Global shares fall as oil price jumps

A combination of concerns left global markets lower, with a rising oil price on Middle East tensions adding to the worries about Greece and the state of the US economy. By the close of play European markets had come off their worst levels with Wall Street - down sharply overnight as Saudi Arabia’s military action in Yemen pushed crude prices higher - staging a slight recovery. The closing scores showed:

- The FTSE 100 finished 95.64 points or 1.37% lower at 6895.33

- Germany’s Dax dropped 0.18% to 11,843.68

- France’s Cac closed 0.29% lower at 5006.35

- Italy’s FTSE MIB fell 1.06% to 22,900.27

- Spain’s Ibex ended 0.1% at 11,453.8

- The Athens market lost 3.74% to 764.88

Meanwhile on Wall Street, the Dow Jones Industrial Average is up around 19 points.

On that note, it’s time to close up for the evening. Thanks for all your comments and we’ll be back again tomorrow.

It’s becoming a little unclear how strong the US economy is, but there is now a general perception that the Federal Reserve will soon be raising interest rates regardless, if not in June then probably by September.

Now James Bullard, president of the St Louis Fed, has repeated his view that the risks of keeping interest rates low for too long “may be substantial.” In a lecture in Frankfurt Bullard - who is a non voting member of the Fed’s board this year - said:

Now may be a good time to begin normalizing U.S. monetary policy so that it is set appropriately for an improving economy over the next two years. Even with some normalization, policy will remain exceptionally accommodative.

And echoing the “bubble” concerns of German finance minister Wolfgang Schäuble he said:

If a bubble in a key asset market develops, history has shown that we have little ability to contain it. A gradual normalization would help to mitigate this risk while still providing significant monetary policy accommodation for the U.S. economy.

Speaking of Draghi, he has been explaining to the Italian Parliament that the ECB cannot buy Greek bonds as part of its quantitative easing programme. From Reuters:

“QE does not buy Greek bonds for three reasons. The first is that it doesn’t buy bonds of countries that are in a programme with the IMF and the European Commission when the review of this programme has not been completed. As you know, in Greece the review was suspended,” Draghi told Italian lawmakers.

Draghi said the other reasons for not buying Greek bonds were that their credit rating was too low and that the ECB could not buy bonds from a country above a certain percentage - to avoid “arriving at a point where it becomes a country’s biggest creditor”.

Meanwhile German finance minster Wolfgang Schäuble has said low interest rates were causing considerable problems in Germany, there was too much central bank money and debt in the world and there was risk of a bubble forming.

German FinMin Schäuble says #ECB QE program removes incentive for reforms.

— Holger Zschaepitz (@Schuldensuehner) March 26, 2015

Speaking at a banking event in Berlin, he said he was snot criticising the European Central Bank because it needed to defend its inflation target. But he said (quote courtesy Reuters):

A low interest rate leads to a misallocation of resources with all the risks and side-effects that you see when bubbles are forming.

A reminder that earlier ECB president Mario Draghi told the Italian parliament that there was no doubt Germany’s trade surplus contravened EU rules on excessive imbalances.

Updated

Kansas Federal Reserve vice president and economist Chad Wilkerson said:

We saw our first monthly decline in regional factory activity in over a year. Some firms blamed the West Coast port disruptions, while producers of oil and gas-related equipment blamed low oil prices.

The full announcement is here, courtesy Calculated Risk.

And more signs of weakness in the US economy:

Kansas City Fed Manufacturing Activity (Mar) -4 versus 1 expected, previous 1

— Sigma Squawk (@SigmaSquawk) March 26, 2015

Kansas City Fed respondent: 'We do not see the economy as being as strong as a portrayed in the national media reports."

— zerohedge (@zerohedge) March 26, 2015

Kansas City Fed: ' Momentum we experienced earlier this year has left and we are again cost cutting and becoming lean"

— zerohedge (@zerohedge) March 26, 2015

Updated

European Central Bank President Mario Draghi said bond-buying by the central bank has brought down long-term interest rates and lowered the euro’s exchange rate against the U.S. dollar, writes Reuters.

“The effect on the exchange rate has been undoubtedly significant,” Draghi said during testimony in parliament on Thursday, noting also the decline in long-term interest rates.

