Closing summary: Waiting for a breakthrough....

It’s late in London, and inching towards bedtime in Greece, so here’s a quick recap.

Greece has submitted its most comprehensive reform plan yet to its creditors, but has yet to unlock any bailout funds.

Athens proposed a 26-page list of reforms today, from tax evasion measures to a new bad bank to help clean out its financial system. It warned that action was ‘urgently needed’, to preserve the viability of the eurozone.

The plan was discussed by eurozone deputy finance ministers this afternoon (these charts outline the main measures)

Greek sources say there was progress, while eurozone insiders say the call was simply to ‘take stock’.

But hopes are fading for a breakthrough next week, with officials in Brussels and Athens both suggesting that finance chiefs might not meet until 24 April.

And in the last few minutes, the ECB has apparently extended Greece a little more liquidity assistance to help its banks stay afloat.

For more details of the day, including some protests in Greece, check out the lunchtime summary:

Thanks, and goodnight. GW

ECB gives Greek banks more emergency liquidity

Some late breaking news....the European Central Bank has agreed to raise the emergency liquidity on offer to Greek banks by another €700m.

That’s quite a small increase, suggesting the ECB is keeping the pressure on Greece to reach a deal.

ECB increased ELA limit for Greek banks by €700 mln to €71.8 bln. #Greece #economy #ECB #ELA #banking #markets

— MacroPolis (@MacroPolis_gr) April 1, 2015

Greece’s government has also proposed setting up a ‘bad bank’ to handle the bad loans that are clogging up its financial system.

It warns that there are “Critical Deficiencies” in the banking sector today, in today’s 26-page list of reforms:

The Greek banking sector has been marred by clientelism, by too close a link with the mass media and the political systems (through the provision of loans on non banking principles) and, lastly, by lending practices that were either too tight or too loose. The economic crisis has in addition created a vast amount of NPLs [non-performing loans] that impedes credit creation.

And here’s the proposed reform strategy:

Broad and deep structural reforms aimed at ensuring financial stability, appropriate credit expansion and governance that constitutes a significant departure from suspect practices of the recent and not too recent past. The Greek government has planned a broad reform programme in order to address critical deficiencies of the banking sector, through the establishment of strong institutions and the introduction of solid processes for the functional supervision of the banks that ensure financial stability, a robust banking sector and banks that are run on sound 8 commercial banking principles.

Dealing with the very high levels of NPLs is a top priority for consolidating the banks and restarting the economy. The government wishes to explore the possibility, in conjunction with the institutions, of a capital asset management company to be created towards dealing with NPLs utilizing the remaining buffer of the HFSF.

(that’s the Hellenic Financial Stability Fund)

Greece’s government is proposing to raise the minimum wage...however, it also predicts that the fiscal impact in 2015 and 2016 will be “negligible”

The reforms plan states:

Proposed reforms will be introduced in stages: unifying the minimum wages of “white” and “blue collar” workers, abolishing wage differentiation based on age, and gradually increasing the minimum wage after consultations with the social partners.

The section on Greek privatizations begins with a pop at the failure of the past:

The initial goal for revenues from privatizations was €50 billion between 2011 and 2016, with a €5 billion target for 2011, €10 billion for 2012 and €5 billion for 2013. In practice, proceeds from privatizations amounted to €1.6 billion in 2011, no revenues in 2012 and €1 billion in 2013. Seldom has a privatization program failed so spectacularly!

The new government is proposing to consider future privatizations on a “case-by-case basis”.

Existing contracts “will be honoured”, but Greece will also use all legal powers to guarantee an equity stake in privatised firms, and protection for workers. But will that be enough to placate critics in the Syriza party?

Greece's reform plan, some highlights

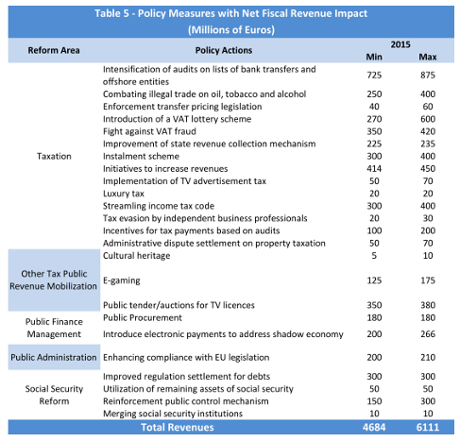

Greece’s list of economic reforms contains some firm pledges to crack down on tax evasion.

The first item is called “Intensification of audits on lists of bank transfers and offshore entities”, and is said to raise €725-€875 million in 2015. €1 billion from 2016 onwards.

It also includes plans for a “VAT lottery scheme”, where consumers who pay the sales tax can enter a prize draw.

A “Wealth database-registry” to prevent rich Greeks hiding their assets is planned.

And the Finance Ministry is also proposing to stop tax evasion by self-employed people through “a point of sale electronic application that will record every incoming customer and transfer real-time notifications to the authorities”.

Agence France-Presse have also heard that eurozone finance chiefs aren’t likely to told another meeting about Greece soon.

This suggests that Greece’s reform plan, although more comprehensive than before, hasn’t persuaded creditors to release bailout funds:

[Today’s conference call] was just to take stock. There won’t be any developments in coming days,” a source close to the discussions told AFP.

“We will continue with technical work in Athens. There is no Eurogroup meeting in sight.”

Greece: still no deal after eurozone teleconf, no Eurogroup meeting in sight, sources tell AFP http://t.co/3C4XI1mI52

— Danny Kemp (@dannyctkemp) April 1, 2015

Greek officials: April will be the busiest month

Over in Athens officials are denying that today’s teleconference with with the euro working group went badly.

