It’s a busy day for central banks on Thursday, with the latest Bank of England interest rate decision as well as the minutes.

Meanwhile the Federal Reserve will release the minutes from its September meeting, when it held rates when it was widely expected to sanction a rise.

So we’ll be back tomorrow to cover all that, as well as the IMF meeting in Lima and the rest of the day’s financial news. For now it’s time to close up, so thanks for all your comments and see you tomorrow.

European markets close off their best levels

Global stock markets have been supported in recent days by the hope that the Federal Reserve will not raise US interest rates this year, in the wake of Friday’s weak US jobs data. Other central banks are also expected to continue to support the global economy with further stimulus measures.

And a recent surge in the oil price, with output predicted to fall and demand stabilising, has also helped, as has the fact that China’s stock market - so volatile - has been closed for a holiday which ends tomorrow.

Hence an early surge on stock markets, with the FTSE 100 at a seven week high despite more gloomy comments from the IMF on the global economy.

However as the markets came towards the close of trading, much of the optimism fizzled out. One factor is the oil price losing all the day’s gains after US crude stocks rose by more than expected last week. Brent crude is currently down 0.08% at $51.88 following the US data, having earlier climbed as high as $53.15.

But with commodity companies still ahead on the day, most markets have ended in positive territory. The final scores showed:

- The FTSE 100 finished up 10.19 points or 0.16% at 6336.35

- Germany’s Dax added 0.68% to 9970.40

- France’s Cac closed up 0.14% at 4666.94

- Italy’s FTSE MIB dipped 0.79% to 22,007.34

- Spain’s Ibex ended up 0.66% at 10,170.0

- In Greece the Athens market added 1.4% to 680.10

On Wall Street the Dow Jones Industrial Average is up just 11 points or 0.07%.

More on oil, and the effect of a falling crude price on exporters, from the International Monetary Fund. Larry Elliott reports:

The full extent of the impact of slumping crude prices on Saudi Arabia’s public finances has been highlighted by the International Monetary Fund in a new report telling oil exporters to be braced for a prolonged period of disruption to their budgets.

The fund’s half-yearly fiscal monitor report shows that in the past three years a hefty budget surplus in Saudi Arabia has been turned into a deficit of more than 20% of GDP – double the shortfalls seen in the UK and the US during the worst of the global slump of 2008-09.

Other leading oil exporters – Russia, Libya, Venezuela, Kuwait, Qatar, the United Arab Emirates, Oman and Angola – have also suffered marked deteriorations in their public finances as a result of the fall in crude from a peak of almost $130 a barrel in 2012 to just under $53 currently.

“Natural resource-rich countries benefited from an exceptional commodity price boom during the 2000s, with metal and oil prices reaching historic highs,” the report said. “This provided a substantial boon to resource-rich developing countries, which benefited from large increases in fiscal revenues and the opportunity to promote economic transformation and development.”

Full story here:

The recent rise in oil prices may not last, according to Joshua Mahony, market analyst at IG. He said:

While the recent rise in the price of oil has led mining firms higher, it is clear that oil price volatility could easily see everything crash lower once more like a house of cards.

This afternoon saw oil inventories rise by 3.1m barrels, taking some of the wind out the sails of this recent rally. The continued build-up of US crude inventories undermines the idea that US producers are finally feeling the pinch and cutting back on production. Oil is and will remain in strong supply going forward.

The question is whether demand will pick up at these lower prices. The EIA today announced expectations that 2016 will see oil demand rise by the most in six years. However, perhaps the most telling announcement from the EIA today was that the past four weeks saw lower demand than this time last year when oil prices were $40 higher that today.

There is a feeling that despite a possible spike in oil prices, the long term cold see them move lower yet.

Oil stocks rise by more than expected

Oil prices have edged down from their highest levels of the day as US crude stocks rose by more than expected last week, up by 3.1m barrels compared to forecasts of a 2.3m increase.

Brent crude is currently up 0.96% at $52.42 a barrel after earlier climbing as high as $53.15. The price has been supported in recent days by signs that Russia and Opec were willing to discuss the oversupply situation and the US energy department said it expected production to fall next year.