The euro hit a 12-year low below $1.05 against the dollar at the start of last week, but has since recovered to $1.09 since.

Updated

ECB's Draghi: Euro zone is probably the part of the world with the highest taxes and this inevitably weighs on growth.

— Reuters Insider (@ReutersInsider) March 26, 2015

ECB’s Draghi: Says ‘ECB Is Very Favourable To EU Investment Plan,’ Must Begin As Soon As Possible

— Live Squawk (@livesquawk) March 26, 2015

And then this:

DRAGHI SAYS NO DOUBT GERMAN TRADE SURPLUS INFRINGES EU RULES ON EXCESSIVE IMBALANCES

— MineForNothing (@minefornothing) March 26, 2015

Updated

More from Draghi in the Italian parliament:

Draghi: High reliance on bank financing in the Eurozone is consequence of large number of small businesses in the area. #ECB

— Open Europe (@OpenEurope) March 26, 2015

Draghi: Compared to US, fiscal consolidation in Eurozone has gone faster. This has had recessionary effects. #ECB

— Open Europe (@OpenEurope) March 26, 2015

Draghi: One may not like banks and markets, but they are the channels through which the ECB acts.

— Open Europe (@OpenEurope) March 26, 2015

Draghi: A more favourable economic situation (as a result of ECB action) will make it easier to implement structural reforms.

— Open Europe (@OpenEurope) March 26, 2015

Lunchtime summary: Greece hopeful, but markets edgy

Time for a recap.

Greece’s economy minister George Stathakis told Antenna TV that Athens will unlock the funds it needs, predicting:

“I think at the beginning of next week we will have a deal, both over the reform package proposed by the Greek government, and over the flow of funding,”

The Greek opposition, though, has warned that Greece will run out of money by Easter.

New ECB data has shown that bank deposits continued to fall last month, with another €7.6bn leaking out in February:

#Greece Feb deposit outflows at €7.64 bln from €12.79 bln in Jan (BoG). #economy #banking pic.twitter.com/zgl8QNU8Ik

— MacroPolis (@MacroPolis_gr) March 26, 2015

private depositors withdrew €20.8bn from their accounts dec-feb, according to Bo#Greece data. hardly a sign of confidence in political devts

— Diane Shugart (@dianalizia) March 26, 2015

where did the money go? abroad, consumption, taxes, under the mattress? certainly there's some data for the first three? #greece

— Diane Shugart (@dianalizia) March 26, 2015

Uncertainty over Greece has helped drive European stock markets down.

The FTSE 100 has shed 1.5%, or 100 points, at 6890. Other European market are also down around 1.5%.

Traders are also alarmed by the military action unfolding in Yemen, which has driven the oil price up by 3% today.

Craig Erlam, senior market analyst at OANDA, told AP that:

“The conflict has the potential to act as a drag on oil supplies as most oil tankers from Arab producers must pass by the Yemen coastline in order to get through the Red Sea and Suez Canal.”

We’ve also had a flurry of generally upbeat economic data:

The Bank of England has identified the Greek crisis as a “significant risk” to the UK economy.

In its latest report, the Bank’s financial policy committee said:

“International and geopolitical risks to financial stability in the United Kingdom persist. Despite recent encouraging signs, the risk of a low nominal growth in the euro area persists.

“There are also risks associated with a further slowdown in China and to some emerging economies as the stance of monetary policy begins to diverge globally. There also remain significant risks in relation to Greece and its financing needs, including in the near term.

“Any of these risks could trigger abrupt shifts in global risk appetite that in turn might lead to a sudden reappraisal of underlying vulnerabilities in highly indebted economies, or sharp adjustments in financial markets.”

Addressing Italian MPs, Draghi stressed several times € not responsible for crisis. Shows he's aware support for € is eroding in Italy.

— Vincenzo Scarpetta (@LondonerVince) March 26, 2015

Mario Draghi is urging Italian MPs not to assume that the eurozone is fixed. We’re seeing a cyclical recovery, he says.

Draghi: This recovery is not structural. It's cyclical. I insist on the word 'cyclical'. #ECB

— Open Europe (@OpenEurope) March 26, 2015

The ECB chief adds that the eurozone has not been designed to cope with “permanent creditors and debtors” existing together.

