The ongoing transformation of payment methods is set to alter the global economic landscape. As a country where cash is king, Japan has been conspicuously slow to begin the transition to cashless payments. Concerns have emerged that if the country continues to lag behind in embracing the cashless trend, it could miss out on growth opportunities.

Changes in developing countries

In a village in the southeast African nation of Mozambique, nearly 2,000 kilometers from the capital, the local way of life has changed. Kanagawa Prefecture-based startup Nippon Biodiesel Fuel Co. is producing biofuel using the seeds of a plant called jatropha, which it purchases from local residents.

The region is gaining increased access to electricity, while at stores in the village, residents are able to purchase daily necessities and agricultural items.

The most significant change of all has been the residents' newfound access to financial services. Farmers can put revenue generated from seed sales onto IC cards. The cards can then be used to pay for items purchased at stores in the village.

The practice of storing money by burying it in the ground has been replaced by a modern approach to savings. Now, even the time and effort associated with traveling to a town that has a bank to send money are unnecessary. Made possible by the IC cards distributed by Nippon Biodiesel Fuel, and by mobile phones, used by over 80 percent of the population, cashless payments are improving the standard of living in the country in the world's least developed category.

In Kenya, the scale of mobile device-based payments is thought to have reached 40 percent of the country's gross domestic product. This "leapfrogging" of payment methods could also provide a path to solving problems such as poverty.

Global economic impact

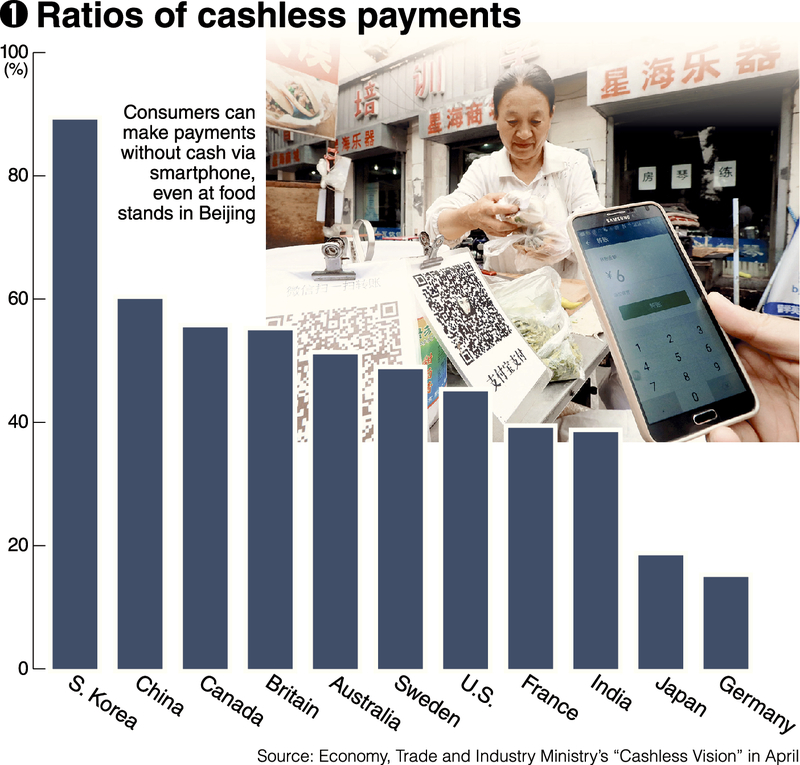

In many countries, the rate of cashless payments has surpassed 40 percent (see Chart 1).

Methods such as using a smartphone to read a QR code and pay on the spot directly from a bank account are now commonplace.

Sweden used the financial crisis of the 1990s as an opportunity to promote the transition to cashless transactions. Swish, a mobile payment system launched jointly by the country's major banks in 2012, has been adopted by 60 percent of the population.

A method of paying that features the use of a chip implanted in the user's hand is also coming into use.

Sweden is viewed as a model by those seeking to improve productivity and solve the problem of labor shortages through payment reform.

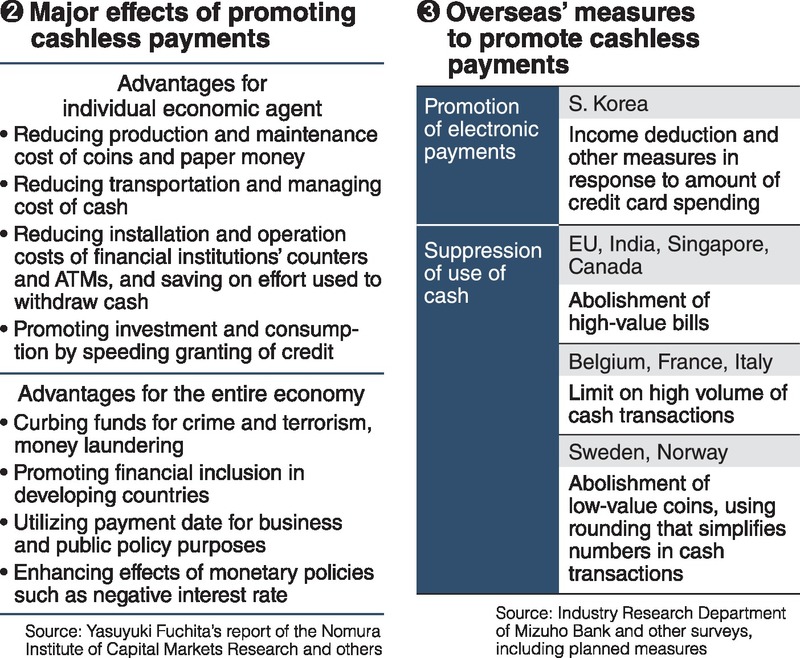

According to U.S.-based Moody's Analytics, the growth in the use of electronic payments from 2011 to 2015 boosted the world's GDP by 0.1 percent, and household spending by 0.4 percent. It also created an average of 2.6 million jobs per year over that span.

