PS: Analysts at Macropolis, the respected Greek news and analysis site, are hopeful that creditors have made progress tonight:

Greece’s negotiations with its lenders have entered the final stretch after creditors met in Berlin on Monday night to discuss the details of the offer that will be put to Athens in a bid to conclude the process and pave the way for the release of €7.2bn in bailout funding

So do come back in the morning to find out if they’re right.

Snap analysis: Creditors devise proposal in Berlin, Tsipras prepares ground in Athens https://t.co/RUaaRWuSU0 #Greece #euro #ECB #IMF

— MacroPolis (@MacroPolis_gr) June 1, 2015

Updated

Closing summary: Creditors pledge intensity as time runs short

We don’t know, yet, exactly what happened in the Berlin chancellery over the last few hours; hopefully details will emerge in the morning.

But as things stand, Greece’s creditors certainly haven’t revealed details of a new offer for Athens, after talking for more than two hours.

The official line Berlin is that Merkel, Draghi, Lagarde, Hollande and Juncker are determined to work hard, and work with Greece, to resolve the crisis that has been dominating the eurozone for most of 2015.

As Germany’s spokesman put it:

“They agreed that work must continue with real intensity,”

“The participants in the talks were in close contact in recent days and want this to remain the case in the coming days both among themselves and of course with the Greek government.”

Tonight’s talks were an opportunity for Greece’s creditors to hammer out their disagreements, so they could present Alexis Tsipras with a new offer.

Another long night without specific progress on Greece, this time in Berlin. And the Greek government wasn't even around...

— Katerina Sokou (@KaterinaSokou) June 1, 2015

At first glance the Juncker mediation between the institutions on #Greece failed in Berlin.

— David Carretta (@davcarretta) June 1, 2015

Perhaps it failed, or perhaps we’re going to learn more on Tuesday?

The very fact Angela Merkel called in Draghi and Lagarde suggests that it will indeed take top-level diplomacy to resolve the deadlock.

Friday’s deadline to hand €300m to the IMF hasn’t evaporated, nor has the fact Greece’s bailout programme expires on June 30.

Schedule of #Greece payments coming up pic.twitter.com/xcQ7X42mtr

— Manish Singh, CFA (@Manish_05Singh) June 1, 2015

It’s now Tuesday in Britain, Germany and Greece already... doesn’t time fly!

So I think we’ll wrap up. We’ll be back in a few hours with a new liveblog covering the latest developments.

Goodnight! GW

Some photos of Greece’s creditors ending their meeting tonight, and leaving the chancellery, just arrived (thanks Reuters!)

Updated

Hopes of a major breakthrough tonight in Berlin have been dented, following those comments from the German spokesman as the meeting broke up.

"Step up intensity" OUCH!

— Market Elf (@MarketElf) June 1, 2015

There surely more to the "step up intensity" cliché, but we won't know until at least tomorrow I suppose.

— Yannis Koutsomitis (@YanniKouts) June 1, 2015

German govt spokesperson: Greece creditors meeting ended in Berlin. Merkel, Lagarde, Draghi discussed status of Greek negotiations. (BBG)

— Holger Zschaepitz (@Schuldensuehner) June 1, 2015

Creditors agree that 'intensive work' needed on Greece

Newsflash from Germany: Creditors have agreed that there must be “intensive work” on Greece, a spokesman says.

And Merkel, Draghi, Lagarde, Hollande and Juncker will stay in close contact with each other, and with Greece, in the days ahead.

That does not sounds like a breakthrough....

Here’s the snaps off Reuters:

- 01-Jun-2015 23:25:10 - GERMAN GOVT SPOKESMAN - MERKEL, HOLLANDE, JUNCKER, LAGARDE AND DRAGHI AGREED ON NEED FOR INTENSIVE WORK ON GREECE

- 1-Jun-2015 23:26:06 - GERMAN GOVT SPOKESMAN -PARTICIPANTS AT TALKS WILL REMAIN IN CLOSE CONTACT IN COMING DAYS, INCLUDING WITH GREEK GOVT

•Merkel, Draghi agree Greek talks must step up in intensity http://t.co/3ihkV8WZI2 pic.twitter.com/2bh3DCWFQx

— ForexLive (@ForexLive) June 1, 2015

#Greece mini-summit in Berlin ended. Waiting for more drama to come.

— David Carretta (@davcarretta) June 1, 2015

Financial news service RANsquawk is reporting that the Berlin meeting has just concluded....

#GREECE CREDITORS MEETING IN BERLIN HAS NOW ENDED - #GERMAN SPOKESMAN

— RANsquawk (@RANsquawk) June 1, 2015

The latest word from Berlin is that creditors don’t plan to hit Greece with a ‘final ultimatum’, but will craft the outlines of a deal.

Whether Athens sees it the same way is another matter.....

Or in other words, something for Tsipras to then call an ultimatum. (via http://t.co/jEObfJ1aQZ) pic.twitter.com/B5OEXjksjP

— Joseph Cotterill (@jsphctrl) June 1, 2015

The FT’s Peter Spiegel reports that the Berlin meeting includes paperwork showing where compromises might be made:

Berlin summiteers working frm paper prepared by @EU_Commission to find trade-offs acceptable to all #Greece creditors http://t.co/9lt781AwoE

— Peter Spiegel (@SpiegelPeter) June 1, 2015

Ian Traynor: Merkel is trying to defuse the crisis

This meeting in Berlin was meant to be focused on the worthy topic of boosting Europe’s economy through more investment.

But it’s turned into so much more, once Christine Lagarde and Mario Draghi arrived unexpectedly to discuss the Greek crisis.

Our Europe editor, Ian Traynor, reports:

The German chancellor Angela Merkel moved to try to defuse Greece’s financial and European crisis late on Monday, converting a routine long-scheduled meeting with French and EU leaders into a mini-summit on Greece that was said to be preparing a final response to Athens’ intractable debt dilemmas.

Merkel met France’s president François Hollande and the president of the European commission, Jean-Claude Juncker, for what was billed as a session on how to boost investment in the EU. But they were joined by Mario Draghi, the president of the European Central Bank, and Christine Lagarde, the head of the International Monetary Fund, in what turned into a late-night session on Greece.

Athens is facing insolvency and payments of €1.6bn (£1.1bn) to the IMF within the next few weeks, with the first payment of €305m due by Friday. Now it appears that the Greek drama is shifting up a gear, heading for its denouement, after five months of negotiations between the Greeks and its eurozone/IMF creditors going nowhere.