US COMMERCIAL CRUDE STOCKS rose +3.1 million bbl last week, up +10.2 million bbl in last 6 weeks: pic.twitter.com/ChUZPDlnjP

— John Kemp (@JKempEnergy) October 7, 2015

US GASOLINE STOCKS stand at 24.76 days of current consumption, up from 23.99 days this time in 2014 pic.twitter.com/ijH5BbRqBJ

— John Kemp (@JKempEnergy) October 7, 2015

Updated

Here’s Heather Stewart’s analysis of the IMF financial stability report:

The next financial crisis is coming, it’s a just a matter of time – and we haven’t finished fixing the flaws in the global system that were so brutally exposed by the last one.

That is the message from the International Monetary Fund’s latest Global Financial Stability report, which will make sobering reading for the finance ministers and central bankers gathered in Lima, Peru, for its annual meeting.

Massive monetary policy stimulus has rekindled growth in developed economies since the deep recession that followed the collapse of Lehman Brothers in 2008; but what the IMF calls the “handover” to a more sustainable recovery – without the extra prop of ultra-low borrowing costs – has so far failed to materialise.

Meanwhile, the cheap money created to rescue the developed economies has flooded out into emerging markets, inflating asset bubbles, and encouraging companies and governments to take advantage of unusually low borrowing costs and load up on debt.

“Balance sheets have become stretched thinner in many emerging market companies and banks. These firms have become more susceptible to financial stress,” the IMF says.

The full piece is here:

Wall Street higher in early trading

US markets are joining in the global rally, helped by energy companies as crude continued to rise on talk of falls in output. The prospect of the US Federal Reserve raising interests has grown less likely, which is also giving some support to shares.

The Dow Jones Industrial Average is currently up 145 points or 0.8% while the S&P 500 is around 0.7% higher.

The FTSE 100 is up 0.95%, Germany’s Dax is 1.7% better and France’s Cac has climbed 1.2%.

IMF: Shock could come from Greece, or China

Risks to financial stability are pointing firmly to the downside, says the IMF (ie, there’s more chance of a nasty ending than a nice one).

In its new report, it warns:

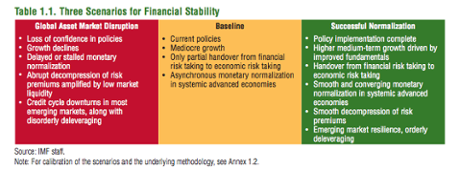

The possibility of a global asset market disruption, whereby market risk premiums would decompress in a disorderly way and spread financial contagion, remains heightened.

What might cause it? The IMF says it could come from the eurozone, or from emerging markets:

Potential near-term adverse shocks in the presence of system vulnerabilities could prematurely halt the rise in U.S. interest rates, degrade nancial stability, and stall the economic recovery.

Shocks could originate in advanced economies—possibly owing to greater spillovers from Greece to the euro area and international markets—or emerging markets, for example, from greater-than-expected spillovers from China.

And here’s a nicely colour-coded chart of how things might play out:

Updated

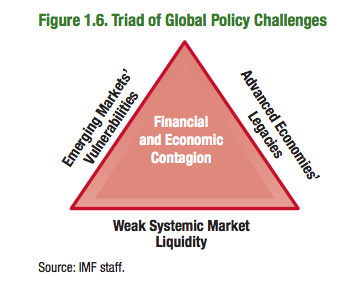

IMF warns of 'triad' of risks facing world economy

The International Monetary Fund has warned that that the global economy faces a ‘triad of risks’ which could trigger a new phase of the crisis.

Its new Global Financial Stability Report, the IMF identifies ‘crisis legacies’ in advanced economies, vulnerabilities in emerging market economies, and systemic market liquidity concerns.

It says:

If these challenges are mishandled, they could materialize as significant risks to financial stability.

Here’s some detail from the report, being released now.

Emerging markets: the IMF warns that bank and corporate balance sheets are stretched, meaning they are vulnerable to a downturn. It singles out China, and its “delicate balance of transitioning to more consumption-driven growth without activity slowing too much”.