But they are also saying April is likely to be a month packed with negotiations ... suggesting that a reform-for-cash deal is unlikely to be found at least until the next scheduled euro group of euro area finance ministers on April 24.

Helena Smith reports:

Government sources are saying another Euro working group will be held next Wednesday - traditionally regarded as the Holy Week by Greek Orthodox faithful who will celebrate Easter a week later than the Catholic communion on April 12.

“Today’s teleconference took place in an unexpectedly good climate even if there was no decision to dispense [bailout] funds,” one official said:

“There is a growing sense of convergence even if the talks are difficult.”

Auditors were pouring over the Greek government’s proposed reforms in minute detail, they said, adding that “the whole of April” was likely to be taken up with negotiations.

Greece’s government has also argued that its reform programme could deliver a chunky primary surplus.

Open Europe flags up the details:

Greek reform list says impact of reform programme could lead to 2015 primary surplus of up to 3.9% of GDP. #Greece pic.twitter.com/cW1NcABSq9

— Open Europe (@OpenEurope) April 1, 2015

Updated

So, how much progress was made on today’s eurozone conference call?

One eurozone official has told Reuters that there is been “progress and convergence”, but there is still “quite some work that needs to be done” to reach a successful conclusion.

So, we’re not there yet.

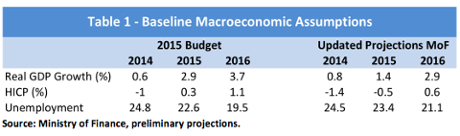

Greece has also warned that growth in 2015 and 2016 will be weaker than previously expected, confirming that its economy has deteriorated in recent months.

The Ministry of Finance now only expects growth of 1.4% this year, down from 2.9% estimated in the 2015 budget, rising to 2.9% in 2016 (down from 3.7%).

Unemployment is also expected to be higher than planned, this year and next year.

Here’s the chart from today’s report:

Greece also expects to only post a primary surplus of just 1.2% of GDP for 2015, down from an original forecast of 3%.

Greece: Viability of the euro is in question

Greece has also warned its creditors that the “viability” of the EU, and the single currency, is at stake.

The introduction of the 26-page list of reforms presented today states that:

The Hellenic Republic considers itself to be a proud and indefeasible member of the European Union and an irrevocable member of the Eurozone. Yet the viability of that Union, and especially of the common currency, is now in question, in the minds of many Greek citizens as it is in the minds of many among our European partners.

The question before us all, as Europeans, is whether the European Union can rise to the challenge before it. It is necessary now, without further delay to turn a corner on the mistakes of the past and to forge a new relationship between member states, a relationship based on solidarity, resolve, mutual respect and a new hope for common progress.

To that end, it is now urgent that the books be closed on the past programme with the rapid conclusion of the Final Review, so that Greece and her partners can proceed to negotiate and to launch a new partnership and a new model for development and growth in Greece.

'Viability of Union, and especially of the common currency, is now in question,' warns new Greek eurozone document

— Bruno Waterfield (@BrunoBrussels) April 1, 2015

Updated

Greece's reform plan: the key charts

The reforms plan submitted by Greece today could raise between €4.6bn and €6bn of revenue (according to Athens’ calculations, anyway).

Here’s the details:

It also includes around €1.5bn in privatisation revenue (as Helena reported earlier).

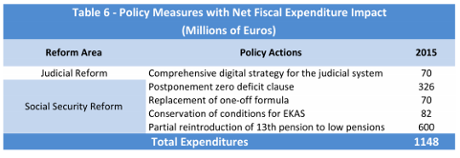

But the plan also includes new expenditure, including €600m to raise pensions (as demanded by protesters today).

Updated

FT: Here's the list of Greece's new reforms

Peter Spiegel of the Financial Times has obtained the list of reforms which Greece has proposed to its creditors today.

It’s 26 pages long, covering taxation, privatisations, Greece’s public sector, its labour market and healthcare, among others.

The Greek goverment says it is a “comprehensive list” of policy reforms, meeting its commitments to its creditors and to the Greek people, and urged its lenders to respond quickly, and positively.

The government requests a speedy and successful conclusion of the Final Review on the basis of this list, so that shortterm funding issues may be resolved and the current crippling economic and financial uncertainties brought to an end. This is an urgent and necessary precondition for the success of the economic and reform program.

But Peter, having perused it, reckons it may not go far enough.

Financial Times: Greece submits new list of reforms to eurozone

He writes:

The new reform measures are similar to Friday’s initial effort and fail to address several issues that bailout monitors have insisted on, including an overhaul of the Greek pension system and further labour market liberalisation.

Indeed, the proposal appears to reverse past reforms in several of these areas. The document includes €1.1bn in new spending this year, more than half of it reinstating a so-called “13th pension” — an extra months’ pay — for low-income pensioners. The document suggests that change would add €600m this year.

It also would suspend a so-called “zero deficit clause” that would force further cuts to state pensions; the measure would add another €326m this year.

And while the document includes five separate measures under the heading “labour market reforms”, they include a gradual increase in the minimum wage and strengthening collective bargaining — both measures that would effectively undo reforms adopted earlier in the rescue programme.

Still, the document includes several concessions to eurozone authorities, particularly in the area of privatisations. Some government ministers from the far left of the governing Syriza party have publicly stated that all privatisation of state assets would come to an end.

Peter has also kindly uploaded the whole document, here:

More to follow....