Draghi: No sign of bond shortage so far. We intend to carry on with QE at least until September 2016. #ECB

— Open Europe (@OpenEurope) March 26, 2015

Draghi adds that the ECB has ‘removed doubts’ over the reversibility of the euro.

Heads-up: ECB chief Mario Draghi has begun speaking in the Italian parliament, reminding MPs that his powers are limited:

ECB President Draghi now addressing Italian MPs, reminds them that monetary policy can't solve the structural problems of an economy.

— Open Europe (@OpenEurope) March 26, 2015

Scotland’s oil industry continues to suffer from the drop in the oil price since last summer.

Royal Dutch Shell has announced that it is cutting more than one in 10 of its North Sea workforce.

Just in: the number of Americans filing new claims for unemployment benefit fell by 9,000 last week to 282,000.

That’s a five-week low, and might possibly calm some of the worries about the US economy. Alternatively, it could fuel concerns that the Federal Reserve will take the plunge and raise interest rates in June....

Updated

Former Greek PM releases bailout agreement

Over in Athens, former prime minister Antonis Samaras has raised the stakes by making public the bailout extension accord which finance minister Yanis Varoufakis agreed with creditors on February 20.

Helena Smith reports:

The conservative leader - taking the moral high ground - said prime minister Alexis’ Tsipras Syriza/Anel government had failed to release the document fearing the backlash from its own MPs.

In effect, the the new administration had “co-signed” the hated “memorandum” it had vowed to wipe away when in opposition, Samaras argued.

“For one and a half months, the government hasn’t dared bring the accord extending the loan agreement to parliament because the parliamentary groups of Syriza and Anel are afraid of a vote in the House and even more they don’t want the Greek people to learn the truth,” said the erstwhile premier.

“We are making the text public so that every Greek citizen can see it and understand it.”

The Tsipras government has made much of the fact that for the FIRST TIME creditors have been taken to task by an administration in Athens bent on conducting real negotiations by putting up a robust defence of the country’s interests. HS

Here’s a photo of Samaras during his press conference:

Σαμαράς: Να εφαρμόσει η κυβέρνηση όσα υπέγραψε στις 20 Φεβρουαρίου http://t.co/AImFbJvq1r pic.twitter.com/ywxDT5xinl

— Views.gr (@Viewsgr) March 26, 2015

And here’s a picture of the Greek sides’s signatures on the February 20th memorandum.

ΝΔ: Στη δημοσιότητα η συμφωνίας της 20ης Φεβρουαρίου με τις υπογραφές του Βαρουφάκη (ΥΠΟΙΚ), Στουρνάρα (ΤτΕ) pic.twitter.com/zGQBSEb5f2

— BankingNews.gr (@bankingnewsgr) March 26, 2015

Newsflash from Reuters:

- GREEK PM TSIPRAS, IMF’S LAGARDE DISCUSSED GREECE’S NEGOTIATIONS WITH LENDERS OVER THE PHONE ON WEDNESDAY - GREEK GOVT OFFICIAL

Bloomberg have pulled together a handy timelines of Greece’s financial obligations over the next five months, including maturing bonds and repayments to the IMF and the ECB. Worth bookmarking.

Next big deadline for Greece is Monday. For complete list of dates to watch, see our timeline: http://t.co/N4I9wGO2k1 pic.twitter.com/ebMA9ZOOI3

— David Powell (@davidjpowell24) March 26, 2015

A new survey from the CBI has shown that Britain’s retailers are more positive, echoing this morning’s decent retail sales figures (see here).

A total of 34% of respondents told the CBI that sales volumes rose in March, compared with a year ago, and 15% said they were down, giving a rounded balance of +18%. Last month, the balance was just +1%.

Rain Newton-Smith, CBI Director for Economics, says:

“Sales have recovered following a tough month in February for retailers, and we expect solid growth to continue through Easter.

“The outlook ahead is looking bright, with household incomes buoyed by zero inflation and improving pay packets, which will continue to encourage spending.

“However, the retail sector isn’t in the clear yet, with some companies, especially food retailers, still feeling the heat from stiff price competition.”

Italy just sold two-year bonds at a record low yield of just 0.162%.

That’s a remarkably low cost of borrowing, showing the impact that the ECB’s new bond-buying programme continues to have on the markets. It also suggests traders don’t expect eurozone inflation to pick up anytime soon.