Legacy issues from the crisis in advanced economies: these include high public and private debt, and the remaining problems in the architecture of the eurozone (ie, the need for more fiscal union)

Weak systemic market liquidity: The IMF is concerned that risk premiums are below historical averages, even though the Federal Reserve is poised to raise interest rates son:

As such, the global financial system faces an unprecedented adjustment as risk premiums “normalize” from low levels alongside rising policy rates, amid a modest global cyclical recovery.

Last October, there was a ‘flash crash’ in the market for US Treasuries (government bonds), and analysts wonder if it could happen again....

The challenge will be for abnormal market conditions to adjust smoothly to the new environment.

However, there are risks from a rapid decompression, particularly given what appear to be more brittle market structures and market fragilities concentrated in credit intermediation channels, which could come to the fore as financial conditions normalize.

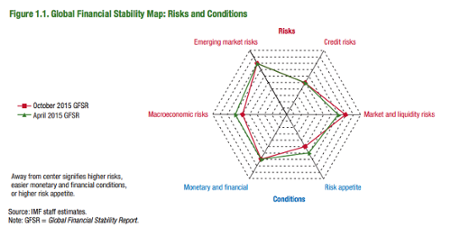

And this chart confirms that liquidity is a growing worry for the IMF:

Updated

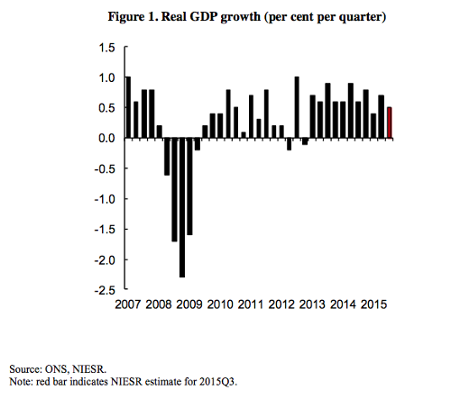

UK economic growth slows in third quarter - NIESR

UK economic growth slowed in the third quarter compared to the previous three months, according to the think tank The National Institute of Economic and Social Research.

NIESR’s latest monthly estimate of GDP suggests that output grew by 0.5% in the three months to the end of September after growth of 0.5% in the three months ending in August.

That compares to official figures for the second quarter to the end of June of a 0.7% rise in GDP. NIESR said:

This slight softening in the third quarter is expected to be temporary. It is consistent with our latest forecast for the year as a whole.

Economic growth remains reasonable and, although we do not expect the Bank of England’s Monetary Policy Committee to vote to raise rates at its October meeting [on Thursday], we continue to expect the first rise in Bank Rate in the first half of 2016.

The broad story of output growth post-recession is little changed and the return to the pre-recession peak following the most recent recession remains the most protracted in the last 100 years.

NIESR is forecasting GDP growth of 2.5% per annum in 2015 and 2.4% in 2016.

On Tuesday the IMF predicted UK growth of 2.5% in 2015, falling to 2.2% in 2016.

Heads-up. In 30 minutes the International Monetary Fund will issue its latest Global Financial Stability Report, outlining its latest concerns over the world economy.

The pick-up in commodity prices today hasn’t prevented Glencore from laying off 800 staff in South Africa.

Reuters is reporting that the company has put its platinum mine on ‘care and maintenance’ , and reining in production at the site.

When a slowdown in China hits a global mining firm HQ’d in Switzerland and listed in London, the ripples are felt worldwide.

Updated

You have have heard conspiracy theories that our central banks don’t actually own all the gold they claim to.

Well, worry not! At least if you’re in Germany, where the Bundesbank has now published a list of every single gold bars, individually numbered.

Bundesbank to doubters: Here Is our gold. Every. Single. Bit of it. http://t.co/ugupEHhxiY Publishes 2,302 page long list of gold holdings.

— Bloomberg Markets (@markets) October 7, 2015

Germany has been in quite a tizz over its gold reserves.

Campaigners have protested that the bullion shouldn’t be kept in New York and Paris, while the country’s top auditors court politely suggested three years that an audit should take place.

Bloomberg’s Lorcan Roche Kelly explains:

Perhaps the Bundesbank has learned a lesson here and realized that if it had just complied with the wishes of the Federal Court of Auditors back in 2012 it could have avoided this mess.

Or perhaps it has just become tired of people asking and decided to give the doubters enough data to keep them busy for a very, very long time.

