The Group of Seven (G7, see below) major industrialized nations, which includes Japan, the United States and European countries, has played a key role in maintaining global financial stability, as demonstrated in the autumn 2008 financial crisis when they came together to bring the situation under control. Now, U.S. President Donald Trump's remarks are causing repercussions in currency diplomacy among governments. In the event of a new crisis, will the world be able to deal with it?

Tacit deals

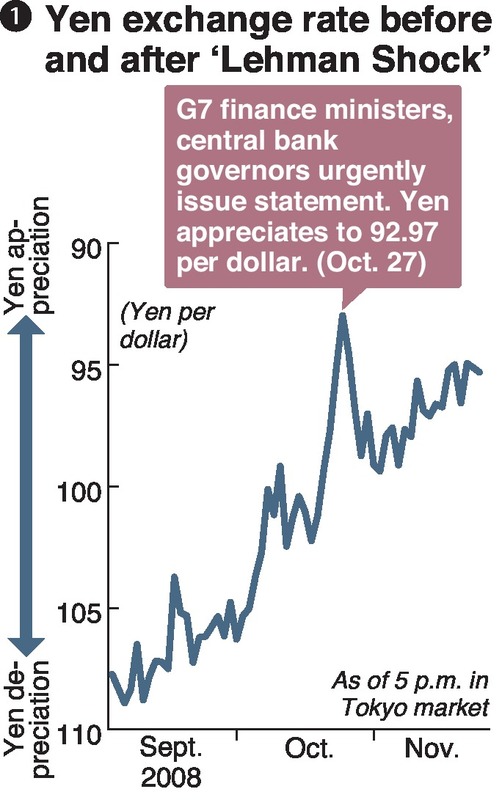

On Oct. 27, 2008, as the crisis triggered by the collapse of U.S. investment bank Lehman Brothers sent shock waves throughout the world, G7 finance ministers and central bank governors urgently issued a highly unusual statement.

"We are concerned about the recent excessive volatility in the exchange rate of the yen and its possible adverse implications for economic and financial stability," the statement said, specifically naming the yen to warn against its appreciation.

At the time, the yen was soaring against the dollar (see chart 1). Many traders were buying the Japanese currency -- considered a safe asset -- in a drastic move to avoid risk in the wake of the crisis. One dollar was worth over 100 yen in mid-October, but the yen surged as the dollar dropped to a little above 95 yen on Oct. 24. Later on the same day, European time, it plunged to slightly over 90 yen.

In currency diplomacy, a war of nerves is waged among nations to mutually curb currency depreciation, which makes a country's exports more competitive. Why did the G7 agree on the unique statement that would allow measures to bring down the soaring yen, including Tokyo's unilateral interventions in the currency market?

Naoyuki Shinohara tirelessly worked with U.S. and European authorities as vice finance minister for international affairs at the time. "There were an awful lot of arguments, but the United States persuaded Europe [on Japan's behalf] behind closed doors," he recalled.

Washington took such a move because it was indebted to Tokyo.

Deputies meetings are often the main stage for currency diplomacy where senior officials -- second to ministers -- hold discussions in preparation for ministerial meetings and clash with each other in pursuit of their national interests. Such meetings are sometimes simply called "D" meetings. In Japan's case, the vice finance minister for international affairs attends the meeting.

Among participants in G7 deputies meetings, unstated "debtor-creditor" relations take place, according to Shinohara. If one country helps out another in a pinch, it can expect to receive support in turn when their positions reverse.

Japan cooperated with the U.S. Treasury by providing support for U.S. financial institutions, including government-sponsored housing finance enterprises, which were in trouble in 2008. This subsequently worked as a "credit" for Japan, leading the G7 to share the view that an unrestrained rise of the yen could negatively affect the stability of the global economy and finance. Tokyo breathed a sigh of relief as the soaring yen was brought under control.

Tough battles

The G7 member states came together to tackle the financial crisis, even as their mutual maneuverings fiercely continued behind the scenes.

