Some late news: The European Central Bank’s governing council has ended its deliberations.

And the word from Frankfurt is that Greece’s banks will be given an extra 2 billion euros emergency liquidity, taking the ELA total up to 78.9bn euros.

But that’s not all. After “intense” discussions, the ECB had decided not to change the ‘haircut’ applied to the assets Greek banks hand over as collateral for the ELA. But they will reconsider it next week, after Monday’s eurogroup meeting.....

Breaking now on Bloomberg: #ECB gives #Greece benefit of doubt for another week, before discussing tighter funding. #eurogroup #may11

— Jeff Black (@Jeffrey_Black) May 6, 2015

European markets edge higher despite Yellen comments

With talks between Greece and its creditors continuing - and the Brussels group of the ECB, IMF and EU maintaining they are working hard together to find a solution - shares have edged higher, even as bonds across the eurozone continue to slip. Stock markets were also unsettled by comments from US Federal Reserve chair Janet Yellen that equity values were “quite high” and potentially dangerous. However Wall Street reacted more than European markets to this warning. The final scores showed:

- The FTSE 100 is up 6.16 points at 6933.74

- Germany’s Dax has added 0.2% to 11,350.15

- France’s Cac has closed up 0.15% at 4981.59

- Italy’s FTSE MIB finished up 0.37% at 22,659.85

- Spain’s Ibex ended 0.43% higher at 11,163.6

- The Athens market jumped 2.86% to 816.94

On Wall Street, the Dow Jones Industrial Average is currently down 85 points or 0.48%.

On that note it’s time to close up for the evening. Thanks for all your comments, and we’ll be back tomorrow.

And there is even some optimism around about Greece now:

Productive call between Tsipras and @JunckerEU today on key reforms for #Greece. #ECB also upped liquidity assistance. Things looking up?

— Simon Marks (@MarksSimon) May 6, 2015

Speculation on the ECB’s decision on liquidity for Greek banks:

ECB SAID TO RAISE ELA CEILING FOR GREEK BANKS TO EU78.9BLN

— MineForNothing (@minefornothing) May 6, 2015

@minefornothing 2bln increase

— MineForNothing (@minefornothing) May 6, 2015

.@yanisvaroufakis has proposed bad bank to take bad loans off bank balance sheets. But bad loans total €72bn who will fund the bank?

— Open Europe (@OpenEurope) May 6, 2015

Updated

Some speculation on the timing of the European Central Bank’s decision on whether to keep supplying emergency liquidity assistance to Greece’s banking sector, following today’s meeting:

Decision on ELA for Greece will be communicated in writing around 21:00 CET Wednesday - source.

— Morris Cabrioli (@insidegame) May 6, 2015

ECB board discussed various Greece haircut scenario http://t.co/IcAMwzTm3P

— Morris Cabrioli (@insidegame) May 6, 2015

Back with Greece and former prime minister George Papandreou has added his voice to the current debate:

*PAPANDREOU SAYS GREEK EXIT WOULD HAVE GEOPOLITICAL REPERCUSSION #Greece #Grexit

— Advisory Desk (@advdesk) May 6, 2015

*PAPANDREOU SAYS GREEK EURO EXIT WOULD CAUSE EUROZONE UNRAVELING #Greece #Grexit

— Advisory Desk (@advdesk) May 6, 2015

Yellen warns on high stock market values

Earlier Federal Reserve chair Janet Yellen caused some tremors in the markets by warning about high valuations.

Speaking at a Finance and Society conference in Washington, she said:

I would highlight that equity market valuations at this point generally are quite high. There are potential dangers there.

Updated

“Concrete progress” is now the aim for Monday’s eurogroup meeting, according to a joint statement from the European Commission, the European Central Bank and the International Monetary Fund:

The European Commission, the European Central Bank and the International Monetary Fund share the same objective of helping Greece achieve financial stability and growth.

The institutions continue to work closely together toward that goal.

All three institutions are working hard to achieve concrete progress on 11 May.

This appears to be a reply to Greece’s accusations that divisions between the creditor group are causing problems with resolving its financial difficulties.

Greece talks are clearly not going well pic.twitter.com/qS9uJJSh2L

— Bruno Waterfield (@BrunoBrussels) May 6, 2015

Updated

The European Central Bank has issued a list of 8 banks which will face stress tests and balance sheet reviews, while Portugal’s Banco Novo will face a stress test only. The moves because of their increased systemic significance since the ECB’s last health check last year.

ECB Decision On Identifying Credit Institutions That Are Subject To Comprehensive Assessment http://t.co/6F6NGDk3jJ

— Live Squawk (@livesquawk) May 6, 2015

The banks are:

Belgium

Banque Degroof S.A.