Merkel’s staff let it be known that the chancellor wanted the mini-summit in Berlin to deliver a “final offer” to Athens, German public television reported. “The creditors want to agree a common position tonight,” ZDF television said. Merkel wanted the deal sealed before a meeting this weekend in Germany of the G7 countries. Whether the terms of the proposed resolution represented an ultimatum to Greece was unclear.

Updated

Tonight’s emergency meeting shows that Greece’s creditors are losing patience, after months of crunch meetings, tough negotiations and scarce progress:

So says the WSJ tonight, which adds:

Officials from European institutions and the International Monetary Fund sent a draft text on the economic overhauls that Greece needs to implement to unlock bailout financing to a meeting in Berlin of key European leaders, according to people familiar with the matter.

Creditors Prepare ‘Final’ Text of Greek Bailout Deal - @MMQWalker & @v_dendrinou report on what's happening in Berlin http://t.co/CTj3aQ8MXh

— Nick Malkoutzis (@NickMalkoutzis) June 1, 2015

Greece turns to Berlin to learn its fate

Over in Athens, everyone is watching and waiting to see how this gripping crisis develops.

Helena Smith our correspondent reports:

Excluded from talks that he had wanted to attend, the Greek prime minister Alexis Tsipras has been relegated to the sidelines tonight - forced by circumstance into the role of spectator at what may well be the make-or-break meeting that decides the fate of his debt-stricken country.

Earlier on Monday a finance ministry official had told me:

“We are on the brink. We know something is going to happen, we just don’t know what.”

This, it seems, is it. Going into a mini meeting of senior cabinet officials held at the prime minister’s office tonight, the man heading Greece’s negotiation team, deputy foreign minister, Euclid Tsakalotos told reporters:

“People don’t have to be worried.”

No statements were made when the meeting ended an hour ago. The leftist-led government is desperate to douse any concerns over a run on banks.

Describing tonight’s Berlin talks, the daily newspaper Ethnos said it was likely that the Greek prime minister would be presented with a proposal offering the only “realistic solution” to avert bankruptcy and remain in the euro zone.

The solution was likely to be presented in the form of an ultimatum, the newspaper said.

However, sources are suggesting that they do not expect a statement to be made by Greece’s creditors until Tuesday. This may, of course, be wishful thinking....

Updated

The Financial Times has just published a handy explanation of the differences that have emerged between Greece’s creditors in recent weeks, prompting tonight’s emergency mini-summit.

The IMF has been holding to a tough line, out of respect for its own lending rules and regard for pressure from countries in other parts of the world, which say Athens has already enjoyed very favourable treatment.

The European Commission has argued for more generous terms for Athens because it sets a high priority on keeping the eurozone intact — a key symbol of EU unity.

The ECB, too, wants to keep the common currency together but is also afraid of damaging its credibility by overextending its role as a central bank.

. And if Angela Merkel, Europe’s most powerful politician, decides that Greece needs more financial aid, that cash would probably come from the eurozone not the IMF, the FT adds.

Greek bailout monitors hold emergency summit http://t.co/suWUwsiUME

— FT Economics (@fteconomics) June 1, 2015

#grexit berlin mini-summit kicked off 2130. 'endgame begins' says @welt, quotes german sources.'the aim is to make the greeks a final offer'

— Ian Traynor (@traynorbrussels) June 1, 2015

Tonight’s meeting on Greece is now well underway, between Angela Merkel, Francois Hollande, Jean-Claude Juncker, Mario Draghi and Christine Lagarde.

One official told Reuters that:

“They will discuss how to proceed and and whether they should make a new offer for an agreement to (Greek Prime Minister Alexis) Tsipras.”

Tonight’s meeting in Berlin is missing one crucial actor - Alexis Tsipras himself, the left-wing leader who swept to power in January on a promise to end austerity and break away from the last five years.

Tsipras had hoped to reach a political agreement over Greece, but tonight’s meeting suggests he’s going to get an ultimatum from creditors.

And that might not be compatible with his own political mandate, so whatever emerges from Berlin probably won’t be the end of this story.

Tsipras not invited to the party in Berlin. He will be handed a take it or leave it when he does finally sit down with Greece's creditors.

— Megan Greene (@economistmeg) June 1, 2015

People actually voted for Syriza expecting minimum wages to go up, taxes to go down, to be hired in the public sector & the end of austerity

— helena chari (@helena_chari) June 1, 2015

Updated

It’s now midnight in Athens, but prime minister Tsipras and his top team are going nowhere yet -- they’re watching events in Berlin like the rest of us

#Greece cabinet mtng over. Tsipras in continuous mtng w Varoufakis, Alt FM Tsakalòtos & StateMin Pappàs, monitoring developments in Berlin

— Yannis Koutsomitis (@YanniKouts) June 1, 2015

Here’s another photo of “Super Mario” Draghi being whisked into tonight’s meeting in Berlin:

#Draghi pulling into the Chancellery in Berlin for talks w #Merkel #Hollande #Lagarde & #Juncker on #Greece #IMF #ECB pic.twitter.com/WN8dlYg7az

— Patrick Donahue (@patrickjdo) June 1, 2015

With thanks to Patrick Donahue, Bloomberg’s political correspondent in Berlin.

It’s looking like quite a night....

Greece: Final countdown has begun. In Berlin, now, meeting of IMF, ECB, EUCOM, GER and FRA. Aim is to agree on a final offer to Tsipras.

— Stefan Leifert (@StefanLeifert) June 1, 2015

#IMF confirms Ms Lagarde is in Berlin to consult on #Greece. /via @mignatiou

— Yannis Koutsomitis (@YanniKouts) June 1, 2015

And here’s the German chancellery tonight, where the heads of the EC, the ECB, the IMF, Germany and France are trying to devise an offer to Greece to keep it in the euro and calm the crisis.

A photo of Mario Draghi, head of the European Central Bank, arriving at tonight’s talks in Berlin has just arrived:

(OK, it’s not the best picture of Draghi ever, but he’s third from the left)

Updated

Germany’s Frankfurter Allgemeine Zeitung newspaper reckons that tonight’s talks in Berlin could go late into the night (it’s currently 10.15pm there) in a bid to break the deadlock over Greece.

