LONDON -- The problem of sluggish inflation despite economic recovery is an issue shared among leading advanced economies. Japan has struggled with deflation and sluggish inflation since the latter half of the 1990s, but Europe and the United States have only had to confront this problem since the financial crisis in 2008. Greater attention must be focused on the influence of price trends on monetary policy.

The leaders of central banks, economists and other experts from around the world gathered in Sintra, a tourist destination in Portugal, in mid-June. They came to participate in a European Central Bank Forum on the theme of how economic recovery links to price growth through wages.

Is it wage suppression?

Participants discussed the problem of suppressed wage growth as a possible cause for stagnant prices. A variety of theories were offered, including the weakening of labor unions and the trend among workers toward valuing stability over pay raises.

There is analysis that backs this up. International Monetary Fund Economist Stephan Danninger cited a decrease in the number of people changing jobs in pursuit of higher wages, after the global financial crisis in 2008, in an article analyzing U.S. wage conditions in 2016. The United States is polarized with a small number of wealthy individuals and low-wage workers, shrinking the middle class and making it difficult to find work with better wages even by changing jobs. Danninger views the decline in job turnover rate as leading to falling wages

However, at the forum, ECB President Mario Draghi stated: "[T]here is clearly a variety of reasons why the response of inflation and wages has been so slow ... [T]o disentangle all these reasons is very difficult." U.S. Federal Reserve Board Chairman Jerome Powell also remarked, "[It is] hard to assess whether movements in inflation reflect the cyclical position of the economy or other influences." He expressed the view that the situation is difficult to explain as a labor market issue alone.

U.S., Europe follow Japan's path

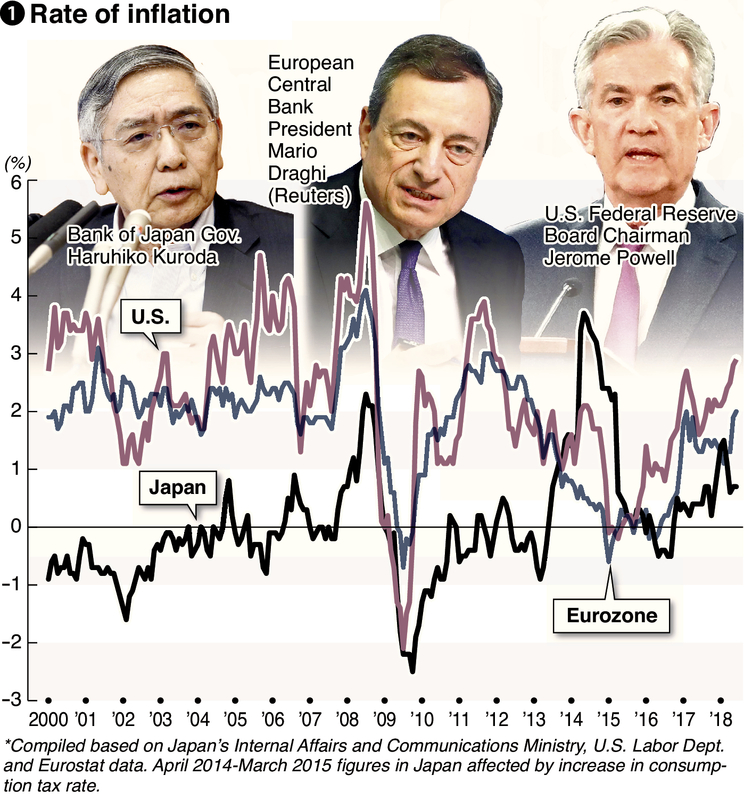

Price stagnation is a relatively new problem for Europe and the United States. Prior to the collapse of Lehman Brothers in September 2008, the U.S. consumer price index (see below), or CPI, indicated growth of more than 5 percent over the previous year (see chart 1), and the eurozone also achieved 4 percent growth, which prompted elevated wariness about inflation. In contrast, Japan fell into deflation in the latter half of the 1990s when a succession of financial institutions went bankrupt, and it has still not reached the point at which it could declare the end of deflation. Europe and the United States are following the path of Japan's challenges.

Price trends are thought to be intimately connected with wages. When economic conditions improve, large amounts of goods and services are purchased, causing prices to go up. Business performance improves and wages rise as well.

It was feared that if the monetary easing policy went too far, the economy would overheat, and inflation would get out of control.