France

Agence Française de Développement* Luxembourg

J.P. Morgan Bank Luxembourg S.A.*

Malta

Mediterranean Bank plc*

Austria

Sberbank Europe AG VTB Bank (Austria) AG

Portugal

Novo Banco, SA (only for the stress test)

Slovenia

Unicredit Banka Slovenija d.d.

Finland

Kuntarahoitus Oyj (Municipality Finance plc)*

Updated

Oil prices have climbed further after US crude stocks fell last week for the first time since January.

Brent crude is now up around 2.4% at $69.14 as the US energy information administration said inventories dropped by 3.9m barrels compared to expectations of a 1.5m increase.

But crude is still well down from its highs:

Keeping the crude oil (Brent) rebound in context pic.twitter.com/8cJHFZZAaP

— Eric Burroughs (@ericbeebo) May 6, 2015

Greek finance minister Yanis Varoufakis has said next week’s eurogroup meeting could serve as a “platform” for a deal.

Hopes of a real breakthrough at Monday’s meeting have pretty much faded but as Varoufakis continued his meetings with EU minister, he held out the hope that it could at least be another step on the road to an agreement. Varoufakis was speaking after a meeting with Italian economy minister Pier Carlo Padoan and said their discussion had given him confidence that an agreement could be reached. He told reporters (quote from Reuters):

We had a very fruitful and intense exchange of views on the best ways to make the eurogroup next Monday a platform to enter into the kind of agreement between Greece and our partners which not only resolves the current negotiations but will lead to a period after June that will allow the Greek economy to recover and grow again.

Juncker and Tsipras issue statement

Update: EC President Jean-Claude Juncker and Greek prime minister Alexis Tsipras have just issued a joint statement following their phone call:

It shows that they discussed the key points of difference between Greece and her creditors, and agreed that Greece needs a better pay bargaining mechanism.

President Juncker and Prime Minister Tsipras spoke on the phone today.

They took stock of progress made in the talks between Greece and its partners over the last days on a comprehensive set of reforms to achieve a successful completion of the review. They notably discussed the importance of reforms to modernise the pension system so that it is fair, fiscally sustainable and effective in averting old-age poverty. They also discussed the need for wage developments and labour market institutions to be supportive of job creation, competitiveness and social cohesion. In this context, they concurred on the role of a modern and effective collective bargaining system, which should be developed through broad consultation and meet the highest European standards.

Constructive talks should continue within the Brussels Group.

Joint statement by @JunckerEU and Greek PM #Tsipras following their phonecall this morning http://t.co/J5K2qheQjF #Greece

— Simon O'Connor (@socbxl) May 6, 2015

Updated

Another flurry of newsflashes -- revealing that the head of the European Commission, Jean-Claude Juncker, has spoken with the Greek prime minister today:

- 14:48:23 - EU’S JUNCKER SPOKE BY PHONE TO GREEK PM TSIPRAS, DISCUSSED NEED FOR WAGE AND LABOUR MARKET REFORM-COMMISSION SAYS

- 14:50:04 - JUNCKER, TSIPRAS DISCUSSED PENSION REFORM TO MAKE IT FISCALLY SUSTAINABLE-COMMISSION

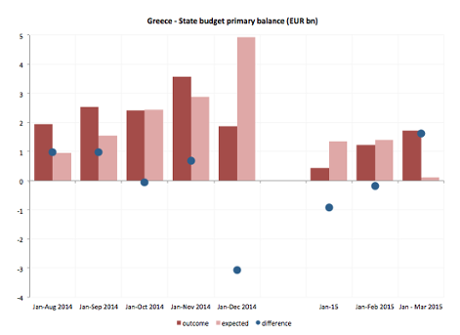

Have you wondered how Greece keeps meeting its debt repayments and other bills, despite being on the brink of bankruptcy?

Well, the secret is that Athens reverted to the tried and tested route of cutting back on spending, and squeezing as much taxation out as possible.

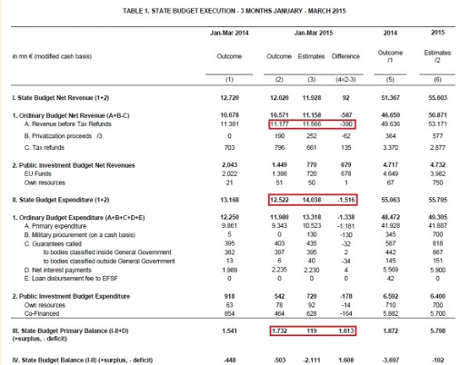

Silvia Merler, analyst at the Bruegel thinktank, has crunched the numbers to shows how Greece appears to be growing its primary budget surplus, creating the cash needed to keep afloat:

Peter Spiegel of the FT has just launched a blogpost on it. Here’s a flavour:

Not only have tax receipts crept back up to where they’re almost at last year’s levels (and pre-crisis estimates) for the first quarter of the year, but spending has been slashed to where the government has paid out €1.5bn less than anticipated.

