Here’s our update on the latest developments at Volkswagen, by Graham Ruddick:

The new chief executive of Volkswagen has warned the carmaker’s staff that the fallout from the diesel emissions scandal “won’t be painless” and that the company needs to make “massive savings” as it faces the prospect of a multibillion-euro bill.

Matthias Müller told a gathering of 20,000 workers at VW’s headquarters in Wolfsburg that “every euro that stays in the company helps us”.

The comments underline the pressure on VW’s finances for the first time since the carmaker revealed two and a half weeks ago that it had installed defeat devices to cheat official emissions tests.

The company has since admitted that it fitted up to 11m vehicles worldwide with the rogue software and has put aside €6.5bn (£4.8bn) to meet the cost of recalling the cars and fixing them so they meet environmental standards. However, it also faces a fine of up to $18bn (£11.9bn) from US regulators as well as legal claims from customers and shareholders.

“It [the €6.5bn] includes the estimated cost to fix the affected vehicles. But it won’t be enough,” Müller said. “We must prepare for significant penalties, and many could take the events as an opportunity to claim damages against Volkswagen.

{Indeed Societe Generale has said the company’s liabilities could total €32bn.]

Here’s our full story:

And on that note, it’s time to close up for the evening. Thanks for all your comments, and we’ll be back tomorrow.

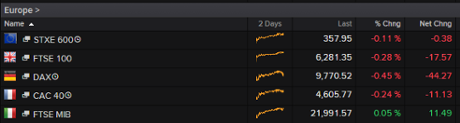

European markets close higher again, oil jumps

Investors have shrugged off the IMF’s latest cut to its global growth forecasts, concentrating instead on the prospect for central banks to continue supporting the global economy and the world’s stock markets. Friday’s poor US jobs numbers continue to convince traders that the Federal Reserve is now less likely to raise interest rates this year. On top of that there are hopes for further stimulus measures from China and the European Central Bank.

Meanwhile energy shares have been lifted by a jump in the oil price after the US cut its output forecasts and suggested that production from non-Opec members was stalling. Opec itself said the organisation and non-members should work together to reduce the global oversupply of oil.

So Brent crude has climbed 4.5% to $51.5, its highest level since the end of August.

As for stock markets, the final scores showed:

- The FTSE 100 finished 27.24 points or 0.43% higher at 6426.16

- Germany’s Dax is up 0.9% at 9902.83

- France’s Cac closed 0.95% better at 4660.64

- Italy’s FTSE MIB added 0.92% to 22,182.65

- Spain’s Ibex ended up 1.32% at 10,103.3

- In Greece the Athens market was 0.54% higher at 670.69

On Wall Street, the Dow Jones Industrial Average is currently flat, up just 3.5 points.

Here’s an interesting chart from the IMF’s world economic outlook, spotted by RBS:

Productivity has been growing slower in all advanced economies after 2008 than before. Apart from one country. #IMF pic.twitter.com/VwqmMU82RZ

— RBS Economics (@RBS_Economics) October 6, 2015

A downturn in emerging markets in September led global economic growth lower, according to a new survey.

The JPMorgan Global PMI, compiled by Markit, fell from 53.9 in August to 52.8 in September, its weakest for nine months and signalling a rate of worldwide GDP growth of just 2% per annum. Markit said:

The divergence between developed and emerging markets widened to the greatest on record over the third quarter. At 49.0 in September, the emerging market PMI fell to its lowest since March 2009, indicating a deterioration in business conditions across manufacturing and services for the third time in the past four months.

The developed world PMI meanwhile also fell but, at 54.0 (down from 55.1 in August), remained in expansion territory.

The developed world PMI is signalling a 1.5% annual GDP expansion, while the emerging market equivalent is broadly consistent with 3% growth.

The emerging market downturn was led by manufacturing, where the PMI has signalled contraction for five successive months, with the rate of decline accelerating in September. However, services also slipped into contraction, suggesting the industrial malaise is spreading to other parts of the emerging market economies.

Global trade fell at fastest rate for 27 months in Sept. Emerging market exports saw largest fall since March 2009 pic.twitter.com/M1opIu2LuT

— Chris Williamson (@WilliamsonChris) October 6, 2015

Wall Street higher in early trading

The Dow Jones Industrial Average has continued its recent buoyant mood, adding more than 70 points or 0.4% in early trading.

European markets, which have been having an uncertain day up until now, are also in positive territory. The FTSE 100 is currently 0.6% higher while Germany’s Dax is up 1%.

