Over in Greece, government officials have announced they are in constant touch with auditors representing the country’s troika of creditors and are working on “further clarifications” in a bid to break the deadlock in negotiations between the two sides. Helena Smith reports from Athens

Emerging from an impromptu meeting of senior officials with prime minister Antonis Samaras, the Greek finance minister Gilkas Hardouvelis said while a planned teleconference call with creditors had been aborted, the government was now working on fine-tuning proposals it had already put forward to the troika.

“We are in constant touch with the troika,” he told reporters. High-level finance ministry officials were cited as saying that an email containing clarifications would be sent to the EU, ECB and IMF by Thursday -widely seen as the cut-off day if the deadline of completing talks by December 8 is to be met.

Mission chiefs have sought further clarification on what is felt to be Athens’ overly ambitious tax raising targets and measures the government has lined up in the event of revenues falling short.

Insiders said the focus of the email would be next year’s projected fiscal shortfall, at the crux of much of the disagreement between the two sides.

From Brussels, Greece’s deputy prime minister Evangelos Venizelos conceded that the negotiations – the last before EU aid disbursements expire on December 31 – were proving to be very hard. “I want to send a very simple but clear message to Greek citizens but also our European partners. These negotiations are very difficult because they concern the future of the country and the future of our relations with our partners. They requires calm and decisiveness,” he said.

The socialist leader also delivered a stark warning to lenders saying that the austerity-whipped nation could take no more. “We will arrive at a solution … as long as our partners understand – which they ought to understand – and they will understand, that Greece has exhausted its possibilities. 2015 is not 2010.”

Aiming his sights at the country’s radical left main opposition Syriza party he added: “So the important thing is that in these critical days we are focused on our goal which is a national [goal]. There is no room for any petty party approach to these matters.”

On that note, it’s time to close up for the evening. Thanks for all your comments, and we’ll be back tomorrow for, among other things, the latest Bank of England and ECB meetings.

Updated

The US Federal Reserve’s policy of keeping interest rates close to zero is risky, and waiting too long to raise rates means they may have to increase more quickly when the time comes.

These are comments from Philadelphia Fed president Charles Plosser made in a speech to the Charlotte Economics Club. He said inflation was heading towards the Fed’s goal and the US economy was approaching full employment. He said:

Waiting too long to begin the process of raising the policy rate risks facing the possibility that the rate may have to increase rapidly when the time comes and that could prove unnecessarily disruptive. And waiting could also risk a more rapid pickup in inflation.

He also called for more transparency from the Fed’s Open Market Committee:

Policy can also be made more transparent and effective by specifying more completely the variables that guide policy and the general way that one can expect policymakers to react to those variables. To this end, I believe the FOMC should move forward to describe in a qualitative way its reaction function and then communicate our actions and decisions in terms of this reaction function.

The full speech is here:

A Longer-Term View of the U.S. Economy and Monetary Policy

Mixed performance from European markets

Weak service sector surveys in the eurozone added fuel to the idea that the European Central Bank will sanction more measures to boost the economy when it meets on Thursday. Hopes that president Mario Draghi would pave the way for the purchase of sovereign bonds pushed yields lower and equities higher. In the UK, the main event was the autumn statement, with banking shares slipping lower after the chancellor blocked them from offsetting losses from the financial crisis against tax on future profits. An exception was Royal Bank of Scotland, which after a volatile time, ended the day higher. Airline shares welcomed the news that air travel taxes would be scrapped for children, while housebuilders benefited from a cut in stamp duty. However Foxtons, which specialises in expensive housing in London and the south east, fell back as buyers of higher prices properties would have to pay more tax. Overall, the final scores showed:

- The FTSE 100 finished 25.47 points or 0.38% lower at 6716.63

- Germany’s Dax added 0.38% to 9971.79

- France’s Cac edged up 0.08% to 4391.86

- Italy’s FTSE MIB rose 1% to 19,978.32

- Spain’s Ibex ended 1.18% better at 10,875.9

On Wall Street the Dow Jones Industrial Average is currently 12 points or 0.07% higher.

#Sweden PM Stefan Lövfen to call a new election on March 22 after budget is voted down.