That has produced a primary surplus of €1.7bn, which is €1.6bn ahead of expectations. And that’s all cash the government can use to keep itself running while it’s trying to hammer out a deal to get the final €7.2bn remaining it its current bailout.

And this chart shows how Greece has spent less than estimated so far this year (the second red box):

#Greece seems to have found a radical way to avoid default: raise more in taxes and cut spending! A look at new data: http://t.co/Gcdit8FsG3

— Peter Spiegel (@SpiegelPeter) May 6, 2015

So is all well? Certainly not. The spending cuts include bills that have simply been deferred, such as on healthcare - doctors have warned that some payments are months behind. But it indicates that Athens could keep running for longer than some had thought.

Greece’s cash has arrived safely at the International Monetary Fund:

IMF say Greece had made interest payment as expected today.

— NTMarkets (@NTMarketscom) May 6, 2015

Dijsselbloem: Don't expect a Greek deal on Monday

There’s no chance of a big breakthrough at next Monday’s eurogroup meeting of finance ministers.

That’s according to Jeroen Dijsselbloem, head of the eurogroup, a few minutes ago. He warned that there are still “lots of issues to resolve”.

He also declined to confirm Greece’s claim of disagreements between the three ‘Institutions” (IMF, EU and ECB).

DIJSSELBLOEM SAYS NO AGREEMENT EXPECTED MONDAY ON GREECE. - But.. but there is a deadline? pic.twitter.com/UKd9AEZ0zn

— *Russian Market (@russian_market) May 6, 2015

Newsflashes from Paris... where French finance minister Michel Sapin says the Greek bailout crisis will be resolved, but not soon....

- 06-May-2015 13:39:16 - FRANCE’S SAPIN SAYS SURE DEAL CAN BE FOUND ON GREECE

- 06-May-2015 13:40:01 - SAPIN SAYS DEAL WITH GREECE WILL NOT BE FOUND IN COMING DAYS

Germany finance minister Wolfgang Schauble, meanwhile, has warned that Germany and Greece will suffer together without a deal.

is he ok? :) https://t.co/xkLPTvYQCc

— Efthimia Efthimiou (@EfiEfthimiou) May 6, 2015

*DAMAGE FOR GREECE IS DAMAGE FOR GERMANY TOO, SCHAEUBLE SAYS

— Michael Hewson (@mhewson_CMC) May 6, 2015

As I was saying...

#Greece & the creditors do not agree yet on: - 2015 budget figs - Pension system viability - labor mrkt deregulation ~EU source to @Real_gr

— Yannis Koutsomitis (@YanniKouts) May 6, 2015

Greek media are reporting that the bailout negotiations are making progress on some important issues:

#Greece & creditors are close to agrmnt on: -VAT & tax collection -Privatizations list -Banking sector stability & NPLs ~EU srce to @Real_gr

— Yannis Koutsomitis (@YanniKouts) May 6, 2015

However, that suggests little progress over two key point - pensions, and labour market reform.

Just in.. US companies created fewer new jobs than expected in April, adding to concerns over its economy.

The ADP Institute reports that 169,000 new private sector positions were created in April, versus forecasts of around 200,000.

March’s ADP was also revised lower to 175,000 from 189,000.

That suggests that Friday’s non-farm payroll (the wider measure of the US labour market) could be disappointing. March’s NFP was surprisingly weak, so economists had been hoping for a big bounce-back. Perhaps not....

ADP vs. NFP Private Payrolls: pic.twitter.com/ogOQ3tCbwt

— Michael McDonough (@M_McDonough) May 6, 2015

ADP suggests March payroll stumble may extend into April

— Carl Riccadonna (@Riccanomix) May 6, 2015

Greece had been hoping that the European Central Bank might grant Athens permission to issue more short-term debt, but will probably be disappointed today.

Currently, Greece is capped from issuing more than €15bn of short-dated Treasury bills. It has pushed for this to be increased to €25bn, creating headroom to cover funding demands over the next few months.

Bruno Waterfield of The Times has heard that the ECB won’t raise the cap until Greeece and its creditors have a “firm” deal.

ECB will only agree to raise t-bill threshold for Greece with a firm agreement at eurogroup next Tues, declarations will not be enough

— Bruno Waterfield (@BrunoBrussels) May 6, 2015

Greece’s deputy finance minister has been forced to deny newspaper reports that he transferred an estimated €80,000 to a bank in Luxembourg in recent months.

The story, hotly refuted by the government, has been making waves this morning.

Helena Smith explains:

Put on the back foot as the government official identified to have transferred a large chunk of money abroad - in an another article carried by Bild this morning - Dimitris Mardas came clean saying he had indeed transferred some €40,000 abroad to cover university tuition fees for his daughter who is currently studying in Belgium.