Meanwhile oil continues to climb, with Brent crude now 2.5% better at $50.51 a barrel.

Talk that producers might work together to deal with the issue of oversupply had already lifted crude out of the doldrums, and it has now been helped by the US Energy Information Administration forecasting that US crude output would fall between now and mid-2016. The EIA also raised its 2016 forecast for world oil demand by 100,000 barrels a day to 1.41m.

IMF cuts global growth forecasts again

Ahead of its annual meeting, the International Monetary Fund has cut its global growth forecasts for 2015:

[The IMF] is warning that the weak recovery in the west risks turning into near stagnation after cutting its global economic growth forecast for the fourth successive year.

In its half-yearly update on the health of the world economy, the Washington-based fund predicted expansion of 3.1% in 2015, 0.2 points lower than it was expecting three months ago and the weakest performance since the trough of the downturn in 2009.

“Six years after the world economy emerged from its broadest and deepest postwar recession, a return to robust and synchronised global expansion remains elusive,” said Maurice Obstfeld, the IMF’s economic counsellor...

The IMF’s world economic outlook (WEO) predicted the US would have the strongest growth of the leading G7 industrial nations in both 2015 and 2016, at 2.6% and 2.8%, respectively. Britain is expected to be the second-fastest growing G7 nation, although output growth is predicted to slow from 2.5% to 2.2%.

None of the other G7 countries – Germany, France, Italy, Japan and Canada – is predicted to post growth as high as 2% in either 2015 or 2016.

Full story here:

And here is Larry’s analysis:

Spain was warned about its budget submission after the Eurogroup meeting on Monday, but it appears the warning will not be adopted by the European Commission:

Very very surprising. EC's is not adopting today its opinion on the Spanish budget 2016, as announced yesterday by @pierremoscovici

— María Tejero Martín (@Maria_Tejero) October 6, 2015

Moscovici was quite hard on Spain on his press conf. Schäuble has said today that he was "surprised" about Moscovici's critical remarks

— María Tejero Martín (@Maria_Tejero) October 6, 2015

Oil prices have reversed their earlier losses, with Brent crude now up 1% at $49.79 a barrel, after Opec said it saw the market improving due to higher demand and a drop in supply from non-members.

Oil prices have been under pressure amid falling demand amid weak economic growth, and increased production leading to a supply glut.

But Opec’s general secretary Abdullah al-Badri told reporters at an industry conference in London that the market was improving, although it could take two years to rebalance, according to Reuters.

Opec has been firm in not cutting production to prop up prices, instead concentrating on protecting its market share.

He told the conference there was an overhang of 200m barrels, and Opec members and non-Opec members alike should work together to address the issue. With falling investment from oil companies, he expected prices to rise in the next few months.

Russia and Saudi Arabia have already held talks on the oil market last week and plan to continue consulting each other.

Updated

Global stock markets have been volatile in recent weeks, largely on concerns about a slowdown in China and the knock on effect on commodity prices. But the risks from China are less than many imagine, according to Capital Economics. The research company’s Andrew Kenningham said:

Although China’s growth has slowed sharply in recent years, we do not expect a “hard landing”. What’s more, even if we turn out to be wrong, some emerging economies would be hit hard by a slump in China, but the impact on advanced economies should generally be modest.

GDP growth in China has already slowed from double-digit levels before 2008 to around 5% this year, according to our in-house estimates. However, it has been relatively stable over the past six months, when a slump in its equity market has triggered falls in global asset prices. Looking ahead, we think China will regain some momentum, helped by the policy support now in the pipeline.

If China’s economy weakens much further, global growth would also slow. Growth of 2% rather than 6% in China would directly reduce world GDP growth by nearly one percentage point. Along with the knock-on effects elsewhere, global growth could fall from around 31⁄2% to just over 2% for a year or two. Industrial metal producers such as Australia and Chile could be hard hit. But the impact on the major advanced economies, including the US and euro-zone, would be much smaller.

Finally, there would be some offsetting advantages for the rest of the world from slower growth in China. Most importantly, although any further fall in commodity prices would hurt commodity producers, it should be a net positive for the world as a whole. Overall, therefore, while a slump in China would clearly dampen global growth, it would not be the catastrophe that many fear.

The European parliament has approved plans to speed up a €35bn funding programme for Greece earmarked in the EU’s 2014-2020 budget.