This is going to make some riveting weekend reading. http://t.co/ueBE55r0HX pic.twitter.com/YYU4gqxEjE

— Joseph Weisenthal (@TheStalwart) October 7, 2015

AB InBev will have to dig rather deeper into its pockets if it wants to sate its thirst for SABMiller (an experience many familiar to many in the City, I suspect).

Ha...course no such transparency in the boozy M&A dance! But ppl familiar told Bloomberg £45 fairer value...@Brenda_Kelly @SABMiller

— Caroline Hyde (@CarolineHydeTV) October 7, 2015

SABMiller rejects £68bn takeover proposal

It’s official - SABMiller has resoundingly rejected AB InBev’s £68bn takeover proposal.

After mulling it for a few hours, the SAB board have concluded that the £42.15 per share offer, made this morning, undervalues them.

Here’s the statement:

The Board of SABMiller has now met formally to consider the new proposal announced by AB InBev today (the “£42.15 Proposal” as defined in the announcement by SABMiller earlier today).

The Board, excluding the directors nominated by Altria Group Inc., has unanimously rejected the £42.15 Proposal as it still very substantially undervalues SABMiller, its unique and unmatched footprint, and its standalone prospects.

#SABMiller rejects #InBev offer for £42.15 per share.

— Ipek Ozkardeskaya (@IpekOzkardeskay) October 7, 2015

Updated

After the turmoil in late August and September, the stock markets have quietly posted some solid gains in October.

Bloomberg’s Mark Barton is tweeting some key charts:

European #mining companies rise for a 7th day - the best run since December 2013... pic.twitter.com/hnuKHI70Vr

— Mark Barton (@markbartontv) October 7, 2015

#EmergingMarket stocks rise for a 6th day - longest stretch since April pic.twitter.com/6eui7YmZKA

— Mark Barton (@markbartontv) October 7, 2015

The 7-day 18% rally in European #oil stocks is the biggest since 2008... pic.twitter.com/u5wwhegMLJ

— Mark Barton (@markbartontv) October 7, 2015

Mining stocks push markets higher

Europe’s stock markets are refusing to be downhearted by the German and Spanish factory slowdown.

The FTSE 100 has hit its highest level in seven weeks, with four mining companies leading the way. Anglo American is leading the risers, up 10%.

Oil companies are also gaining, reflecting a 1.7% rise in the cost of crude oil today.

The trigger is a research note from Morgan Stanley, who reckons sentiments against emerging markets have turned too sour.

They argue:

We recommend investors raise their exposure to emerging markets/commodities given the combination of very low sentiment, attractive relative valuations and a likely inflection in macro sentiment...

We upgrade mining/materials from underweight to overweight and reiterate our overweight position in energy.

Full details in Nick Fletcher’s latest market report:

UK companies that actually make things are lagging behind those who dig stuff out of the ground:

British industry is doing okay - but manufacturers continue to struggle – a global phenomenon pic.twitter.com/CrjTOYPAa4

— RBS Economics (@RBS_Economics) October 7, 2015

Encouraging news from Greece. The European Central Bank has cut the amount of emergency support it is providing to the country’s banks by €1bn, to €87.9bn.

That’s at the request of the Bank of Greece.

The ECB explains:

The reduction of €1.0bn in the ceiling reflects an improvement of the liquidity situation of Greek banks, amid a reduction of uncertainty and the stabilization of private sector deposits flows.

Britain’s factories posted a 1.0% rise in industrial output in August, beating Germany and Spain.

That’s much stronger than the 0.3% rise which economists had expected. It was mainly driven by stronger oil and gas production, and a pick-up in car production after shutdowns in July.

UK manufacturing output (a more narrow measure) rose by 0.5% during the month, but was still 0.8% lower than a year ago after some tough months.

Manufacturing output increased by 0.5% in August - unlike to be enough to halt a 3rd consecutive quarter of contraction however #ukmfg

— EEF Economics Team (@EEF_Economists) October 7, 2015

Howard Archer of IHS Global Insight says the UK industrial sector has been through a soft patch:

August’s rebound in industrial production means that the sector may have managed to eke out marginal growth in the third quarter rather than contracting as had previously looked likely.

Even so, industrial production was still only up 0.1% in the three months to August compared to the three months to May.