Serving as deputy assistant secretary at the U.S. Treasury from 2000-15, Mark Sobel was in charge of negotiations at finance ministers and central bank governors meetings of the G7 and the G20 economies. With a career spanning about 40 years, he is sometimes called a walking dictionary of the Treasury.

In a commentary to British independent think tank Official Monetary and Financial Institutions Forum (OMFIF) in May this year, Sobel explained the aims of the Treasury's traditional monetary policy. If the United States, Japan and European nations embrace the floating exchange rate system without intervening in the market and refrain from open-mouth operations, it would serve the U.S. national interest, he stressed.

Countries with a current account surplus are generally said to face upward pressure on their currencies. A country's current account is the sum of its international trade balance of goods and services, earnings on cross-border investments and other items. A country with a current account surplus receives a large amount of dollars. If these dollars are used by Japan, it is necessary to sell them for yen, which consequently increases the value of the yen.

Upholding a floating exchange rate system will lead to the appreciation of the currencies of current account surplus countries, thus stalling their exports and eventually rectifying imbalances. Through this process, Sobel said, other countries' excessive reliance on the United States as the engine for world economic growth can be avoided.

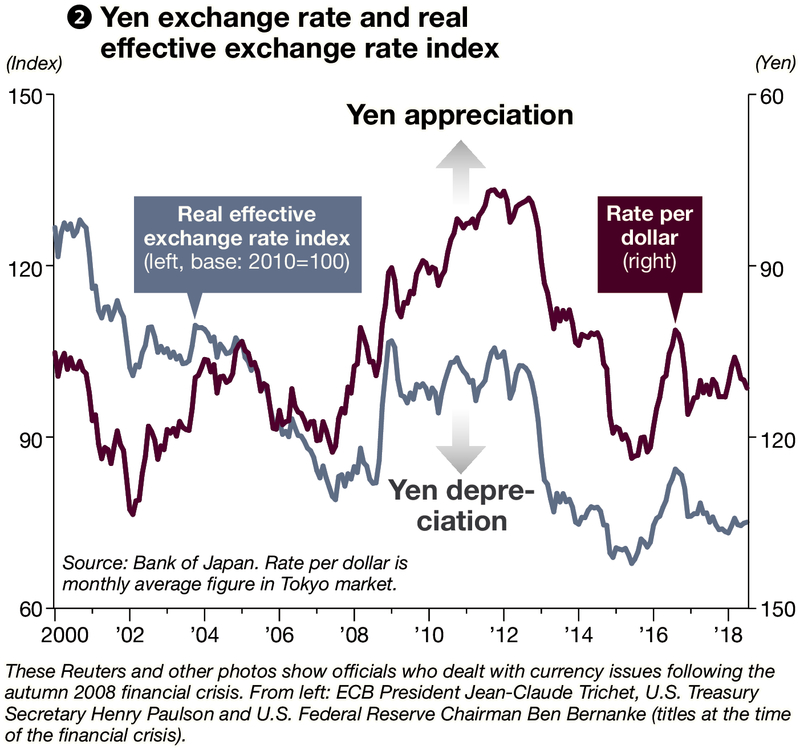

Based on this line of thinking, the Treasury's monetary policy is not easy on Japan, which has a large current account surplus. In the summer of 2007, Europeans pointed to Japan's large current account surplus and the yen's substantial undervaluation (see chart 2) based on the real effective exchange rate (see below) and pressed Tokyo hard behind the scenes to correct the undervaluation. The real effective exchange rate is an index often cited among officials.

French senior financial official Xavier Musca was particularly hard-line, according to Shinohara. Musca "repeatedly asked me to express concern over the excessive depreciation of the yen," the former Japanese official recalled. Shinohara deflected the French official's pressure by denying any yen depreciation efforts.

