Closing summary

Before we close up for today, here is a summary of the main events:

- It was officially confirmed by eurogroup minister Jeroen Dijsselbloem on Twitter

- As details of the proposals emerged, commentators concluded that it amounted to a climbdown for Athens

- The European Commission welcomed the plans and said they could pave the way to eurozone stability

Greek shares remain up, with the ATG index up 1% at 856.5.

Other major European markets - apart from the FTSE 100 - are up slightly (by less than 1%) on hopes that a Greek deal can still be struck.

The FTSE is down slightly by 0.1% at 6,888.62.

Thank you for reading the blog today and for all your comments. Please join us again tomorrow when we will be bringing you coverage of the crucial eurogroup meeting of finance ministers in Brussels. AM

Kate Connolly, the Guardian’s Berlin correspondent, brings us more on Germany’s rejection of Greek proposals:

Schauble continues to insist that Greece sticks to the bailout conditions agreed with previous governments under which financial support will be given only in exchange for substantial structural reforms.

The finance ministry’s position risks deepening splits within Europe over how to deal with Greece as an end of February deadline nears at which the previous bailout agreement with its creditors and the European Central Bank runs out, leaving Greece facing bankruptcy.

In contrast to Berlin, the EU commission president Jean-Claude Juncker welcomed the Greek application, saying in his opinion it could pave the way for a “sensible compromise in the interest of financial stability in the Eurozone as a whole”.

But experts said Greece was merely playing for time, and that its application had indeed contained no new commitments. “The Greeks have simply tried to pass the buck back to the middle,” Matthias Kullas from the Centre for European Politics in Freiburg told The Guardian.

He stressed the German reaction was not a rejection over reaching a compromise with Greece, but did mean that expectations of an agreement on Friday when finance ministers from the eurogroup meet again, were now “slim”.

“If an agreement is reached, it will be at the last minute,” he said. “It’s in the interest of both sides to stick to their guns. The earlier one of them diverts from his course, the weaker his position becomes and the more elbow room he leaves for the other.”

S&P: Greek exit would have limited contagion risk

Ratings agency Standard & Poor’s says a Greek exit from the euro would have limited direct contagion frisks for other sovereigns.

S&P credit analyst Moritz Kraemer:

All things considered, we believe that a Grexit would not lead to a degree of direct contagion that would drive other sovereigns out of the euro, not least because the eurozone rescue architecture is more robust than during the last Grexit scare in 2012.

We believe that the financial burden of a Grexit on the remaining 18 eurozone sovereigns would be moderate and absorbed over decades, and we therefore do not expect that a Grexit, by itself, would have significant rating implications for these sovereign.

S&P says there are a number of reasons why the situation is less risky than it would have been in 2012. Reasons include:

- The eurozone now has the European Stability Mechanism (ESM), which can financially support eurozone sovereigns under market pressure following a hypothetical Grexit.

- Greece’s links with financial markets have been sufficiently reduced to make such a direct contagion less likely.

- The disparity between Greek sovereign bond yields and those of other eurozone sovereigns also suggests that investors consider that redenomination risk of other eurozone sovereigns is currently low. Whereas Greek sovereign debt yields have risen in recent months along with uncertainty about Greece’s relationship with its lenders, bond yields of other so-called “periphery” sovereigns (Italy, Ireland, Portugal, and Spain) have fallen to all-time lows.

Greece: it's this deal or no deal

Reuters says the message from Greece is that eurogroup finance ministers have two options tomorrow - accept the deal it has put on the table or reject it.

- 19-Feb-2015 14:29 - GREEK GOVT SAYS EUROGROUP TOMORROW HAS ONLY TWO OPTIONS, TO EITHER ACCEPT OR REJECT OFFER MADE BY GREECE TODAY

- 19-Feb-2015 14:30 - GREEK GOVT SAYS EUROGROUP’S DECISION WILL SHOW WHO WANTS A SOLUTION AND WHO DOES NOT

Helena Smith brings us this update from Athens:

Eery silence from Greek officials on Germany’s rejection of Athens’ proposal. Insiders expressed surprise that officials had “had the time” to properly contemplate the request but refused to be drawn further. When the response comes it will come from the top, they said.

Meanwhile, however, comments by former French president Valery Giscard d’Estaing re Greece leaving the euro zone have caused some commotion.