— Philip O'Connor (@philipoconnor) December 3, 2014

Over in Sweden it looks like the government’s budget has been defeated, a move which could lead to a new election.

Here’s a report from Sweden’s The Local:

Sweden’s coalition government has failed to get its budget through parliament amid a political crisis that could see the fall of the government or even fresh elections, just three months after voters last went to the polls.

Social Democrat Prime Minister Stefan Löfven was pushing for increased spending on welfare and jobs and pledged to maintain Sweden’s liberal immigration laws in his budget.

But he failed to get enough support for the financial package.

This was because the nationalist Sweden Democrats - who hold the balance of power in parliament - chose to support a rival budget from Sweden’s centre-right opposition parties.

Full report here:

Crisis in Sweden as coalition budget fails

Swedish Parliament has voted down govt's budget - the country now faces biggest government crisis since the 1950s. PM could resign today

— Mats Persson (@matsJpersson) December 3, 2014

US crude oil stocks fell by more than expected last week, showing a drop of 3.7m barrels compared to forecasts of a 1.3m barrel increase.

Both Brent and the US WTI index have edged lower on the news albeit they are both still up on the day.

#WTI's negative reaction could be because of the fact that gasoline & distillate stocks both increased sharply last week ^FR

— FOREX.com (@FOREXcom) December 3, 2014

On the ISM services sector report, James Knightley at ING Bank said the report was positive apart from the employment figure, which could mean that Friday’s non-farm payroll number disappoints. He said:

The ISM non-manufacturing index has risen to 59.3 in November, up from 57.1 in October and better than the 57.5 consensus forecast. Business activity has risen to 64.4 from 60.0, which is phenomenally strong and has only been bettered a handful of times in the life time of the series back to 1997. New orders also rose and now stand at 61.4 versus the 50 break-even level while the backlog of orders is also growing, as are export orders. This is really encouraging and with the manufacturing survey also at lofty levels it suggests that the US economy will really drive the global growth story in 2015.

The one disappointment is the employment component, which slipped to 56.7 from 59.6. This follows a slight dip in the ADP employment number earlier today and a pick-up in jobless claims in recent weeks.

This all points to the risk of a data disappointment in Friday’s labour report. Currently, the consensus estimate is for a monthly increase of 230,000, but we expect 215,000 with probable downside risk. Nonetheless, we don’t think it is the start of a weaker trend. Weather may be a factor in the short term, but in the longer term the strength of the economy gives us confidence that the labour market will perform robustly through 2015.

On Wall Street, the Dow Jones Industrial Average has edged up around 5 points following the figures.

And (almost inevitably) the ISM services sector report paints a different picture to the earlier Markit report.

The Institute for Supply Management’s services index rose by more than expected in November to 59.3 from 57.1 in the previous month, and better than forecasts of 57.5.

Two of the elements of the survey - employment and imports - fell compared to October but were still above the 50 level which indicates expansion.

Baffle with BS: ISM Service beats 59.3, Exp. 57.5, 15 minutes after Markit Service PMI missed

— zerohedge (@zerohedge) December 3, 2014

The first of two surveys of the US services sector is out, and it shows the pace of growth was at its lowest level since April.

The Markit services sector purchasing managers index slipped to 56.2 in November from 57.1 in October, and marginally less than an initial estimate earlier in the month of 56.3. The forecast was for 56.5. Markit chief economist Chris Williamson said:

The slowing is still only modest, and leaves the economy growing at its approximate long-term trend rate. The survey data remain consistent with another month of non-farm payrolls rising by at least 200,000 in November.

The non-farms are out on Friday, but more immediately, the ISM non-manufacturing composite index will be released imminently.

Updated

Here’s an interesting Financial Times profile of Russia’s central bank governor Elvira Nabiullina, who is described as having one of the most difficult jobs in world finance. Hard to argue with that assessment, given that raising interest rates and floating the rouble has done little to stop the currency’s decline, hit as it is by factors outside the bank’s control, such as plunging oil prices and the western sanctions on Russia.