#grexit merkel hollande in berlin. expected to agonise over greece into the wee hours. seeking final offer? http://t.co/CycVRakavP

— Ian Traynor (@traynorbrussels) June 1, 2015

Greek cabinet meeting ends

Tonight’s cabinet meeting in Athens has ended, but the top ministers are now hanging around waiting for news from Berlin.....

#greece' mini cabinet meeting ended. Tsipras, Varoufakis, Pappas, Tsakalotos still at PMnistry waiting for Berlin https://t.co/MVLEUkXCz0

— Keep Talking Greece (@keeptalkingGR) June 1, 2015

Channel Four’s Paul Mason has heard that Greece wants the European Central Bank to provide more liquidity to its banking sector, as part of any deal.

IMF-ECB said to be ready to offer take/leave deal to Greece. Greek source saying upfront verbal guarantee of restored liquidity = baseline.

— Paul Mason (@paulmasonnews) June 1, 2015

Greek banks have been dependent on emergency liquidity for months, ever since the ECB decided it would no longer accept Greek government bonds as collateral to guarantee loans (a decision that enraged Athens)

Why Greece's creditors are talking tonight

If you’ve been following this crisis closely, you’ll already know that June is an absolutely crunch month for Greece. But other readers might find this helpful:

Athens owes €305m to the International Monetary Fund on Friday, and it may struggle to find the funds. It could bundle the payment in with other looming IMF bills, which total €1.6bn this month.

Here's the list of June repayments again #Greece pic.twitter.com/kgdxSjfLTC

— Derek Gatopoulos (@dgatopoulos) June 1, 2015

Greece is still ‘owed’ €7.2bn in bailout loans, but they are frozen while the two sides have argued , largely fruitlessly, about a new bailout programme to replace the original one agreed in 2012.

Creditors agreed a four-month extension in late February, which expires on 30 June.

Without a deal, Greece could simply plough into July without its last tranche of bailout funds. It then faces billions of euros of extra repayments this summer, including €6.7bn to the European Central Bank. That’s why economists think Greece needs to agree a third ‘programme’ (a bailout) soon.

But that can’t be discussed while the current programme is mired in deadlock. Thus tonight’s talks in Berlin to decide a common position on Greece, at the highest level.

Greek officials are hoping for positive news from Berlin:

#Greece gov't official: "We expect developments tonight" ~@ThePressProject

— Yannis Koutsomitis (@YanniKouts) June 1, 2015

Rumours are swirling that Athens is about to get a ‘take it or leave it’ offer.

RadioRadicale’s Brussels correspondent, David Carretta, tweets the latest word:

From Berlin tonight could come a "Last offer" to #Greece I've been told.

— David Carretta (@davcarretta) June 1, 2015

Several analysts and commentators are talking about the Greek crisis entering its “endgame” tonight, after four months of deadlock.

Greek radio journalist Giannis Papageorgiou points out that Christine Lagarde has lingered on in Germany after last week’s G7 meeting of central bankers and finance chiefs, ready for tonight’s meeting.

#Lagarde and Thomsen stayed in GER after G7. Final scenario for #Greece on the way. Some say #Tsipras has already agreed on pensions reforms

— Giannis Papageorgiou (@Papageorgiou_J) June 1, 2015

(that’s Poul Thomsen, the IMF’s European director and former joint head of the Troika delegation in Athens)

Updated

Treat with caution: Germany’s Die Welt is reporting that Greece might be prepared to compromise on one of its ‘red lines’, pension reforms.

They say that PM Alexis Tsipras has told creditors that he “wants to talk” about pension cuts and a later retirement age. That’s not the same as a concrete proposal, though. More here

Die Welt report on #Greece PM Tsipras alleged readiness to compromise on pensions & retirement age http://t.co/nqJ4ABOTaT ~@welt

— Yannis Koutsomitis (@YanniKouts) June 1, 2015

Alexis Tsipras has been pushing for a political deal for weeks, arguing that technical talks between officials can never resolve this crisis.

Tonight’s talks between the Big Five in Berlin suggest he’s getting his wish, tweets our Europe editor Ian Traynor.

#grexit sunday @atsipras said thing had to be settled by leaders. monday evening berlin merkel/hollande seem to be conceding he's right

— Ian Traynor (@traynorbrussels) June 1, 2015

But can Tsipras possibly get an offer that’s acceptable to enough of his party?

Earlier today, hope was building in Greece that a temporary deal could be reached.

One well-placed insider told my colleague Helena Smith:

“We are very close to the edge of the cliff, we are on the brink but we are not sure what is going to happen - yet.”

Reuters: Draghi and Lagarde join Merkel, Hollande and Juncker

Reuters is also reporting that Mario Draghi and Christine Lagarde will meet Angela Merkel, Francois Hollande and Jean-Claude Juncker in Berlin tonight.

So the leaders of Greece’s three Institutions (the former Troika) are gathered in one place to discuss the crisis, along with the leaders of the two most powerful countries in the eurozone.

This might just be a ‘moment’ in the crisis.

Over to Reuters:

Draghi, Lagarde joining Berlin meeting on Greece.

European Central Bank President Mario Draghi and IMF chief Christine Lagarde will join the leaders of Germany, France, and the European Commission for talks on Monday evening in Berlin on Greece, European Union officials said.

The goal of the meeting was to reach a joint position on how to negotiate with Greece, the officials said.

Athens and its creditors from the euro zone countries and the International Monetary Fund are trying to hammer out a deal that would prevent the country from defaulting on its debt and potentially leaving the euro zone.

Earlier, German Chancellor Angela Merkel, French President Francois Hollande and European Commission President Jean-Claude Juncker gave brief statements before meeting to discuss the digital economy. They made no mention of Greece. [end]

The MNI newswire is reporting that a statement might be released following tonight’s meeting in Berlin.

We may get a statement following Berlin meeting today --MNI sources

— Live Squawk (@livesquawk) June 1, 2015

Greek media are also reporting that prime minister Alexis Tsipras is meeting with some of his cabinet tonight:

Mini cabinet in progress with the participation of PM #Tsipras and ~10 ministers, according to local media. #Greece #politics

— Manos Giakoumis (@ManosGiakoumis) June 1, 2015

Bloomberg: Greece’s Creditors Said to Meet in Berlin to Discuss Plans

Hello again. An interesting development tonight to flag up.

Angela Merkel, Francois Hollande and Jean-Claude Juncker have been meeting in Berlin tonight to discuss a range of issues, including Greece (as we covered earlier). And there are some reports that they could be developing a proposal to present to Greece, to avoid a default.