Building trust

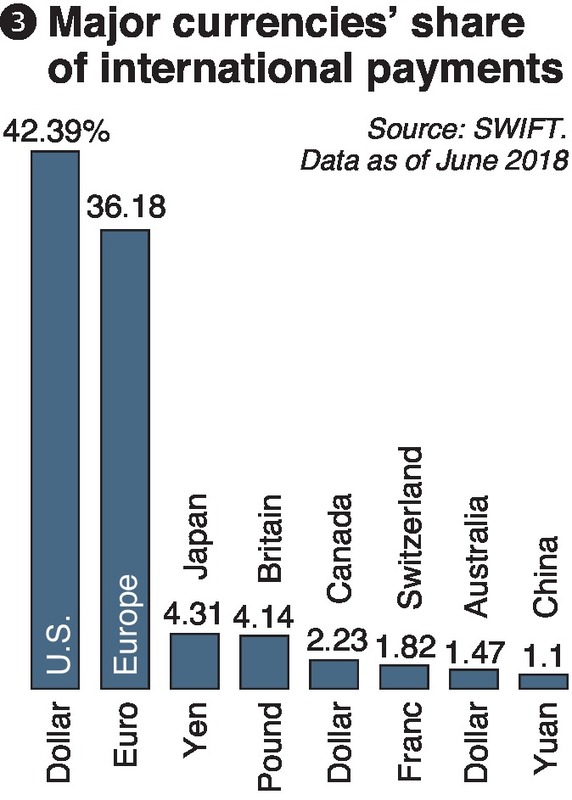

While nations wage diplomatic battles behind the scenes over currencies, this process builds up mutual trust among relevant officials -- a shared infrastructure that underpins global financial stability. China has been rising, but the dollar, euro and yen are still the dominant currencies for international payments, according to the Society for Worldwide Interbank Financial Telecommunication (SWIFT, see chart 3). The G7's role in international finance remains large.

Since 2009, the G20, which includes emerging economies such as China, has become a major stage for economic talks. Sobel recently replied to a query by The Yomiuri Shimbun about the significance of the G7. The G7 "can be an important informal body on many global issues, including currency if needed," he said.

As an example, the former U.S. official cited the G7's coordinated intervention on March 18, 2011, in the wake of the Great East Japan Earthquake, the first such intervention in about 10-1/2 years.

"Enormous energy was put into it," said Rintaro Tamaki, then vice finance minister for international affairs, recalling the coordination between G7 nations. The member states shared the view that the sudden rise of the yen was a disorderly movement. Jean-Claude Trichet, then president of the European Central Bank -- which is responsible for currency intervention in the eurozone -- phoned central bank governors of ECB nations one by one to persuade them, according to Tamaki.

The G7 summit in June this year faced divisions among its members in relation to trade frictions, but close ties among relevant finance officials remain strong, a senior Finance Ministry official said.

Trump and senior U.S. officials have repeatedly resorted to verbal interventions to warn against the undervaluation of other countries' currencies, marking a departure from Washington's traditional monetary policy. But this has not resulted in currency wars right away. With an eye on the next crisis, we must not break the close ties between G7 officials.

-- G7

The Group of Seven advanced nations -- Japan, Britain, Canada, France, Germany, Italy and the United States. It provides a framework for discussing economic and other issues, holding such events as summit meetings attended by presidents and prime ministers, as well as meetings of finance ministers and central bank governors. In the 1970s, closer policy coordination was called for among advanced nations as they faced such issues as the first oil crisis, and the first summit was convened in Rambouillet, France, in 1975 in response to an overture by the French president. The summit was attended by the leaders of six countries -- Japan, Britain, France, Italy, the United States and West Germany. Canada joined the group the following year.

-- Real effective exchange rate

An index showing a currency's strength against a basket of other currencies, rather than measuring its value by comparing it with a single currency, for example the yen against the dollar. The rate is calculated based on trade volumes with other countries and also adjusted for inflation. For the currencies of countries such as Japan with continuing deflation, this index figure tends to move lower.

Read more from The Japan News at https://japannews.yomiuri.co.jp/