PS: Greece’s government spokesman (a reader of this blog, it seems) has got in touch to repudiate any suggestion that Greek savers could face a levy, as part of a new aid deal for Greece.

From Athens, Helena Smith reports

I just took a call from Gavriel Sakellarides hotly denying any notion that a bail-in is being considered.

“We exclude any such scenario,” Sakellarides told me adding that he only mentioned the subject at today’s daily briefing because a journalist brought it up.

“I was asked about it and wholeheartedly ruled it out. The stability of the financial sector and banking system is very important to us. Categorically there will be no bail in.”

Government sources are now saying that while they expect progress to be made by technical teams this week, a breakthrough is unlikely to happen by the time the EU summit begins on Thursday.

One insider said:

“The Riga summit will see progress on a technical level and perhaps meetings on the sidelines (between Greek prime minister Alexis Tsipras and his counterparts) but we don’t expect a deal to be agreed there. That will likely require an emergency eurogroup meeting before the end of May.”

It was vital, the source acknowledged, that an agreement was reached by the end of May “but that is also up to the other side too. We have already made lots of concessions. Labour market reform and pensions are the two things we are not going to go back on.”

Updated

Greek finance minister Yanis Varoufakis will get the chance to comment on today’s developments late night, when he’s interviewed by Star TV.

Enikos will be providing a live translation:

#Varoufakis live interview on Monday with simultaneous interpretation #Greece #enikos - http://t.co/2uJoqfyWg6 pic.twitter.com/nP7q7b17wQ

— enikos_en (@enikos_en) May 18, 2015

As that’s not until 11.30pm Greek time (9.30pm UK), I’m going to nail the lid down for the day, unless there are major developments tonight......

FT: Juncker plan shows tensions between creditors

Reports that Jean-Claude Juncker has been beavering away on a new Greek rescue plan has not amused the country’s other creditors, reports Peter Spiegel, the FT’s Brussels bureau chief.

Peter reckons that the proposal is one in a series of ideas being bounced between the Commission and Athens, rather than as concrete plan.

That explains why the plan offered various concessions to Greece (such as lower primary surpluses, and delayed tax rises)

And that could further hurt relations between the EC and its fellow lenders, he says:

It is now no secret that the Commission views the IMF and Berlin as being unreasonably hard-line in the Greek talks and Commission officials, including Juncker himself, have been trying to bridge differences between Athens and hard-line elements for weeks.

It is also no secret that many others involved in the talks are none-too-pleased with the Commission’s freelancing. Jeroen Dijsselbloem, the Dutch finance minister who leads the negotiations on the part of his fellow eurozone ministers, has been quite open about his unhappiness that the Commission tried to intervene without his knowledge back in February, when everyone was desperately trying to convince Athens to seek an extension of the current €172bn bailout before it expired.

The new Juncker effort could touch off similar recriminations, because it appears that none of the other players knew what Juncker was up to. “We are thunderstruck,” said one official involved in the talks, who said the ECB and the IMF – who are theoretically on a co-equal standing with the Commission when it comes to talks with Greek authorities – were unaware such a proposal was being mooted.

Even tho @EU_Commission distancing itself from @tovimagr scoop on #Greece "Juncker Plan", shows troika relations raw http://t.co/KcLnrzRG0j

— Peter Spiegel (@SpiegelPeter) May 18, 2015

Pierre Moscovici’s spokesman, Olivier Bailly, has just declined to confirm those reports of a new proposal to resolve the Greek crisis.

We can't confirm media allegations about @EU_Commission proposal on #Greece. Hard work continue towards deal, with #IMF @ecb & #eurogroup

— Olivier Bailly (@OlivierBaillyEU) May 18, 2015

“Can’t confirm” does leave some wriggle room, though...

Amid the confusion over Greece, London’s stock market has ended the day largely where it started.

