If you’re just tuning in, here’s our full news story on today’s developments:

Updated

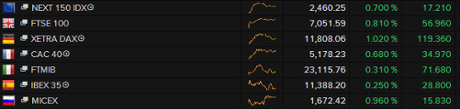

London's FTSE 100 index closed up 58 pts or 0.82% at 7,052.13 in a quiet day's trading. Tesco slipped 1.5% ahead of its results on Wed. #UK

— Andrew Duncan (@andrewsduncan1) April 20, 2015

Another sign of alarm; the spread between Greek bonds and safe-haven German debt is now at its highest in almost two and a half years:

#Greece 10-years yield #spread vs Bund climbs 39 bps to 1,283, highest since Dec. 7, 2012 pic.twitter.com/SIsHD7p8TL

— Advisory Desk (@advdesk) April 20, 2015

Today’s decree shows that Greece is now operating under extremely tight funding constraints, says CNBC:

As default fears grow, Greece moves to seize cash from public sector: http://t.co/tCwrATYomV pic.twitter.com/G0Mzzrp3d7

— CNBCWorld (@CNBCWorld) April 20, 2015

Greek tensions may build up through this week, ahead of Friday’s meeting of eurozone finance ministers, says Jasper Lawler of CMC Markets:

The unlikelihood of a deal being struck between Greece and its creditors has sent short-term Greek bond yields to new record highs again on Monday.

For now Greece’s troubles are contained within Greek markets but once the positive sentiment from Chinese stimulus has worn off, other European markets may follow suit closer to the Eurogroup meeting on Friday.

This cash call is the latest sign that Greece is running perilously low on funds, without any new bailout funds from its creditors.

It must pay 1.7bn euros of public sector wages and pensions at the end of this month, and 200m euros to the IMF at the start of May.

Economists had warned that reserves were very low. As Gabriel Sterne of the consultancy Oxford Economics put it to us:

“It is more of a question of what barrel they can still scrape to find some money to stave off default.”

Unless Greece and its lenders reach some deal soon, Athens may have to keep scraping.

Greece blames 'unforeseen circumstances'

Here’s Bloomberg’s early take:

The Greek government issued a decree that forces local governments to transfer all cash balances to the central bank, as a cash crunch worsens and debt to the International Monetary Fund comes due.

“Central government entities are obliged to deposit their cash reserves and transfer their term deposit funds to their accounts at the Bank of Greece,” the presidential decree issued Monday said on the government gazette website. The “regulation is submitted due to extremely urgent and unforeseen need

Some early reaction:

OH. #Greece government issues decree forcing local governments to transfer cash to central bank. “Extremely urgent & unforeseen need” cited.

— Maxime Sbaihi (@MxSba) April 20, 2015

#Grexit #Greece , decree forcing local governments to move cash to Central bank, these kind of moves raise more questions , death spiral ?

— Manus Cranny (@ManusCranny) April 20, 2015

Greece 'orders cash reserves transferred to central bank'

Heads-up: Greece’s government has just passed a decree to force local government authorities to place cash reserves at the central bank, according to local reports.

Legislative decree forcing general gov't bodies to deposit cash reserves with Bank of Greece published in Government Gazette #Greece

— MacroPolis (@MacroPolis_gr) April 20, 2015

The move shows Greece is taking steps to shore up its finances, to meet looming repayments.

.@kev_twine Gov't to use pension funds' assets to pay wages, pensions and the IMF. @Holbornlolz

— Yannis Koutsomitis (@YanniKouts) April 20, 2015

New data from the ECB shows that it continued to expand its balance sheet though its new QE programme last week (although the rate slowed slightly).