With delicious timing, the European Central Bank has just advertised for a Greek translator....

Hmmm RT @ecb: Job alert: Greek Translator (traineeship) – Communications http://t.co/rtzT1aaRry

— Matthew C. Klein (@M_C_Klein) April 1, 2015

Greece submits new reforms to creditors

The Greek government has provided further details of its reform plans to lenders today, in an attempt to unlock bailout funds.

Helena Smith reports that:

Greek officials say in addition to €3.7bn worth of fiscal measures the left-led government is proposing, privatisations worth €1.5 bn in 2015 have also been outlined in the package the finance ministry has drafted.

The operation and management of 14 regional airports (concessions long sought after by Germany) has been included in the privatisations.

Reuters is also reporting that Greece fleshed out its propose reforms, but the two sides are still divided over pensions and labour reform.

* Greek Fin Min official says toughest issues in talks with lenders are labour and pension reforms - RTRS

— Fabrizio Goria (@FGoria) April 1, 2015

Updated

Greek insiders angry about bailout talks

Over in Athens, officials say a campaign of rumour, innuendo and deliberate leaks is being waged against the new government.

Helena Smith, our correspondent, reports:

Greek officials are finding it increasingly hard to hide their exasperation with tactics they say are deliberately aimed at undermining Athens’ new leftist-led government. “A campaign of rumour, innuendo and deliberate leaks is being waged against us,” said one well-placed source.

“They keep saying ‘the Greeks are not well prepared, they haven’t done their homework, their proposals are vague’; all of which are grotesque and preposterous lies.

The Greek side has never been as well prepared and the issue really is not whether they agree with our figures but whether they want an agreement.”

Today’s suggestions that Greece was about to withhold the €450m payment to the IMF on April 9 was part and parcel of the campaign, insiders feel [even though the quotes did actually come from a Greek minister....GW]

“What we are seeing is an intent to stall the situation so that there is an accident in our banking system and liquidity becomes so constrained we are unable to pay an installment or one of the banks is forced to shut down,” another official said.

“The banking system is at risk, outflows are growing, non-performing loans are mounting. What they are doing is criminal. The February 20th agreement was supposed to give us four months of financial stability and instead they are using it to asphyxiate us.”

Today’s euro working group meeting was important, Greek officials said, because it would signal whether creditors were prepared to be conciliatory. Thomas Wieser, an Austrian who presides over the group, is believed to be more aligned to the school of hardliners lead by Germany finance minister Wolfgang Schauble.

Our official adds:

“The Euro working group prepares the ground for the euro group so if anything it would be surprising if there were a breakthrough....It seems they want to push us to the brink of Grexit, squeeze us to our last drop of blood and breath in the hope that they can get just a little bit more out of us.”

Greece’s strength lay in its proposals – a 52 page document that the government was prepared to disclose if necessary. The anti-austerity coalition was sticking to its guns and refusing to reduce pensions, make cuts or forge ahead with mass lay-offs.

Tensions remain high, judging by this final quote:

“From the start we made that clear. The whole aim is to defeat this government. If they see us retreating they will wipe us out. From time of the Roman legions that is how the Germans have worked. We are not going to do them the favour.”

HS

Heads-up: Eurozone deputy finance ministers have just ended their conference call about Greece.

Euronews’s Efi Koutsokosta reports that the Greek finance minister was also on the call:

#euroworkinggroup where @yanisvaroufakis also participated finished.

— EfiKoutsokosta (@Efkouts) April 1, 2015

The Greek stock market has fallen again today, as the uncertainty and occasional eyebrow-raising headlines jangled nerves.

The main ATG index fell 1.3% by the close of trading.

The very fact that Greece could threaten to withhold its IMF repayment shows the need for a proper process to handle debt defaults.

So argues Eric LeCompte, Executive Director of the religious debt relief organization Jubilee USA Network.

LeCompte writes:

”We’re watching a poker match between Greece, the IMF and the European Union. The stakes couldn’t be higher with the lives of millions of ordinary people on the line.

“This is more proof that we need a global bankruptcy process with rules that are above board. We can’t be playing poker with people’s lives.”

And just in case any Greek ministers are reading, and considering leaving the IMF empty-handed next Thursday, here’s what would happen next:

Greece, here's what the IMF will do if you don't repay its loans on time. h/t @IanTalley: pic.twitter.com/9ZVQeuIkkp”

— Marcus Walker (@MMQWalker) April 1, 2015

Greek government bonds have weakened today, pushing up the yields on its short and long-term debt.

Over in the City, Steve Collins has kindly tweeted the details:

Greek sweep : 10-yr 11.81½ +18½ 5-yr 17.10½ +18 3-yr 23.31½ +69 Not the highest we have seen, but market taking today's rumours negatively

— Steve Collins (@TradeDesk_Steve) April 1, 2015

Greek gov't celebrates April Fool's Day in excellence.

— Yannis Koutsomitis (@YanniKouts) April 1, 2015

Greek government denies planning to withhold IMF payment

The Athens government has moved swiftly to deny that it won’t meet its €450m repayment to the IMF next week unless its gets a bailout payment quickly.

A government spokesman has denied Spiegel’s story, and insisted that it still hopes for a ‘positive’ outcomes to the current situation.