The FTSE 100 ended the day up just 8 points, or 0.1%. Silver producer Fresnillo jumped 5%, tracking a rally in the price of silver. Pharmaceuticals company Hikma led the fallers down 1.4% after announcing the death of its cofounder Samih Darwazah (his family own 29% of the firm).

Most other European markets rose, although the Milan index fell over 1%, partly because several large Italian firm went ex-dividend (so new shareholders won’t qualify for the next payout).

- EUROPE’S FTSEUROFIRST 300 PROVISIONALLY CLOSES UP 0.4% AT 1,579.01 PTS

- FRENCH CAC 40 UP 0.3%, GERMAN DAX UP 1.3%

- SPAIN’S IBEX UP 0.6%

Breaking away from Greece..... activist investor Carl Icann has just declared that Apple shares should be worth almost double their current value.

Icann has renewed his pressure on the company to boost its share buyback scheme, with a new letter to CEO Tim Cook. In it, he claims Apple is actually worth $240 per share, not the $128 it is currently trading at.

BREAKING: Carl Icahn says Apple is worth $240/share today • http://t.co/0zyCjuOtzM

— CNBC Now (@CNBCnow) May 18, 2015

Icann writes:

Apple is poised to enter and in our view dominate two new categories (the television next year and the automobile by 2020) with a combined addressable market of $2.2 trillion, a view investors don’t appear to factor into their valuation at all.

He also cited Apple Watch, Apple Pay, Homekit, Healthkit, and Beats Music as further proof that Apple will only increase its domination, before riffing on the environmental factors that will drive demand for lithium-ion batteries.

The bottom line remains the same -- Apple should spend even more of its massive cash pile repurchasing its shares.

New open letter from Carl Icahn to Tim Cook http://t.co/dk45Kbxsl6

— Joseph Weisenthal (@TheStalwart) May 18, 2015

Updated

Now the intrigue starts......

If the #Juncker plan for #Greece is real, who wants to sink it by leaking it?

— Eric Maurice (@er1cmau) May 18, 2015

The Greek stock market staged a little rally after To Vima reported that EC president Juncker had proposed a compromise:

Greek stocks not hating the idea of a deal http://t.co/rUQoa79Z2d pic.twitter.com/OM5V4crSK5

— Mike Bird (@Birdyword) May 18, 2015

Unfortunately for Athens investors, the exchange closed for the day before the EC declined to confirm the story.

#junckerleak denial came late enough to give the people who did this to the ASE a night to have a good think about it pic.twitter.com/MdrwXmuNoY

— Marcus Bensasson (@mbensass) May 18, 2015

Updated

Greek insiders are also downplaying the idea that Jean-Claude Juncker has cracked the crisis:

Govment sources in #Greece deny the existence of a @EU_Commission /Juncker proposal on GR but say a deal is possible the coming days

— Symela Touchtidou (@stouchtidou) May 18, 2015

Updated

The EC has left itself some wriggle room, points out Danny Kemp, AFP’s deputy bureau chief in Brussels:

'Not aware' is a non-denial denial if ever I saw one #junckerleak

— Danny Kemp (@dannyctkemp) May 18, 2015

Perhaps the proposal seen by To Vima is tied up with this week’s EU leaders meeting in Riga? Perhaps it’s a draft plan, or an old plan? Perhaps it’s all a mistake. Perhaps we’ll never know....

EU Commission says not aware of any new #Juncker proposal for Greece @A_Breidthardt

— EfiKoutsokosta (@Efkouts) May 18, 2015

That semi-denial again:

-

EU COMMISSION SAYS NOT AWARE OF ANY NEW JUNCKER PROPOSAL FOR GREECE WITH LOWER PRIMARY SURPLUS TARGETS

Updated

EC 'can't confirm' Juncker plan is genuine

European Commission spokeswoman Annika Breidthardt says she cannot confirm that Jean-Claude Juncker has made a new proposal to break the Greek deadlock.