The former president, who worked hard to promote Greece’s entry to the European Union described Athens’ admission to the single currency in 2001 as “evidently a mistake” this morning and advocated that the debt-stricken now make a “friendly exit.”

One Greek official told me the former president’s intervention was “less than helpful at such a sensitive time. Old leaders should learn to shut up, he said.

Main thing is #Schaeuble remains loyal to his principles! #Greece #eurogroup pic.twitter.com/CllKLM00LN

— Keep Talking Greece (@keeptalkingGR) February 19, 2015

Updated

A reader has kindly pointed out an important typo in my 12.53 post on the euro.

It should have read (and now does):

Germany’s tough stance on Greece (rejecting its bailout extension plan) has sent the euro lower, down 0.3% against the dollar at $1.13595.

Apologies for the confusion.

“The white flag has been raised over Athens” according to Larry Elliott, the Guardian’s economics editor.

He continues:

Greece has bowed to the intense pressure of its eurozone partners and will stick to austerity. After defiantly saying for the past three weeks that it will end the country’s fiscal waterboarding, the Syriza-led government is suing for peace.

That, bluntly, is the only way to interpret news that Greece has formally asked for a six-month extension to its bailout agreement. There is no longer the pretence that the bailout is to be replaced by a loan agreement with no strings attached. The hated troika of the European Central Bank, the European Union and the International Monetary Fund will be monitoring Greece’s economy for the next six months, something that has been anathema to Syriza until now.

The Greek government has some demands of its own. It wants to negotiate a new growth deal for the four years until 2019. It is asking for debt relief under the terms of the bailout agreement signed in November 2012. And it wants to be able to take steps to deal with the humanitarian crisis caused by the 25% collapse in the size of the economy over the past five years.

Developments in Greece have rather overshadowed the publication of the European Central Bank’s first set of minutes (which can be found here).

Jennifer McKeown, senior European economist at Capital Economics, says there are few surprises in the report from the meeting held on 22 January, at which the ECB agreed a €1.1tn programme of quantitative easing.

For one, the decision was not unanimous. McKeown comments:

The first ever timely publication of ECB minutes confirms that support for the new QE programme was not unanimous and highlights the Bank’s reluctance to take on more risk related to peripheral governments’ debts.

[The account] supports President Draghi’s explanation last month that while all members backed the idea of QE, some were not ready to implement it now. Members’ votes are not published.

But we know from information leaked previously that executive board Member Sabine Lautenschlaeger and the heads of the German, Dutch and Austrian central banks were all opposed at this stage.

The minutes also highlight discomfort with any policy that might appear to be bailing out indebted governments or that would put the ECB’s balance sheet at greater risk. We already had a good idea of this – the Bank explained last month that QE would be done largely at the risk of national central banks. But the account states that the decision was made “in view of concerns about moral hazard”.

Meanwhile, the decision to cap asset holdings at 33% of any individual government’s outstanding bonds was taken partly to “mitigate the risk of the ECB becoming a dominant creditor of euro area governments”.

Together with the Bank’s decision yesterday to allow only a meagre increase in emergency liquidity assistance for Greek banks, this makes clear that the ECB will not be riding to Greece’s rescue.

Some brutal headlines out of Germany at the moment: "Schäuble smashes Athens' request" etc pic.twitter.com/m2Y7m9Fsgy

— Mats Persson (@matsJpersson) February 19, 2015

Germany’s rejection of Greece’s proposals is a reminder of how volatile and changeable the situation is.

Kathleen Brooks, research director at forex.com:

The Greek crisis remains fluid, and the situation continues to change on a daily basis. Yesterday, the outlook was bleak until the ECB stepped in a boosted its emergency lending assistance to Greek banks. Today, the situation improved further on the back of news that the eurgroup will meet on Friday , which is a sign that Greece may have shifted its negotiating position to a more eurogroup-friendly stance. However, excitement is being contained after Germany said it would reject the deal proposed by Greece in its current form.

The Eurogroup meeting on Friday, the third in a week, comes after Greece requested a 6-month bailout extension. The good news is that, if approved, Greece will be able to pay back the EUR 21 billion of principal debt repayments that come due between now and August. The bad news, is that even if this extension is approved, we will be back in the same position in 6-months’ time and Greece’s long-term debt problems remain unsolved.