The profile is here (£):

The woman trying to tame the rouble

US jobs data below forecasts

Ahead of Friday’s US non-farm payroll numbers, the latest ADP report on private payrolls is out and looks disappointing. Here are Reuters’ snaps:

- 03-Dec-2014 13:15 - ADP NATIONAL EMPLOYMENT REPORT SHOWS U.S. EMPLOYMENT INCREASED BY 208,000 PRIVATE SECTOR JOBS IN NOVEMBER

- 03-Dec-2014 13:15 - REUTERS CONSENSUS FORECAST FOR ADP PAYROLL CHANGE FOR NOV WAS FOR INCREASE OF 221,000 JOBS

- 03-Dec-2014 13:15 - US ADP OCTOBER PAYROLL CHANGE REVISED TO +233,000 FROM +230,000

Updated

As George Osborne speaks, here’s a comment on his earlier decision to redeem the 3.5% War Loan from Fidelity, the largest single holder of the bond. Ian Spreadbury, Portfolio Manager of Fidelity MoneyBuilder Income and Fidelity Strategic Bond funds, said:

Today’s announcement is clearly good news for holders of the Fidelity MoneyBuilder Income, Fidelity Strategic Bond and Fidelity Extra Income funds.

We have been happy holders of the War Loan for some period of time on the basis of two reasons. Firstly, the bond has generated attractive income compared to much lower yielding long maturity gilts. And secondly, there has also been the potential for price appreciation if the government called the instrument, as the bond has been trading below par. Obviously, we are pleased with how this has played out.

It had been something of a double-edged sword for the government – if yields drop further from here they could have refinanced it at a much lower level, so they’re giving up that option. But with yields close to all time lows, I suppose it is important for them to lock in the benefit now.

The biggest challenge for investors now is what to do with the proceeds. I have recycled the proceeds back into long-dated gilts, but to achieve a yield equivalent to War Loan before the announcement you have to look at single-A rated corporate bonds. Fortunately, there are opportunities to switch into bonds in that area still offering an attractive yield for the small amount of credit risk. But I caution investors not to extend risk too far down the credit spectrum in their search for yield at this point in the credit cycle.

A reminder:

We are live blogging the chancellor’s autumn statement here.

Updated

The cost of insuring Ukraine’s debt has jumped to a five and a half year high after the government confirmed an accident at its Zaporizhzhya nuclear power plant.

Markit said Ukraine’s five year credit default swaps had opened at 1824 basis points but fell to 1775 after the news, even though the government said the incident was a minor one.

Italian 10 year bond yields have fallen below 2% for the first time, with the market expecting the European Central Bank to hint at more stimulus measures and bond buying at its meeting on Thursday.

The weak eurozone service sector data earlier has also helped to send most bond yields lower.

Some UK corporate news and Richard Glynn, the embattled chief executive of Ladbrokes, is to step down from the bookmaker after five years in charge. My colleague Simon Goodley reports:

The move, which had long been predicted in the City, came as Ladbrokes tried to claim that Glynn had completed a five-year turnaround of the business, despite the company’s shares being 24% lower than when he started in the job. During that time, shares in rival William Hill have risen by 60%.

In a statement Ladbrokes admitted that Glynn’s “recovery programme has taken longer to deliver than initially anticipated” but insisted that it believes that the changes made are now “deeply embedded in the organisation and that increasing attention should now be focused on delivering sustainable growth from a much stronger operational and digital platform”.

Chairman Peter Erskine, who personally picked Glynn, added: “I would like to thank Richard for his leadership of the company and his considerable achievements in delivering a new digital future for Ladbrokes. He has devoted enormous energy and dedication to securing the transformation of the company and the benefits of that work are beginning to be seen. I am pleased that he will both see through the final steps of the implementation plan and be on hand to facilitate an orderly succession process. Ladbrokes has been transformed and is a far stronger company as a result of his work”.

Full story here:

Ladbrokes chief to step down after five-year term

More from Reuters on the Ukrainian power plant situation:

Ukraine’s Energy Minister Volodymyr Demchyshyn said on Wednesday an accident at the Zaporizhzhya nuclear power plant in southeast Ukraine posed no danger and that the plant would return to running as normal on December 5.