Reuters has the details:

- GREEK GOVT SPOKESMAN DENIES PLAN TO DELAY PAYMENT TO IMF ON APRIL 9 UNLESS IT GETS FUNDS FROM LENDERS

- GREEK GOVT SPOKESMAN SAYS GOVERNMENT TO CONTINUE SPECIFYING REFORMS, HOPES FOR POSITIVE OUTCOME AT A EUROGROUP MEETING

Greek journalist Efi Efthimiou also has the denial:

#Greece sources tell @capitalgr that Voutsis comments re IMF payment not new,were similar 2 what was mentioned in the Tsipras letter 2Merkel

— Efthimia Efthimiou (@EfiEfthimiou) April 1, 2015

Updated

That Spiegel story suggesting Greece might not repay the IMF next week has sent ripples through the financial markets.

Nikos Voutzis’s comments have left traders edgy that the Greek crisis may be flaring up again....

Greece choosing not pay IMF loan on April 9 without backstop is more "Lehman Brothers" than "AIG" - let's hope it doesn't get there.

— Christopher Vecchio (@CVecchioFX) April 1, 2015

Market wobbling on this headline: *GREECE DOESN'T WANT TO RESPECT IMF APRIL 9 DEADLINE: SPIEGEL

— Steve Collins (@TradeDesk_Steve) April 1, 2015

Updated

Spiegel: Greece may not repay IMF next week

The crisis just took another twist. Germany’s Spiegel news magazine is reporting that Greece might not meet the €450m loan repayment due to the IMF next week.

Greek Interior Minister Nikos Voutzis has apparently told the paper that, without fresh bailout aid, Athens would be forced to miss this payment.

Voutzis also warned that Greece only has enough money to last until mid-April, and would prioritise public sector wages and pensions if its creditors fail to release some of the €7.2bn aid currently being withheld.

The story is online here (in German). Reuters has snapped the key points:

- GREEK INTERIOR MINSTER TELLS GERMANY’S SPIEGEL ONLINE IF INTERNATIONAL CREDITORS SEND NO FURTHER FUNDS TO ATHENS BY APRIL 9, GREECE WON’T REPAY IMF ON TIME

- GREEK INTERIOR MINSTER TELLS GERMANY’S SPIEGEL ONLINE WE SHOULD AGREE TO POSTPONE REPAYMENT TO AVOID DEFAULTING ON DEBT

- GREEK INTERIOR MINSTER TELLS GERMANY’S SPIEGEL ONLINE WE HAVE SUFFICIENT MONEY UNTIL MID APRIL

No April fool's day joke: #Greece doesn’t respect #IMF Apr9 deadline (when Greece is due to repay €460mln), BBG reports citing Spiegel.

— Holger Zschaepitz (@Schuldensuehner) April 1, 2015

Being late with an IMF repayment isn’t unprecedented -- Sudan, Zimbabwe and Somalia have all missed payments. But it would be a major event, raising a lot of concern over Greece’s ability to meet other obligations and sending Grexit fears soaring.,

It could also potentially trigger ‘cross-default’ clauses in other Greek bonds, if Greece doesn’t meet the payment within a month.

The Open Europe thinktank have just released a good analysis on the issue. Here’s a flavour:

One of the biggest problems for Greece is that it is still working with the Fund and relies on its sign off (as part of the ‘institutions’) to get its current review completed and therefore funding released. The response of the fund on the ground will therefore be important. Of course, the fund finds itself in a bit of a circular position. It is unlikely to get paid if it does not approve Greece’s review, but how can it approve the review if it is not getting paid?....

Gap with creditors grows, reputation harmed: Linked to the above, given that not paying the IMF is usually a course of action reserved only for war torn countries or those on the fringes of the international system, not to mention severly underdeveloped economies, Greece could see its reputation severely dented. Furthermore, it is possible that Greece’s creditors will see that Greece has decided to pay wages and pensions first rather than meet its commitments to them. Whether or not this is a fair assessment, this could drive further animosity between the two sides.

So what happens if #Greece fails to pay the IMF on time? Time to read our blog post from this morning: http://t.co/RYrzXAN18I

— Open Europe (@OpenEurope) April 1, 2015

Updated

Summary: At least they're still talking...

A brief recap:

Eurozone deputy finance ministers will hold a conference call shortly to discuss the state of play around Greece’s reform plan.

Germany’s finance ministry has already predicted that the call won’t yield much, though. Despite five days of talks in Brussels (which ended yesterday), we still don’t have a list of solid reforms that could persuade creditors to hand over bailout cash.

Officially, Greece’s government remains upbeat. Economy Minister George Stathakis set the scene this morning by telling Skai TV that the two sides will agree a package of reforms next week. He said:

“The agreement will close on (Greek Orthodox) Easter week.

But the word from Brussels is that a deal is still far away, with eurozone finance ministers not expected to meet until late April.

And the uncertainty is weighing on Greek bonds, pushing up its borrowing costs while other eurozone members benefit from lower yields:

Greek negotiations are widening the spread between its yields and the rest of the periphery http://t.co/M2PU92yRim pic.twitter.com/zWU9HbmrZG

— fastFT (@fastFT) April 1, 2015

Greek pensioners have rallied in Athens, urging the government to reverse cuts to pensions and healthcare. Photos here.

And a group of protesters have been arrested after invading the courtyard of the Greek parliament, in a show of solidarity with anarchists and hunger striking prisoners.

The latest economic data has shown that the political uncertainty gripping Greece is hurting its economy. Factory output fell in March for the third month running, with export orders weakening.

The rest of the eurozone did better, though, with manufacturing growing at its fastest rate in 10 months.

Britain’s factories also posted solid growth last month,. but this has been overshadowed by confirmation that UK productivity is stuck in its worst rut since 1948.

Updated

We’ve not seen so much of Yanis Varoufakis, recently -- hopefully he’s been hard at work writing that economic reform plan.