#ECB settles €73.29bn in Public-Sector Bond Buying as of Apr17 up from €61.68bn pic.twitter.com/PqJoe5erSQ

— Holger Zschaepitz (@Schuldensuehner) April 20, 2015

Wall Street has followed Europe’s lead, rising at the start of trading in New York:

Stocks open higher on China stimulus; Dow tops 150 points: http://t.co/pVNyODbQlL pic.twitter.com/BLBh0hP0Ss

— CNBC (@CNBC) April 20, 2015

In other news, the boss of Russia’s Gazprom is due to visit Athens tomorrow and meet with prime minister Alexis Tsipras.

Over the weekend, Russia denied reports that it would soon sign a gas pipeline deal with Greece which could potentially yield €5bn for the Greek government. So Alexei Miller’s “working visit” will be closely watched....

#Gazprom CEO to visit #Greece Tuesday http://t.co/wtSBLDogXf pic.twitter.com/5v9vCvH1st

— Sputnik (@SputnikInt) April 20, 2015

Summary: Pressure builds on Greece as time ticks down

Concern over Greece’s negotiations with its creditors continues to swirl through the eurozone today.

A series of top politicians and officials have urged Athens to speed up the pace, with fears that the country could default on a debt repayment soon unless

The IMF’s top man in Europe, Poul Thomsen, struck an optimistic note this morning, saying that talks over the weekend had made some progress.

There has been a little bit more impetus in the negotiations between the three institutions and the Greek government for several days.”

“That’s a good development and gives us reason to hope.”

But fears are growing that the crisis could escalate rapidly without serious progress.

Harris Georgiades also warned that a Grexit would be “unchartered water, for which no planning can be fully adequate”.

El-Erian sees little chance of a breakthrough this week, writing:

The realist would point out that there is a 90% chance that no decisive breakthrough is achieved, and that Greece and the euro zone experience an intensification of recurrent tensions and political stalemates, either immediately or down the road.

The euro has weakened this morning, dragged down by Greek fears.

And Greek bond yields have soared again, some hitting their highest levels since the crisis began:

More scary spikes from the market. HT @Investingcom #Greece pic.twitter.com/zJgn4uKUlF

— Derek Gatopoulos (@dgatopoulos) April 20, 2015

Analysts are also digesting the impact of Finland’s general election, and the prospect of the eurosceptic Finns party joining the government.

Open Europe’s Mats Persson reckons this could make a third Greek bailout politically trickier, but not impossible.

Ultimately, however, it’s unlikely that Finland will veto a third Greek bailout on its own accord (Finns MP may be given permission to abstain in any such vote, for example.) Helsinki will likely following Berlin’s line on the issue.

And back in Greece, the prosecution of the extremist Golden Dawn party was adjourned after just two hours today, with reports circulating that a witness had been attacked.

Here are some photos from the scene:

Interesting.... Bloomberg columnist David Powell suggests that Greece could struggle on until July 20 without a deal.

He’a arguing that the European Central Bank could still provide emergency funding, even if Greece failed to make scheduled repayments to the IMF in May and June:

The most important deadline for Greece is July 20. For details, see: {NI ECOCOM <GO>} on the BBG terminal. pic.twitter.com/PV65T0OWfb

— David Powell (@davidjpowell24) April 20, 2015

Is he right? Well, I’d hate to second-guess Mario Draghi on this issue. But it seems very likely that Greek savers would be spooked if an IMF payment was missed; so an intensified bank run could bring the crisis to a head quickly.

Royal Bank at Scotland’s economist team reckons Greeks will be heading back to the polls soon:

Greece to have fresh elections by June, "Grexit" still unlikely, says RBS.

— Jamie McGeever (@ReutersJamie) April 20, 2015

Reuters have now published the full quotes from Ewald Nowotny about how Greece’s exit from the eurozone would be less serious than in 2013:

“It (a Greek exit) does not have that impact or potential impact on the euro zone as it would have had ... some two years ago. I really don’t see a contagion in the financial and economic sense.”

Nowotny added, though that he could not predict the “psychological effect” of Grexit, and urged Athens to provide “numbers”, concluding

“Time is running out.”