“There is no threat ... there are no problems with the reactors,” Demchyshyn said at briefing, saying the accident affected the power output system and “in no way” was linked to power production itself.

In Vienna, the International Atomic Energy Agency said it had no immediate comment on the report. Under an international convention, adopted after the 1986 Chernobyl accident in what was then Soviet Ukraine, a country should notify the IAEA of any nuclear accident that can impact other countries.

Updated

Over in Greece, and the troika of international lenders want more information on proposed pension reforms, newspaper Kathimerini is reporting:

Greece’s international lenders have asked for more information on pension reform to plug a potential budget gap next year, a government official said on Wednesday, as the two sides continue to haggle in a bailout review.

Athens has offered to raise value-added tax on hotels and implement pension reform to satisfy European Union/International Monetary Fund lenders’ concerns of a potential budget shortfall next year.

The aim is to get a deal by a December 8 deadline that would, in turn, allow Greece to exit its bailout program by the end of the year.

Government spokeswoman Sofia Voultepsi confirmed that Greece received a response from lenders early on Wednesday. She did not give further details and it was not immediately clear whether the two sides were closer to reaching a deal.

A labor ministry official said the lenders had sought more information on pension reform proposed by the government.

The lenders did not specify any date for returning to Athens to complete the review, Adonis Georgiadis, an official from Prime Minister Antonis Samaras’s conservative party told Greek television.

Samaras has staked his government’s political survival on exiting the deeply reviled EU/IMF bailout by the end of the year, but his plans have been held up by deadlocked talks on the review.

The lenders have demanded additional measures to make up for an expected budget shortfall next year but Samaras on Tuesday said the government refused to hike taxes and cut incomes, arguing it would hurt a nascent economic recovery.

Updated

Here’s Reuters first take on the Ukraine situation:

Ukrainian Prime Minister Arseny Yatseniuk said on Wednesday an accident had occurred at the Zaporizhye nuclear power plant (NPP) in south-east Ukraine and called on the energy minister to hold a news conference.

“I know that an accident has occurred at the Zaporizhye NPP,” Yatseniuk said, asking new energy minister Volodymyr Demchyshyn to make clear when the problem would be resolved and what steps would be taken to restore normal power supply across Ukraine.

News agency Interfax Ukraine said the problem had occurred at bloc No 3 - a 1,000-megawatt reactor - and the resulting lack of output had worsened the power crisis in the country. Interfax added that the bloc was expected to come back on stream on Dec. 5.

The Ukraine energy minister seems to be playing down the problems at one of its nuclear plants:

UKRAINE ENERGY MINISTER: NUCLEAR PLANT WORKING BELOW CAPACITY; INSIGNIFICANT DAMAGE IN ACCIDENT

— Russian Market (@russian_market) December 3, 2014

Ukrainian Energy Minister: Says There Is No Threat To Reactor Following ‘Accident,’ Damage Was Insignificant

— Live Squawk (@livesquawk) December 3, 2014

Updated

Reports are coming in of a possible accident at a nuclear power plant in Ukraine, as revealed by the country’s prime minister Arseny Yatseniuk:

#Ukraine's Yatseniuk discloses accident at nuclear power plant in SE of country. Instructs new energy min to call news conference.

— Reuters UK (@reuters_co_uk) December 3, 2014

UKRAINE BONDS DECLINE AS PREMIER REPORTS NUCLEAR PLANT ACCIDENT

— MineForNothing (@minefornothing) December 3, 2014

YATSENYUK SAYS ACCIDENT HAPPENED AT ZAPOROZHYE NUCLEAR PLANT IN UKRAINE pic.twitter.com/NrFpUowZNg

— Russian Market (@russian_market) December 3, 2014

not clear that this Ukraine nuclear plant incident is really an accident - shutdown yes but maybe more technical issues

— Tony Tassell (@TonyTassell) December 3, 2014

Updated

Elsewhere, Russia’s central bank is intervening in the currency market again to defend the rouble, according to Reuters. It reports:

“Without doubt, the central bank is selling (foreign currency). The whole question is what volumes it is limiting itself too,” said a trader at a large Western bank in Moscow.