But Greece’s finance minister has just appeared on Twitter, to plug a ‘witty’ joke about Greece moving to Bitcoin.

Happy April Fool's Day everyone... http://t.co/HELEDGDpOk

— Yanis Varoufakis (@yanisvaroufakis) April 1, 2015

No worse than Yanis’s idea of turning tourists into undercover tax snoopers, I guess.

Incidentally, it’s not been a great April Fool’s Day for the European Central Bank’s media chief, Michael Steen. Germany’s FAZ newspaper told its readers we could all dine at the ECB’s new restaurant. For reservations, phone Michael! (no don’t, he’s had a bad morning)

Yeah @FAZ I was nearly chuckling until I realised you printed my phone number and my phone is now unusable. pic.twitter.com/t7ohYQ35HP

— Michael Steen (@michaelsteen) April 1, 2015

In grand scheme of things of course, this might be one of the more accurate FAZ stories about the ECB. (Spoiler: there is no restaurant.)

— Michael Steen (@michaelsteen) April 1, 2015

Updated

Interesting....

#Greece Gov't to present new fiscal measures at #Eurogroup Working Group's teleconference call this pm, @euro2day_gr reports

— Yannis Koutsomitis (@YanniKouts) April 1, 2015

Updated

Germany: Hard to predict how Greek situation will develop

Germany’s finance ministry has confirmed that eurozone deputy finance ministers will hold a conference call this afternoon, to discuss the state of play around Greece.

But it has also dampened hopes that this call would take the eurozone closer to an agreement over Greece’s reform plans.

Spokesman Martin Jaeger told reporters in Berlin that he only has “modest” expectations for the call.

“In the best case scenario we expect there could be some kind of preliminary interim review but it’s hard to predict how things will develop next week.”

That’s notably gloomier than the Greek side, who remain upbeat despite the lack of progress. Remember, economy minister George Stathakis said this morning that:

“The agreement will close on (Greek Orthodox) Easter week.”

Last week, I rather expected that we’d soon see another late-night crunch session in Brussels to debate Greece’s finances.

But this (obviously) hasn’t happened yet. And as long as we don’t have an agreement between Greece and her creditors over a reform package, it’s not going to happen.

The FT’s Peter Spiegel is hearing that the next meeting of eurozone finance ministers might not take place for another three weeks....

More I talk to people here, the more saying no #Eurogroup before regularly-scheduled meet Apr 24 in Riga. No sign of #Greece deal in sight

— Peter Spiegel (@SpiegelPeter) April 1, 2015

Journalist Loukia Gyftopoulou has more details about those protests, and arrests, in the Greek parliament courtroom this afternoon:

Anarchist invasion in Parliament will be a real test for gov after #Syriza promised absence of police in dems. So far 15 detained #Greece

— Loukia Gyftopoulou (@loukia_g) April 1, 2015

Protesters demand abolition of anti-terror laws, prisoners' release and closure of maximum security prisons #Greece

— Loukia Gyftopoulou (@loukia_g) April 1, 2015

Greek police have now swept into the parliament courtyard to break up the protests:

Greek police make arrests follwing invasion of parliament courtyard - VIDEO - http://t.co/MZaPieO5oq pic.twitter.com/oo43MPvkn2

— enikos_en (@enikos_en) April 1, 2015

It’s all looking rather lively in Greece today.

A group of protesters are now demonstrating on the courtyard of the Greek parliament, as part of a solidarity campaign with prisoners conducting a hunger strike.

Solidarity action at the Greek parliament #now by anarchists #hungerstrike2015 p/v @kinimatini #antireport pic.twitter.com/sjLvz1kkHw

— Souidos (@Souidos) April 1, 2015

Group of anarchists invade Greek Parliament courtyard - http://t.co/hZjiawBtcs pic.twitter.com/5ZiWtmzGcM

— enikos_en (@enikos_en) April 1, 2015

They are calling for members of an anarchist group to be released from custody, and for Greece’s maximum-security prisons to be closed. Earlier this week they invaded Athens University.

Greece’s parliamentary speaker, Zoe Konstantopoulou, is apparently taking developments in her stride.

Speaker GR Parl Konstantopoulou's first comment on the anarchists' break-in was "you got jumpy bc some people protested?" via @g_evgenidis

— The Greek Analyst (@GreekAnalyst) April 1, 2015

German economist Holder Schmieding blames the new Greek government for the downturn in its economic fortunes this year:

Berenberg Bank's Holder Schmieding on #Greece: "Rarely has a new government caused so much economic damage in such a short time."

— Michael McKee (@mckonomy) April 1, 2015

Pensioners hold anti-austerity rally in Athens

Over in Athens, pensioners have held an anti-austerity rally to demand pensions and healthcare benefits to be increased.

The Kathimerini newspaper explains:

The elderly, who have faced several pension reductions since 2010, also demanded immediate subsidy of their pension funds and measures to restore damage caused by the 2012 haircut (PSI).

The protest comes as eurozone officials prepare to hold their teleconference call to discuss the progress (or lack of it) towards an agreement on Greece’s economic reforms.

Russia faces a lengthy recession, as the sanctions imposed over Ukraine weaken an economy already suffering from lower oil prices.

That’s according to the World Bank, which has just slashed its forecasts for the Russian economy. It now predicts that GDP will shrink by 3.8% in 2015, and another 0.3% in 2016.

In December, it expected a mere 0.7% contraction this year, and growth of 0.3% next year.