We’re still working towards a comprehensive deal, she adds.

Can't confirm media reports on @EU_Commission /Juncker proposal on GR. Not aware of such proposal. Working towards comprehensive deal.

— Annika Breidthardt (@A_Breidthardt) May 18, 2015

Teneo Intelligence’s Wolf Piccoli has his doubts too:

Juncker's emergency rescue plan for #Greece = Juncker's investment plan. Both unlikely to succeed

— wolf piccoli (@wolfpiccoli) May 18, 2015

At first glance, it’s not clear that Juncker’s new proposal contains enough reform measures to satisfy Greece’s creditors.

Delaying VAT rises, modifying labour reforms and lowering the primary surplus targets will all make a dent in Greece’s budgets. There’s no mention of new reforms to make up the gap.

Effectively it would unlock some aid for Athens today, in return for fiscal consolidation tomorrow.

To Vima: Juncker proposes Greek breakthrough

Greek newspaper To Vima is reporting that EC president Jean-Claude Juncker has proposed a deal to break the deadlock between Greece and its lenders.

This deal include smaller primary budget surplus targets (just 0.75% this year, down from 3%), and also delay VAT changes until after the summer. A review of the sustainability of the pension system would also be delated until the autumn.

The plan would also see Greece’s collective bargaining agreements reviewed in light of ILO guidance on ‘best practice’ to improve competitiveness and reduce unemployment.

However, Greece would still implement the unpopular ENFIA property tax.

In return, Greece’s lenders would hand over €1.8bn of loans, plus the €1.9bn of profits that the ECB has made on its Greek bonds.

Here’s the story (in Greek).

#Greece | Big scoop by @tovimagr: Juncker submits proposal to break Greek impasse. 0.75% surplus in 2015, 2% in 2016 http://t.co/qvmKT6rwK9

— Yannis Koutsomitis (@YanniKouts) May 18, 2015

According to To Vima, the plan is designed to “cut the Gordian knot”. It would remove the immediate danger of default and buy time for more negotiations over a new reform programme.

Paul Mason of Channel 4 is tweeting the key points now, along with some analysis:

My response to @tovimagr #Juncker leak. 1) IMF not likely to fund it. 2) It is a major throw of dice by @JunckerEU (1/5) #junckerleak

— Paul Mason (@paulmasonnews) May 18, 2015

Re #Junckerleak (2/5) 3. It funds Greece thru summer but delays debt restructure til autumn. 4. It keeps the ENFIA tax = greeks hate it

— Paul Mason (@paulmasonnews) May 18, 2015

#Junckerleak (3/5) as IMF recognieses - it’s a clear back loading of austerity, i.e. relaxation in Syriza’s favour

— Paul Mason (@paulmasonnews) May 18, 2015

#junckerleak (4/5) concedes to Syriza a delay on pension reform and hands them labour market reform because ILO supports Greek position

— Paul Mason (@paulmasonnews) May 18, 2015

#junckerleak doc would give Greece €5bn now but also opens up ECB access and ? QE… Syriza will hate some details but its a big relaxation

— Paul Mason (@paulmasonnews) May 18, 2015

(re that last tweet, I think it actually unlocks around €4bn of aid -- but all will become clear later)

Updated

Reuters has now published Pierre Moscovici’s comments in Berlin this morning, in which the European Commissioner warned that time is running out:

“Time available to reach an agreement at staff level is now, I would say, very limited,” said Moscovici. “We have got to conclude before the end of May.”

“The only scenario that we consider in the Commission is Greece in the euro zone,” said the commissioner, adding that his political experience had taught him it was best not to discuss a Plan B “because that means you don’t believe in Plan A”.

#Greece's bonds tumble on speculation banks weeks away from failure. 2yr yield jumps by 433bps http://t.co/GiFeaxv9rz pic.twitter.com/HEMIL8K0Bc

— Holger Zschaepitz (@Schuldensuehner) May 18, 2015

Lunchtime summary: May deadline looms.....