Mardas, who rather embarrassingly is the finance minister in charge of revenues, however hotly denied that he had made any transactions in the three months since the Syriza-led government assumed power.

His “outing” sparked vivid debate amongst politicians on Greece’s popular morning TV shows. The former finance minister Gikas Hardouvelis, no less, was also accused of transferring thousands of euros abroad within days of the previous administration being defeated by Syriza.

Hardouvelis vehemently rejected accusations that the money had not been taxed.

Andreas Loverdos, a former education minister with the socialist Pasok party, told Mega TV this morning that “any politician who has money abroad has to bring it back to set an example for our compatriots and to prove that this money has been taxed.”

Government officials are describing today’s report as a “vulgar calumny” of the deputy finance minister, saying Mardas had properly declared his assets in parliament.

Reminder: the European Central Bank’s governing council has been discussing Greece this morning, at a regular non-monetary policy meeting.

The ECB must decide whether to extend more emergency liquidity assistance to Greek banks (it probably will), and whether to get tough by imposing a more severe haircut on the assets the banks hand over in return (it probably won’t). So analysts are watching Frankfurt closely....

Wednesdays. The days of lunch-in-front-of-the-monitors waiting for ECB's Greek ELA decision.

— Yannis Koutsomitis (@YanniKouts) May 6, 2015

“Constructive” is the word of the week:

*GERMAN FINANCE MINISTRY'S TIESENHAUSEN COMMENTS IN BERLIN: TALKS AMONG GREECE’S CREDITORS ARE CONSTRUCTIVE

— Dealingroom (@Dealingroom_EN) May 6, 2015

Back in London, the British financial trader accused of contributing to a multi-billion dollar stock market crash from his parents’ home, has appeared in court again.

Nav Sarao failed to persuade a judge to change his bail conditions, saying he cannot meet the £5m security set last month because his funds have been frozen by US authorities.

The Press Association adds:

As he was being led away from the dock he turned to the public gallery, held his arms out wide and declared: “I haven’t done anything wrong apart from being good at my job.

“How is this allowed to go on, man?”

Nav Sarao, accused flash crash trader, still in clink; judge says he must pay bail via @journosooz #houndofhounslow pic.twitter.com/yZ3Pvdn2x8

— Ryan Chilcote (@ryanchilcote) May 6, 2015

Yanis Varoufakis continues to make waves – not least in Greece, where the finance minister is now being seen as a very saleable asset.

Helena Smith reports from Athens:

As Yanis Varoufakis continues his European tour – holding talks in Rome today before moving onto Madrid at the end of the week – diehard supporters here in Athens have devised a new way of expressing their affection for the controversial politician. In Kypseli, the Athenian surburb that is home to prime minister Alexis Tsipras – shopkeepers trying to make the most of sale time in the country are, literally, cashing in on Varoufakis’ legendary “wow” factor.

An athletics store in area this morning was spotted attempting to draw consumers by plastering its façade with a poster emblazoned with a sketch of the finance minister under the words: “Wow prices!!! Until the end of negotiations.”

Thanks to Newsit.gr, we have a photo:

Few politicians have been as divisive as the vocal anti-austerian. Since his reported sidelining last week – hotly denied by Varoufakis himself and most of Tsipras’ left-dominated government – debate over the economist’s role (and qualities) has reached fever pitch.

Varoufakis’ 90-year-old father felt fit to step into the fray over the weekend, telling Ethnos newspaper:

“Yanis is talented, that is why they are attacking him. He s decent and tells the truth and will fight until he wins at least something.”

Varoufakis senior, a leftist who spent years in exile persecuted by the right, said the Greek prime minister was “very close” to his son and would never relinquish him. “My son is a an excellent person. He is honest and what he says, he does. He fights for what he wants to achieve and it was always he who gave the line [defined policy] to the prime minister who, for that reason, loves him a lot. He won’t sell him out.”

Tsipras is not the only one to adore his son, according to Varoufakis senior.

“Everyone loves him”.... [IMF chief Christine] Lagarde likes him very much along with every woman in Greece and Europe.”

Feel free to disagree below the line....

NIESR: Significant risk of disorderly Grexit

The thinktank, National Institute of Economic and Social Research (NIESR) has released its latest forecasts for the UK and world economies today, and it is a mixed bag of news for the eurozone.

NIESR sees brighter prospects for the region as a whole, but big question marks over Greece’s chances of staying in the the single currency bloc and what an exit might mean for its neighbours.

In the UK, NIESR says growth will be slower than it had pencilled in three months ago. The forecast for UK GDP growth has been cut to 2.5% from 2.9%, after official figures showed a much slower start to 2015 than expected.

