Emerging countries, already economically unstable, are being challenged by the currency depreciation that occurs due to capital outflow. This is because the United States, which continues to raise its interest rates, has become a more appealing destination for capital. Emerging economies have been rocked by U.S. financial policy in the past as well. If they fumble their response, it could put the world economy at risk.

Defense plans

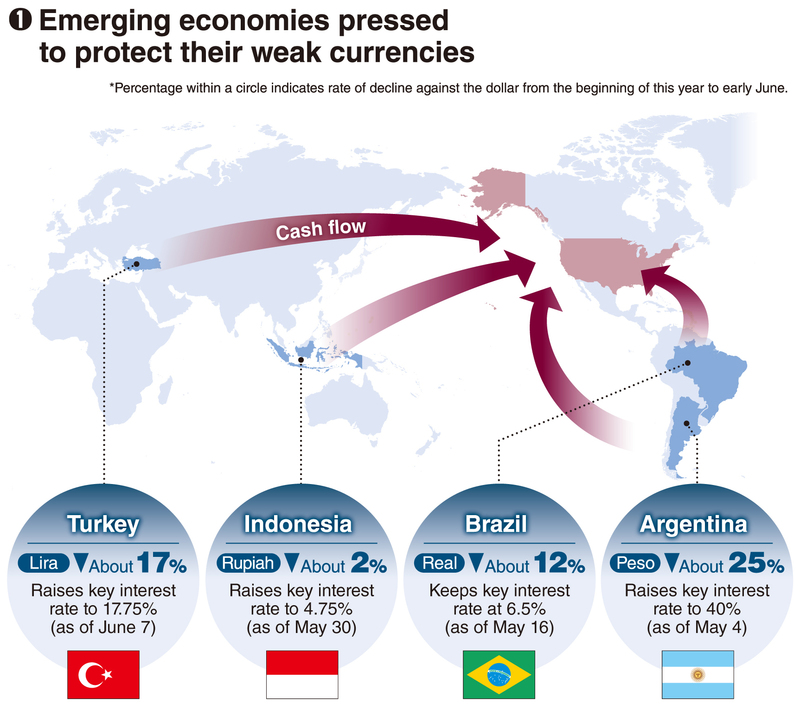

The Central Bank of Turkey announced on June 7 it would raise one of its main key interest rates from 16.5 percent to 17.75 percent. The Turkish lira took a big plunge from the start of the year.

Alarmed by selling pressure on its currency the rupiah, Bank Indonesia, that country's central bank, held a special meeting on May 30 and decided to raise its key interest rate by 0.25 percentage point to 4.75 percent.

Central Bank of Argentina, which has seen its currency plummet amid economic turmoil, has repeatedly raised key interest rates, with its benchmark rate climbing as high as 40 percent in May. The JP Morgan Emerging Market Currency Index, the U.S. financial giant's compilation of price fluctuations in the currencies of primary emerging markets, has fallen about 5 percent from the start of the year.

According to estimates of the Institute of International Finance, the amount of outflow from stock and bond markets in emerging nations in May was about 12.3 billion dollars (about 1.35 trillion yen). It was the largest-scale outflow since November 2016, prompting a market official to say, "This is tremendous outflow, despite the fact there were no major events that shook financial markets in May."

To prevent the currency sell-offs that come with capital outflow to other countries such as the United States, many emerging nations resort to currency defense (see below, chart 1).

The currency depreciation of emerging nations is closely connected to movements in the monetary policy of the U.S. Federal Reserve Board. Because it was implementing large-scale monetary easing in response to the financial crisis in autumn 2008, capital flowed from the United States, which had extremely low interest rates, to emerging nations, which had high interest rates. As the U.S. economy has recovered, however, and the Fed continues to raise interest rates, capital is returning to the United States.

The U.S. economy is robust and its employment situation has improved, with May's unemployment rate at 3.8 percent, the lowest in about 18 years. Given the trend that the United States' major companies are seeing increased profits, the Dow Jones Industrial Average for 30 companies' stocks has stayed in the high range of 23,000 to 26,000 since the start of the year.