Updated

SABMiller responds to £68bn offer

Brewing giant SABMiller has just issued a lukewarm, borderline chilly, response to AB InBev’s new £68bn takeover offer.

In a statement to the City, SAB points out that the new proposal, at £42.15 per share, is only 15p higher than the previous proposal which was rejected on Monday.

It’s not a full-blown rejection, as the board are planning to meet to discuss this new plan.

However, chairman Jan du Plessis was pretty blunt, saying:

“SABMiller is the crown jewel of the global brewing industry, uniquely positioned to continue to generate decades of standalone future volume and value growth for all SABMiller shareholders from highly attractive markets.

AB InBev needs SABMiller but has made opportunistic and highly conditional proposals, elements of which have been deliberately designed to be unattractive to many of our shareholders. AB InBev is very substantially undervaluing SABMiller.”

SABMiller signals rejection of new approach http://t.co/TsNrsxW5cx

— fastFT (@fastFT) October 7, 2015

Updated

A UK lawyer representing around 1,200 Volkswagen owners in the UK is extremely unimpressed by Matthias Müller’s plan to start vehicle recalls in January:

Ms Michalowska-Howells of Leigh Day says drivers need more answers:

“The way in which this is being handled by Volkswagen is staggering. Rather than responding to very serious concerns from their customers, they are providing the minimal information.

“The latest lamentable statement, given today to a German newspaper, does reveal that some customers will need serious interventions to parts of their vehicle. Which cars and what interventions?

“How will anyone be able to buy or sell an affected car without knowing this essential information?”

Updated

Volkswagen shares have jumped by 5% this morning after the German carmaker coughed up its plan to fix the emissions scandal.

CEO Matthias Mueller told the daily Frankfurter Allgemeine Zeitung that it will start recalling cars in January.

“If everything goes as planned, we can start the recall in January...All the cars should be in order by the end of 2016.”

This pushed VW’s share price up to €102.5, from €97 last night. But that is still more than a third below its pre-crisis level:

Volkswagen's stock chart is starting to look like BP's after oil spill http://t.co/IK62g3vi52 pic.twitter.com/nWCCjUkqQV

— Bloomberg Business (@business) October 7, 2015

In another development, Volkswagen has reported that more than 50,000 defective cars were sold in Australia, plus 17,000 trucks.

This chart shows that a) monthly German industrial orders are volatile, b) August’s 1.2% decline was the biggest in a year:

More bleak numbers. German industry output unexpectedly falls even ahed of VW crisis. http://t.co/m5q7i61p5K pic.twitter.com/0sv2zn9db0

— Holger Zschaepitz (@Schuldensuehner) October 7, 2015

European stock markets are all gaining ground this morning, despite the disappointing factory output figures from Spain and Germany.

Speculation that the US Federal Reserve won’t raise interest rates this year is driving up the value of commodities. Weak data probably means looser monetary policy, for even longer.

The FTSE 100 has gained 41 points, hitting its highest level since late August, led by mining stocks. Anglo American is up 8.5%, with Rio Tinto gaining almost 6%.

Last couple of days have seen FTSE100 back above 6300 for first time since August's Black Monday. pic.twitter.com/tmdCfJp1An

— David Jones (@JonesTheMarkets) October 7, 2015

In Germany, the DAX has gained 0.4%.

Another blow to the eurozone. Output at Spain’s factories shrank by 1.4% month-on-month in August.

That’s rather worse than the 0.4% decline which economists had expected, and even sharper than the reversal in Germany.

Spanish Industrial Production Data (Aug): M/M -1.4% v -0.4% exp, prev +0.6% rev +0.7% SA Y/Y +2.7% v +4.7% exp, prev +5.2%

— Sigma Squawk (@SigmaSquawk) October 7, 2015

There’s a frisson of deal mania in the City this morning, after brewing giant Anheuser-Busch InBev hiked its proposed takeover offer for British brewer SABMiller to £68bn.

This would be one of the biggest half-dozen deals ever, creating a brewing giant producing a third of the world’s beer.

There’s not response from SAB yet, but its shares are up 2.7% as traders anticipate more developments.

According to Reuters, a quarter of the average daily volume of SAB shares changed hands in the first four minutes of trading today.