Another day, another deadline. A quick recap.

1) Greece’s government has warned that it needs to reach a breakthrough with its creditors to unlock bailout funds by the end of this month.

Government spokesman Gabriel Sakellaridis told reporters in Athens today that:

“A deal is required immediately, this is why we are talking about the end of May, to resolve these critical liquidity issues.”

Sakellaridis also insisted that Greece would not accept a one-off bank deposit levy to resolve the cash crisis, pledging no repeat of the Cyprus bailout of 2013.

2) Bank officials, though, fear that the very mention of a bail-in could encourage Greeks to tap their bank accounts. One told us:

Many see it as the logical next step and after today’s statement we expect the outflows to increase.”

3) The European Commission has dampened Athens’ hopes of a breakthrough could be achieved that a summit of EU leaders in Riga on Thursday. A political deal cannot replace the detailed technical negotiations needed to unlock bailout funds, an EC spokesman said.

4) Two leaks over the weekend have raised concerns over Greece’s future. One showed that the IMF won’t accept a “quick and dirty” fudge over the current aid programme, and fears that Greece can’t meet this summer’s repayments.

The second leak revealed that Greece feared it couldn’t meet last week’s €750m repayment to the Fund [before eventually using emergency funds at the IMF].

5) Uncertainty over Greece’s future has hit its sovereign debt today, driving up bond yields.

FXTM Market Analyst Jameel Ahmad explains:

“Greece is continuing to remain as a headline attraction in the news and unfortunately it is repeatedly for the wrong reasons.

If it wasn’t worrisome enough for investors that the Greek economy has basically allowed itself to slip back into a recession, then the reports that it only avoided a potential default to the IMF by using an emergency reserves account from the IMF, to repay the IMF, will send sentiment to new lows.

6) The German Bundesbank has also weighed in, warning that Greece faces insolvency if it doesn’t take substantial reforms.

Updated

Bank officials fear more withdrawals

Over in Athens, bank officials say they now expect more people to remove savings, despite the government promising today that it won’t impose a levy on deposits.

Our correspondent Helena Smith reports:

The government’s pledge to leave bank accounts untouched in its battle to keep bankruptcy at bay does not appear to have convinced investors. Bank employees have been speaking of a marked increased in withdrawals by depositors in recent weeks.

“People are taking more or less everything they have got out of their accounts for fear that the government will be dipping into them next,” said an official talking on condition of anonymity at the Bank of Greece.

“Many see it as the logical next step and after today’s statement we expect the outflows to increase.”

Around €35bn is thought to have been withdrawn from Greek bank accounts since last December. Economists, politicians, bankers and officials are convinced that a Cyprus-style bail-in, if executed, would be the straw that broke the camel’s back.

“We would see the revolt that this crisis has not yet produced. There would be blood in the streets. The Greeks are not like the Cypriots,” added the Bank of Greece official.

“It was wrong of the government to even raise it as a possibility and once again speaks more of its inexperience [in office].”

Meanwhile, prime minister Alexis Tsipras’ Syriza-led administration has been heavily criticised by former prime minister Antonis Samaras this morning.

Addressing the Federation of Greek Industries convention, Samaras accused the government of not only endangering the country’s future with increased talk of default and Grexit, but deluding Greeks.

“It is a government of non-decisions and it is still telling lies to the people,” said the head of the main opposition centre-right party, New Democracy.

Samaras added:

“It has promised everything to everyone and now it is telling lenders that they can’t pay [maturing debt], essentially pre-announcing a credit event.”

Moscovici: Time is running out

Another flurry of newsflashes just landed, from European commissioner for economic affairs, Pierre Moscovici.

He’s trying to sound optimistic, saying that Greece and her creditors are closer to a “common understanding”, but warns that time is short.

