozone isn’t prepared to start talking about that until the existing programme is completed.

And as the ESM’s shareholders are the 19 members of the eurozone, this idea can’t get off the ground -- as Peter Spiegel of the FT tweeted this morning:

By the way, worth nothing @ECB also supports @yanisvaroufakis idea of swapping GGB bonds held by ECB for ESM bonds. But not gonna happen.

— Peter Spiegel (@SpiegelPeter) May 14, 2015

Greek readers might appreciate this too:

For Greek speakers, here's @yanisvaroufakis remarks that got everyone so confused this morning. https://t.co/Nsqlkwo0Zb

— Peter Spiegel (@SpiegelPeter) May 14, 2015

Updated

Greece would face 'major recession' if deal isn't reached

The European Bank of Reconstruction and Development has also warned that Greece would be plunged into a major recession if it defaulted on its debts, hurting economies across Eastern Europe.

The baseline assumption in today’s EBRD report is that an agreement will be reached between Greece and the lending institutions,.

That would helping confidence and stability and could pave the way for a return to modest growth in the second half of the year, pulling Greece out of recession. Growth could then rise to 2% in 2016, as improved confidence and the ECB’s QE programme kick in.

However...

these forecasts would be rendered completely invalid in a negative scenario of missed sovereign debt payments, capital controls, limits on deposit withdrawals and the possible introduction of IOUs (“pseudo euros”) or equivalent instruments to pay domestic obligations.

In this case, Greece would likely fall back to a major recession, the size and duration of which are difficult to quantify now.

The European Bank for Reconstruction and Development has worrying news for Russia and Ukraine today.

In its new Regional Economic Prospects report, the EBRD warned that Russia’s downturn is hurting neighbouring countries, undermining the benefit of the stronger eurozone.

The Bank sees little immediate improvement either:

Russia itself is expected to suffer a significant recession with the economy shrinking by 4.5% percent in 2015 and by close to two per cent in 2016. The country may face a protracted period of slow growth or stagnation. Low oil prices and sanctions have taken their toll on an already weak economy with deep-seated structural problems.

Ukraine is expected to suffer an extremely deep recession this year, of around 7.5%:

The economic disruption in the east of the country, the negative impact of the depreciation of the hryvnia, tight economic policies, energy tariffs hikes and a continued contraction of credit are expected to maintain pressures on the economy this year.

Here’s the report:

EBRD economies split between eurozone boost and harsh wind of Russian recession

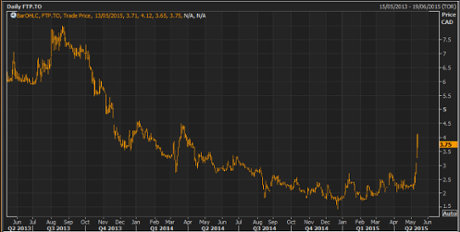

Now here’s a funny thing. Shares in a Canadian banknote printing firm have soared this month, amid rumours that it has a deal with Greece to produce a new currency if it left the eurozone.

Shares in Vancouver-based Fortress Paper jumped from 2.30 Canadian dollars to over C$4 this week, before dipping back to C$3.75 last night.

Bloomberg has been chasing the story:

Fortress said Tuesday it doesn’t know why its shares are climbing, and chief executive officer Chadwick Wasilenk declined to comment when a Bloomberg reporter cornered him.

Meanwhile, some 6,000 miles from Athens, a banknote printing company in Vancouver ... MT @BV Depositors flee Greece http://t.co/WzkQxjrFIn

— Beate Reszat (@rszbt) May 14, 2015

Under stock market rules, Fortress couldn’t keep quiet if it had actually won a major contract, especially once its shares started motoring. So there may be precisely nothing in it.

I can’t immediately find another reason for the rally, though. Fortress did report results week, showing it racked up an EBITDA loss of $2.5 million for the first quarter. One to watch, though...

Updated @Reuters story makes clear @yanisvaroufakis talked bond swap, not ECB payment delay http://t.co/mHKXmHXDWj pic.twitter.com/GNkEJJ4NbX

— Peter Spiegel (@SpiegelPeter) May 14, 2015

Elsewhere in Greece today, the deputy defence minister has reignited speculation that a referendum could be held.

Kostas Isychos insisted that Greece will not oblige foreign lenders by simply crossing its “red lines,” .

Helena Smith reports:

Speaking to Star TV, Isychos said:

“It [the referendum] is something that is still on the table. Leftists have to decide what kind of Europe they want.”