Commenting on today’s vote in favour, the European Commission said:

The aim is to allow Greece to make full use of EU funds and inject liquidity into the Greek economy.

Valdis Dombrovskis, vice-president for the euro and social dialogue, said:

I welcome today’s vote in the European Parliament giving its green light to frontloading existing EU funds for investment in growth-enhancing projects in Greece.... It should be seen in a wider context of the reform process undertaken in Greece. Timely and effective implementation of reforms to modernise Greek public administration and the economy – as agreed under the new stability support programme – is crucial to regain financial stability and, consequently, ensure economic growth and job creation.

Updated

America’s trade gap has hit a five-month high, in another sign that global economic growth may be weakening.

US imports rose by 1.2% in August, fuelled by a 3% increased in purchases from China.

But exports shrank by 2%, to their lowest point since October 2012. That indicates weakness in key markets such as emerging nations and Europe. It could also reflect the impact of the stronger US dollar, which has gained against other currencies.

This drove the US Trade Deficit up to $48.33bn in August, up from $41.81bn a year ago.

US trade deficit jumps 15.6% to $48.3 billion in August as exports fall to 3-year low - @AP

— Breaking News Money (@breakingmoney) October 6, 2015

The VW scandal hasn’t hurt the UK auto industry yet - car sales hit an all-time high in September, according to new data today.

Petrol-powered cars saw the strongest demand; suggesting some consumers might be more wary about diesel now.

Updated

Volkswagen boss: Painful changes are ahead

Workers at Volkswagen have been warned to expect painful changes as the German carmaker tackles the emissions scandal.

New CEO Matthias Müller told staff that non-essential investments will be delayed or abandoned as it wrestles with the crisis.

Müller told today’s meeting in Wolfsburg that:

“Technical solutions to the problems are within view. However, the business and financial consequences are not yet clear”.

“Therefore we are putting all planned investments under review. What is not urgently needed will be scrapped or delayed”.

“And therefore we will adjust our efficiency programme. I will be very open: this won’t be painless.”

Muller’s warning came after works council boss Bernd Osterloh predicted that bonus payments to workers are now at risk too.

Updated

Our Katie Allen confirms that Britain’s directors do not march on an empty stomach, or an environmentally friendly one....

all for free lunches but in week we tried to kill off plastic bags, is it time for sun to set on #IoDAC lunchbox? pic.twitter.com/vBKJnm8guV

— Katie Allen (@KatieAllenGdn) October 6, 2015

Update: IoD delegates have now plonked themselves outside in the sun -- making a nice photo for visiting tourists.

The annual Albert memorial picnic at the IoD convention has attracted the attention of tourists #IoDAC pic.twitter.com/dCTqd1x4wb

— Katie Allen (@KatieAllenGdn) October 6, 2015

Updated

Delegates at the Institute of Directors’ conference are tucking into their legendary lunchboxes -- a chance to refuel after a morning discussing weighty topics like Europe and migration.

There’s an astonishing amount of packaging on display too -- here’s a photo of just one box:

Genius conference chow!! Lunch boxes @TheIoD #IoDAC #eventplanning pic.twitter.com/gjf210s64k

— Cheryl Chickowski (@Chicch) October 6, 2015

Perhaps Britain’s new tax on plastic bags should be extended? £10 per plastic lid might cover it....

Here’s a couple of photos of Volkswagen staff arriving in Wolfsburg, where they were briefed on the emissions crisis today:

Brewing firm SABMiller has turned down an ‘informal offer’ from rival Anheuser-Busch InBev, according to a Bloomberg newsflash.

That’s sent SAB’s shares down 3%, to the bottom of the FTSE 100 (budge up, Glencore!).

This come three weeks after AB INBev, which brews Stella Artois and Budweiser, approached SAB, whose brands including Grolsch and Peroni.

Any deal would be huge, creating a new company worth perhaps $250bn (£160bn).

AB InBev has just a week to make a firm bid or walk away, so it’s not Last Orders in this story, yet.

SABMiller diving on reports it's knocked back an informal takeover offer from ABInBev http://t.co/2TQcKrMFt4 pic.twitter.com/HOsVGt5Wnv

— Oscar Williams-Grut (@OscarWGrut) October 6, 2015

The works council boss at Volkswagen, Bernd Osterloh, has told staff that the company will have to review all its investments following the emissions crisis.

He also predicted that their pay packets will suffer too.