In the longer term, the apparent U-turn by the Greek government seems at odds with Syriza’s election pledge. This could put pressure on the new government to continue to demand a new bailout agreement without austerity conditions when the next round of Greek bailout negotiations come round sometime in the summer. Don’t expect the Greek crisis to go away just because of any “positive” developments in the next few days.

Greek assets have been knocked off their highs on the back of the German comments that it rejects Greece’s proposal, however 10-year yields remain below 10%. If the rest of the EU agrees with Greece’s proposal, then surely Germany will have to acquiesce? If they do then expect European risk assets to stage a rally, if not, then we could see a sharp increase in risk aversion.

Germany’s tough stance on Greece (rejecting its bailout extension plan) has sent the euro lower, down 0.3% against the dollar at $1.13595.

Greek shares are still up but to a lesser extent than earlier in the trading session. The ATG is up 0.8% at 854.17.

It's time for the #Eurozone to reject the German Finance Ministry @schieritz German finance ministry: letter from Greece not acceptable

— Sony Kapoor (@SonyKapoor) February 19, 2015

Confirmed. #Schaeuble refuses Greek request. Lack of supervision and commitment. http://t.co/ci15aHHcY3

— Carsten Brzeski (@carstenbrzeski) February 19, 2015

Updated

Germany says Greek proposals are insufficient

Germany has thrown a major spanner in the works, rejecting the proposals put forward by Greece.

Martin Jaeger, a spokesman for the German finance ministry, said in a statement:

The letter from Athens is not a proposal that leads to a substantial solution.

In truth it goes in the direction of a bridge financing, without fulfilling the demands of the programme. The letter does not meet the criteria agreed by the eurogroup on Monday.

Updated

The European Commission has welcomed the bailout extension request from Greece, claiming it could pave the way for compromise and stability in the eurozone.

A spokesman for Jean-Claude Juncker, EC President, said:

President Juncker sees this letter as a positive sign which, in his assessment, could pave the way for a reasonable compromise in the interest of the financial stability in the euro as a whole.

The detailed assessment of the letter and the response is now up to the eurogroup.

Updated

Guardian reporter Jennifer Rankin is in Brussels and bringing us updates on a potential deal for Greece.

She says eurozone officials are meeting in the Belgian capital today to assess the Greek proposals and lay the groundwork for the emergency meeting of eurogroup finance ministers tomorrow.

Greek finance minister Yanis Varoufakis has written to the president of the eurogroup, Jeroen Dijsselbloem, to put the bailout extension request into context.

Dear President of the eurogroup,

Over the last five years, the people of Greece have exerted remarkable efforts in economic adjustment. The new government is committed to a broader and deeper reform process aimed at durably improving growth and employment prospects, achieving debt sustainability and financial stability, enhancing social fairness and mitigating the significant social cost of the ongoing crisis.

The Greek authorities recognise that the procedures agreed by the previous governments were interrupted by the recent presidential and general elections and that, as a result, several of the technical arrangements have been invalidated. The Greek authorities honour Greece’s financial obligations to all its creditors as well as state our intention to cooperate with our partners in order to avert technical impediments in the context of the Master Facility Agreement which we recognise as binding vis-a-vis its financial and procedural content.

In this context, the Greek authorities are now applying for the extension of the Master Financial Assistance Facility Agreement for a period of six months from its termination during which period we shall proceed jointly, and making best use of given flexibility in the current arrangement, toward its successful conclusion and review on the basis of the proposals of, on the one hand, the Greek government and, on the other, the institutions.

The purpose of the requested six-month extension of the Agreement’s duration is:

(a) To agree the mutually acceptable financial and administrative terms the implementation of which, in collaboration with the institutions, will stabilise Greece’s fiscal position, attain appropriate primary fiscal surpluses, guarantee debt stability and assist in the attainment of fiscal targets for 2015 that take into account the present economic situation.

(b) To ensure, working closely with our European and international partners, that any new measures be fully funded while refraining from unilateral action that would undermine the fiscal targets, economic recovery and financial stability.

(c) To allow the European Central Bank to re-introduce the waiver in accordance with its procedures and regulations.

(d) To extend the availability of the EFSF bonds held by the HFSF for the duration of the Agreement.

(e) To commence work between the technical teams on a possible new Contract for Recovery and Growth that the Greek authorities envisage between Greece, Europe and the International Monetary Fund which could follow the current Agreement.