- EU’S MOSCOVICI SAYS EU AND GREECE HAVE MOVED CLOSER TO COMMON UNDERSTANDING IN A NUMBER OF AREAS

- EU’S MOSCOVICI SAYS TIME FOR AGREEMENT IS LIMITED, ONLY WAY FOR SUSTAINABLE RECOVER FOR GREECE IS WITHIN EURO ZONE

- EU’S MOSCOVICI SAYS THERE ARE SIGNALS THE GREEK GOV’T IS ENGAGING MORE CONSTRUCTIVELY ON PRIVATISATIONS

- EU’S MOSCOVICI SAYS EUROPEAN COMMISSION ONLY WORKING WITH SCENARIO OF GREECE STAYING IN EURO ZONE

Germany’s central bank has waded into the debate today, warning that Greece must make “substantial” reforms to avoid falling into insolvency.

The Bundesbank cited the Greek crisis in its regular monthly report, saying:

“The current Greek government is obliged to make appropriate proposals, to implement those agreements that have been reached and thereby do their part to avoid the insolvency of the state, with strong repercussions for Greece.

A sustainable solution is not possible without substantial reform in Greece....

The Bundesbank also urged policymakers to hold Greece to its commitments:

Financial help should be linked to the relevant preconditions

Greek government debt is taking a pummelling today.

The yield (or interest rate) on two-year bonds has jumped from 21.1% to 24%, showing a higher risk that Athens could default on the debt.

Greek 2-year yield now through 24% +300bps today. Ugly. pic.twitter.com/PJHjUKgQBP

— Jonathan Ferro (@FerroTV) May 18, 2015

The European Commission has just dampened hopes of a political breakthrough when EU leaders gather in Latvia on Thursday and Friday.

Margaritis Schinas, the EC’s top spokesman, told reporters in Brussels that negotiations over Greece’s reform programme have still not reached a deal, and are proceeding too slowly.

- EU COMMISSION SAYS PROGRESS IS MADE IN TALKS WITH GREECE, BUT AT A SLOW PACE AND MORE EFFORT NEEDED TO BRIDGE GAPS

- WHATEVER HAPPENS IN RIGA CANNOT BE A SUBSTITUTE FOR BRIDGING THE GAPS IN NEGOTIATIONS WITH GREECE- EU COMMISSION

At midday presser, @MargSchinas being v careful on #Greece at Riga summit, but clearly signalling that's not place for a bailout deal

— Peter Spiegel (@SpiegelPeter) May 18, 2015

The Greek government’s promise not to confiscate bank deposits has caused a flurry of concern among commentators and market experts:

No one is suggesting or implying Cyprus-style bail-in of deposits for #Greece and suddenly Sakellaridis needs to deny such a scenario.

— Yannis Koutsomitis (@YanniKouts) May 18, 2015

Now everyone is talking about the possibility of bail-in. That's a serious gaffe.

— Yannis Koutsomitis (@YanniKouts) May 18, 2015

#GREECE #SAKELLARIDES: NO BAIL-IN PLAN SUCH AS CYPRUS; NO THIRD BAILOUT

— Ishaq Siddiqi (@IshaqSiddiqi) May 18, 2015

Why did they have to go and say something silly like that? https://t.co/Sn9gxWjVyb

— Mike van Dulken (@Accendo_Mike) May 18, 2015

A snap summary of the Greek government’s press briefing:

#Greece govt spox Sakellaridis: "There will be no Cyrpus-like solution! There will be no bail-in alternative. GR govt won't sign new MoU!"

— The Greek Analyst (@GreekAnalyst) May 18, 2015

And the markets don’t like the sound of it; Germany’s DAX has shed its early gains, and the FTSE 100 has now dipped into the red.

Greek government spokesman Gabriel Sakellaridis added that Athens won’t implement a “Cyprus-style” solution, such as imposing losses on bank depositors.