Isychos, a leading member of the governing radical left Syriza party who was raised in Canada, also defended the government’s decision to play what has been described as a highly provocative video, depicting Nazi war atrocities, to passengers on the Athens subway.

At a time when World War II anniversaries had been coming in thick and fast, Isychos said it was very important that young Greeks were reminded of what had happened during the Third Reich’s occupation of the country.

“We want and, we we will, find ways to heal wounds of the past with the German people,” said Isychos who is leading Greece’s campaign to win war reparations from Berlin.

Idea of ESM buying out #Greece's SMP bonds at ECB is not new. My idea too since mid-2014. The catch: ESM needs MoU + conditionality

— Yannis Koutsomitis (@YanniKouts) May 14, 2015

I must confess I’m a little confused about exactly what Yanis Varoufakis is proposing about Greece’s bond repayments.

So in an attempt to nail down precisely what’s happening, here’s Reuters latest story from Athens:

Greece’s Varoufakis says debt swap fills Draghi’s “soul with fear”

Repayment of what Greece owes to the European Central Bank should be pushed into the future, but it is not an option because it fills ECB chief Mario Draghi’s “soul with fear”, Greece’s finance minister said on Thursday.

Yanis Varoufakis said Draghi, president of the European Central Bank, cannot risk irritating Germany with such a debt swap because of Berlin’s objection to his bond-buying programme.

Varoufakis first raised the idea of swapping Greek debt for growth-linked or perpetual bonds when his leftist government came to power earlier this year, But Athens has since dropped the proposal after it got a cool reception from euro zone partners.

The outspoken minister, who has been sidelined in talks with European Union and International Monetary Fund lenders, brought it up again on Thursday, saying €27bn of bonds owed to the ECB after €6.7bn worth are repaid in July and August should be pushed back.

“What must be done (is that) these 27 billion of bonds that are still held by the ECB should be taken from there and sent overnight to the distant future,” he told parliament.

“How could this be done? Through a swap. The idea of a swap between the Greek government and the ECB fills Mr. Draghi’s soul with fear. Because you know that Mr. Draghi is in a big struggle against the Bundesbank, which is fighting against QE. Mr. Weidmann in particular is opposing it.”

Varoufakis was referring to the ECB’s quantitative easing (QE) or bond-buying plan and Bundesbank President Jens Weidmann’s unabashed criticism of it.

Varoufakis said the bond-buying plan is “everything for Mr. Draghi” but that “allowing such a swap of our own new bonds with these bonds ... would feed Mr. Weidmann with excuses to create problems with the ECB’s QE.”

Prime Minister Alexis Tsipras’s government stormed to power in January promising it would end austerity and demand a debt writeoff from lenders to make the country’s debt manageable.

It has spoken little about debt relief in recent months as it tries to focus on reaching a deal with lenders on a cash-for-reforms deal, which has proved difficult amid a deadlock on pension and labour issues.

Updated

Key clarification. Initial comments seemed to suggest pay delay MT @yanisvaroufakis: I spoke of possible ESM-mediated repayment of ECB GGBs

— Peter Spiegel (@SpiegelPeter) May 14, 2015

Greek Govt says more talks due with creditors in Athens tomorrow.

— Steve Collins (@TradeDesk_Steve) May 14, 2015

Greek finance minister hits back

Yanis Varoufakis has just turned to Twitter to insists he’s not refusing to repay the European Central Bank:

I spoke of a possible ESM-mediated repayment of ECB's SMP GGBs and some journos report I announced....nonpayment. Astonishing propaganda!

— Yanis Varoufakis (@yanisvaroufakis) May 14, 2015

A good example of the dangers of speaking at Economist conferences during vital debt negotiations, I’d humbly suggest.

But in the interests of fighting propaganda, let’s remind ourselves what Varoufakis said [from 9.38am], according to Reuters.

Over July-August the finance ministry will have to borrow €6.7bn from our partners in one way or the other to repay bonds from the SMP programme.

“About €27bn of those bonds are still left, which should be repaid in the next months or years. These bonds should be pushed back to the distant future. This is clear.”

Updated

The pound has hit a new near-six-month high this morning, hitting $1.58 against the dollar for the first time since November.

GBPUSD enjoying its best 5 days since October 13-17th 2009 pic.twitter.com/ixf4YBVStG

— World First (@World_First) May 14, 2015

Better chart of that GBPUSD outperformance here pic.twitter.com/pzkJzx02Hx

— World First (@World_First) May 14, 2015

Greece’s prime minister appears to have rolled out his best summer suit to welcome a group of visitors from the US.