The economic impacts of the transition to cashless payments are wide-ranging (see Chart 2). There are costs associated with the transportation and management of cash. In Japan, the annual costs associated with the operation of automated teller machines and related matters have been estimated at 2 trillion yen. The logistics industry, which is facing a labor shortage, is another that can expect to optimize its operations.

The matter of cashless payments can also be understood in terms of its potential to increase the effectiveness of monetary policy. Even if a country's central bank introduces negative interest rates, if households and companies store cash away in the form of "under-the-mattress" deposits, the amount of money circulating on the street will not increase. The expectation of positive economic effects is driving the transition to cashless payments on two fronts: restraints on the use of cash, and the promotion of electronic payments. (see Chart 3).

A cash-first country

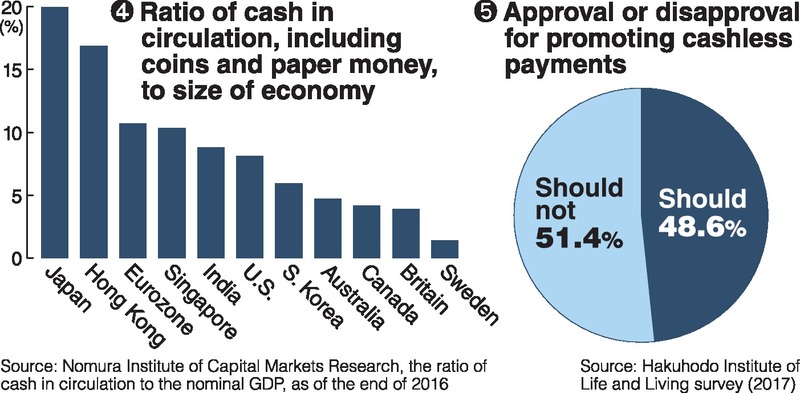

Japan's lagging start on the transition to cashless payments is also evidenced by its high ratio of cash in circulation to nominal GDP. (see Chart 4). Bank branches and ATMs stretch nationwide.

Japan's bank note printing technology is also outstanding. According to the country's National Printing Bureau, the rate of counterfeiting the euro as of 2012 was 223 times the level of the yen. The rate for the U.S. dollar is 659 times the level of the yen.

The Japanese public places great trust in paper money. The nation's preference for cash is deeply rooted. (see Chart 5). The transition to cashless payments is being hindered by the difficulty in personally experiencing the benefits.

The Japanese government has set the goal of increasing the cashless payment ratio to 40 percent by 2027. Forty percent of foreign visitors to Japan are dissatisfied with the country's excessive emphasis on cash. Estimates suggest that at the current rate -- should the number of tourists visiting the country in 2020 reach 40 million, as planned -- the lost opportunities would likely amount to 1.2 trillion yen.

Growth of Alipay

The scripted scenario in which the government's target is met has yet to be finalized.

Financial institutions and other companies are independently developing their own payment services. The unification of standards and other factors has stalled, and compatibility has suffered. The current state of affairs "will not lead to reduced costs for businesses or improved convenience for users. Rather, it will increase reliance on cash," notes Yasuyuki Fuchita of the Nomura Institute of Capital Markets Research.

Meanwhile, the rapid increase in the use of mobile payments in China is drawing attention. Alipay is a payment service from the Alibaba Group, which operates China's largest e-commerce website. About 40,000 businesses in Japan have adopted QR code-based Alipay payments as an option for visitors from China. This trend has also extended to rural areas, as well as medium, small and micro-enterprises.

With 520 million users in China, Alipay annually processes the equivalent to 187 trillion yen in payments. It has been adopted as a payment service for Chinese tourists and consumers in 38 countries and regions, including Japan. In seven countries and regions in Asia -- including India, Thailand, Malaysia and South Korea -- Alipay has the potential to become a "standard" capable of handling payments made in local currency to users' home areas.

The massive quantities of payment data processed by Alipay form the basis of the credit-scoring system (see below) administered by Alibaba affiliate Sesame Credit, or Zhima Credit. As a business that uses data as its resource, Sesame Credit has been able to keep its fees close to zero, allowing other businesses to introduce its services at minimal cost.

As Japan rushes to meet the needs of visitors, if the use of Alipay becomes more widespread, there might be calls to add Japanese customers to the service's target group.

However, the two countries have yet to agree on any clear-cut rules regarding the handling of data. In addition to Japanese companies lagging behind in launching projects involving the leveraging of data, "There are fears that the personal information of Japanese nationals could be captured in China," said Yukio Noguchi, professor emeritus at Hitotsubashi University.

Cashless payments are spreading as "a means of connecting billions of people, and of realizing financial inclusion," said Makoto Goda, president of Nippon Biodiesel Fuel. Momentum is also accelerating in Asia.

How can Japan maintain an appropriate distance from China, which is at the forefront of the movement? As the unification of domestic standards remains out of reach, new challenges are emerging.

--Credit score

A consumer's credit score is calculated on the basis of data, including their history of payments for public utilities and purchased goods, and their actions when using sharing services. Consumers who have attained high scores are not required to pay deposits when using services such as hotels and shared bicycles, and obtain beneficial loan conditions. The service's system of raising an individual's score in proportion to the quantity of information they provide is seen as a driving force behind its accumulation of data.

Read more from The Japan News at https://japannews.yomiuri.co.jp/