The thinktank’s outlook for the global economy is for growth of 3.2% this year following growth of 3.4% each year in 2012–14. It had pencilled in 3.3% growth for 2015 back in February.

“Growth has been slightly weaker than expected so far in 2015 and inflation remains well below target in almost all developed countries,” NIESR comments.

On the Euro area, it continues:

“Prospects in the Euro Area have improved; the ECB’s monetary policy, the euro’s depreciation, and lower oil prices are all expected to support demand and activity in the period ahead, while fiscal policies are expected to be broadly neutral, and the risks of deflation have lessened.

“Nevertheless, economic conditions remain very weak in much of the area, with unemployment extremely high and expected to decline only slowly.

“Greece has undertaken an extraordinary adjustment since the crisis: between 2009 and 2014, the government’s primary fiscal balance was tightened by 11.7 percentage points of GDP. Output collapsed by 25% and unemployment rose to 27.5%; hence, the debt burden rose. Sustainable economic recovery is impossible without further international financial support and further reform of the economy. If an agreement is not reached in the next few weeks, there is a significant risk of a Greek default and a disorderly exit from the monetary union. Greece accounts for only about 2% of euro area GDP, but there would be risks of contagion to the rest of the area and to the euro itself.”

At a press briefing to unveil the latest forecasts, Simon Kirby, principal research fellow at NIESR said the thinktank’s central case was that there would not be a Greek exit from the eurozone. But were it to leave, the risks to other countries were by no means negligible. Kirby said:

“When you look at data from the Bank of International Settlements it is clear that the exposure of most European banking systems is significantly less than it was in 2011, the start of 2012. Dramatically less, in particular for France and Portugal... However, just because the banking sectors of these countries are significantly less exposed... it doesn’t necessarily mean that there is no contagion effect there. Much of this is very opaque, it relies to a large extent on the sentiment of investors in a number of countries and if the view is taken of those countries that are still by and large classified as peripheral Europe, or crisis economies, or whatever phrase you want to use, there clearly is a risk that there will be a negative spillover to these economies. Now, it’s significantly less than is was at the end of 2011, in 2012, but the risk is there. So the question then becomes: ‘Why go down the path that actually pushes us into the position where we actually give this risk a chance of materialising?’”

Asked if the thinktank was calling for a debt writedown or other relief measures, NIESR’s researchers said one thing that might be considered is extending the maturity of Greece’s debt.

NIESR director Jonathan Portes explained:

“The IMF have said very explicitly ... Greece’s debt burden is unsustainable ... so it has to be written off. Now you can write it off... by extending maturities and pretending you are not really writing it down because you are not changing the face value but we all know what’s really happening in economic terms.”

He feels the warning from the IMF, reported in Tuesday’s FT, that Greece’s debt mountain has become unsustainable again was overdue. Portes continues:

“Even the Commission’s optimistic forecast which was published today [Tuesday, as covered in the live blog here] still shows Greece with a debt burden of about 180% next year. The IMF’s message here is, I think, long overdue... Essentially European policymakers ... either want to force Greece out of the euro and take the risk, which, as Simon says, we really cannot quantify very sensibly .... or they are going to have to recognise economic reality, if they want Greece to stay in the euro, an economic reality that is saying significant write-off in some form or other [will be needed].”

Investors still believe there is a high risk that Greece will default on its debts within the next five years:

Greek 5yr default probability continues to rise as the blame game between #Greece and it's creditors is in full swing pic.twitter.com/I2O316HntO

— Holger Zschaepitz (@Schuldensuehner) May 6, 2015

Associated Press has also confirmed that Greece is making its €200m repayment to the IMF today (as flagged up early this morning).

Next week’s bill will be harder, though.

AP explains:

Greece is making a 200 million euro ($222 million) repayment to the International Monetary Fund, though another, larger one looms next week that it will struggle to manage.

A Greek finance ministry official said Wednesday: “The payment is proceeding normally.” The official spoke only on condition of anonymity in line with government regulations.

Greece is struggling to agree on a deal with its creditors to get more rescue loans and is gradually running out of cash. The sides hope to make progress by May 11, when they will hold a eurozone meeting.

On May 12, Greece is due to repay €750m to the IMF, money it will have to scrape together from local reserves, such as those of local governments and hospitals.

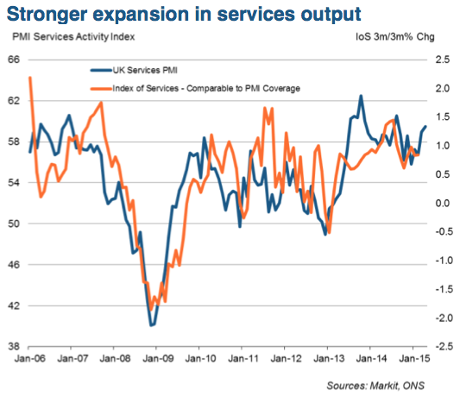

Here’s Angela Monaghan on the jump in UK service sector growth last month:

Back in the City, shares in Sainsbury’s have slid by 3% to the bottom of the FTSE 100 leaderboard, after it posted its first loss in a decade.