Osterloh gave the warning at today’s staff meeting in Wolfsburg (see earlier post)

Reuters has the story:

All investments at Volkswagen will be placed under review, the carmaker’s top labour representative said on Tuesday, as the embattled German group grapples with the fallout of its diesel emissions scandal.

“We will need to call into question with great resolve everything that is not economical,” Bernd Osterloh, head of VW’s works council told more than 20,000 workers at a staff gathering in Wolfsburg, Germany.

The scandal is not yet having consequences for jobs at VW, which employs 60,000 people at its main factory, but will impact earnings at the core autos division as well as bonus payments to workers, Osterloh said.

VW: eight million cars sold in EU with cheat software

Volkswagen has revealed that it sold eight million cars with defective emissions testing software across Europe.

It made the admission in a letter to German MPs, dated last Friday.

That’s the bulk of the 11 million cars affected, including almost 500,000 in the US.

We already know that 1.2m cars sold in the UK contained software to beat emission tests, plus 2.8m in Germany.

Updated

Looks like Lord Lawson got the last blow in:

Mandelson summing up in EU debate with Lawson at IoD: EU makes us stronger, better off and safer #IoDAC

— Katie Allen (@KatieAllenGdn) October 6, 2015

Lawson closing EU ref debate: Mandelson was wrong "time and time again" about joining euro - "he was wrong then, he is wrong now" #IoDAC

— Katie Allen (@KatieAllenGdn) October 6, 2015

They’re still arguing...

Mandelson to Lawson: "Nigel, go to Norway, go to Switzerland" see that in trading with EU they must enforce "every dot & comma" of Europ reg

— Katie Allen (@KatieAllenGdn) October 6, 2015

Lawson and Mandelson on Europe

Back at the IoD conference, Nigel Lawson and Peter Mandelson are having a brisk exchange of views over Britain’s membership of the EU (Lord M is pro, Lord L is con).

Katie Allen is impartial, and tweeting the key points from the Albert Hall:

Lord Lawson tells IoD: there may be reasons why Britain should remain in the EU but they are not economic. #IoDAC

— Katie Allen (@KatieAllenGdn) October 6, 2015

Lawson at IoD convention says: More Europe means too often more European regulation and that EU is "project of the elites of Europe" #IoDAC

— Katie Allen (@KatieAllenGdn) October 6, 2015

Peter Mandelson tells #IoDAC convention "EU tries to do too much. It has to do less better." But ppl must ask what alternatives are for UK

— Katie Allen (@KatieAllenGdn) October 6, 2015

Mandelson on Brexit: UK would be "notionally more independent if we came out but more isolated and less influential as a result." #IoDAC

— Katie Allen (@KatieAllenGdn) October 6, 2015

Mining shares are leading the fallers in London this morning.

The 1.8% drop in German factory orders in August isn’t helping the mood.

Investors are concerned that falling demand from emerging markets could increase the raw materials glut, which has already driven commodity price down to multi-year lows.

Slump in commodities may last for years, banks warn http://t.co/SelpXFav29 pic.twitter.com/xoqDeN56xP

— Bloomberg Business (@business) October 6, 2015

Updated

The Institute of Directors’ chief is also rebuking UK politicians for playing the migrants card:

Simon Walker @The_IoD repeats criticism of main parties for "pandering to myths about immigration" when growing economy, NHS need migrants

— Katie Allen (@KatieAllenGdn) October 6, 2015

Business leaders demand early EU referendum

Over at London’s Royal Albert Hall, business leaders are gathering for the annual Institute of Directors convention.

The 2,000 or so delegates will be hearing first from IoD head Simon Walker. As we reported this morning, Walker will use his speech to warn prime minister David Cameron that waiting till 2017 to hold the referendum on EU membership risks turning it into a confidence vote in the government.

He wants the referendum brought forward to 2016.

Walker will tell the audience that:

“By 2017 this government will have implemented spending cuts that, while necessary, will not be popular. The third year of an election cycle is a difficult time for any administration. There is a real possibility that a 2017 referendum would be a short-term judgment on the government: a chance to whack the political elite.”

Next up, just after 10am is a debate on Britain’s EU membership between former Labour business secretary Lord Mandelson and former chancellor Lord Lawson, who last week announced he will lead a Conservative party campaign to leave the EU.

Also making an appearance, is chief executive of Lloyds Banking Group, Antonio Horta-Osorio, just a day after chancellor George Osborne announced the sale of the taxpayers’ remaining stake in the bailed out bank. The bank boss is talking on a panel under the banner “The future of banking: How to win back trust in a changing world.”