Meeting now with representatives from AHEPA. We value the diaspora's support. #Greece pic.twitter.com/wpFLkfulNC

— Alexis Tsipras (@tsipras_eu) May 14, 2015

AHEPA, or the American Hellenic Educational Progressive Association, was set up more than 90 years ago to help Greek immigrants integrate into US society.

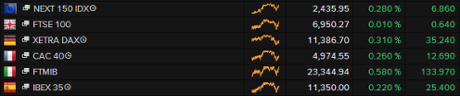

Over to the markets. After a weak start, the FTSE 100 is now flat this morning as traders take a breather.

Other European markets are up, welcoming the fact that bond markets are calm after some wild days recently.

Credit Agricole’s Fred Ducrozet reckons that Greece has no hope of persuading the ECB to let it delay repaying €6.7bn of maturing debt.

http://t.co/vapRbf9AC5.Happen. https://t.co/l04HFTWk6C

— Frederik Ducrozet (@fwred) May 14, 2015

Delaying Greece’s ECB repayments would effectively be a debt restructuring, points out ING economist Carsten Brzeski:

Debt restructuring here we come...acc to Bild, Varoufakis wants to delay reimbursement of maturing Greek bonds held by ECB.

— Carsten Brzeski (@carstenbrzeski) May 14, 2015

Mario Draghi will get the chance to respond to Yanis Varoufakis’s comments this afternoon, when he gives the Michel Camdessus Central Banking Lecture in Washington.

#Draghi speaks today at 3pm GMT at IMF central banking lecture. He might also use the stage to comment on recent QE market jolts & #Greece

— Maxime Sbaihi (@MxSba) May 14, 2015

Yanis Varoufakis has also argued that Greece shouldn’t meet the €6.7bn of debt repayments it owes the European Central Bank this summer.

He told the Economist conference that Greece’s debts aren’t viable, and that those ECB repayments should be kicked into the long grass.

Reuters has the details:

“Over July-August the finance ministry will have to borrow 6.7 billion euros from our partners in one way or the other to repay bonds from the SMP programme,” Yanis Varoufakis told a conference in Athens, referring to bonds bought by the ECB under the Securities Market Programme over 2010-2011.

“About €27bn of those bonds are still left, which should be repaid in the next months or years. These bonds should be pushed back to the distant future. This is clear.”

Unless Greece get an agreement with its creditors soon, it will enter July with no bailout funds.

The ECB repayment bill is the biggest hurdle facing Greece in the next few months, as this chart shows:

Greece's debt repayment schedule. #debt #grexit #default #ecb #europe #greekcrisis #reforms pic.twitter.com/kyeJVxLrLR

— Bay Lounge (@BayLounge) May 5, 2015

(T-bills are short-term debt that can usually be rolled over.)

Updated

Greek finance minister: I won't sign a bad deal

Yanis Varoufakis, the embattled Greek finance minister, has just sparked fresh speculation over his future.

He told the Economist conference in Athens that he will “never put my signature” to an agreement where Greece is once again plunged into an economic death spiral.

Analysts are saying this might well foreshadow his departure - either he gets the deal he wants or he leaves, explains our correspondent Helena Smith.

"As finance min I refuse to put my signature to a package .. if it proves mathematically that it doesn't add up," says #YanisVaroufakis

— Helena Smith (@HelenaSmithGDN) May 14, 2015

As we covered earlier, negotiations between the Greek government and its creditors are resuming in Brussels today as the clock ticks down.

On Monday night, Varoufakis warned that Greece’s liquidity crisis was now extremely urgent, and could come to a head within two weeks.

Greece must pay wage and pensions at the end of this month, and then faces repayments to the IMF in June.

Updated

Over in Athens, Greece’s finance minister Yanis Varoufakis is addressing a conference organised by the Economist.

Helena Smith reports:

In a speech that is likely to be dominated by a Q & A session, the Greek finance minister started out saying that “if Greece doesn’t reform it will sink” after explaining why the ongoing negotiations were “so marathon.”

“We all agree that Greece should not suffer the indignity of [excessive primary surpluses].”

Last night emerging from the finance ministry Varoufakis told protesting tax office employees gathered outside that negotiations between Greece and its creditors were now at “the most difficult … precarious point.”

The minister took the protestors aback saying the negotiations had reached a point where the government had come under pressure to “take all existing wages above €700 and bring them below €700.”

Updated

And here’s exactly what Mark Carney said about the risks that uncertainty over the EU referendum poses, via ITV News.

We talk to a lot of bosses and there has been an awareness of some of this political uncertainty - whether because of the election or because of the referendum.