Updated

Tesco shares slide after profits shrink

Shares in Tesco have fallen by more than 3% after the supermarket chain told shareholders that operating profits more than halved in the last six months, to £354m.

As my colleague Fiona Walsh explains, today’s figures show that the turnaround job at Tesco isn’t over yet:

Tesco has had a traumatic year, hit by an accounting scandal and the fierce grocery price war. It has been losing sales to discount retailers such as Aldi and Lidl and last year posted a record £6.4bn loss, one of the biggest in British corporate history.

The company’s chief executive, Dave Lewis, who joined from Unilever just over a year ago, has embarked on a turnaround plan for the group, cutting prices and improving customer services. But some City analysts say progress has been too slow.

Lewis said: “We have delivered an unprecedented level of change in our business over the last 12 months and it is working. The first half results show sustained improvement across a broad range of key indicators.”

Germany’s economy ministry is urging us not to panic, and claiming that the drop in factory output is partly due to the summer holidays.

Carsten Brzeski, economist at ING, agrees that’s a factor -- but says the figures are still disappointing.

Yesterday’s drop in new orders already signalled a note of caution. The August drop marked the first decline for two consecutive months since the beginning of the year. A clear sign for caution.

Over the last couple of months, the industrial safety net of low inventories and filled order books has become thinner.

German industrial production disappoints. Impact of Chinese slowdown or simply too much vacation? http://t.co/gSJWWSofRm

— Carsten Brzeski (@carstenbrzeski) October 7, 2015

The German economy doesn’t need any more bad news at present, given the VW emissions scandal:

Warning lights are flashing RED on entire Germany economy, not just on the dashboards of Volkswagen. MINUS 1.2% https://t.co/ULcKANOLoA

— HansNichols (@HansNichols) October 7, 2015

Christian Lips, an economist at NordLB in Hanover, says today’s report shows Germany’s industry is now lagging behind the consumer sector.

He told Bloomberg:

“A certain weakness in the [German] manufacturing sector cannot be ignored, even though it stands in stark contrast to strong private consumption.”

Production of “investment goods” (such as machinery) shrank by 2.1% in August; a sign that companies aren’t splashing out on new equipment.

Updated

German industrial output drops by 1.2% in August

Germany’s powerhouse manufacturing sector has suffered a poor August, in another signal that the global economy is feeling a chill.

Figures just released show that industrial output across Germany shrank by 1.2% in August, much worse than the +0.2% which economists had expected.

These monthly figures can be volatile - but it comes a day after German firms reported a slide in factory orders in August too.

German Industrial Production for Aug follows in footsteps of yesterday's awful Factory Orders

— Mike van Dulken (@Accendo_Mike) October 7, 2015

German IP down 1.2% vs forecast for 0.2% increase. After factory orders, that's second disappointment this week.

— Fergal O'Brien (@fergalob) October 7, 2015

It indicates that the slowdown in emerging economies such as China is now hitting Europe’s largest economy. More reaction to follow....

Introduction: IMF warning looms over markets

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

There’s a subdued feeling in the markets this morning, after the International Monetary Fund warned that the global economy is on the brink of stagnation

As we covered yesterday, the IMF has cut its growth forecast again and warned that “a return to robust and synchronised global expansion remains elusive”.

It’s another reminder that the slowdown in emerging markets could cause more pain for developing nations, as America’s central bank keeps its finger hovering over the rate rise button.

#IMF cuts its global forecast to 3.1% this year. Now pretty similar to us. But key thing is heightened EM risks as #US tightening nears

— Robin Bew (@RobinBew) October 7, 2015

New industrial production data released this morning from Germany, Spain, and the UK will show whether factories are now finding conditions tougher

In the City, traders are crunching through financial results from Tesco. Britain’s largest supermarket has posted a 55% drop in operating profits, to £354m down from £779m last year. More on that shortly.

And Greece’s parliament will conclude the debate on its 2016 budget today, with a confidence vote at midnight Athens time (so we might pick up the result tomorrow morning). Finance minister Euclid Tsakalotos has predicted that Greece could pull out of recession by the middle of 2016, if all goes well.

We’ll be tracking all the main events through the day

Updated