Alongside its trailing of Walker’s EU referendum thoughts, the IoD is also using its convention to adds its thoughts to the never-ending UK productivity puzzle debate.

Policymakers are looking at the puzzle all wrong, according to the business group’s new report, Balancing UK Productivity and Agility. It wants more focus on “agility” to ensure “new ideas and technologies spread throughout the economy as quickly as possible”.

It warns factors that have driven productivity gains in the past, such as large firms realising economies of scale and developing deep specialisations in certain areas, are no longer relevant for the UK and “it would be foolish to try to recreate them”.

IoD chief economist James Sproule explains:

“In pursuing the nirvana of steadily-rising productivity, one has to bear in mind how our economy is changing, how people choose to work, and what future economic success will look like.

We need to ask if too close a focus on productivity numbers without considering wider factors could pose a long-term risk to the economy and prosperity.”

His report echoes scepticism over how much can be gleaned from current productivity data and what many economists see as a narrow focus on mere output per hour measures.

Here we go then – attendees seated and ready. Let’s get this convention started! #IoDAC pic.twitter.com/mVaGPfIL0o

— IoD (@The_IoD) October 6, 2015

Updated

Back in the UK, house prices dipped by 0.9% last month, according to mortgage lender Halifax.

But that’s little relief to those hoping to get a house (or buy a bigger one. Prices are up around 8.9% year-on-year. On a quarter-on-quarter basis, they’ve been gaining since the start of 2013.

In September last year the average UK home was worth £187k according to Halifax. This September it was £203k. pic.twitter.com/8RkYjJ1u72

— RBS Economics (@RBS_Economics) October 6, 2015

Interesting.... Jonathan Portes, one of the UK’s better known economists, has left his post as director of the National Institute of Economic and Social Research thinktank.

There doesn’t appear to be an official announcement, but NIESR has updated its website to show that Dame Frances Cairncross is now ‘interim director’.

Portes (who’s staying at NIESR as a research fellow until April) is known for using his statistical nous to fact-checking erroneous claims in the papers, especially over the impact of fiscal policy on poorer households.

But he also raised hackles among right wingers for his comments on austerity; they claimed loudly that Portes (once PM Gordon Brown’s chief economist) was too partisan for an independent thinktank:

So farewell, then, Jonathan Portes: he has left NIESR ‘by mutual consent’. @steerpike has details: http://t.co/hRq8H8khgJ

— Fraser Nelson (@FraserNelson) October 6, 2015

Those spats culminated in an epic row with historian Niall Ferguson over an article in the Financial Times, which spawned an 16-page adjudication - and no clear winner (although the FT cleared itself of any failings, of course)

Updated

Over in Wolfsburg, thousands of Volkswagen employees are meeting at company HQ to hear from their new CEO.

Matthias Müller will brief staff on the ongoing emissions scandal, as Volkswagen strives to find a solution after selling millions of vehicles containing ‘defeat devices’ to fool emissions tests.

Müller was appointed as CEO less than two weeks ago, after Martin Winterkorn stepped down following the revelations that VW engines contained illicit software to hide how much noxious gases they produced.

It emerged last night that the probe into the VW scandal centres on two top engineers. Ulrich Hackenberg, Audi’s chief engineer, and Wolfgang Hatz, developer of Porsche’s Formula One and Le Mans racing engines, were among the engineers suspended last week, according to the WSJ.

European stock markets are being dragged down by the news that German factory orders slid in August.

The main indices are all in the red in early trading, with Germany’s DAX shedding almost 0.5%.

Investors may also be anxious about the eurozone, after Brussels warned Spain last night that i’s 2016 budget isn’t good enough, and needs more spending cuts.

Conner Campbell of SpreadEx explains:

A huge miss in German factory orders (complete with a downward revision for last month’s figure) seems to have taken the edge off of the Eurozone, following a Eurogroup meeting yesterday that hinted at more trouble for the currency union going forwards.

European Commissioner Pierre Moscovici warned that Spain will miss its headline targets in 2015 and 2016, providing yet another bearish note from the country that already includes a 21 month low manufacturing figure, a 9 month low services PMI, a separatist victory in Catalonia AND an impending general election in September.