What they’ve been telling us, and we see it in the statistics, is they have not yet acted on that uncertainty - or to put it another way, they are continuing to invest, they are continuing to hire.

Mark Carney: EU in-out referendum 'should happen as soon as necessary' http://t.co/3xbkGVg8RY pic.twitter.com/AsteRFlCPD

— ITV News (@itvnews) May 14, 2015

Carney on migration and the EU: snap summary

Mark Carney has done his best to take the string out of today’s Daily Mail front page splash, saying he blamed foreign workers for “dragging down wages”

As he explained, at some length, to John Humphrys, net migration is only one factor in the complicated puzzle of why UK productivity has been so weak.

The wider expansion of the labour market (older workers, and part-timers working more hours) has also made it easier for companies to take on more staff rather than paying existing workers more - or investing in expensive machinery.

And if they have the right skills, foreign workers can be a key driver of higher productivity (and thus higher wages), as they become established in the UK.

Carney still irritatingly (for journalists) unrattleable and on-message. Dampening only vaguely controversial comment(on migration)from yday

— Catherine Boyle (@cboylecnbc) May 14, 2015

Humphrys immigrant shaming on #r4today as he talks to Mark Carney who is himself an immigrant.

— Peter Spence (@Pete_Spence) May 14, 2015

On interest rates, Carney was rather vague, saying it was ‘possible’ that rates would be higher in a year.

Such a change from his early days in the UK, when he laid out clear ‘’forward guidance’ of the conditions that could prompt a rise in borrowing costs.

Anyone remember forward guidance? Carney's language on the path of rates now firmly back in the King-era. #r4today

— Duncan Weldon (@DuncanWeldon) May 14, 2015

And his comments on the EU referendum were interesting. Governors aren’t allowed to cross into politics*, but Carney did indicate that it would be good to get the uncertainty out of the way before business confidence and investment is hit.

Here’s the key quote (from Reuters):

“It’s in the interests of everybody that there is clarity about the process and the question and the decision...

The government has made it clear that it is a priority. I am sure the government will act with appropriate speed in developing the negotiations.”

Mark Carney gets within a fag paper's width of calling for a referendum sooner rather than later on #r4today

— josh lowe (@JeyyLowe) May 14, 2015

* - although it wouldn’t be a big surprise if Mr Carney switched to Canadian politics when his work at the Bank of England is over.

Updated

Carney: UK faces significant headwinds

Mark Carney also cautions against assuming that the UK economy recovery will be smooth and simple.

We face a weak global economy, the impact of fiscal consolidation [George Osborne’s deficit reduction plans], and the challenge of completing the repair of the financial system.

Economic growth will also be “dampened” by the strong pound, he adds [it hit a five-month high against the dollar yesterday].

The next interest move will probably be up, Carney adds, and it’s “possible” that rates will be higher in a year’s time.

Updated

Onto general economic issue, and Carney says that interest rates will rise in a gradual manner, when the time comes....

Carney: EU referendum should take place as soon as necessary

Is the Bank of England worried that a referendum on Britain’s membership of the EU will cause uncertainty and hit business confidence?

The Bank doesn’t believe that businesses have yet acted on the uncertainty.

It’s in the interests of everybody that there is clarity about the process and the question and the decision, governor Carney replies.

And the speed?

I wouldn’t put a timetable on it, Carney says

Humphrys presses him - Would you like it to be completed earlier than the end of 2017?

It should take place “as soon as necessary”, Carney concludes.

Mark Carney wants an EU referendum "as soon as necessary". Presumably some sort of Canadian idiom. #r4today

— Andrew Clark (@clarkaw) May 14, 2015

Updated

As businesses run out of labour, productivity should go up, says Carney.

But you’ve been predicting a rise in productivity for years...

Yes, and it should start to move up soon, Carney replies

But there are 4.8m foreign workers in the economy, isn’t that pushing down wages and productivity, asks Humphrys.

Mark Carney explains that foreign workers usually enter the labour market in jobs which are below their skill set. Over time, they rise up through the workforce, take on more high-skilled jobs and contribute to rising productivity.

The bottom line is that British people want to work more, and they have been able to do so (unemployment has fallen to 5.5%).

Updated

Carney: Don't blame foreign workers for poor productivity

Humphrys asks if foreign workers are to blame for Britain’s poor productivity growth.

“I’d really dampen that down”, Mark Carney replies.

There are 300,000 more older workers who wouldn’t normally still be in the labour market.

And there are 200,00 to 300,00 more people who wanted to work more hours.

That’s around 500,000 people.