Details are sketchy, and obviously rumours are rife. But Bloomberg had a good take. They reckon that the European Central Bank and the International Monetary Fund are involved too.

Bloomberg: Greece’s Creditors Said to Meet in Berlin to Discuss Plans

It would make sense, given today’s concerns that Greece is running out of time to avoid a default, capital controls or fresh elections [as Goldman Sachs explained]

Here’s a flavour of Bloomberg’s piece:

Top level talks were said to be taking place in Berlin on Monday evening to hammer out a proposal that would be presented to Greece as its only realistic chance of avoiding default and safeguarding its membership of the euro.

German Chancellor Angela Merkel met with French President Francois Hollande and European Commission President Jean-Claude Juncker in the German capital. Representatives of creditor institutions are said to be preparing to convene with them this evening to discuss a plan to resolve the deadlock over Greece, according to people familiar with the plan. They asked not to be named because the negotiations are private.

The talks are at the highest level, according to the people. They involve Christine Lagarde, managing director of the International Monetary Fund, and European Central Bank President Mario Draghi, they said. A spokesman for the ECB declined to comment on the meeting....

Merkel, Holland, and Juncker meeting tonight to save Greece. http://t.co/xFAF2bvjxL

— Joseph Weisenthal (@TheStalwart) June 1, 2015

Some big names crashing Merkel/Juncker/Holladde Greece party: Draghi and, supposedly, Lagarde too.

— Landon Thomas Jr. (@Landonthomasjr) June 1, 2015

We’ll keep an eye for further developments....

Updated

Markets mixed after manufacturing data

Worries about Greece continued to unsettle investors, but differing results from May’s manufacturing surveys was the main influence on markets. Signs of growth in Europe lifted most continental markets, but a disappointing UK figure - along with a falling oil price - helped send the FTSE 100 lower. Wall Street edged higher after a better than forecast ISM factory activity index, which pointed to a revival in the US economy but also suggested the Federal Reserve might indeed raise interest rates before the end of the year. The final scores showed:

- The FTSE 100 finished down 30.85 or 0.44% at 6953.58

- Germany’s Dax added 0.19% to 11,436.05

- France’s Cac closed 0.35% better at 5025.30

- Italy’s FTSE MIB dipped 0.26% to 23,435.67

- Spain’s Ibex ended up 0.18% at 11,238.1

On Wall Street, the Dow Jones Industrial Average is currently up 21.63 or 0.12%.

On that note, it’s time to close up for the evening. Thanks for all your comments, and we’ll be back again tomorrow.

Italy’s public finances are improving, according to the latest government figures.

The country’s state sector budget deficit came in at around €4.3bn in May, compared to €6.5bn in the same month last year. The Treasury said the deficit for the first five months of the year had narrowed by around €15bn from the same period last year to €33.8bn.

The broader deficit figure which the stablity and growth pact uses is expected to fall from 3% of GDP in 2014 to 2.6%.

Back with manufacturing, and here’s Markit’s global chart:

Global #manufacturing's soft-patch persisted in May amid a stalling of trade flows http://t.co/5bYol107BM pic.twitter.com/JRg5F31bCJ

— Chris Williamson (@WilliamsonChris) June 1, 2015

A Greek exit from the eurozone may cause market ruptions in the short term but it could be a different story looking further ahead, says Capital Economics.

But the recent moves in bond markets suggesting a deal could be reached may be mistaken, it adds, with spreads between German bunds and other goverment bonds looking remarkably low. Capital Economics Kevin Ferriter said:

Spreads have presumably been contained as a result of four beliefs, each of which may be mistaken. First, a deal could be reached between Greece and its creditors. Second, a default does not automatically mean that Greece must exit the euro. Third, the ECB has backstops in place which are intended to prevent contagion. And fourth, if Greece does abandon the euro, this does not mean that other countries will necessarily follow suit.

However, we think that investors are being complacent about these risks. Although a deal may be reached in these negotiations, the matter at hand is only the release of the final tranche of the existing bailout. We have not even got to the issue of the third bailout yet. Given how fractious the current talks have been, we envisage that further negotiations would reach an impasse.

Meanwhile, although there is no automatic link between Greek default and Greek exit from the euro, one surely makes the other more likely. In particular, if losses are imposed on Greek debt held by the ECB, the Bank probably wouldn’t then increase its exposure to Greece by sanctioning the provision of liquidity to its banks. In this situation, staying in the euro could mean a full-blown financial crisis in Greece. And even if defaulting allowed the Greek government to ease off on austerity, its economy will probably require a significant currency depreciation (only possible outside the euro-zone) to restore the competitiveness necessary to boost growth.

Whatever the specifics of how a Greek default were handled, we are sceptical that the ECB’s backstops would fully insulate other markets. The purchases of its quantitative easing (QE) programme be distributed across countries in proportion to the Bank’s capital key, so it is currently an inappropriate tool for fire-fighting spikes in the bond markets of particular countries. And for the ECB’s outright monetary transactions (OMTs) programme to be activated for a country, its government must have signed and be abiding by the conditions of a Memorandum of Understanding. Spreads could rise significantly before sufficient political will was mobilised to circumvent these technicalities.

Finally, if Greece does exit the euro-zone, it is possible that it will only be the first domino. If Greece’s economy eventually thrives without the choke of austerity and with a devalued currency, this may fuel the rise of anti-austerity and euro-sceptic movements in other European countries.

Overall, we still think Greece’s future inside the currency union remains highly uncertain, and if and when it leaves, this is likely to have a large short-run impact on markets – higher spreads on euro-zone sovereign bonds, a weaker euro, falls in equity prices and a rise in safe-haven demand. But the longer-term impact could be quite different if, as we expect, Greece was better off outside the euro-zone.

Updated

The US market seems uncertain what to make of this latest set of data.

As reported, the ISM manufacturing index came in stronger than forecast, and construction spending rose 2.2% to an annual rate of $1trn, the biggest percentage increase since May 2012.

But other figures showed US consumer spending was unexpectedly flat in April as households cut back on expenditure and boosted their savings.

So the Dow Jones Industrial Average is drifting somewhat, and is currently around 7 points or 0.03% lower.

The ISM data adds to the likelihood of the US Federal Reserve raising interest rates in the third quarter, says James Knightley of ING. He says:

The US ISM manufacturing index for May has come in at 52.8 versus 51.5. This is above the 52.0 consensus expectation and is the best reading since February. The production component actually fell (to 54.5 from 56.0 in April), but there was a decent rise in new orders (55.8 versus 53.5 previously) and employment (51.7 versus 48.3). Indeed, new orders are at a five month high while the employment component is recording its strongest reading since January.