Sarah Butler explains why, here:

Here’s that story about new possible taxes on Greek super-rich that we mentioned earlier...

.@BILD reports Greek gov't plans to levy special tax against 500 richest Greek families: http://t.co/6hJCq6SCkX pic.twitter.com/c9lruVPF2z

— Nina Schick (@NinaDSchick) May 6, 2015

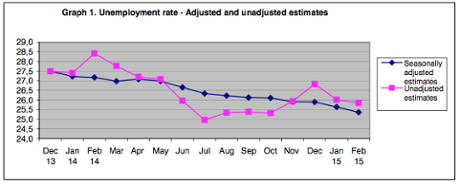

Greece’s unemployment rate has fallen, but still remains alarmingly high.

The seasonally adjusted unemployment rate in February 2015 fell to 25.4%, down from 25.6% in January, according to Elstat. A year ago it was 27.2%.

The data shows that the number of unemployed people fell by over 15,000 during February. But they didn’t all find work. While the employment total rose by 7,662, the number of ‘inactive people’ picked up by 3,797.

Back to Greece, and a new poll has shown that a majority of German executives now believe the eurozone would be better off without Greece.

Mike Bird of Business Insider has the story:

According to Germany’s premier business newspaper, Handelsblatt, 44% of the 673 executive-level German managers surveyed think that Greece should leave the eurozone of its own accord.

A further 13% think Greece should be actively ejected from the monetary union.

79% believe if Greece left the euro it wouldn’t have contagion effects with other countries, and less than a fifth are concerned about that financial knock-on impact.

Handelsblatt poll shows a majority of German executives now want Grexit - 79% see no contagion/domino effect http://t.co/tmNliA6lr5

— Mike Bird (@Birdyword) May 6, 2015

UK Service growth hits eight-month high

Fears that Britain’s recovery is faltering have been allayed by the latest survey of UK services firms.

Growth across the sector jumped to an an eight-month high in April, according to Markit. Its service sector PMI hit 59.5, up from 58.9 in March, showing faster growth (anything over 50 points shows growth).

Service sector firms, from IT companies to hotels, reported that demand rose last month, despite worries about the general election.

It suggests that the UK economy could grow by as much as 0.8% in the second quarter of 2015, having growth slipped to just 0.3% in January-March.

David Noble, group CEO at the Chartered Institute of Procurement & Supply, reckons services firms are performing well:

“The services sector offered a more upbeat level of performance than the other sectors this month and demonstrated a continued assurance in the growth of the UK economy.

New business was the primary driver of activity, even amidst increased competition, more marketing activity, the scrabble for good staff and the availability of raw materials.”

A pre-election boost to the Conservatives?....

Big jump in UK services PMI, a strong indicator for UK GDP, when other data pointed to faster slowdown. A Tory boost 24hrs before #GE2015

— Joshua Raymond (@Josh_CityIndex) May 6, 2015

Waiting for Dave to explain PMIs to the wider electorate. #anythingabove50

— World First (@World_First) May 6, 2015

Updated

European stock markets have bounced back from yesterday’s selloff.

-

FTSE 100: up 29 points at 6956, + 0.4%

-

German DAX: up 99 points at 11426, +0.9%

-

French CAC: up 25 points at 4999, +0.5%

Tony Cross, marrket analyst at Trustnet Direct, sees turbulence ahead, though, given events in Britain and Greece.

Until now, there may have been a degree of willingness to look beyond the bigger political issues – both in terms of the UK election and what’s happening with regard to the Greek debt talks – but it’s easy to see how this could mark the start of several downbeat sessions as the market attempts to predict how matters will evolve between now and the start of next week.

The news that Greece is meeting its €200m repayment to the IMF is welcome, but it’s only a small hillock in the mountain of debt repayments that Athens faces this summer:

Reuters is reporting that #Greece has met its €200mn payment to the #IMF, due today. But plenty of payments to go. pic.twitter.com/nhvKebvndw

— Holger Zschaepitz (@Schuldensuehner) May 6, 2015

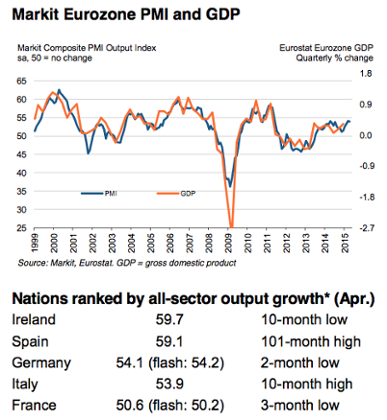

Eurozone businesses post decent growth

This morning’s flurry of data shows that eurozone businesses reported pretty solid growth in April as the region’s recovery continues.