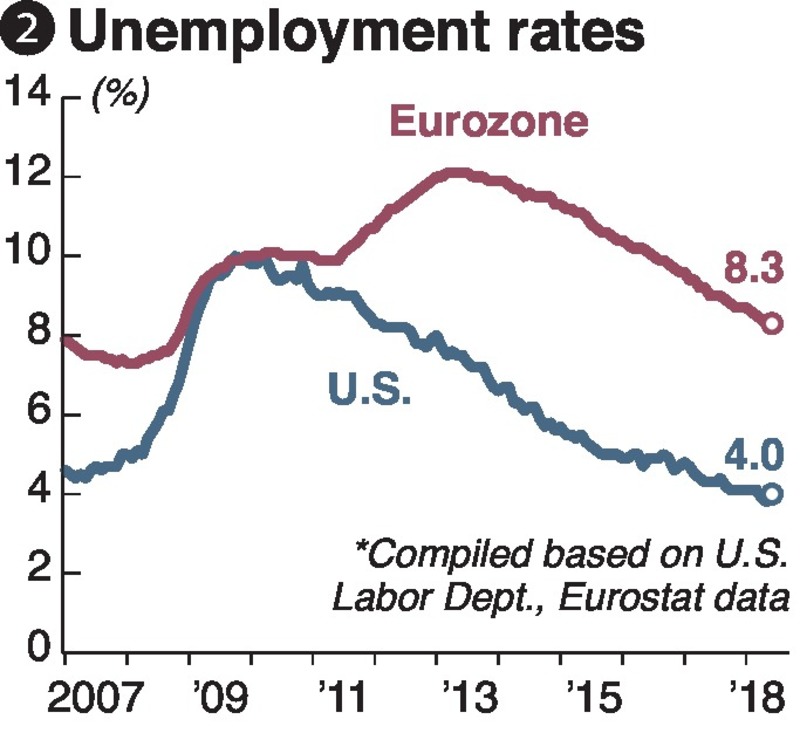

The United States is currently considered to have a state of nearly full employment, with an unemployment rate of 4 percent in June and 3.9 percent in July (see chart 2). The June unemployment rate in the eurozone was 8.3 percent, the lowest level in almost nine years. While large-scale monetary easing has led to economic recovery and employment has improved, prices are not growing at a level that reflects these conditions.

Contrast with Japan

While price rises in the United States and Europe are sluggish, they are still higher than in Japan. The U.S. consumer price index for June rose nearly 3 percent over the same month last year, and also rose in the eurozone by 2.1 percent in July, topping Japan's 0.7 percent in June.

However, when looking at items on an individual basis, there are cases in which it is difficult to claim that an economic virtuous cycle is having a ripple effect leading to rising prices.

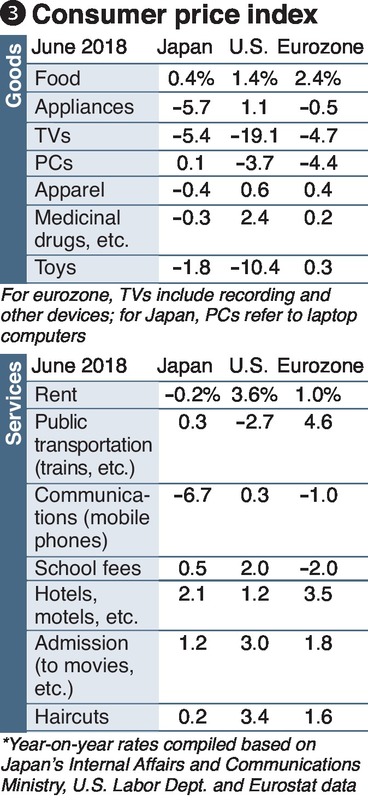

Examining U.S. consumer prices, rents in urban areas rose by 3.6 percent over the last year (see chart 3), which also made a large contribution to the overall rise in prices. For example, in the New York borough of Manhattan, it is not unusual for the monthly rent on a new one-bedroom property to exceed 4,000 dollars (about 440,000 yen). At this level, the increase in rent would be 144 dollars. When capital floods markets through monetary easing, prices related to real estate are comparatively more likely to rise.

In contrast, Japanese statistics showed rents dropped by 0.2 percent from the previous year. For real estate markets, the differences in characteristics from country to country play a significant role.

At the same time, there are other items for which prices have fallen in the same way. In the United States, television prices dropped roughly 19 percent from the previous year in June, while in Japan and the eurozone, prices fell roughly 5 percent. Multinational companies create optimized international production systems to keep down labor and distribution costs, enabling consumers to purchase products at lower prices. Factors used to explain price stagnation such as these are shared by Japan, the United States and Europe.

For the eurozone, high oil prices play a significant role in driving figures up, as the CPI minus volatile items such as energy and food grew at only 1.1 percent.

Financial risks

What sort of monetary policy can we expect from the central banks of Japan, the United States and Europe amid sluggish price growth?

The Fed raised the target for the federal funds rate, the U.S. policy interest rate, to between 1.75 percent and 2 percent annually, but there is a growing perception in the market that it will end at roughly 3 percent. It was raised to 5.25 percent in 2006, and to 6.5 percent in 2000, cooling down the economy, but there are few who anticipate the return of such times.

The ECB is carrying on with its negative interest rates policy and plans to make no rate hikes until next summer at the earliest. The Bank of Japan also revised its prices forecast downward on July 31, with the market taking this as a sign that there will be no rate hikes until 2020. Low interest rate policies of this sort may become semi-normalized.

Low interest rates lead to a lower interest burden on companies and individuals, but they also risk harming the financial system. A report released by the Bank for International Settlements in July warned, "An environment characterized by 'low-for-long' interest rates may dampen the profitability and strength of the financial firms and thus become a source of vulnerability for the financial system."

To achieve stable economic growth in Japan, the United States and Europe, it is important that no time is wasted in determining the causes of price stagnation and more in-depth analysis is conducted on its impact on the financial system.

-- Consumer price index

This index is an aggregate of the price changes for a range of individual goods and services. Conceptualized as selecting items representative of household consumption and placing them in a single basket, it expresses the change in the total value as an index number.

In Japan, there are more than 500 research items. For items that undergo rapid innovation such as computers, if the performance increases while the price remains the same, it will be counted as though the price had fallen. There are also indexes that exclude energy prices, which fluctuate due to market conditions.

While the Bank of Japan and European Central Bank take the CPI into consideration when managing monetary policy, the U.S. Federal Reserve Board places greater emphasis on the more comprehensive personal consumption expenditures price index.

Read more from The Japan News at https://japannews.yomiuri.co.jp/