This all hints at a rebound from the economic contraction experienced in the first quarter of 2015 although other numbers, such as today’s personal income and spending report, suggest it won’t be particularly vigorous growth in the second quarter.

Nonetheless, with the labour market continuing to make progress and real incomes moving in the right direction we suspect that consumer spending will make a more positive contribution to the growth story in the second half of the year with the Federal Reserve likely responding in the third quarter of 2015 with tighter monetary policy.

US manufacturing growth accelerates, says ISM

Here’s the Institute of Supply Management’s manufacturing data, which shows the pace of growth rising in May, with new orders and employment both rebounding.

The ISM index of national factory activity was 52.8, up from 51.5 in April. The April figure was unchanged from March and the lowest since May 2013.

The employment index rose from 48.3 in April to 51.7 in March, while new orders climbed from 53.5 to 55.8.

Updated

Like the UK, final US manufacturing PMI misses forecasts but beats last month, at 54.0 vs 54.2 exp. and 53.8 in April #US #manufacturing

— Spreadex (@spreadexfins) June 1, 2015

Over in the US it’s time for the day’s two manufacturing surveys.

First comes Markit’s data, with its purchasing managers’ index coming in at 54 in May, up slightly from an initial reading of 53.8 and marginally lower than April’s 54.1.

The new order component of the index fell from 55.3 in April to 54.3, its lowest level since January 2014. Chris Williamson, chief economist at Markit, said:

With manufacturers reporting the smallest rise in new orders since the start of last year, the survey provides further evidence that the strong dollar is hurting the economy.

While the economy still looks set to rebound from the decline seen in the first quarter, the extent of the second quarter recovery therefore remains highly uncertain and could well disappoint.

The ISM survey should follow shortly...

Updated

Summary: Greek fears as crunch month begins

Time for a recap on the Greek situation:

Chief European economist Huw Pill predicts that “a new political mandate and thus a new government, a referendum or new elections ” may be required in Greece.

Not only is it possible that we may need to see sovereign technical default and/or blocked Greek bank deposits in order to come to an accommodation between Greece and its official creditors, it may be necessary to do so in order to break the current impasse in negotiations.

Political tensions are swirling in Athens, after a group of Syriza MPs forced economist Elena Panaritis to withdraw as Greece’s new IMF representative.

One insider blamed the move on “the usual personal vendetta,” showing that

The European Commission has not reacted well to an opinion piece written by prime minister Alexis Tsipras in Le Monde today, accusing creditors of threatening European democracy.

Spokeswoman Mina Andreeva told reporters in Brussels that:

What matters more than op-eds are concrete reform proposals.

As one official put it:

“We are very close to the edge of the cliff, we are on the brink but we are not sure what is going to happen - yet.”

Updated

Paul Mason of Channel 4 News has a good explanation on why Greece’s prime minister launched such a fierce critique of Europe’s approach to the crisis, in Le Monde today.

Mason (who is well-connected with Syriza) says Tsipras has reassessed his view of the situation, and is now convinced Germany wants to create a two-speed Europe...

“...where the ‘core’ will set tough rules regarding austerity and adaptation and will appoint a ‘super’ Finance Minister of the EZ with unlimited power, and with the ability to even reject budgets of sovereign states that are not aligned with the doctrines of extreme neoliberalism.

For those countries that refuse to bow to the new authority, the solution will be simple: Harsh punishment. Mandatory austerity. And even worse, more restrictions on the movement of capital, disciplinary sanctions, fines and even a parallel currency”.

So Tsipras has responded by digging in, and showing he’s prepared to take Greece into a default if the creditors don’t compromise.

Mason again:

So we’re in yet another nail-biting week. In a final flourish Tsipras advised the EU leaders to read Hemingway’s novel, For Whom the Bell Tolls. As it’s about a vicious civil war and the collapse of democracy in Europe in the 1930s, I think we all get the drift.

But he could just as easily have quoted John Donne, from whom the phrase is taken: “If a Clod bee washed away by the Sea, Europe is the lesse, as well as if a Promontorie were.” We’ll know, I estimate within seven days, whether the Germans think Greece a promontory worth saving.

More here: Greece: a clod of earth worth saving?

As always, @paulmasonnews has @syriza_gr inside dope: thought deal was nigh swapping more austerity for debt relief https://t.co/xNBQwxELSQ

— Peter Spiegel (@SpiegelPeter) June 1, 2015

Greek insiders still hoping for political solution

Back in Athens, Prime minister Alexis Tsipras’ anti-austerity coalition is hoping that tonight’s meeting between the German chancellor Angela Merkel and French president Francois Hollande will provide a breakthrough (of sorts), reports Helena.

The Greek media is now full of reports of an interim deal being cut that would tide the country over in the coming months in terms of its heavy debt repayment schedule - but leave all the hard work of a longer-term agreement for the fall.

The well-informed Naftemporiki is splashing the story under the headline “close to a temporary agreement.”

Tsipras, it says, is placing his hopes on tonight’s meeting helping to create a “political solution” even if Greece will not be the focus of talks when Merkel, Hollande and EU president Jean-Claude Juncker do sit around the table.

Naftemporiki says:

“Under no circumstances will it be the broad “unified” deal that the government had hoped for, since it will even leave open the evaluation of the current programme which expires on June 30.

The “good” scenario for the government would be for the deal [to include] a forecast for the debt (something that at this juncture is considered extremely difficult if not impossible) and to have a growth prospect (which is the more likely scenario).

Essentially, with a “temporary” agreement the government and the prime minister will solve, albeit fleetingly, the suffocating problem of the country’s financial needs while on the lenders part a painful “Grexit” will be avoided.”

Both sides, the paper said, had agreed that the differences of view expressed by technical teams had not been resolved and would not (and could not) be bridged in the days ahead.

Elena Panaritis’ resignation letter today has (if unwittingly) underlined the disparities saying “the country is going through its most difficult period.”

A finance ministry official, speaking on condition of anonymity, told me earlier that that the government recognised it was “very close to the edge of the cliff.”

He said:

“We are very close to the edge of the cliff, we are on the brink but we are not sure what is going to happen - yet.”