(f) To agree on supervision under the EU and ECB framework and, in the same spirit, with the International Monetary Fund for the duration of the extended Agreement.

(g) To discuss means of enacting the November 2012 Eurogroup decision regarding possible further debt measures and assistance for implementation after the completion of the extended Agreement and as part of the follow-up Contract.

With the above in mind, the Greek government expresses its determination to cooperate closely with the European Union’s institutions and with the International Monetary Fund in order: (a) to attain fiscal and financial stability and (b) to enable the Greek government to introduce the substantive, far-reaching reforms that are needed to restore the living standards of millions of Greek citizens through sustainable economic growth, gainful employment and social cohesion.

Sincerely,

Yanis Varoufakis

Minister of Finance

Hellenic Republic

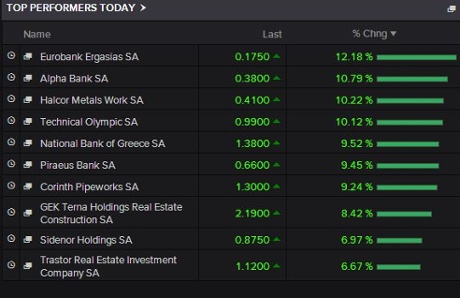

Greek investors are feeling increasingly optimistic that a deal can be struck between the government in Athens and the rest of the eurozone.

The main ATG index is now up 2.9% at 871.86. The Greek banks are among the main beneficiaries, partly because of the ECB’s agreement to hand them a €3.3bn liquidity extension.

If Greece has capitulated, officials are putting on a brave face according to Helena Smith, the Guardian’s correspondent in Athens.

Government officials close to prime minister Alexis Tsipras are sounding a triumphant note. Helena brings us this report:

The request for a sixth-month extension of the financial assistance programme propping up the country’s economy is “in total accordance” with the leftist-led government’s electoral mandate, prime ministerial aides insist.

“It respects the popular will, promotes the dignity of [our] society and at the same time is acceptable to our partners,” officials were quoted as saying in the financial daily, Naftemporiki, adding that it would provide a “protective umbrella to Greece’s financial system” while allowing its austerity-whipped society to breathe.

Calling the request an “interim agreement,” well-placed insiders said the request was significant in two important domains: it raised the issue of debt restructuring and included a pledge from the new government to keep to a balanced budget.

“It’s not very often that you get left-leaning governments making those sort of commitments,” one told me. “They’ve clearly sought to strike a very fine balance between tackling the humanitarian disaster and promising to be a government that will not only tackle corruption and tax evasion, the malfunctions of Greek society, but take on all the invested interests that plague political and business life.”

Updated

Economists at German bank Berenberg believe there is a 65% chance that Greece will stay in the euro, but...

That leaves a 35% risk of Greek default and euro exit: In practice, this could happen in two ways: (1) the double populist coalition rejects the Eurozone offer and starts printing money; (2) Mr Tsipras calls a referendum which concludes in a vote for exit, despite 80% of Greeks currently wanting to stay.

In the first few months after the exit decision, Greece would have to survive a collapse of its financial system amid widespread default. Economic uncertainty and capital controls would trigger severe output contraction.

In the longer run, Greece’s future outside the eurozone would depend on its policy choices. A Venezuela/Argentina scenario of years of populist leadership eroding economic foundations looks most likely. Retaining or quickly regaining EU membership would be crucial for Greece.

Long-term consequences for the Eurozone would be mixed: On the one hand, Grexit could set a dangerous precedent. It could lead to higher risk premiums and, thus, borrowing costs in parts of the periphery. On the other hand, it would give bite to Europe’s rules. It would raise the incentives for good macro policies to safeguard euro membership and would deflate populists.

Commentators on Twitter say the Greek request appears to amount to a climbdown.

Looking as if #Greece & #Syriza folded in all but name & agreed extend current terms. If true, domestic fallout & party management difficult

— Open Europe (@OpenEurope) February 19, 2015

Is it me or has the Greek gov't just capitulated?