Strong growth in Spain, and a pick-up in Italy, made up for France’s ongoing weakness, according to data provider Markit.

Markit’s Composite Output Index came in at 53.9 in April, little-changed from 54.0 in March, showing steady growth.

Chris Williamson, chief economist at Markit, says:

“The survey is signalling a rate of economic growth of approximately 0.4% at the start of the second quarter, similar to that indicated by the PMI in the first quarter.

“The fact that the rate of growth failed to gain further momentum is a disappointment, but the national growth variations will give policymakers some real encouragement that the economic health of the region is improving.”

Not in Greece, though - data on Monday showed that its manufacturing sector continues to contract.

Updated

Growth across Germany’s service sector also slowed... with its PMI coming in at 54.0, down from 55.4 in March.

That’s also weaker than the ‘flash estimate’ of 54.4 published two weeks ago; suggesting growth slowed in late April.

*GERMANY APRIL SERVICES PMI FALLS TO 54; PRELIM. 54.4

— World First (@World_First) May 6, 2015

Disappointing news from France, though - growth across its private sector has slowed.

The French service sector PMI fell to 51.4 last month, from 52.4 in March. And with its manufacturing shrinking, the overall French Composite PMI fell back to 50.6.

*GERMANY APRIL SERVICES PMI FALLS TO 54; PRELIM. 54.4

— World First (@World_First) May 6, 2015

More good news for the eurozone -- Italy’s service sector has reported its fastest growth in 10 months.

The Italian service sector PMI jumped to 53.1 last month, up from 51.6 -- on a scale where any reading over 50 shows growth.

#Italy's service sector grows at fastest rate for 10 months. Headline Index at 53.1 (Mar:51.6) http://t.co/7YRmf0QBlP http://t.co/5whZgbyShe

— Markit Economics (@MarkitEconomics) May 6, 2015

UK 10-year gilt yields hit 2%

Back in the bond markets, Britain’s headline borrowing costs have hit their highest level of 2015.

#UK 10-year bond yield climbs above 2%; first time since December pic.twitter.com/gkhI1cDdcS /via @moved_average

— Yannis Koutsomitis (@YanniKouts) May 6, 2015

The deficit just got a little more expensive to service....

Updated

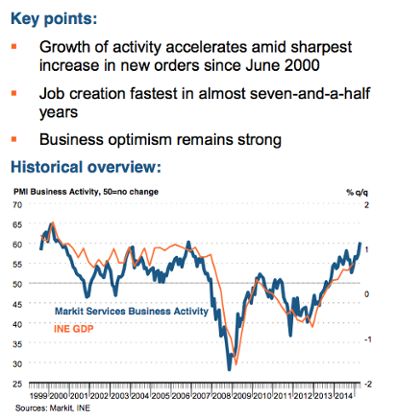

Here comes the first Purchasing Managers Index report from the eurozone....and it’s good news for Spain.

The Spanish service sector PMI has surged to 60.3 last month, up from 57.3 in March, a really strong reading that shows growth is accelerating.

Activity, new business and employment are all increasing at rates not seen since prior to the economic crisis, as Spain’s recovery continues.

Olé!

— Mike Bird (@Birdyword) May 6, 2015

Losses mount as bond selloff continues

A major readjustment appears to be underway in the bond market.

Prices of eurozone sovereign debt are falling this morning, pushing up yields, continuing a trend that began late last month:

Sell-off in #Eurozone bonds continue. 10yr govt bond yields of Italy and Spain spike, make fresh 2015 highs. pic.twitter.com/EU2giLaXpy

— Holger Zschaepitz (@Schuldensuehner) May 6, 2015

Traders aren’t certain exactly what’s caused it. Greek worries are one factor, but another theory is that investors have realised that they should perhaps demand a little more interest in return for lending to governments.

Even after recent losses, Italy’s 10-year bond is yielding just under 1.9% -- which feels a more ‘normal’ level than the 1.1% reached in March. Of course, anyone who bought the bonds recently is nursing losses.....

Global bond markets have lost about $340 billion since the start of last week

— Francine Lacqua (@flacqua) May 6, 2015

Jens Nordvig of Nomura warns that these ‘big moves’ could have serious implications, and makes three important points:

- How is credit going to cope with this type of weakness in rates space?

- How will fixed income flows from the Eurozone (a key driver of many moves over the last 6-9 months) be impacted?

- Could risk aversion support the Euro? (if the Euro is the new yen, it will).

Interesting times ahead...