The scenario sounds very much like the four-month extension we had reported in this blog on May 21st - under which Greece would be given some leeway to draw up reforms (and perhaps hold fresh elections).

Updated

The euro is coming back from its earlier selloff too....

#Euro up on ‘imminent’ Greek deal chatter. Common currency trades now >$1.0950. pic.twitter.com/8s3kkg2M4W

— Holger Zschaepitz (@Schuldensuehner) June 1, 2015

Don’t get excited if you hear that a Greek deal is coming this afternoon.

A wild, unsourced and frankly baffling rumour did just sweep City trading floors and Twitter, but there seems to be nothing in it.

And it’s now being denied:

- OFFICIALS CLOSE TO CREDITOR TALKS WITH ATHENS DENY MARKET TALK THAT A DEAL WITH GREECE IS TO BE ANNOUNCED THIS AFTERNOON

A false alarm on Greece isn’t new. What’s truly perplexing, though, is that it actually moved the markets...

Bund future erases gains on unconfirmed Greece rumour. What a market. pic.twitter.com/LQQIKib84B

— Jonathan Ferro (@FerroTV) June 1, 2015

That Greek deal rumour was possibly the most ridiculous things I've ever seen on finance twitter. I'm walking away for the day in protest.

— Jonathan Ferro (@FerroTV) June 1, 2015

Updated

In the wake of Elena Panaritis’ withdrawal, the Greek government has issued one of its famous non-papers distancing finance minister Yanis Varoufakis from her appointment to the International Monetary Fund in the first place.

Helena Smith, our correspondent in Athens, reports.

“The choice of Elena Panaritis, as the country’s IMF representative, was made collectively,” the paper stated. “The view that has been heard that Yanis Varoufakis appointed her does not correspond to reality.”

In her own statement, Panaritis made clear that she did not ask for the post.

“As I never sought this post, and given that I accepted it exclusively to help the government based on my experience on the way the IMF works (and other corresponding organisations) it is impossible for me to accept my appointment in the midst of the negative reactions of Syriza’s MPs and cadres.”

A finance ministry official told me this morning that Panaritis had been at the receiving end of ugly sniping. “It’s the usual personal vendetta,” said one.

Panaritis thanked Varoufakis and national economy minister Giorgos Stathakis for their support.

The irony, though, is that Panaritis, a former World Bank economist, was thoroughly disheartened by the Pasok party (she was an Pasok MP from 2009 to 2012), and especially its erstwhile leader George Papandreou who persuaded her to leave the US for Greece.

Papandreou, who appealed to the IMF for help when it became clear that the country would be unable to stand alone, financially, was accused by Panartisis of ignoring her, and the invaluable advice she had to offer, when she moved, at his request, to Athens.

Updated

Bond traders are ditching short-term Greek debt this morning, driving up the yield on two-year bonds higher into the danger zone.

The lack of a deal and Alexis Tsipras’s claim that Greece’s creditors are threatening European democracy have not calmed nerves in the City today:

- GREEK TWO-YEAR BOND YIELDS RISE OVER 100 BASIS POINTS TO DAY’S HIGH OF 24.67%

Associated Press is also reporting that government MPs forced Elena Panaritis to abandon plans to represent Greece at the International Monetary Fund.

Elena #Panariti, named as #Greece's representative at the #IMF, declines post after fierce criticism from members of governing #Syriza.

— Elena Becatoros (@ElenaBec) June 1, 2015

Greece's IMF candidate withdraws amid political backlash

Breaking News! Elena Panaritis has just announced that she does not wish to be Greece’s new representative at the International Monetary Fund, according to local media.

She has withdrawn following the backlash from Syriza MPs who wrote to prime minister Alexis Tsipras, saying her previuus support for Greece’s bailout programmes made her an unacceptable candidate (see earlier post).

This u-turn calms the danger that the government could split.

But it’s also something of a blow to finance minister Yanis Varoufakis, as he’d proposed Panaritis for the role.

It's impossible to accept my appointment (at the #IMF) amid negative reactions from #SYRIZA MPs, says @Elena_Panaritis (via @naftemporikigr)

— Manos Giakoumis (@ManosGiakoumis) June 1, 2015

Blow To Greece Talks As Appointed IMF Rep. Panaritis Turns Down Post

— Live Squawk (@livesquawk) June 1, 2015

#Panariti declares no longer interested to represent #Greece in IMF. Syriza crisis over. Varoufakis continues as FinMin.

— Keep Talking Greece (@keeptalkingGR) June 1, 2015

Problem solved!? #Greece #Panaritis https://t.co/jG7eogWIL6

— The Greek Analyst (@GreekAnalyst) June 1, 2015

EC: Never mind the op-eds, where's the reforms?

As feared, Alexis Tsipras’s blunt attack on the “absurd demands” made by Greece’s creditors has not improved the mood in Brussels.

Jean-Claude Juncker’s official spokesperson, Mina Andreeva, has just told reporters that it’s more important to deliver ‘concrete reform proposals’ rather than opinion pieces in Le Monde.

Danny Kemp, AFP’s Brussels deputy bureau chief, has all the details from Andreeva’s briefing:

'We are not in the business of setting deadlines -- the only deadline is the end of June' says EU's @Mina_Andreeva on Greece

— Danny Kemp (@dannyctkemp) June 1, 2015

Ouch: 'What matters more than op-eds are concfrete reform proposals', says @Mina_Andreeva of Tsipras comments

— Danny Kemp (@dannyctkemp) June 1, 2015

And there’s no chance of an emergency eurogroup meeting until those proposals are drawn up:

Hint: 'The next eurogroup is on June 18, the eurogroup stands ready to reconvene earlier if need be'

— Danny Kemp (@dannyctkemp) June 1, 2015

Sigmar Gabriel, the vice-chancellor of Germany, says he’s not given up hope of a Greek deal.

Gabriel told reporters in Berlin that:

“I believe that all the proposals are now on the table and we can only hope that those holding political responsibility, also those in responsibility in Greece, will use the little time that is still left to reach decisions.”

(quote via Reuters)

Nice line in understatement here:

GERMAN GOV'T SPOKESMAN SAYS GREECE WILL NOT BE CENTRAL TOPIC AT MEETING OF MERKEL, HOLLANDE AND JUNCKER BUT CAN'T RULE OUT IT WON'T COME UP

— Pauly@spz_trader (@spz_trader) June 1, 2015

This is why June is such a crunch month for Greece:

Key dates for #Greece in Jun (via @MacroPolis_gr) pic.twitter.com/VDqrqxQBES #economy #politics #ec #ecb #imf #banking #markets

— Manos Giakoumis (@ManosGiakoumis) June 1, 2015

Goldman: New Greek elections may be needed to break impasse

Negotiations between Greece and her creditors seem to have hit an impasse, and could trigger new elections, a referendum or capital controls on bank deposits, or even a default, warns Goldman Sachs this morning.