Nowotny: Grexit is less of a threat today

Austria’s top central banker has just raised the stakes over Greece, by declaring that a Greek exit from the eurozone wouldn’t be as serious as in the past.

Interviewed by CNBC, Ewald Nowotny also warned that a deal this week is unlikely.

- ECB’S NOWOTNY SAYS WHEN ASKED ABOUT GREEK EXIT FROM EURO, IT WOULD NOT HAVE POTENTIAL IMPACT ON EURO ZONE AS IT WOULD HAVE TWO YEARS AGO- TV

- ECB’S NOWOTNY SAYS NUMBERS HAVE TO BE PROVIDED BY GREEK GOVERNMENT TO ESTABLISH NEW PROGRAMME - TV

- ECB’S NOWOTNY SAYS FEARS DEAL WILL NOT BE READY FOR EURO ZONE FINANCE MINISTERS MEETING THIS WEEK - TV

- ECB’S NOWOTNY SAYS EUROPEAN ECONOMY CLEARLY IMPROVING - TV

Bloomberg’s Hans Nichols says it’s a worrying sign:

When a central banker says, as Austrias Ewald Nowotny just did, that contagion from Greece will be *limited*, start looking for old drachmas

— HansNichols (@HansNichols) April 20, 2015

Updated

Euro hit by Greek worries

The euro is suffering from Greek uncertainty today. The single currency has fallen 0.7% against the US dollar today to $1.073.

It’s down 0.5% against sterling too, at 71.9p -- meaning one pound is now worth €1.391.

#Greece matters for the Euro: Common currency drops to $1.0730 as Greek 3yr yields jump. pic.twitter.com/4nl3kNJsTX

— Holger Zschaepitz (@Schuldensuehner) April 20, 2015

Ilya Spivak, Currency Strategist, at DailyFX, explains:

“The Euro has come back under pressure to start the week amid ominous comments about the festering crisis in Greece.

ECB policymaker Christian Noyer said the country may not find collateral for loans and warned that its exit from the Eurozone would be traumatic for the region as well as the world economy at large.” (see earlier post for details)

Greece’s three-year bond is now yielding almost 28% this morning, as its price falls further below its face value:

Greek 3yr yields jump by almost 100bps as #Greece and its creditors remained at loggerheads. http://t.co/rA4I0wBgre pic.twitter.com/CS1gLIAkyC

— Holger Zschaepitz (@Schuldensuehner) April 20, 2015

Here’s our Athens correspondent on today’s Golden Dawn trial:

The wheels of #greek justice disappoint again as #goldendawn trial takes farcical turn of being adjourned until May 7

— Helena Smith (@HelenaSmithGDN) April 20, 2015

#GoldenDawn court explains trial adjournment saying lawyer needs to be found for one of 69 accused - despite having had 18 months to do so

— Helena Smith (@HelenaSmithGDN) April 20, 2015

El-Erian: We could be facing a Graccident

The IMF may indeed be hopeful (see opening post). But there’s only a 10% chance of a significant breakthrough over Greece’s debts, according to Mohamed El-Erian, chief economic adviser at Allianz.

El-Erian reckons that both sides could hammer out a temporary deal that buys more time, but there’s as much risk of failure, possibly leading to a chaotic exit from the euro.

There is a 45 percent chance that a last minute messy compromise allows the muddling-through to continue; a 10 percent chance that a meaningful policy breakthrough will be achieved, and a 45 percent chance that the outcome is a Graccident in which both the Greek government and its European partners lose control of the situation.

Under this third scenario, a series of Greek payment defaults, bank runs and the imposition of capital controls would force Greece out of the single currency.

An optimist would espouse the 45 percent probability that a muddle-through compromise materializes at the 11th hour (or, to be more accurate, at 5 minutes to midnight). The realist would point out that there is a 90 percent chance that no decisive breakthrough is achieved, and that Greece and the euro zone experience an intensification of recurrent tensions and political stalemates, either immediately or down the road.