World Bank - says GDP in Russia to fall around -3.8% in 2015 assuming $53 oil

— Steve Collins (@TradeDesk_Steve) April 1, 2015

Ireland’s economy continues to bounce back from the lows plumbed during the financial crisis, when its banking collapse triggered a eurozone bailout and years of austerity.

Data just released show that Ireland’s unemployment rate has fallen to 10%, from 10.1%. The number of people claiming unemployment benefit fell by 4,700 to 350,600, down from 450,000 five years ago.

And in a further piece of good news, Ireland’s central bank has hiked its growth forecast for this year and 2016.

#ireland Central Bank’s 2015 GDP Forecast Revised To +3.8% Vs +3.7%, 2016 Revised To +3.7% Vs 3.8% /via @livesquawk #euro

— Yannis Koutsomitis (@YanniKouts) April 1, 2015

Most European stock markets have defied expectations and rallied this morning, reversing yesterday’s slide.

The news that eurozone factory growth strengthened last month helped to send shares up in Paris, Frankfurt, Milan and Rome.

And in London, the FTSE 100 has jumped by 67 points, or 1%, led by financial stocks - as Nick Fletcher reports here.

Greece stock market, though, has been hit by the failure (so far) to reach a package of reforms with creditors. The ATG index has shed 1.2% this morning.

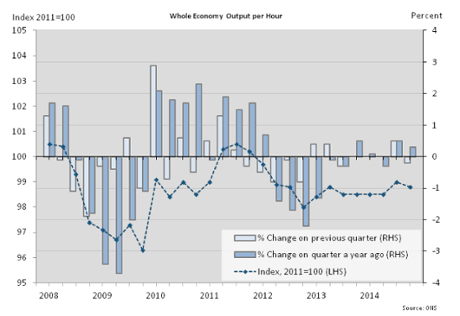

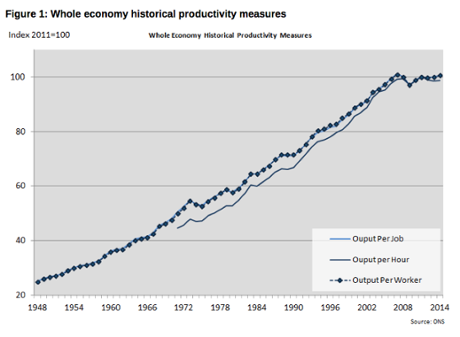

Howard Archer, economist at IHS Global Insight, is also disappointed that Britain’s labour productivity fell back in the fourth quarter of 2014.

He writes:

Productivity currently remains limited compared to pre-crisis levels and the latest relapse will fuel concern that much of this has to do with structural factors. How productivity develops going forward will be a critical factor in how soon and how far the Bank of England raises interest rates.

If productivity has taken a significant lasting hit, it means that the economy has less potential to grow without generating inflationary pressures and that interest rates will need to rise at an earlier stage.

Back to Greece......and eurocrisis expert Yannis Koutsomitis is tweeting some interesting developments around its funding needs:

#Greece Public Debt Agency head Papadopoulos to meet with @PIMCO execs today over next week's T-bill auction ~@EFSYNTAKTON

— Yannis Koutsomitis (@YanniKouts) April 1, 2015

(T-bills are short-term government debt, which Greece has been issuing to keep itself afloat)

#Greece | General Accounting Office notifies Gov't cash runs out May 15 http://t.co/OhDhBjiNGn /via @EFSYNTAKTON

— Yannis Koutsomitis (@YanniKouts) April 1, 2015

As we covered early this morning, Greek ministers are predicting a deal next week on economic reforms, that would unlock some aid from its creditors.

Without a deal, Greece will struggle to meet an €450m IMF payment a week tomorrow, and then must pay workers salaries and pensions at the start of May.

Updated

Vicky Redwood, UK economist at Capital Economics, is concerned that Britain’s productivity fell by another 0.2% in the last quarter:

“This still isn’t great - productivity has still not even returned to its long-run average rate of about 2%, let alone recouped any of the shortfall relative to its pre-crisis trend.”

Britain’s persistently weak productivity gives another insight into the true state of the UK economy, as politicians trade blows ahead of May’s election.

Today’s ONS report shows that David Cameron has presided over an economy with the weakest productivity record of any government since the second world war, says economics editor Larry Elliott.

If the UK economy was truly strengthening, surely labour force productivity would be increasing as firms invested in new equipment and pioneered better ways of working?

We're no more productive (q4 2014) than we were in 2007 (ONS): "the absence of productivity growth...is unprecedented in the post-war period

— Andrew Verity (@andyverity) April 1, 2015

If reducing corporation tax increases wages and investment, then why have real wages and productivity been taking a hammering?

— Simon Parker (@SimonFParker) April 1, 2015

Britain's "unprecedented" weak productivity run continues

Despite the recovery, Britain’s economy still suffers from weak productivity.

Data just released by the Office for National Statistics shows that labour force productivity fell by 0.2% in the last three months of 2014.

In simple terms, that means British employees actually generated slightly less economic activity for each hour they spent at work during the last three months of 2014.

The ONS says there was no improvement in productivity last year, and that the economy is still less productive than before the financial crisis.

It says:

The absence of productivity growth in the seven years since 2007 is unprecedented in the post-war period.

7 lean years of no productivity growth... Time for a biblical analogy?

— Duncan Weldon (@DuncanWeldon) April 1, 2015

Updated

Eight-month high for UK manufacturing purchasing managers' index counters some of those slowdown fears: http://t.co/16fY2GkFMk

— David Smith (@dsmitheconomics) April 1, 2015

March was a good month for UK factories too -- the sector grew at its fastest rate in eight months.