Huw Pill, Goldman’s chief European economist, fears it will be “very challenging” for the two sides to reach a deal to unlock the final €7.2bn of Greece’s bailout aid.

And although his “base case” is still that a compromise will ultimately be reached, the situation could become a lot worse first.

Pill argues that the platform on which the current Greek government was elected – to retaining the Euro but with no further adjustment and/or external oversight – is “irreconcilable” with the demands of lenders.

And without a deal, Greece’s remaining government cash reserves will soon be exhausted.

Facing this reality, a new political mandate and thus a new government, a referendum or new elections will be required in Greece.

Not only is it possible that we may need to see sovereign technical default and/or blocked Greek bank deposits in order to come to an accommodation between Greece and its official creditors, it may be necessary to do so in order to break the current impasse in negotiations.

Default, capital controls, euro referendum, new elections. All now real possibilities for Greece, says Goldman: pic.twitter.com/Wz7VdctbRx

— Jamie McGeever (@ReutersJamie) June 1, 2015

Pill argues that Greece’s creditors cannot give ground on three key principles, which aren’t compatible with Athens’ own pledges:

- Retaining the Euro requires further economic adjustment in Greece;

- To the extent that this adjustment entails further financial support (which is selfevident given upcoming obligations), that support will only be provided on the basis of conditionality.

- In order to assess compliance with such conditionality, external oversight of the Greek economy is required.

And prime minister Tsipras can’t change his own position without a new political mandate.

As such, Goldman believes that the probability of a Greek exit is “clearly not zero”, and has been rising in recent weeks.

As Pill concludes:

The ongoing negotiations between Greece and its official creditors are intensely political. And forwardlooking economic rationality is not characteristic of such interactions.

Not only is it possible that we may need to see technical default and deposit blocks in order to come to a new programme, it may be necessary to do so in order to break the current impasse in negotiations.

Updated

Pressure builds over Greece's IMF representative

Back to Greece....and it appears that a major row is blowing up over the nomination of the new Greek representative at the IMF.

As flagged earlier, 43 Syriza MPs and other senior party officials have signed a letter expressing strong disapproval for the selection of Elena Panaritis.

They argue that Panaritis is a poor choice, as she was a Pasok MP between 2009 and 2012, when the left-wing party signed up for Greece’s first bailout. As the letter puts it:

“A prominent representative of bailout policies cannot represent the government...It’s not a symbolic but a political issue. It’s a wrong decision and we ask that it is taken back.”

Panaritis was the favoured choice of finance minister Yanis Varoufakis (thus his announcement yesterday that rumours of his resignation were grossly premature)

But pressure is building. Enikos, the Greek news site, has published photos of a rather stressed-looking Varoufakis last night after talks with prime minister Alexis Tsipras.

Varoufakis under pressure and it shows - PHOTOS - http://t.co/ePGE9awzPs pic.twitter.com/ZcOMrR5VE5

— enikos_en (@enikos_en) June 1, 2015

There are reports today that Tsipras is now looking for a new candidate to replace Panaritis.....

Britain’s factories grew a little faster last month. The UK manufacturing PMI edged up to 52.0, up from 51.8.

Heads-up. German Chancellor Angela Merkel, French President François Hollande and European Commission President Jean-Claude Juncker are meeting in Berlin today for talks about Europe’s future.

Greece’s bailout talks, and David Cameron’s bid to renegotiate the UK’s links with Europe, will be on the table.

Just in case there's any doubt about who makes the call on #Grexit / #Brexit - Merkel, Hollande and Juncker hold 3-way talks in Berlin today

— Danny Kemp (@dannyctkemp) June 1, 2015

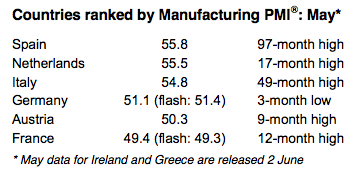

Eurozone factories post modest growth

It’s official: Germany and France are dragging the eurozone back.

Markit’s Eurozone Manufacturing PMI, just released, came in at 52.2 in May. That is up from April’s 52.0 and matches March’s figure (which was a 10-month high), but is below the flash estimate of 52.3 two weeks ago.

And as covered earlier, Spain and Italy performed rather better than the eurozone’s two largest members:

Chris Williamson of Markit says factories in the core need to watch out:

“The rate of growth is modest rather than spectacular, however, and there are clearly countries which continue to struggle. Weakness is centred in the region’s core, with France’s manufacturing sector still in decline and Germany only seeing very meagre growth.

“On the other hand, Spain and Italy appear to be staging strong recoveries, benefitting in particular from impressive export performances. Such export gains point to improved competitiveness which bodes well for longer-term economic prospects. Manufacturers in France and Germany need to be mindful of such competition.”

Updated

In contrast with Italy and Spain manufacturing in Germany is struggling according to the Markit #PMI https://t.co/bhTDLcZcNE

— Shaun Richards (@notayesmansecon) June 1, 2015

Germany’s factory growth slowed last month, and by more than expected:

*GERMANY MAY MANUFACTURING PMI FALLS TO 51.1; PRELIM. 51.4

— World First (@World_First) June 1, 2015

France’s factory sector is still shrinking.

Markit’s French manufacturing PMI rose to 49.4, up from 48.0 in April -- the best reading in a year, but still below the 50-point mark showing no-change.

Italian factory PMI hits four-year high

Boom! Italy’s manufacturing sector has reported its biggest jump in output in four years.

Factories saw a sharp increase in output and new orders in May, leading to a rise in hiring. That pushed Markit’s Italy manufacturing PMI up to 54.8 from 53.8 in April -- which is the highest reading since April 2011.

Italy’s economy finally returned to growth in the last quarter, and the outlook looks quite bright:

Phil Smith, Economist at Markit which compiles the Italy Manufacturing PMI® survey, said:

“Italy’s manufacturing sector is enjoying its best quarter of expansion since 2011. Output growth has accelerated in every month this year so far, and a further strong increase in new orders suggests production is set to remain on an upward trend throughout the summer.