There’s still an opportunity for “visionary policy making” to end the crisis, but time is running out, El-Erian concludes.

.@elerianm on the 11 steps that could make a Grexit occur. http://t.co/qVXTFSHLVG

— Joseph Weisenthal (@TheStalwart) April 20, 2015

Updated

Greek Golden Dawn members appear in court

Over in Greece, the trial of scores of Golden Dawn party members began his morning, and was almost immediately adjourned until May 7.

Sixty nine members of the extreme right-wing Golden Dawn party faces charges of running a criminal organisation, following the death of left-wing rapper Pavlos Fyssas in September 2013.

Δικη χρυσής αυγής. Διακοπή για τις 7 Μαΐου! #GoldenDawn #jail pic.twitter.com/WyG0Stw9Ne

— Miltos Sakellaris (@MiltosSak) April 20, 2015

More than 40 of the defendants appeared in court today, but the trial was then adjourned for more than a fortnight, than amid reports that prosecution witnesses had been attacked.

Kathmerini newspaper reports:

Journalists were told that witnesses of Fyssas’s murder were attacked by Golden Dawn supporters as they arrived at Korydallos Prison.

Details of the alleged incident were not immediately available but the police was notified.

no, this doesn't bode well. https://t.co/iHjT7uhJqD

— Diane Shugart (@dianalizia) April 20, 2015

Fyssas, a well-known campaigner against fascism in Greece, died after being stabbed on September 18th 2013 in Athens.

Outrage over the killing prompted a crackdown against the party, which entered parliament on an anti-immigration platform.

There was tight security outside the specially built courtroom, where anti-racist groups and unions held a protest march.

Cyprus urges rapid progress to solve Greek crisis

Cyprus’s finance minister just urged the Greek government and its creditors to make progress “without delay”.

Speaking on Bloomberg TV, Harris Georgiades said Greece can avoid the banking crisis and capital controls that gripped Cyprus in 2013, if both sides act quickly.

I would hope Greece does not go through a similar situation…. it can definitely be avoided.

Greece has made some progress, Georgiades said, but now it must “specify and agree with the institutions on the details.... I hope that this happens soon”.

Georgiades hopes that progress is made in time for Friday’s eurogroup meeting, warning that:

“If we do not receive feedback on good progress... that will be negative.”

Georgiades also declines to say whether Cyprus has taken contingency planning for a Grexit, as ‘no planning’ could possibly be comprehensive enough.

Such an outcome would imply we are entering unchartered water, for which no planning can be fully adequate….. and that’s why I’m not even willing to speculate or discuss an outcome which the Greek government itself has ruled out.

#Cyprus' FinMin Georgiades in interview w/ Blooomberg TV: No planning could be adequate for any #Grexit.

— Holger Zschaepitz (@Schuldensuehner) April 20, 2015

Updated

Turning back to Finland’s general election quickly, and this chart shows how the next government will take control of a country in a significant economic hole:

Millionaire businessman wins #Finland, likely to need propping up by vehemently anti-EU group. http://t.co/e9OhbpzDzR pic.twitter.com/XqQc4Phf4Z

— Holger Zschaepitz (@Schuldensuehner) April 20, 2015

The demise of Nokia, the erosion of its lumber industry, and the economic problems of neighbouring Russia have all hurt Finland.

At the same time, pressure to keep to eurozone deficit targets forced the previous government into deep spending and welfare cuts.

The Greek bond selloff is intensifying, pushing yields higher into the danger zone.

Greece sweep - its deteriorating : 10-yr 13.09 +19bp 5-yr 19.195 +62½bp 3-yr 27.86½ +111½bp

— Steve Collins (@TradeDesk_Steve) April 20, 2015

Chinese stimulus gives European markets a boost

European investors are shrugging off the Greek crisis, pushing shares up in early trading.

The FTSE 100 is up almost 1%, led by mining stocks. That follows the China’s central bank’s decision to ease monetary policy last night.