Earlier on Wednesday the central bank said it had made $700m in market interventions on Monday, its first interventions since November 10, the day before it floated the rouble.

Back to the news that the Treasury will pay off the first world war bond.

Toby Nangle at Threadneedle, which is one of the two biggest holders of the debt, has been lobbying the Debt Management Office to pay it off. Reacting to the news, he said:

We are really pleased to hear Chancellor Osborne announcing today that the War Loan is being refinanced. We estimate that refinancing this bond will deliver around £15m of interest savings per annum, comparable to a debt reduction of over £500m.

We engaged with officials at the UK Debt Management Office outlining our assessment of the benefits of calling of the War Loan. We are delighted that on reflection they arrived at the same conclusion.

The Treasury’s move to refinance government debt at lower yields in a market friendly manner echoes similar moves conducted by previous chancellors, notably George Goschen in 1888, albeit on a smaller scale.

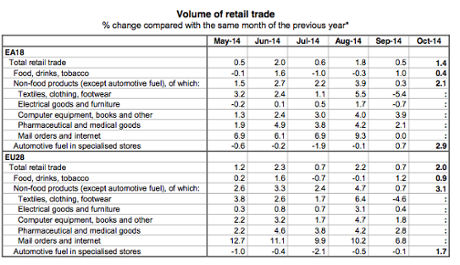

Eurozone retail sales disappoint

More data from Europe, and eurozone retail sales returned to growth in October but fell short of expectations.

After a weak third quarter, sales rose 0.4% month on month for a 1.4% year on year gain. This follows a fall of 1.2% month on month in September but was below forecasts of 0.6% growth.

Sales of non-food products and fuel at petrol stations were the biggest contributors to the rise, with sales of food, drink and tobacco flat in the month, according to Eurostat.

Euro zone retail sales also miss forecasts, printing +0.4% month-over-month versus +0.6% expected and -1.3% last #FX ^FR

— FOREX.com (@FOREXcom) December 3, 2014

Updated

Speaking of the autumn statement, my colleagues Andrew Sparrow and Graeme Wearden are live blogging the chancellor’s speech and all the reaction here:

Autumn statement 2014: George Osborne to miss deficit targets - live

More comment on the UK services figures.

James Knightley at ING Bank said:

The UK service sector purchasing managers’ index offers more encouragement on fourth quarter GDP growth. The headline index has risen to 58.6 from 56.2 and with the manufacturing index also having risen on Monday (while the construction index fell yesterday) it leaves the composite PMI at 57.6 versus 55.8 previously – the consensus forecast was for a reading of 56.2.

In terms of the services survey, there were strong gains in new orders, which points to decent output growth in the first quarter of 2015, while the employment index rose further. Inflation pressures remain very subdued though, suggesting little imminent pressure for Bank of England policy action. [Reminder: both the Bank of England and ECB are meeting on Thursday].

Indeed, there is a growing prospect of a sub-1% inflation reading in January given the plunge in motor fuel costs and the ongoing supermarket price-war.

The survey compiler suggests that these figures are roughly consistent with GDP growth of 0.6% quarter on quarter. We are more optimistic in terms of fourth quarter GDP, pencilling 0.8% quarter of quarter, on the basis of a strengthening household sector and a rebound in investment.

Nicholas Ebisch, currency analyst for Caxton FX, said:

Services PMI data this morning solidly beat expectations with a reading of 58.6, when a reading of 56.6 was previously forecast. The pound has rallied slightly against the dollar and strongly against the euro this morning as eurozone PMI data earlier today was disappointing and triggered euro weakness across the board. This latest PMI reading bodes well for sterling, but the broader market reaction seems a bit more muted than it would usually be, as market participants are likely to be waiting for the autumn statement this afternoon before making their final decisions.

Updated

I’m now handing over to my colleague Nick Fletcher.

Here is some instant reaction to the UK services numbers. Alan Clark at Scotia Bank said:

The CIPS Services survey was much higher than expected last month, rebounding to 58.6 from 56.2 - regaining pretty much all of the ground that it lost the prior month.