Govt spokesman Sakellaridis: Government won't sign 3rd bailout or agree to Cyprus-style solution #Greece pic.twitter.com/7uTaxnXEOF

— Derek Gatopoulos (@dgatopoulos) May 18, 2015

*GREECE WON'T IMPOSE DEPOSITOR BAIL-IN, GOVT SPOKESMAN SAYS

— lemasabachthani (@lemasabachthani) May 18, 2015

Greece hopes to conclude talks in May

Newsflashes are coming in from Athens, showing that the Greek government hopes to reach a deal by the end of May.

But spokesman Gabriel Sakellaridis also insisted that Greece is still sticking to its “red lines”.

And as flagged up earlier, the EU leaders’ summit in Riga on Thursday and Friday is seen as crucial.

- GREEK GOVERNMENT SPOKESMAN SAYS FOUR RED LINES REMAIN IN TALKS WITH LENDERS - PENSION CUTS, GROWTH PLAN, PRIMARY SURPLUS TARGET AND DEBT RESTRUCTURING

- GREEK GOVERNMENT SPOKESMAN SAYS GOVT AIMS TO MAKE ALL PAYMENTS, WHEN ASKED ABOUT JUNE 5 IMF PAYMENT

- GREEK GOVERNMENT SPOKESMAN SAYS CONFIDENT DEAL WITH LENDERS WITH FALL WITHIN MANDATE SO BOTH COALITION PARTIES CAN SUPPORT IT

- GREEK GOVERNMENT SPOKESMAN SAYS WE ASSUME MAY IS THE MONTH WHEN TALKS WITH LENDERS WILL CONCLUDE

GREECE HOPES FOR POLITICAL AGREEMENT AT RIGA SUMMIT: SPOKESMAN

— Jonathan Ferro (@FerroTV) May 18, 2015

Hope springs eternal, but I can’t see how it translates into a deal unless there is compromise over those key economic reforms.

Nor can Teneo Intelligence’s Wolf Piccoli:

how do you say "wishful thinking" in Greek? or it is mere day-dreaming? https://t.co/aY0iDgWi01

— wolf piccoli (@wolfpiccoli) May 18, 2015

Updated

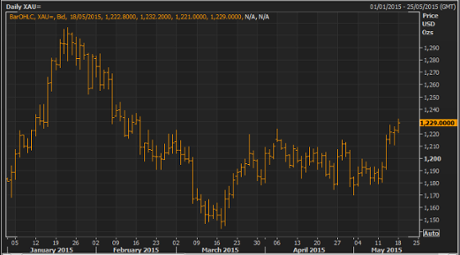

The price of gold has hit a three-month high this morning, touching $1,230 per ounce for the first time since mid-February.

Demand for gold has risen after last week’s disappointing economic data, showing US consumer confidence and industrial production had dipped.

But Sebastien Marlier, commodities analyst at the Economist Intelligence Unit, warns that this situation won’t last:

Gold will take a hit when the Fed eventually raises interest rates later this year.”

Two issues are looming over the UK this morning; Britain’s position in Europe, and the new government’s fiscal plans.

Manufacturing firm JCB has shifted the tone of the debate over Brexit, saying Britain leave the European Union if David Cameron can’t cut the red tape holding back UK firms.

Britain’s civil servants are bracing for hefty job cuts when George Osborne presents a new budget on July 8.

Chocolate maker Thorntons has announced the departure of its CEO, following some disappointing financial results:

And sales at sausage maker Cranswick are going with a bang.

It reported today that revenues broke through the £1bn mark for the first time, including a 23% jump in exports outside the European Union.

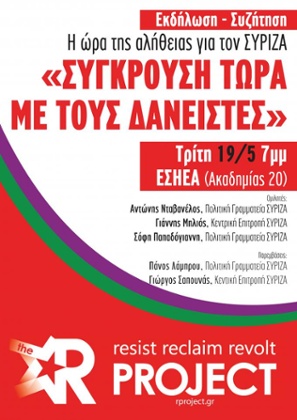

Syriza members to discuss 'rupturing' from lenders.