— Yannis Koutsomitis (@YanniKouts) February 19, 2015

Probably the most important part of #Greece extension proposal is the fact #Troika can stay and monitor

— Joshua Raymond (@Josh_CityIndex) February 19, 2015

More Reuters snaps:

- 19-Feb-2015 10:39 - GREECE SAYS EXTENSION SHOULD ALLOW EFSF TO EXTEND VALIDITY OF ITS BONDS FOR GREEK BANK RECAPITALISATION FOR SIX-MONTHS

- 19-Feb-2015 10:41 - GREECE SAYS BAILOUT EXTENSION WILL ALLOW GREEK, IMF, EUROPEAN TECHNICAL TEAMS TO NEGOTIATE POSSIBLE NEW CONTRACT FOR RECOVERY AND GROWTH

- 19-Feb-2015 10:42 - GREECE SAYS BAILOUT EXTENSION WOULD BE MONITORED BY THE TROIKA-DOC

- 19-Feb-2015 10:44 - GREECE SAYS DURING BAILOUT EXTENSION EURO ZONE AND ATHENS WOULD DISCUSS ENACTING FURTHER DEBT RELIEF MEASURES AS MENTIONED BY EURO ZONE MINISTERS IN NOV 2012-DOC

We have yet to hear from either the Greek finance minister Yanis Varoufakis or the Greek PM Alexis Tsipras on the bailout extension request.

But the noises coming out of Greece suggest the tone of the submission is reconciliatory.

- 19-Feb-2015 10:28 - GREEK REQUEST FOR BAILOUT EXTENSION SAYS ATHENS WILL HONOUR ITS FINANCIAL OBLIGATIONS TO ALL CREDITORS-DOCUMENT

- 19-Feb-2015 10:29 - GREECE RECOGNISES EXISTING BAILOUT AGREEMENT AS BINDING IN ITS FINANCIAL AND PROCEDURAL CONTENT-DOCUMENT

- 19-Feb-2015 10:33 - GREECE SAYS IT WILL PROCEED JOINTLY WITH EURO ZONE OVER NEXT 6 MONTHS TO SUCCESSFULLY CONCLUDE THE BAILOUT ON THE BASIS OF TROIKA, GREEK GOVT PROPOSALS

- 19-Feb-2015 10:35 - GREEK BAILOUT EXTENSION REQUEST SAYS NEXT 6 MONTHS WOULD BE USED TO AGREE ON “APPROPRIATE” PRIMARY FISCAL SURPLUSES

- 19-Feb-2015 10:36 - GREECE SAYS WILL REFRAIN FROM UNILATERAL ACTION THAT WOULD UNDERMINE FISCAL TARGETS, ECON RECOVERY AND FIN STABILITY-DOC

- 19-Feb-2015 10:38 - GREEK REQUEST SAYS THE EXTENSION SHOULD ALLOW THE ECB TO RETURN TO ACCEPTING GREEK GOVT PAPER AS COLLATERAL

Why set up meeting upon meeting? During WWII the Cabinet was in constant session. #Eurogroup

— Yannis Koutsomitis (@YanniKouts) February 19, 2015

A few more details are emerging on Greece’s request for a six-month bailout extension.

Reuters snaps, based on a conversation with a Greek government official:

- 19-Feb-2015 10:14 - GREECE IS COMMITTED TO FISCAL BALANCE DURING INTERIM PERIOD UNDER REQUESTED LOAN AGREEMENT EXTENSION - GREEK GOVT OFFICIAL

- 19-Feb-2015 10:15 - GREECE COMMITTED TO REFORMS IMMEDIATELY ON TAX EVASION AND CORRUPTION- GOVT OFFICIAL

- 19-Feb-2015 10:16 - GREEK PROPOSAL INCLUDES MEASURES TO DEAL WITH HUMANITARIAN CRISIS AND KICK START ECONOMY-GOVT OFFICIAL

- 19-Feb-2015 10:17 - GREEK GOVT’S SIX MONTH EXTENSION TO GIVE GOVT ROOM TO PROCEED WITH NEGOTIATIONS FOR A NEW GROWTH DEAL OVER 2015-2019 - GOVT OFFICIAL

- 19-Feb-2015 10:17 - GREEK GOVT OFFICIAL SAYS NEW DEAL WILL ALSO INCLUDE AGREEMENT ON DEBT REDUCTION

- 19-Feb-2015 10:17 - GREEK GOVT OFFICIAL SAYS SEEKING DEBT REDUCTION DEAL IN LINE WITH 2012 EUROGROUP AGREEMENT

Eurogroup finance ministers meeting will kick off at 3pm in Brussels (2pm UK time) tomorrow, the boss confirms.

#Eurogroup Friday in Brussels as of 15.00.