German economy minister: Global demand is 'less reliable'

Here’s Associated Press’s early take on the decline in German factory orders:

German factory orders dropped for the second consecutive month in August, led by a drop in demand from countries outside the eurozone and lower demand at home.

The Economy Ministry said Tuesday that orders were down 1.8% in seasonally adjusted terms compared with the previous month. That followed a 2.2% drop in July.

Orders from other countries in the euro area were up 2.5%, following a smaller gain in July. However, demand from inside Germany was off 2.6% percent and orders from outside the eurozone dropped 3.7%.

The Economy Ministry noted that demand from countries beyond the euro area appears to be “less reliable at present.”

Germany has Europe’s biggest economy and is one of the world’s biggest exporters.

Updated

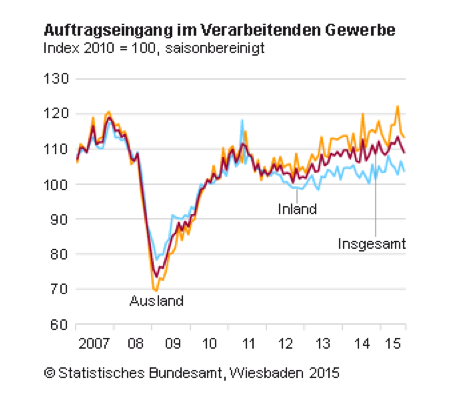

This chart confirms that German industrial orders have tailed off in the last couple of months, after a decent start to the year.

The red line shows the total (or Insgesamt), while the blue line shows domestic orders (Inland) and the yellow line shows overseas orders (Ausland).

German factories suffer sliding orders

German factory orders fell unexpectedly in August, fuelling fears that Europe’s largest economy is being hit by slowing global growth.

Industrial orders slid by 1.8%, according to the economy ministry, dashing expectations of a 0.5% rise.

The decline was mainly due to falling demand from outside the eurozone, according to the ministry (which also attribute some of the decline to holidays). Orders from non-euro countries slid by 3.7%, while domestic orders shrank by 2.6%.

This is before the Volkswagen emissions scandal struck, hurting confidence in German industry.

Ugly German factory orders...August slump -1.8% & July fall revised down further. Shows exposure to weak China. Eurozone a bright spot

— Caroline Hyde (@CarolineHydeTV) October 6, 2015

July’s industrial orders has been revised down too, from -1.4% to -2.2%; again, driven by a decline in overseas demand.

In July foreign German factory orders slumped 6.1%...not quite so bad in August, but domestic demand worsening amid holidays

— Caroline Hyde (@CarolineHydeTV) October 6, 2015

It’s a worrying sign, suggesting ripples from the emerging market slowdown are now lapping against the eurozone.

Updated

The Agenda: Stimulus hopes keep markets buoyant

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

There’s a relaxed mood in the markets this morning, as investors become increasingly convinced that central banks won’t be able to tighten monetary policy anytime soon.

European stock markets are expected to inch higher after the Dow Jones industrial average jumped by 304 points overnight.

Last Friday’s disappointing US jobs report has probably helped to kick the first American interest rate rise into 2016.

Modest continued rally expected at European opening - FTSe +27, DAX +45, CAC +22 (courtesy of IG)

— David Buik (@truemagic68) October 6, 2015

Jasper Lawler of CMC Markets explains:

The weaker than expected US jobs report significantly reduces the chance of a rate hike this year from the Federal Reserve.

Europe and China could also be on the verge of adding stimulus with deflation and low growth possibly enough motivation for the respective central banks to intervene before the end of 2015.

Over in Japan, the Nikkei has closed 1% higher, as traders in Tokyo anticipate more stimulus from their own central bank.

#Japan's Nikkei ends up 1% at 18186.10 on the prospect that the BoJ may need to ease again. http://t.co/zmeGKcNyoO pic.twitter.com/CvF2WUEByg

— Holger Zschaepitz (@Schuldensuehner) October 6, 2015

Also coming up....

The bosses of Britain’s top companies will be gathering at the Institute of Director’s annual bash in London. They’ll be discussing Europe and the refugee crisis (among other topics).

It’s #IoDAC day!! Looking forward to seeing everyone later today at the @RoyalAlbertHall! pic.twitter.com/Qk5LiJ0Fai

— IoD (@The_IoD) October 6, 2015

Six former City brokers are going on trial over allegation that they rigged the benchmark Libor interest rate.

And in the City, we’ll be looking at results from budget airline easyJet and pastry purveyor Greggs.....

Updated