*ITALY SELLS 2017 ZERO COUPON NOTES AT RECORD LOW 0.162%

— lemasabachthani (@lemasabachthani) March 26, 2015

RT @lemasabachthani *ITALY SELLS 2017 ZERO COUPON NOTES AT RECORD LOW 0.162% << also zero inflation though

— MineForNothing (@minefornothing) March 26, 2015

Updated

Greek opposition claims money will run out by Easter

Over in Greece, opposition New Democracy parliamentary spokesman Kyriakos Mitsotakis has issued a warning that the country could go bankrupt by Easter.

Helena Smith reports from Athens:

Calling on the leftist-led government to meet the euro group’s demand for a list of reforms as soon as possible, Mitsotakis told Mega TV liquidity problems were such that Greece could hit the rocks of bankruptcy by [Orthodox] Easter.

“Money will run out by Easter,” he said insisting that the debt-stricken nation was now at risk of defaulting because of lost time.

Mitsotakis also criticised the ruling coalition for still not bringing the bailout extension accord, reached with creditors on February 20, to parliament.

The government is fearful of “the truth” being told in parliament, he claimed, and worried that many of its own MPs would not vote the agreement through.

“We, however, would back it,” Mitsotakis said.

Nikos Filis, parliamentary spokesman for the governing Syriza party, also appeared on the show and insisted that pensions and salaries – due to be paid next week – and worth a reputed €1.7bn were - “not in danger.”

“There is not going to be a credit event,” said Filis, a former chief editor of Avgi, the left-wing party’s paper.

Opposition MPs have accused the government of leading the country to an “Internal default” where it is unable to meet certain payments, most notably pensions and public sector salaries.

But anecdotal evidence suggests that growing numbers of Greek civil servants are taking precautionary measures.

“I have ensured that I have paid all my bills, including doctors’ visits, because frankly there is very little assurance that we will be paid in full in the coming months,” said one high ranking public sector employee in her sixties.

“We are bankrupt and it is clear the state is running out of money.”

It’s not a full-blown run, yet, but Greece’s banking sector continues to suffer from a slow shuffle to the exits.

Deposits fell by €7.8bn in February, according to new ECB data today, as some savers pulled out cash.

Greek bank deposits fell by €7.8bn in Feb (following a record €12.2bn drop in Jan). Here's the broader picture. pic.twitter.com/IOSveKUFzm

— Frederik Ducrozet (@fwred) March 26, 2015

Stock markets fall deeper into the red

The selloff in the European stock markets has accelerated, with all the main indices shedding at least 1% so far this morning.

London’s FTSE 100 has shed 85 points, in a broad-based selloff.

Mike van Dulken at Accendo Markets says confidence has been hit by the conflict in Yemen, Greece’s debt problems, and signs that the US economy is slowing.

Over in Frankfurt, shares in German exporters are suffering as the euro rallies against the US dollar, back over the $1.10 mark.

Wall Street is on track for further falls today.

US futures are tumbling again today. pic.twitter.com/kWO84JC0R7

— Bloomberg Markets (@markets) March 26, 2015

The biggest faller in the City today is the London Stock Exchange itself, after its biggest shareholder sold a 10% stake.

Travel stocks are also suffering, with British Airways owner IAG down 4.5%.

Rob Wood of Berenberg Bank isn’t surprised to see UK retail sales rising so strongly last month.

Explaining this is not rocket science. Cheaper petrol, food and import prices are cutting shop prices fast, leaving consumers with a little more money to spare after buying essentials.

And UK consumers being the shoppers they are tend to spend that extra disposable income.

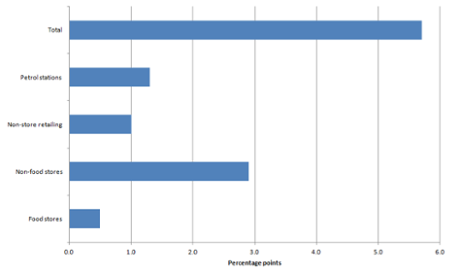

UK retail sales jumped last month, indicating that British consumers are upbeat about economic prospects ahead of May’s general election.

The Office for National Statistics reported that sales were up by 0.7% month-on-month in February, and were 5.7% higher than a year ago.