Dutch factories enjoyed a good May (like their counterparts in Spain) with the sector growing at its fastest rate since December 2013.

NEVI #Netherlands Mfg #PMI rises to 17-month of 55.5 (April: 54.2) high as Dutch mfg sector strengthens further http://t.co/6W2qrz90V6

— Markit Economics (@MarkitEconomics) June 1, 2015

The euro is weakening this morning, as concerns over Greece weigh on the market.

The single currency has dropped by 0.7% against the US dollar, from $1.0987 to $1.091.

That’s helping to push Europe’s stock markets higher this morning, as a weaker euro is good news for exporters.

Spanish factories post fastest growth since 2007

The recovery in Spain’s factory sector continued last month, with output growing at the fastest rate since April 2007.

Markit’s Spanish manufacturing PMI jumped to 55.8 in May from 54.2 in April, showing “a sharp improvement in business conditions”.

New orders and new exports both increase, encouraging firms to take on more staff – that’s welcome news for Spain’s army of unemployed.

Updated

Italy’s prime minister, the reformist Matteo Renzi, has been given a wake-up call by disgruntled voters.

Renzi’s centre-left Democratic party performed worse than expected in regional elections last weekend, as populist and anti-establishment parties enjoyed a rise in support. It lost the governorship of Liguria, which is usually a left-wing stronghold, and was pushed hard in other districts.

The Five Star Movement led by comedian Beppe Grillo performed well, picking up more than 20% of the vote in some areas.

Worryingly for Renzi (and pro-Europeans generally), is the strong showing recorded by the anti-euro, anti-immigrant Northern League.

Italian Government received a slap from the electorate as the Northern League and 5* movements did well.

— Steve Collins (@TradeDesk_Steve) June 1, 2015

One consolation for Renzi, though... at least he didn’t campaign for the wrong party....

Updated

China’s stock market has surged this morning, following the news that its factory sector had contracted for the third month running.

Traders piled into stocks in Shanghai, giving the main index its biggest one-day gain since January.

They reckon that the weak PMI report (details here) raises the chances that Beijing will announce new stimulus measures.

#China | *SHANGHAI COMPOSITE INDEX RISES 3.4%, BIGGEST GAIN SINCE JAN. 21 ...need worserer data pic.twitter.com/YIMZJyBFpE

— Ioan Smith (@moved_average) June 1, 2015

Updated

A top official at Germany’s Bundesbank has warned that Greek banks are on the brink of crisis.

Andreas Dombret, an executive board member of the German central bank, told Germany’s Bild newspaper that the Athens government must move swiftly to reach agreement with creditors:

“The Greek government would be well advised to act quickly - for the Greek banks, it is five minutes to midnight.”

“The situation in Greece is very critical and bank customers see that naturally...The direct dangers for European banks are relatively small.”

Last Friday we learned that Greece’s bank deposits had hit an 11-year low in April, as fears of default or capital controls spooked savers:

Bundesbank's Dombret says It’s Five to Midnight for Greek Banks in interview w/ @BILD as deposits drop like a stone. pic.twitter.com/rXHAoMAmYb

— Holger Zschaepitz (@Schuldensuehner) June 1, 2015

Tsipras blasts Greece's creditors over 'absurd' demands

Greece may have invented democracy, but it still has a bit to learn about diplomacy.

Last night, Greek prime minister Alexis Tsipras tore into the country’s creditors for making ‘absurd’ demands on Athens.

Writing in Le Monde, Tsipras insisted that the blame for the lack of progress since he took office in late January must lie on the institutions who oversee its bailout programmes.

He wrote:

“The lack of an agreement so far is not due to the supposed intransigent, uncompromising and incomprehensible Greek stance.

It is due to the insistence of certain institutional actors on submitting absurd proposals and displaying a total indifference to the recent democratic choice of the Greek people.”

And those counties who believe Greece must be put in her place risk:

....the beginning of the end for the European unification project by shifting the Eurozone from a monetary union to an exchange rate zone, [and] also triggers economic and political uncertainty, which is likely to entirely transform the economic and political balances throughout the West.

Europe, Tsipras concludes, is at “a crossroads”, and must choose between “solidarity, equality and democracy,” or “rupture and division?”

Here’s the full piece: Prime Minister Alexis Tsipras’ article in Le Monde newspaper: Europe at crossroads

The Financial Times reckons that Tsipras’s intervention has “increased the sense of chaos around negotiations in the week many believe a deal is needed to avoid a Greek default.”

#Greece's creditors long hoped @atsipras swoops into bailout talks to save deal. Not sure how he can after this op-ed http://t.co/KtChpba5xX

— Peter Spiegel (@SpiegelPeter) May 31, 2015

Perhaps the closest to a "this is it, take it or Grexit" public statement by Tsipras: http://t.co/RmXjUwILHH

— TRUMAN (@trumanfactor) May 31, 2015

The Agenda: Greek talks, manufacturing data

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

The clock is ticking louder for Greece, as Athens and its creditors continue to struggle to agree a deal before its bailout expires at the end of the month.

Hopes of a deal by Sunday have, alas, not materialised.

Instead, finance minister Yanis Varoufakis spent part of yesterday denying that he was about to resign. He’s under pressure from a group of 40-plus government MPs, who oppose his choice of economist Elena Panaritis as Greece’s new representative at the International Monetary Fund.

Rumours of my impending resignation are (for the umpteenth time) grossly premature...

— Yanis Varoufakis (@yanisvaroufakis) May 31, 2015

@nikimoza1 "In the long run we are all dead." J.M.Keynes. (In the medium run, those nostalgic of the troika days are stuck with me @ FinMin)

— Yanis Varoufakis (@yanisvaroufakis) May 31, 2015

More here: Yanis Varoufakis dismisses rumours he intends to resign as ‘grossly premature’

Also coming up....

There’s plenty of economic news around this morning, as Markit releases its estimates of growth across the global manufacturing sector.

We get Spain, Italy, France and Germany between 8am and 9am BST, followed by the UK at 9.30am.

Markit and HSBC have already reported that output across China’s small and medium-sized factories fell again last month, in the latest sign its economy is slowing. An official government report reckoned the overall sector grew slightly.

More here: China HSBC PMI contracts for third month in May

And we’ll keep an eye on the oil market. The OPEC cartel are due to meet on Friday, to vote whether to maintain production levels.

I’ll be tracking all the main events through the day....