Greece has pledged to pull together a comprehensive list of reforms by the start of next week, in an attempt to unlock fresh funds before Athens runs out of cash in April.

Government spokesman Gabriel Sakellaridis said on Tuesday that the programme demanded by Greece’s increasingly impatient creditors would be finished within days.

“It will be done at the latest by Monday,” Sakellaridis told Mega TV, potentially teeing up another crunch meeting in Brussels to decide Greece’s future within the eurozone.

Although Greece’s financial position remains perilous, there are signs that Alexis Tsipras’s visit to Berlin on Monday improved ties between the eurozone’s largest member and its smaller, indebted neighbour.

The German foreign minister, Frank-Walter Steinmeier, declared that relations between the two countries have improved.

“I’m pleased that the atmosphere in German-Greek talks in recent days has changed and improved significantly,” Steinmeier told reporters in Berlin.

Greek government bonds strengthened on Tuesday on hopes of a breakthrough. The yield on Greece’s two-year debt fell from nearly 22% to 20%, a level that still suggests a high risk of default or restructuring.

The UK chancellor, George Osborne, gave an insight into how toxic relations had become in recent weeks as Athens tried to break away from its austerity programme.

“The risks of Greece leaving are rising, because the ill-will around the table is palpable between the eurozone and Greece,” Osborne told parliament’s Treasury select committee.

Britain must be prepared for the danger that Greece leaves the eurozone through “accident … or misjudgment”, Osborne added.

The billionaire investor-turned-philanthropist George Soros also remained gloomy, claiming there is a 50:50 chance that Greece will eventually leave the eurozone.

“It’s now a lose-lose game and the best that can happen is actually muddling through,” Soros told Bloomberg, adding that:

Greece is a long-festering problem that was mishandled from the beginning by all parties.

Greece must present a credible list of reforms to its creditors soon, to unlock the €7.2bn (£5.3bn) of bailout funds still available under its existing financial programme. Its financial position remains very fragile, with €467m due to be repaid to the IMF on 9 April.

One source told Reuters that Greece would run out of funds by 20 April without additional help.

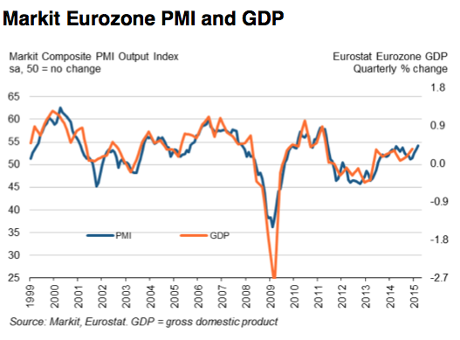

There are signs that the wider eurozone economy is recovering. The region’s private companies are now growing at the fastest rate since May 2011, according to Markit’s latest survey of the sector.

New order growth and job creation in the periphery, excluding Germany and France, was both the strongest since mid-2007.

Chris Williamson, chief economist at Markit, says the eurozone’s economic recovery “gained further momentum in March”.

The improvement provides welcome news to a region awaiting signs that the ECB’s quantitative easing is stimulating the real economy.