The UK manufacturing PMI rose to 54.4 in March, up from 54.0 in February, thanks to strong domestic demand. Export orders picked up too, as the “bright start to the year” continues.

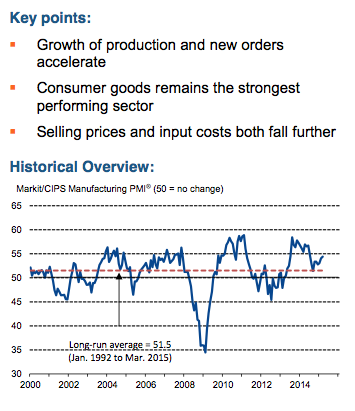

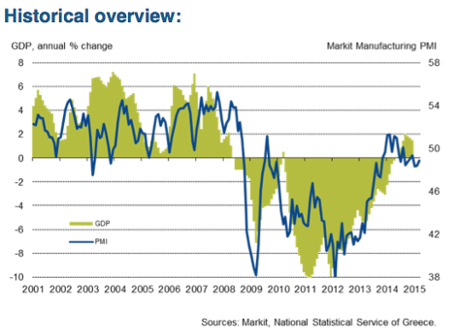

Political uncertainty hits Greek factories

Greece is not sharing in this revival in the eurozone economy -- its factory sector contracted again last month.

Greece’s manufacturers reported a third straight monthly drop in output in March, confirming that economic conditions have deteriorated since the country’s political upheaval began.

Firms reported another drop in new orders, particularly from abroad, suggesting uncertainty over its bailout programme has hit confidence.

This pushed the Greek factory PMI, measuring activity across the sector, below the 50-point mark separating expansion from contraction for the seventh month running.

Markit explains:

Weighing on overall inflows of new business was a sharp and accelerated decrease in new export orders, which panel members linked in part to foreign clients being deterred by political uncertainty in Greece.

Economist Phil Smith warned that Greece’s recovery “looks to be on hold for now.”

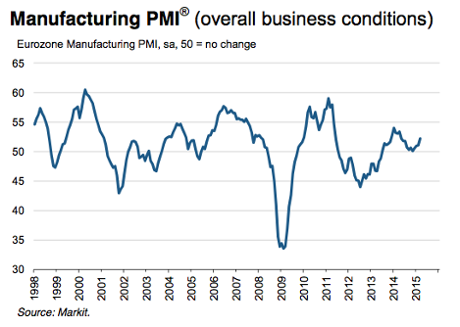

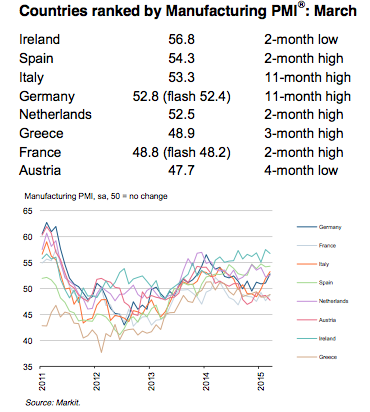

Eurozone factory growth hits 10-month high

The eurozone’s economic recovery has strengthened, as manufacturing activity across the region grew at the fastest pace since last May.

Growth accelerated in Germany, Spain, Italy and the Netherlands, as the European Central Bank’s quantitative easing programme stimulates demand and drives down the euro.

Markit’s manufacturing PMI, just released, hit a 10-month high of 52.2 -- higher than that 51.9 estimated two weeks ago. And as already flagged up this morning, many firms reported they took on more staff to handle increased demand.

Chris Williamson, Chief Economist at Markit, says the eurozone economy is reviving, but there are black spots.

“Producers are benefitting from the weaker euro, which has had the dual effect of boosting competitiveness in export markets as well as making competing imports more expensive in the home markets.

“New orders are consequently showing the best growth for nearly a year, and the fact that manufacturers are boosting their payroll numbers at the fastest rate for three-and-a half years indicates optimism that the upturn will be sustained in coming months.

“Rising demand is also helping firms and their suppliers to re-establish some pricing power. Factory input prices rose for the first time in seven months and selling prices were broadly stable, providing encouraging news that deflationary forces are easing.

“This is still a fledgling recovery, however, and the overall rate of expansion remains only modest. Importantly, manufacturing is still in decline in France, Greece and Austria, acting as drags on the region’s revival.”

Those French and German PMIs are both higher than the ‘flash’ readings two weeks ago, suggesting that conditions improved during March.

Upward revisions to final PMIs (Germany/France) suggest positive momentum continued in the past 10 days or so. #QEuphoria #QEboost

— Frederik Ducrozet (@fwred) April 1, 2015

Here comes Germany’s manufacturing PMI...

...and it’s another month of solid growth for factories in Europe’s largest economy.

The German manufacturing PMI rose to 52.8 in March, up from 51.1, which shows tht faster growth in eleven months.

France’s factory sector has shrunk again, but at least the pace of decline has slowed.

The French manufacturing PMI came in at 48.8 for March, up from 47.6 in February -- but still below the 50-point mark that splits expansion and contraction.

France Manufacturing #PMI rises to 48.8 but still signals deteriorating business conditions http://t.co/bJEqHa6k3W http://t.co/6u8ZIS0WFp

— Markit Economics (@MarkitEconomics) April 1, 2015

Finally some good economic news for #Italy As its manufacturing #PMI rises to 53.3 http://t.co/4I79ddcDIF #ECB #QE #Euro

— Shaun Richards (@notayesmansecon) April 1, 2015

Good news from Italy too -- factory output has hit an 11-month high last month.