Demand for non-food goods such as furniture was particularly high.

The ONS also reported that prices fell by 3.6% in February 2015, the largest year-on-year fall since consistent records began in 1997.

We learned on Tuesday that inflation across the economy was zero in February; this jump in retail sales suggests people aren’t worried that deflation is setting in [if they were, they’d be deferring purchases until they’re cheaper].

Volume of sales at household goods stores up 9.1% in last year. That's a strong sign of consumer confidence.

— Duncan Weldon (@DuncanWeldon) March 26, 2015

Updated

Another encouraging sign for the eurozone: Money supply across the single currency region jumped by 4% last month, the fastest rise in almost six years.

4% M3 growth for the eurozone - strongest since April '09. pic.twitter.com/xh6DGcgwt0

— Mike Bird (@Birdyword) March 26, 2015

However, total lending to eurozone households and firms dipped by 0.1%, the 34th consecutive monthly fall. That suggests the ECB’s stimulus measures aren’t, yet, spurring on lending (although loans to non-financial corporations did rise by €8bn). Here’s the ECB’s data.

Spain’s economic recovery appears to be gathering pace.

The Bank of Spain has raised its growth forecast for 2015 to a punchy 2.8%, and predicted that the economy expanded by 0.8% in the first three months of this year.

That would make it one of the best-performing areas of the eurozone.

More good economic news for #Spain RT @ForexNews87 Bank of Spain says sees Q1 Gdp up 0.8 Pct from Previous Quarter http://t.co/xlq340xRrB

— Shaun Richards (@notayesmansecon) March 26, 2015

Updated

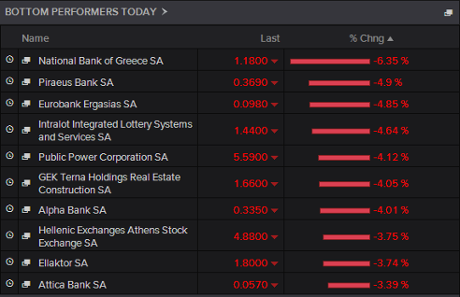

Anxiety over Greece’s bailout is hitting its stock market this morning, despite economy minister George Stathakis predicting a deal early next week.

The ATG index of leading shares has dropped by 2.5% in early trading, led by financial stocks:

Greek government bonds are coming under pressure too, pushing up the yield (or interest rate) on its shorter-term debt.

#Greece yields 3y 19.83%; +19 bps 5y 15.62%; +16 bps 10y 10.94%; +1 bps 15y 10.82%; -1 bps

— Advisory Desk (@advdesk) March 26, 2015

The Russian ruble has jumped by 1.5% against the US dollar , on the back of the oil price spike.

#Russia Ruble rallies on higher #oil price. pic.twitter.com/7cAs0Ocmug

— Holger Zschaepitz (@Schuldensuehner) March 26, 2015

Oil price leaps after Yemen air strikes

The oil prices has surged this morning, after Saudi Arabia launched military action against rebels in Yemen, raising the prospect of wider conflict in the Middle East.

The price of a barrel of Brent crude has jumped by 6%, or over three dollars per barrel, to $59.50.

US Crude oil also jumped, by a similar amount, to $51.26

#Oil extends gains on Yemen escalation. Brent crude up >6%.http://t.co/Jb7MihRpcI pic.twitter.com/mEODpwV7wj

— Holger Zschaepitz (@Schuldensuehner) March 26, 2015

Having bombed Houthi rebels in Yemen yesterday, Saudi authorities said that several other countries in the region including Egypt, Pakistan, Jordan and Sudan were ready to commit troops to a ground offensive.

The US is also supporting the Saudis, who acted after Houthi rebels - backed by Iran -seized al-Anad airbase and the seaport city of Aden.

As Dan Roberts and Kareem Shaheen explain:

The advance set the stage for a confrontation between Iran, which backs the rebels also known as Ansar Allah, and regional powers eager to halt the broadening of the Islamic Republic’s regional influence

Geo-political risk back in #oil traders minds...oil price spikes as Saudi & allies start targeted bombing in Yemen. WTI +18% last 5days

— Caroline Hyde (@CarolineHydeTV) March 26, 2015

European stock markets have opened in the red, tracking losses on Wall Street following yesterday’s weak US data (see opening post for details).