Bild: Greece considering special levy on richest families

Curious.....Germany’s Bild newspaper claims that Athens is planning a special tax on the country’s 500 richest families.

Bild says the measure is included on the Greek finance ministry’s list of reforms, whcih also includes a luxury tax on items such as expensive cars and trips to Greek islands, and higher taxes on workers earning over €30,000 per year.

It’s not clear what levy Athens is thinking of imposing on its wealthiest families. On assets, or income? And what about those who keep their funds offshore? (locked up in Zurich, for example...)

good morning! new status symbol? "#Greece's 500 richest families may face special levy: newspaper" https://t.co/v3OJ8IFQSC via @sharethis

— Diane Shugart (@dianalizia) May 6, 2015

If true (and we’re on the case now.....), it’s the latest in a series of innovative measures from the Greek government.

Yesterday, we learned that Greece was considering a surcharge on cash withdrawals as a way of raising revenue (and deterring a bank run).

One down, lots more to go....

That's one less - Greece Has Made EU200m IMF Repayment, CNBC Says, Citing Reuters.

— Frederik Ducrozet (@fwred) May 6, 2015

A Greek official has confirmed to Reuters that the €200m interest payment is winging its way to the International Monetary Fund.

“It’s done, the money is on its way,” the official said, on condition of anonymity.

Cash-strapped Athens is quickly running out of money while it tries to persuade euro zone partners and the IMF to extend further aid. The payment on Wednesday was not expected to be a problem for the country, but a €750m payment to the IMF that falls due on May 12 is expected to be a bigger struggle.

Greece 'makes IMF repayment'

Newsflash from Athens: Greek officials have just announced that they’ve met the €200m repayment to the IMF due today - lifting the immediate threat of a default.

Via Reuters:

- GREECE MAKES 200 MLN EURO REPAYMENT TO IMF - GREEK OFFICIAL

#Greece makes €200ml repayment to #IMF ~Greek official /via @EM_Equity

— Yannis Koutsomitis (@YanniKouts) May 6, 2015

#Greece | MAKES €200M REPAYMENT TO IMF-GR OFFICIAL..IMF gives Greece money so that Greece can pay IMF so that IMF can give Greece more money

— Ioan Smith (@moved_average) May 6, 2015

The agenda: Greek deadlock, more PMI surveys

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

With relations with its lenders deteriorating, Greece must pull together €200m to meet an repayment to the International Monetary Fund today.

It’s a fitting way to mark the fifth anniversary since Greek MP voted to accept deep austerity cuts in return for the country’s first bailout programme.

Insiders say Athens has got the cash, but the payment will intensify the remorseless squeeze on its finances as it struggles to get a deal with its creditors over pensions, labour reforms and the minimum wage.

As we reported last night, Greece officials are now blaming “serious disagreements and contradictions” between the IMF and the European Union for the continued failure to agreed a package of economic reforms that all sides are happy with.

Greek health minister, Panagiotis Kouroumblis, told my colleague Helena Smith that Greece’s creditors are making impossible demands on Athens:

“They are not only implacable, the feeling that they give us is that they are impossible to satisfy.”

“They ask for 10 things to be done and then come back the next day and ask for another 10 more. As much as we would like, that’s not going to lead to compromise.”

But if someone doesn’t compromise soon, Greece risks running out of funds altogether with another €800m due to the IMF later this month.

The third of Greece’s creditors, the European Central Bank, will decide today whether to keep supplying emergency liquidity assistance to its banking sector.

Analysts expect that the ECB will offer a little more help, to allow banks to keep operating despite the drip-drip-drip of deposit withdrawals as savers hoard cash.

Another #ECB Day for #Greece. Central Bank's Gov Council to review ELA to Greek banks. Market expects new small increase & no haircut. Yet.

— Yannis Koutsomitis (@YanniKouts) May 6, 2015

Looks like we’re rattling towards another showdown on May 11, when eurozone finance minister meet again to assess the situation.

The Greek crisis is expected to weigh on sentiment in the markets today, after helping to trigger a chunky selloff yesterday.

Investors will also be watching the latest PMI surveys from Markit this morning, which will show whether the eurozone private sector kept growing last month.

And in the City, Sainsbury’s has reported its first loss in a decade. The supermarket chain made a pre-tax loss of £72m, dragged down by £628m of one-off charges.

Sainsbury's falls to first statutory loss in a decade - £72m after property write offs

— Sarah Butler (@whatbutlersaw) May 6, 2015

Sainsburys boss Mike Coupe: "The UK marketplace is changing faster than at any time in the past 30 years which has impacted our profits"

— Graham Ruddick (@GrahamtRuddick) May 6, 2015

Sainsbury have a conference call shortly, so we’ll catch up on them later, along with other developments through the day.....

.png?w=600)