Data firm Markit reports that the Italian manufacturing PMI jumped to 53.3, from 51.9, showing that the sector expanded. Growth is “gathering momentum”, it says, with firms hiring staff at the fastest rate since February 2011.

Here’s the key points:

Spanish factory recovery accelerates

Spain’s economic recovery continues to pick up pace, as the weaker euro gives Spanish firms a boost.

The Spanish PMI jumped to 54.3 from 54.2, which is another month of solid growth.

Crucially, firms hired staff at the fastest rate since June 2007.

And many reported that new business from abroad was boosted by the relative weakness of the euro, particularly against the US dollar.

Andrew Harker, senior economist at Markit and author of the report, says the trend of “consistently solid growth” continued last month:

The highlight from the latest survey was the strongest rise in employment since mid-2007, as the labour market continues to recover.

Meanwhile, the sharp reductions in input prices seen in the first two months of the year were not repeated at the end of Q1 as the weakness of the euro led to rises in the cost of imported items.”

Turkey’s factory sector has contracted at the fastest rate in almost six years.

Output, new orders, and new export orders all declined, adding to concerns that its economy is slowing down. Firms reported “generally weak domestic and international market conditions”.

Yesterday’s mysterious power cut, which left half the country without energy, won’t have helped -- many factories in the western city of Izmit weren’t able to work, for example.

Turkish manufacturing downturn intensifies in March, #PMI at 48.0 (49.6 in Feb), lowest since April 2009 http://t.co/TZAzecfbof

— Markit Economics (@MarkitEconomics) April 1, 2015

Russia’s factory sector continued to contract last month.

HSBC’s Russia Manufacturing PMI, measures activity in the sector, fell to 48.1 from 49.7. Any reading below 50 shows a drop in activity.

The sanctions imposed on Russia over the Ukraine conflict may be biting, along with the impact of the lower oil price. Many firms reporting that conditions have deteriorated.

Paul Smith, Senior Economist at Markit, warned that some companies are struggling to get financing too:

“March’s survey data indicated that operating conditions remained challenging overall, with output, new orders and employment all posting modest falls. Access to working capital also remains a hurdle to overcome for a number of manufacturers.”

Updated

Overnight, an official survey of the Chinese factory sector was a little stronger than expected in March, driving the Shanghai stock market to a new seven-year high.

The official Chinese manufacturing PMI rose to 50.1 from 49.9, showing very marginal growth. But a rival survey was less optimistic, showing a drop in employment and new orders.

More stimulus may still be needed to stop the country’s economy slowing. More here.

Overnight data from China - especially HSBC manufacturing survey - point to a further slowdown in growth.

— Duncan Weldon (@DuncanWeldon) April 1, 2015

Updated

Greek minister: Deal before Orthodox Easter

With a deal before Western Easter looking very unlikely, Greece’s government has now declared that it will reach agreement with its lenders before Orthodox Easter (which falls on 12 April).

Economy Minister George Stathakis has just told Skai TV that the two sides will agree a package of reforms next week, saying:

“The agreement will close on (Greek Orthodox) Easter week.”

For that to happen, the Greek side will have to produce a credible, detailed programme of reforms. Some officials in Brussels have warned that the current plan is still too much of a ‘wish list’.

And next week looks rather lively; with the IMF expecting a €450m repayment from Greece on Thursday, April 9th.

Stathakis also tried to placate critics in his own party, who oppose selling off state assets. He said the government still plans to hold a stake in the country’s largest port, Piraeus, rather than selling the whole thing.

“The idea that prevailed is that we will not proceed with a privatisation of the 67 percent stake, which would mean a full privatisation of Piraeus port. We are not discussing this.”

“We are trying to find some kind of joint venture.”

(quotes via Reuters)

The agenda: Greek teleconference call, and euro PMIs

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

With Greece’s negotiations with its creditors over economic reforms seemingly becalmed, eurozone finance officials will hold a teleconference call today to assess the state of play.

The euro working group will discuss the chances of a deal, following five days of talks in Brussels which ended yesterday.

Although the Athens side are making positive noises, there’s no indication yet that we’re close to a breakthrough that would release the bailout funds it desperately needs.

No wonder Angela Merkel and Francois Hollande were chivvying Greece to speed things up, at a press conference on Tuesday.

Billionaire investor Warren Buffett waded into the issue last night, telling CNBC that

“If it turns out the Greeks leave, that may not be a bad thing for the euro.

“If everybody learns that the rules mean something and if they come to general agreement about fiscal policy among members, or something of the sort, that they mean business, that could be a good thing.”

The European Central Bank is also expected to ponder the Greek crisis today, to decide whether to continue providing emergency liquidity to the Greek banking sector.

That support is effectively keeping Greek banks alive, as worried savers continue to withdraw funds

The lack of progress in Greece is weighing on Europe’s stock markets; they’re expected to fall again today, adding to yesterday’s tumble.

#FTSE expected to open around 20 points lower. European stock index futures down on #Greece bailout uncertainty

— David Morrison (@jmoz62) April 1, 2015

And there’s also lots of economic data due this morning, with Markit releasing its Purchasing Managers Index surveys of Europe’s manufacturing sectors. The PMIs are likely to show that eurozone factories continued to grow, but that France lagged behind again.

Eu #daybook: manufacturing PMI data; ECB policy makers are said to be holding weekly review of Emergency Liquidity Assistance to Greece Wed.

— Francine Lacqua (@flacqua) April 1, 2015

We’ll be tracking all the main events through the day...

{kind=link}