Compare that to net migration - it’s up by 50,000 in the last two years.

Carney concludes:

The real story is that British people want to work more.

John Humphrys asks if it’s true that households would be £5000 per year, after tax, if productivity had grown at the pre-crisis rate.

Wages would be higher in the “high teens”, Carney agrees.

Mark Carney interviewed by the Today Programme

Governor Carney is on the Today Programme now....

John Humphrys asks why productivity is so weak.

Carney says the Bank has been repeatedly disappointed by UK productivity.

It is the key determinant for wages and living standards in the UK.

Updated

@bankofengland Gov Carney on R4 shortly. http://t.co/e4F1F6Dvu3 inflation, interest rates and productivity. Will they ask about DOJ + fx?

— F O'Brien (@fergalob) May 14, 2015

You can listen to the Mark Carney interview live, here.

Mark Carney is likely to be quizzed about migration when he is interviewed on the Today programme in a few minutes.

Yesterday’s Bank of England Inflation Report identified net migration as one factor that has pushed down wage growth; the comment made the front page of the Daily Mail:

Thursday's Daily Mail front page - Bank chief: foreign workers drag down UK wages #tomorrowspaperstoday #bbcpapers pic.twitter.com/Z3XbOhbhJO

— Nick Sutton (@suttonnick) May 13, 2015

So what did Carney actually say?

In recent years labour supply has expanded significantly owing to higher participation rates among older workers, a greater willingness to work longer hours and strong population growth, partly driven by higher net migration. These positive labour supply shocks have contained wage growth in the face of robust employment growth.

Wages have grown by around 2% in the past year – less than half the average rate before the global financial crisis – and a key risk is that these subdued growth rates continue.

Here’s Mark Carney’s full statement.

Updated

Last night’s Greek cabinet meeting focused on changes to the tax system, and possible privatisations, ahead of today’s talks with creditors today.

The Kathimerini newspaper adds:

Officials also discussed the possible timing for drafting some of these changes into legislation in a bid to show good will and convince the European Central Bank to relax liquidity restrictions on Greece.

Greece tells its negotiators to speed up

Greece’s government has instructed its negotiating team to speed up the talks with its lenders, in an attempt to bridge the gaps before it runs out of funds.

The Athens government issued the instructions after a late-night cabinet meeting, which was overshadowed by the news that Greece was back in recession.

However, Greece has not caved in, yet, on issues such as pension reform and workers’ rights.

Reuters has the details:

Greece’s negotiating team will continue talks with the country’s international creditors to reach a cash-for-reforms deal, a government official said after a cabinet meeting chaired by Prime Minister Alexis Tsipras.

“The cabinet authorised the negotiating team at the Brussels Group to continue talks starting on Thursday, aiming at a mutually beneficial agreement,” the official said.

“The instructions given to the negotiating team were to move in such a way to speed up the process.” However, the leftist government’s red lines have not changed, the official added.

The cabinet also discussed a planned VAT tax reform in order to be ready to legislate, depending on the progress of the negotiations.

Greek govt authorised team in Brussels Group to achieve 'mutually beneficial agreement'. That's it #Greece #Eurogroup

— Daphne Papadopoulou (@daphnenews) May 13, 2015

The Agenda: Mark Carney and Mario Draghi speak

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

We’ll be tracking two of the world’s most powerful central bankers today.

Mark Carney, governor of the Bank of England, is due on Radio 4’s Today Programme his morning, at 8.10am. He’ll be discussing the state of the UK economy, a day after the BOE cut its growth forecasts and warned that productivity remains disappointingly weak.

Mario Draghi, head of the European Central Bank, is in Washington today to give the Camdessus Central Banking Lecture. That starts at 11am East Coast time or 4pm BST.

Draghi will then hold talks with the International Monetary Fund; the Greek debt crisis will be high on the agenda.

#IMF's Lagarde & #ECB's Draghi to meet in Washington today + IMF Executive Board to be briefed on #Greece by Europe Dept head Poul Thomsen .

— Yannis Koutsomitis (@YanniKouts) May 14, 2015

In the City, shares are expected to dip this morning as the recent turbulence in the bond market hits confidence.

Oanda senior market analyst Craig Erlam explains:

“The bond market moves are making investors quite anxious. I think everyone expected yields to rise once we started to see a bounce in oil prices as, naturally, this would change people’s inflation outlook...

“The pace at which they’ve risen has been quite surprising, which is probably a consequence of a lack of liquidity in the market at the moment. A small change in attitude can have a much greater impact.”

I’ll be tracking all the main developments through the day.