The PBOC cut the amount of capital that commercial banks must hold, freeing up more money for lending, which could prevent the economy slowing [good news for the miners].

Curiously, Chinese stocks defied expectations and fell today; on fears of further measures to rein speculative trading.

Stan Shamu of IG reckons European investors may become less concerned with Greece as the rest of the region recovers:

With most of the region seeing signs of bottoming in data, I feel it’s not long before investors focus on the fundamentals and pay less attention to the Greece risk.

A depressing reminder of the social damage suffered since the financial crisis began:

Children living in jobless households in euro-area periphery countries doubled 2008-2013 http://t.co/UmmrX0IoJi pic.twitter.com/Ww1imAnnwJ

— Bruegel (@Bruegel_org) April 20, 2015

European commissioner Pierre Moscovici sounded like a man tapping his watch with increasing impatience this morning.

He told France’s iTele TV network that:

“We really need - now, there is no time to lose - that the Greek government delivers the reforms we’re asking for.”

Moscovici added that Plan A is for Greece to remain in the eurozone, and there is no Plan B. But there’s also no time for prevarication....

Greek bonds are weakening this morning, as fears of a default linger over the bond market.

This has pushed up the yield on its three, five and 10-year bonds:

GREEK YIELDS 10-yr 13.01 +11½ 5 - yr 18.70 +13 3-yr 26.97 +22

— Steve Collins (@TradeDesk_Steve) April 20, 2015

Yields rise when prices fall, and these figures suggest a high risk that investors won’t get all their money back.

Simon Nixon of the WSJ is always worth reading about Greece; today’s column warns that eurozone officials are preparing for a ‘messy’ default.

One option is that Greece fails to get a deal with its creditors (quite plausible), runs out of cash (ditto) and then defaults on a debt repayment payment. But that wouldn’t immediately trigger Grexit, as Simon explains:

How things play out after [a default] that will depend on who Greece decides to default on and the reaction of bank depositors. If Athens defaults on a government bond or loan, then the ECB will have to raise the price that banks pay to access emergency liquidity from the Bank of Greece, effectively depriving them of access to fresh supplies of euros.

If Athens decides instead to default to its own citizens, perhaps by issuing IOUs to pay pensions and salaries, bank customers may start emptying euros from their accounts. Again, banks would quickly run out of collateral for emergency liquidity.

In both cases, Athens would have to introduce capital controls and bank holidays to stop the financial system imploding.

Some officials believe Greece could carry on for several weeks if not months in this state of limbo while still technically remaining part of the eurozone....

That limbo could see the banks shut, capital controls imposed, and perhaps a new election?

Other governments, though, reckon the situation would deteriorate so quickly that Greece would be rapidly ejected from the eurozone....

If you haven't read about Greek crisis then you should start: this @Simon_Nixon is brilliant, clear and frightening http://t.co/W8RpdUhKkb

— Sam Coates Times (@SamCoatesTimes) April 20, 2015

Greek banks risk running out of the collateral they need to keep accessing emergency funding from the European Central Bank, the head of the Bank of France has warned.

Christian Noyer told Le Figaro that the lifeline being provided by the ECB couldn’t last forever:

“At some point, Greek banks are likely to be unable to offer enough collateral to access refinancing even for emergency liquidity.”

Noyer added that a Grexit would be traumatic for the whole eurozone, but particularly for Greece itself.

[by collateral, Noyer means the assets that Greek banks hand over as security in return for euros from the ECB, allowing them to keep running]

Finnish election adds new twist to eurozone crisis

There was drama in the north of the eurozone last night, as Finland eurosceptic Finns party surged to second place in the country’s general election.

The Finns secured 38 seats, while the opposition Centre party came first with 49.

This pushed prime minister Alexander Stubb’s centre-right National Coalition into third place, with 37 seats.

The Centre Party, led by telecoms millionaire Juha Sipilä, must now put together a coalition. And if he invites the Finns into office too, that could complicate the chances of agreeing a third bailout for Greece.