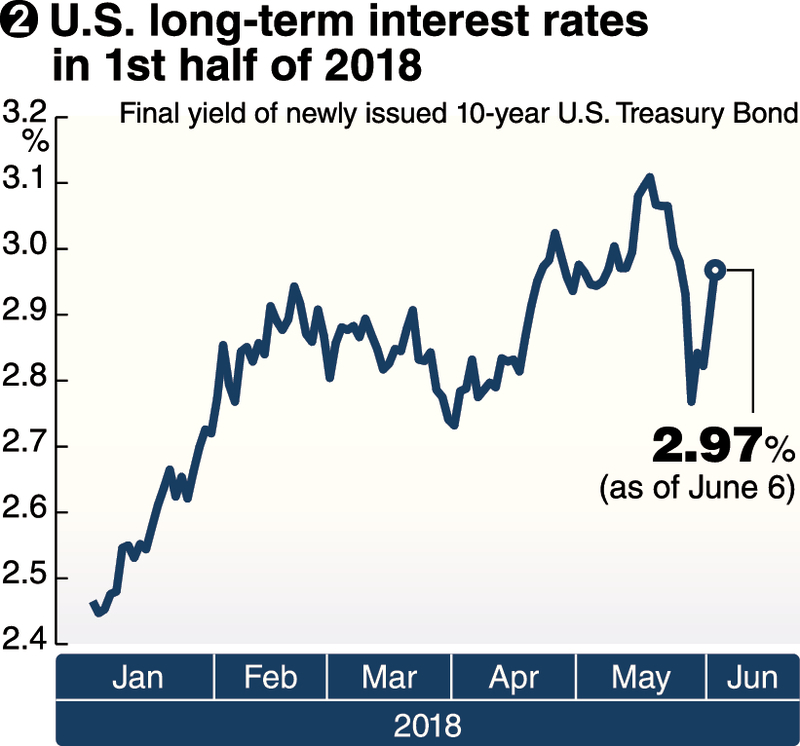

Ever since the Fed ended near-zero interest rate policy in December 2015, to prevent the economy from overheating, it has gradually raised the target range for the federal funds rate that serve as its key interest rate. It currently sits between 1.5 percent and 1.75 percent. Yields on newly issued 10-year government bonds, which serve as model indicators for U.S. long-term interest rates, also reached the 3 percent level in April for the first time in nearly four years. They have since hovered around 3 percent, too (see chart 2).

History repeats

Emerging nations have a history of suffering serious shocks, having been tossed around by U.S. monetary policy in the past. The Mexican currency crisis in December 1994 is one such example.

With the North American Free Trade Agreement's formation in 1992, investment capital began to flow from other countries to Mexico, which was in the midst of economic reform, in anticipation of its growth. When the Fed implemented large-scale interest rate hikes in November 1994, however, investment capital was diverted to the United States. Mexico's foreign exchange reserves almost hit bottom and its fixed exchange rate system became unsustainable. With its move to a floating exchange rate system, Mexico's peso took a steep plunge. The following year, Mexico suffered major negative growth.

The 1997 Asian currency crisis, spurred by speculators' currency sell-offs, is a similar case. Several of Asia's emerging nations that effectively had fixed exchange rate systems, such as Thailand and South Korea, were unable to withstand the sell-offs of their country's currency. When they moved to floating exchange rate systems, their currencies plunged, throwing their economies into turmoil. This, too, was in part caused by interest rate hikes by the Fed.

Emerging nations were hit by the so-called Bernanke Shock (see below) in 2013, which showed how strong an influence the Fed's monetary policy has on emerging nations' economies.

Emerging nations are once again facing currency depreciation due to stalled economic structural reforms and political instability. If the United States' long-term interest rates go higher, investors can safely manage their funds in the United States, which is greatly stable politically and economically.

Most emerging nations still have few industries that are internationally competitive, and are heavily reliant on imports of resources, consumer goods and other items. As currency depreciation continues, domestic inflation accelerates, which reduces consumption of households with effectively less buying power and stagnates production activities of companies hit by rising costs.