A group of influential members of the Syriza coalition have called a meeting tomorrow to discuss whether Greece should split from its creditors, rather than swallow fresh austerity.

Eurocrisis expert @GreekAnalyst reports that the gathering on Tuesday night will be attended by several “prominent” members of the left-wing group which won power in January, including:

Antonis Davellos (SYRIZA Political Secretariat), John Millios (SYRIZA Central Committee), Sofi Papadogianni (SYRIZA Political Secretariat), Panos Lambrou (SYRIZA Political Secretariat), George Sapounas (SYRIZA Central Committee).

The event captures the tensions at the heart of this crisis -- how can Syriza meet its pre-election pledges and stay true to its beliefs, while also committing to reforms that will allow its European partners to keep providing loans?

Here’s a flavour:

We need to choose between the signing of the looming austerity agreement and the rupture with the lenders. SYRIZA cannot be turned into a party of austerity; neither can the government implement the Memorandum. This is the reason why, both domestically and abroad, proposals for the internal “cleansing” of SYRIZA and governmental solutions for “national unity” are put on the table.

For all those reasons, the only way out is the choice of rupture with the lenders.

Call for "rupture now" by the Political Secretariat & Central Committee of #Syriza http://t.co/cGcxZlGExD #Greece

— The Greek Analyst (@GreekAnalyst) May 18, 2015

Updated

June is going to be a tense month, unless a deal does come soon.

Here's an update on Greece's repayment schedule h/t @SocieteGenerale pic.twitter.com/6AZFIUF5WX

— Josie Cox (@JosieCoxWSJ) May 18, 2015

Updated

Greece’s short-dated bonds are also weakening this morning:

Greek yields this morning: 2y +110bps 4y +106bps 10y +26bps

— RANsquawk (@RANsquawk) May 18, 2015

Robin Bew of the Economist Intelligence Unit reckons a Greek breakthrough will come in time, but it’s going to be a nailbiter....

Rumours that #Greece told #IMF it would miss last weeks payment, it was so tight. Think 60% chance of deal by end June. But 40% Grexit

— Robin Bew (@RobinBew) May 18, 2015

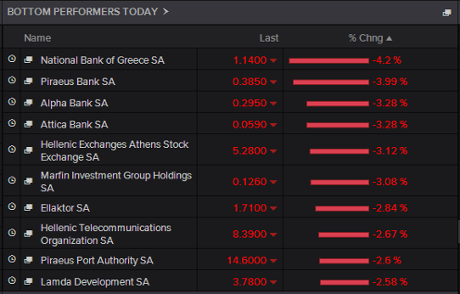

Default fears hit Greek stocks

The Athens stock market has fallen by 1.5% in early trading, as traders fret about the slow pace of progress.

Financial shares are leading the fallers; the main banks are down at least 3%.

Greek bonds are also suffering, following the news that the IMF fears Greece cannot meet its looming repayments (see opening post).

The yield on 10-year government debt has risen to 11.3%, from 10.9% on Friday night, showing that Greece’s debt is seen as riskier.

Investors are pricing in a higher danger of default too:

Greek 5yr default probability jumps as #Greece gets crunched on two fronts. http://t.co/Y4hTpTtCBr pic.twitter.com/dWowgqiVTI

— Holger Zschaepitz (@Schuldensuehner) May 18, 2015

Updated

Greece’s finance minister, Yanis Varouvakis, will give his views on the crisis tonight when he’s interviewed on Greek TV.

Enikos will be providing a simultaneous translation into English (they reckon it doesn’t start until 11.30pm local time, alas)

#Varoufakis live interview on Monday with simultaneous interpretation #Greece #enikos - http://t.co/2uJoqfyWg6 pic.twitter.com/nP7q7b17wQ

— enikos_en (@enikos_en) May 18, 2015

De Guindos added that Europe does not have a “Plan B” for Greece - it wants the country to stay in the eurozone, and meet its commitments.