— Jeroen Dijsselbloem (@J_Dijsselbloem) February 19, 2015

Greece’s official bailout extension request has triggered an emergency meeting of the eurozone’s finance ministers on Friday.

It will be up to them to consider whether to accept or reject the Greek proposals.

Greece asks EU for loan extension, says government source http://t.co/5UTUs1br1N

— Kathimerini English (@ekathimerini) February 19, 2015

Eurogroup chief #Dijsselbloem confirms he has 'received Greek request for six months extension'

— Kathimerini English (@ekathimerini) February 19, 2015

Euro rises on hopes for Greek debt deal http://t.co/4JBZi8q7d3

— Kathimerini English (@ekathimerini) February 19, 2015

It is official! Jeroen Dijsselbloem, the eurogroup’s President, has confirmed receipt of Greece’s request for a six-month bailout extension.

Received Greek request for six months extension.

— Jeroen Dijsselbloem (@J_Dijsselbloem) February 19, 2015

Updated

A note of caution: the Guardian’s reporter Jennifer Rankin is in Brussels and says there is no official confirmation from either side that the Greek bailout extension request is in.

So far all we have to go on is a Reuters snap. More soon.

Greek market rises 1%

Greek investors are happy. The main ATG index is up 1% at 855.85.

The bailout extension request, combined with the ECB’s decision to extend an additional €3.3bn of funding to Greek banks, is driving confidence in Athens this morning.

Que Sera Sera - whatever will be will be .... The future's not ours to see - Que Sera Sera #Greece #Eurocrisis

— Sony Kapoor (@SonyKapoor) February 19, 2015

A Greek government official told Reuters the bailout extension has been requested. Specifically, Athens has requested an extension to the so-called “master financial assistance facility agreement” with the eurozone.

However, Greece is proposing to change some of the terms of the original agreement. We will bring you more detail and reaction as it comes.

Greece requests bailout extension

BREAKING: It’s happening. Greece has formally submitted a request to extend its bailout programme for six months.

Away from Greece, the European Central Bank will publish minutes of its latest policy meeting for the first time today.

The first set of minutes should be interesting, relating to the ECB’s crucial January meeting when it finally pushed the button on a €1.1tn programme of quantitative easing.

The minutes are scheduled to be published at 1.30pm CET (12.30pm UK time) and we will be following the story.

#ECB Set to Release Meeting Minutes for the First Time Ever. http://t.co/ItpK5Tcadv

— Holger Zschaepitz (@Schuldensuehner) February 19, 2015

European markets open lower

Europe’s major markets have opened slightly lower as investors pause to take in developments (or lack thereof) in Greece.

- FTSE 100: -0.4% at 6,867.03

- France’s CAC 40: -0.1% at 4,792.26

- Germany’s DAX 30: -0.3% at 10,932.25

- Spain’s IBEX: -0.1 at 10,784.5

- Italy’s FTSE MIB: -0.5% 21,555.09

ECB would like Greece to impose capital controls

The European Central Bank would be happier if Greece introduced capital controls according to a German newspaper.

It would allow the country to stem the amount of money flowing out of its banks and out of the country.

The Frankfurter Allgemeine Zeitung, a conservative paper, quotes an unnamed ECB source:

The ECB governing council and the ECB banking supervisor would be more comfortable if there were capital controls to prevent the banks bleeding money.

The rate at which deposits have been withdrawn from Greek banks has accelerated in recent days as the new government has so-far failed to reach an agreement with fellow member of the eurozone over a bailout extension.

Under the current agreement, the bailout expires on 28 February.

FAZ story on #Greece & #ECB: http://t.co/ZVne2cwdVE 'ECB GC would prefer that Greece introduces capital controls to prevent capital flight'

— Yannis Koutsomitis (@YanniKouts) February 19, 2015

Greece to submit loan request

Good morning.

It is another crucial day for the future of Greece. Athens is expected to submit its proposal for an extension to its loan agreement today, a day before eurozone finance ministers make a decision on whether to accept the terms.

What is unclear is precisely what terms Greece will seek, and what - if any - compromises the eurozone might be willing to make.

In an important development for Greece, the European Central Bank last night approved a €3.3bn extension of liquidity for the country’s banks.

It took the total funding on offer to €68.3bn. Greek banks are close to using up the €65bn emergency liquidity funds the ECB had already granted them. Read our full story here.