Germany is the biggest faller, with the DAC shedding 1.4%.

The FTSE is down 38 points, or 0.6%, at 6951 points - further away from last week’s record highs.

DAX down 200 points at 8.06am - FTSE -40 points at 6950

— David Buik (@truemagic68) March 26, 2015

German consumer confidence hits 13 year high

While Greeks fret about potential bankruptcy, Germans are their most confidence in over 13 years.

GfK’s monthly survey of German consumer confidence has hit 10.0, up from 9.7% a month ago, which is the highest since October 2001.

GfK analyst Rolf Buerkl said German consumers are becoming “ever more optimistic”; but that would change if the Greek crisis deepened.

“If a Grexit, where Greece renounces the euro and subsequently leaves the euro zone, were in fact to materialise, the German economy could suffer a severe setback as a result.”

Germans on a shopping binge: GfK consumer confidence increased to 10.0, highest level since Oct2001. (via ING) pic.twitter.com/SNMuH08kOr

— Holger Zschaepitz (@Schuldensuehner) March 26, 2015

George Stathaskis’s comments suggest that eurozone finance ministers may gather in Brussels early next week to discuss the Greek crisis again, and potentially release some aid.

Greece optimistic of deal next week

The Greek government has declared it is confident that it can reach a deal on its economic reforms with the rest of the eurozone early next week.

Economy minister George Stathakis told Antenna TV this morning that a breakthrough - which would stave off the risk of bankruptcy - could be just days away.

Stathakis said:

“I believe that at the beginning of next week we will have an agreement on the package of reforms the Greek government is proposing, and on the funding of the country.”

However, he didn’t indicate what kinds of reform are being worked on; Greece’s government must tread a fine line between the demands of its creditors and the expectations of its own MPs.

Economists believe Greece could run out of funds as early as April 9th, when an IMF repayment is due.

Eurozone officials yesterday refused to hand back €1.2bn of bailout funds which Greece believed it was entitled too, a move which forces Greece to produce the ‘concrete’ reforms demanded by lenders.

Updated

The Agenda: Time ticking for Greece....

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

It looks like another day dominated by Greece debt worries. Athens has until Monday to present a convincing set of economic reforms to its lenders, and its cash reserves are looking increasingly stretched.

As our Helena Smith reported last night, Greece is now scrabbling down the back of the fiscal sofa in a bid to meet looming repayments:

In a balancing act not seen by any European administration in recent times, the cash-strapped coalition has sequestered the reserves of public bodies, seized EU subsidies destined for farmers and postponed all payments for state supplies in the scramble to continue servicing its debt and paying salaries and pensions.

Pension funds have been raided to raise money for Treasury bill auctions.

“It is clear we are reaching the end and very soon won’t be able to pay,” former finance minister, Stefanos Manos, told the Guardian. “They are scraping the bottom of the barrel for everything they can find.”

Greek officials insist that they will devise a plan by Monday, which would give investors the confidence to hand over some bailout funds:

#Greece Gov't officials say detailed reform list to be delivered Monday, hope for #Eurogroup meeting Tuesday + unfreeze of subtranche.

— Yannis Koutsomitis (@YanniKouts) March 26, 2015

Also coming up today....

- ECB chief Mario Draghi is visiting his homeland. He’ll be questioned by Italian MPs from 1.15pm GMT (2.15pm local time) about a range of issues, including the eurozone debt

- The latest UK retail sales figures for February are released at 9.30am GMT

- US weekly unemployment figures are released at 1.30pm GMT (8.30am in Washington)

And Europe’s stock markets are expected to fall, tracking a big selloff on Wall Street last night.

US shares were hit by weaker-than-expected economic data on Wednesday, including a 1.4% slide in durable goods orders.

Investors are worried that the American economy might not be prepared for a rise in borrowing costs, as Michael Hewson of CMC Markets explains:

Investors appear to be caught in two minds as to the health of the US economy, with the Federal Reserve on the one hand apparently gearing up for a rate rise, at the same time as revising down their growth and inflation expectations.

This uncertainty has not been helped by further disappointing US economic data, which has served to undermine investor confidence further.

I’ll be tracking all the main events through the day...

.jpg?w=600)