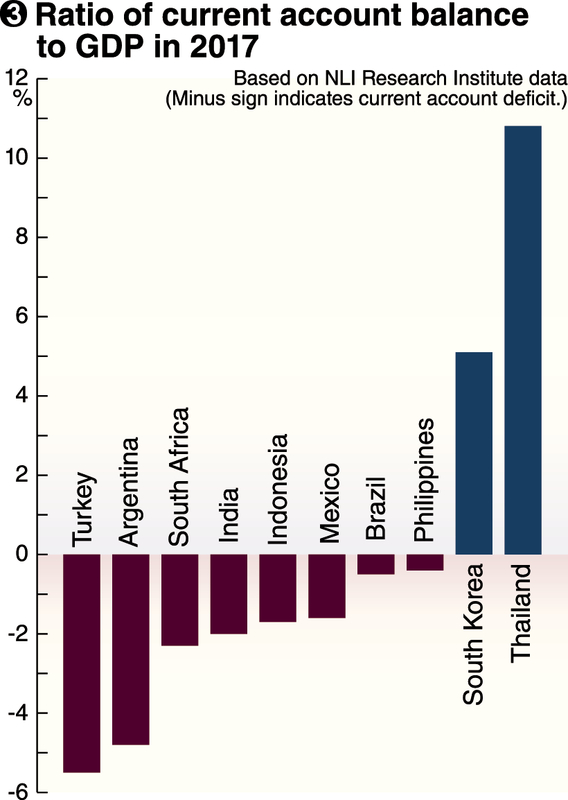

However, the impact of U.S. interest rate rises varies by emerging nation. Countries such as Thailand and South Korea, whose domestic industries are rather developed and whose current account balances are in the black, do not suffer as much of a shock. Countries now facing currency depreciation, such as Turkey, Indonesia and Argentina, have large account balances in the red relative to gross domestic product. (see chart 3)

"If emerging nations, which have fragile economic foundations, don't indicate a willingness to solve their problems, investors will withdraw their capital," said Makoto Saito, a researcher at the NLI Research Institute who is knowledgeable about emerging nations.

Pace of interest rate hikes

Compared to the past, there is little chance of falling into a currency crisis. This is because countries have bolstered preventive measures against crisis, such as having currency swap systems in place so that countries that lack foreign reserves can assist each other with capital.

Kota Hirayama, a senior economist in charge of emerging nations at SMBC Nikko Securities Inc., said: "Many emerging nations are stockpiling foreign exchange reserves, and even if the United States continues to raise its interest rates, it would be hard for a situation like the currency crises of the past to happen."

Despite this, emerging nations are nervous about the pace of interest rate hikes by the Fed. The Fed looks like it will continue to slowly raise its interest rates, reaching about 3 percent by the end of next year. If they move faster than anticipated, capital outflow could accelerate even further.

Hirayama added, "Depending on the pace of interest rate hikes in the future, further currency depreciation could cause the economies of emerging nations to deteriorate, and through the shrinking of trade, negatively affect the global economy."

To prevent turmoil in the global economy, the Fed must keep an eye not only on the U.S. economy but also trends in emerging nations, while emerging nations need to promote the structural reforms that lead to improvements in current account balances.

-- Currency defense

When a country's financial authority, with the aim of stopping capital from fleeing and its currency dropping, undertakes foreign exchange intervention by selling foreign currencies such as the dollar and buying its own currency, with the central bank implementing emergency interest rate hikes and other measures. Common among countries with fragile economic foundations.

-- Bernanke Shock

Occurred May-June 2013, when Ben Bernanke, then-chairman of the U.S. Federal Reserve Board, implied that it would scale back its quantitative easing, plunging the world's financial markets into severe turmoil. Long-term U.S. interest rates climbed as the dollar continued to be bought, while currency depreciation and low stock prices spread in emerging nations.

Read more from The Japan News at https://japannews.yomiuri.co.jp/