Combined with the manufacturing index that gives a composite reading of 57.0 - consistent with ongoing above trend GDP. That is hardly a reading that suggests rate hikes would be a killer blow to the economy.

While I accept that headline inflation is slowing due to energy and food prices, these have the same impact as a tax cut which is good for growth and supportive for core inflation.

I’m not turning all hawkish on you, but my point is that data like these suggest to me that waiting at least another year before we dare risk raising interest rates is a little excessive.

Maybe we are looking at this the wrong way and the Maradona Theory is working to the max. More specifically, earlier in the year the market fully priced 25bp per quarter of rate hikes through to end 2015. That probably dampened sentiment. Right now the market is pricing virtually no tightening until late next year, and sentiment is rebounding.

Surely there must be some middle ground? (for what its worth we are still calling mid-2015 for the first hike).

Markit said:

Supporting the latest increase in activity was another rise in new business volumes. Panellists commented that demand was high, and they had been able to secure contracts from both new and existing clients. Advertising and marketing drives provided further support to sales efforts, and overall new business growth strengthened since October with over 28% of panellists recording a rise in new work.

UK service growth stronger than expected

UK’s services sector is stonking ahead: Growth was stronger than expected last month. The PMI headline index climbed to 58.6 from 56.2 in October, pointing “to a marked and accelerated rate of expansion that was well above the survey’s historical average,” survey compiler Markit said. The City had expected a slight improvement to 56.5.

Updated

Italian services firms recorded a rise in business activity for the second month running in November, although a slight fall in new business and shrinking backlogs of work painted a gloomier picture of the short-term outlook, survey compiler Markit said. The headline business activity index rose to 51.8 from October’s 50.8.

Eurozone data points to 'mere 0.1% growth' in Q4

For the eurozone as a whole, Markit’s composite PMI, based on surveys of thousands of manufacturing and services companies across the currency bloc, slid to 51.1 in November from October’s 52.1, despite heavy price cutting by businesses.

Chris Williamson, Markit’s chief economist, said:

The region is on course to see a mere 0.1% GDP growth in the final quarter of the year, with a strong likelihood of the near-stagnation turning to renewed contraction in the new year unless demand shows signs of reviving.

Updated

French business activity shrinking at fastest rate in 9 months

In France, business activity across manufacturing and services shrank at the fastest rate in nine months in November, dragged down by weak services. Markit’s composite PMI dropped to 47.9 from October’s 48.2, below the 50 mark that separates expansion from contraction. In the services sector alone, the reading was 47.9.

Markit economist Jack Kennedy said:

The latest PMI data show a deepening downturn in the French service sector during November. With manufacturing also continuing to struggle, the private sector looks set to act as a drag on GDP during the fourth quarter.

German PMI points to quarter of 'marginal growth'

Germany’s private sector grew at the slowest pace in 17 months in November, a survey showed. Markit’s final composite PMI, which covers the manufacturing and service sectors, dropped to 51.7 from 53.9 in October. The services index alone fell to 52.1, a 16-month low.

Markit economist Oliver Kolodseike said:

Composite PMI data suggest the German economy is likely to face another quarter of only marginal growth at best, with fears of a renewed downturn intensifying.

Financial markets update: rouble slides further

In financial markets, the rouble opened flat but then resumed its slide despite data confirming that the Russian central bank stepped in to defend the currency on Monday. It is down 1.2% at 54.47 to the dollar, and nearly 1% lower at 67.25 against the euro.

The FTSE 100 index in London is slightly down ahead of the chancellor’s autumn statement: it has slipped more than 7 points or 0.1% at 6734.49. Germany’s Dax is 17 points ahead at 9951.27, a 0.2% gain, while France’s CAC has edged down nearly 4 points, or 0.08%, to 4384.57.

Ireland’s services PMI edged up to 61.6 last month from 61.5 in October, signalling strong expansion.

Celtic tiger still roaring: #Ireland's PMI remained elevated in Nov running at level consistent with 7% y/y growth pic.twitter.com/CSJCbhyEYd

— Chris Williamson (@WilliamsonChris) December 3, 2014

The Markit PMI data for Spain suggests that growth in its service industries lost momentum as both activity and new business grew at much weaker rates than seen in October. The headline business activity index dropped to 52.7 in November from 55.9 in October, the lowest reading for a year.