Spain’s Finmin Guindos: There is no wriggle room in bailout talks for Greece; there is no Plan B

— Live Squawk (@livesquawk) May 18, 2015

Spanish minister: Still optimistic about Greece

Spain’s finance minister, Luis de Guindos, hasn’t given up hope over Greece.

He just told reporters in Madrid that an agreement can be reached in the coming days, despite so much time having been frittered away.

Maria Tadeo, Bloomberg’s Madrid correspondent, has tweeted the details:

Guindos says he's 'optimistic' about greece, says deal can be achieved within days although a lot of time has been wasted

— Maria Tadeo (@mariatad) May 18, 2015

Updated

Greek fears appear to be weighing on the euro this morning. The single currency has lost half a cent against the US dollar in early trading, to $1.1398.

Stan Shamu of IG reports that investors are cautious this morning:

Greece will be front and centre this week as the country looks to secure a deal with its creditors while avoiding harsh austerity.

Greece still hopes a deal can come soon

Greece’s government remains optimistic of a deal soon, perhaps at a summit meeting of EU leaders in Riga on Thursday and Friday.

Nikos Filis, spokesman for the parliamentary group of Prime Minister Alexis Tsipras’s Syriza party, told the Mega TV that:

“We’re striving for a mutually beneficial agreement by Friday.

However, Athens isn’t capitulating over its red lines (as the IMF confirmed in that leaked document). Filis explained:

“Our mandate from the Greek people is to reach an agreement where we stay in the euro area without harsh austerity measures.”

Introduction: Growing fears over Greece's finances

Good morning, and welcome to our rolling coverage of the world economy, the financal markets, the eurozone and business.

Are we approaching the Greek endgame? Two documents published over the weekend show that Athens’ financial situation is increasingly fraught, as time to reach a deal with its creditors runs out.

The first missive came from the International Monetary Fund, and was leaked to Paul Mason of Channel 4 on Saturday. It shows that the Fund believes there is “no possibility” of Greece meeting the payments due over the summer unless some bailout funds are unlocked soon.

The letter said there was still only limited progress between the two sides, while Greece is actually retreating on structural reforms.

More here: IMF leak signals ‘progress’ with Greece, but threat of default in June

And it also warns that IMF will not accept a “quick and dirty” compromise to resolve the deadlock -- suggesting it might not hand over its share of the €7bn in outstanding bailout funds.

Leaked #IMF confidential memo on #Greece. /via @paulmasonnews pic.twitter.com/UFeqGKlWah

— Yannis Koutsomitis (@YanniKouts) May 16, 2015

Sobering stuff. And that was compounded by news of a second letter, this time sent by Alexis Tsipras to the Fund last week, warning that Greece was almost out of cash.

The FT’s Peter Spiegel reports:

Greece came so close to defaulting on last week’s €750m International Monetary Fund repayment that the prime minister warned IMF chief Christine Lagarde he could not pay it without EU aid.

Athens ultimately made the payment without financial assistance from the bloc but only by tapping a rarely used emergency account Greece holds at the fund — an unorthodox transaction that amounted to borrowing IMF funds to pay the IMF.

Alexis Tsipras wrote to Ms Lagarde, warning that the IMF repayment would be missed unless the European Central Bank immediately raised its curbs on Greece’s ability to issue short-term debt.

More here: Tsipras letter reveals precariousness of Greece’s finances

As well as being ‘unorthodox’, the solution also can’t be repeated -- meaning next month’s payments are a new challenge:

How long can #Greece carry on? There’s not much left over to make even small(ish) payments due to #IMF in June. (BBG) pic.twitter.com/mDESz6Xoge

— Holger Zschaepitz (@Schuldensuehner) May 18, 2015

We’ll be tracking all the main developments through the day....

Updated