Timo Soini, leader of Finns, has already vowed to change’s Finland’s approach to Greece. saying:

I believe Finland’s policy towards Greece will change [if he joined the government]. It will change for the better, because it can’t get any worse”.

Finland’s economy has been struggling for several years, and now faces a bout of austerity; Sipilä had pledged a wage freeze and spending cuts to make it competitive again.

Final results in Finnish elections. Centre Party winners. €sceptic Finns Party beats expectations w/ 2nd most seats pic.twitter.com/2PYSntFImH

— Open Europe (@OpenEurope) April 20, 2015

Here’s your regular reminder of the debt repayments and wage bills that Greece faces:

Barclays: Repayment timeline and other key events for Greece pic.twitter.com/EV6VmQPKrU

— Fabrizio Goria (@FGoria) April 16, 2015

Note that Greece owes €780m to the IMF on May 12, the day after the Eurogroup meeting that is now the crunch deadline for a deal.

Updated

Many investors are doubtful that Greece will reach a deal with its creditors in time to avoid a default.

With hopes of a deal at this Friday’s Eurogroup meeting now pretty much sunk, City experts are speculating about how much cash the country can find.

My colleague Katie Allen has been speaking to the experts, and reports:

“Although time is running short, there are clear indications that the Eurogroup meeting in Riga on 24 April might not bring a breakthrough,” said Reinhard Cluse, an economist at the bank UBS.

“In the absence of a deal in the next few weeks, the government might not be able to avoid default, which – we fear – would likely raise the risk of ‘Grexit’ [a Greek exit].”

Greece faces a series of repayments and interest payments on its debts in the coming weeks as well as its usual pensions and public-sector salary obligations. Experts say money is running out.

“As to how much funds they have left to pay back maturing debt, it is almost zero,” said Gabriel Sterne at the consultancy Oxford Economics. “It is more of a question of what barrel they can still scrape to find some money to stave off default.”

Introduction: IMF hopeful as Greek crisis rumbles on

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

It looks like another strained weak for the eurozone, as negotiations over Greece’s bailout drag on.

Greek officials spent last weekend in talks with its creditors, in an attempt to reach agreement on economic reforms to unlock some aid.

IMF chief Poul Thomsen, director of the IMF’s European Department, has declared that the talks have now picked up pace, but still have a long way to go.

Thomsen says (via Germany’s Handelsblatt newspaper):

“There has been a little bit more impetus in the negotiations between the three institutions and the Greek government for several days.”

“That’s a good development and gives us reason to hope.”

Thomsen cautioned, though, that the two sides are still “far from the target”.

"Talks with Greece have gained momentum but still long way from target - IMF" - http://t.co/9NVu6ry2WG pic.twitter.com/ATyohwQ2R0

— Valerio Nicolardi (@ValerioNicolard) April 20, 2015

Over the weekend, ECB chief Mario Draghi and US Treasury Secretary both warned that the situation now was now “urgent”. As Draghi put it:

“We all want Greece to succeed. The answer is in the hands of the Greek government.”

ECB’s Draghi Says Urgent That Greece Strikes Deal With Creditors http://t.co/BdnWV54zxE via @business

— Rebecca Christie (@rebeccawire) April 18, 2015

But despite rising pressure last week, Greece’s government insists – in public at least – that it will not roll over. Deputy PM Yiannis Dragasakis said yesterday that Athen would not “budge from our red lines.”

That suggests no agreement is close on issues like pension reform, labour market liberalization, VAT hikes and privatizations.

Dragasakis also floated the suggestion of “snap elections or a referendum” if a deal isn’t reached.

We’re rattling towards Friday’s meeting of eurozone finance chiefs, but the new ‘finally final’ deadline appears to be the next full Eurogroup meeting on May 11.

If Greece and its creditors haven’t hammered out a deal by then, the situation could turn quite messy.

I’ll be tracking all the main developments through the day....

Updated