Japan's services sector returns to growth

Enough of the past. The main event on the economic calendar today is the PMI services data for the eurozone (released between now and 9am GMT) and the UK (9.30am GMT).

We’ve already had data for Japan, the world’s third-largest economy: its services sector returned to growth in November. Markit’s service sector purchasing managers index (PMI) rose to 50.6 from 48.7 in October. A reading above 50 indicates expansion.

Down under, the Australian economy expanded just 0.3% in the three months to September, compared with expectations of 0.7% growth. The Australian dollar fell below 84 US cents for the first time since 2010, which Joe Hockey, the country’s treasurer, said was very welcome. You can read our story here.

Updated

Returning to the war debt, the first bonds were sold to private investors in 1917 with the advertisement: “If you cannot fight, you can help your country by investing all you can in 5 per cent Exchequer Bonds ... Unlike the soldier, the investor runs no risk.”

Last night, the Bank of England and the Treasury announced a one-year extension to the Funding for Lending scheme, to support bank lending to small and medium-sized businesses next year – “even in the event of stress in bank funding markets”.

They said the scheme, which provides cheap funding to banks to support business lending, has contributed to a “substantial fall in bank funding costs” since its launch in mid-2012.

Fidelity and Threadneedle Asset Management are the biggest holders of the 3.5% bond, called War Loan. No doubt they will be delighted with today’s announcement. Toby Nangle, a fund manager at Threadneedle, has been lobbying the Debt Management Office to pay off the first world war bond.

You can read the Treasury’s announcement in full here.

Updated

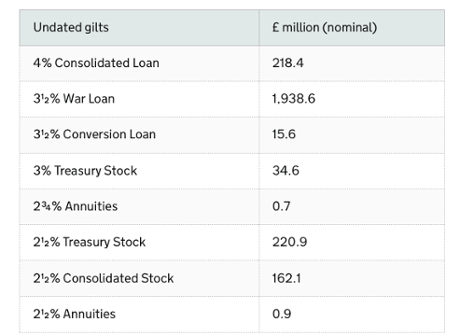

These gilts include some debt originally issued in the era of the South Sea bubble in the 18th century, as well as to fund he Bank of England’s nationalisation.

The nation has paid some £5.5bn in interest on 5% War Loan 1929-47 and 3½% War Loan since 1917.

3½% War Loan is the most widely held of any UK government bond, with more than 120,000 holders. 97,000 of these investors hold less than £1,000 nominal, and almost 38,000 holders own less than £100.

Updated

The news comes just over a month after the government said it would pay off £218m from a 4% consolidated loan next February, as part of a redemption of bonds stretching as far back as the 18th century. They also relate to the South Sea Bubble crisis of 1720, the Napoleonic and Crimean wars and the Irish potato famine.

This was the first planned repayment of an undated gilt of this kind for 67 years. The Treasury said today’s announcement kicks off a strategy to remove all six of the other remaining undated gilts in the government’s portfolio, “when we deem it value for money to do so”.

Updated

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

George Osborne has kicked off the autumn statement (which he will present in the House of Commons at 12.30pm) several hours early by announcing that the Treasury will repay the nation’s entire first world war debt.

The Treasury will redeem the outstanding £1.9 billion of debt from 3½% War Loan on 9 March 2015. This bond was issued in 1932 by the then chancellor Neville Chamberlain to reduce the costs of servicing the national debt. The bond was issued in exchange for 5% War Loan 1929 to 1947, which had been issued in 1917 as part of the government’s efforts to raise money to pay for the first world war.

The Treasury said it would refinance the war debt with new bonds, taking advantage of low interest rates.

Osborne said:

This is a moment for Britain to be proud of. We can, at last, pay off the debts Britain incurred to fight the First World War.

It is a sign of our fiscal credibility and it’s a good deal for this generation of taxpayers.

It’s also another fitting way to remember that extraordinary sacrifice of the past.

Updated