PS: a mini closing market report, courtesy of Chris Beauchamp, Market Analyst, IG:

Oil firms and associated companies are once again populating the bottom of the FTSE 100’s scoreboard as Brent drops below $80 for the first time in over four years.

A hefty day of UK earnings means that the broader index is still posting good gains, helped along by the likes of ITV and the LSE, rising after decent figures this morning. Hopes of Chinese stimulus following underwhelming data this morning look a bit far-fetched, but with a paucity of real data it looks like the market is pleased to believe in the idea for the time being. US indices continue to provide strength from which the UK and Europe can draw to gain further ground, although the DAX’s drop below 9300 will have a few traders fretting that divergences between the economies of the eurozone and the US will continue to make themselves felt.

Even so, a few calming words from Mario Draghi could easily allow Europe to make up the gap, as we continue to await an early Christmas present from the ECB.

And here’s the situation across Europe:

Early finish today, as tomorrow’s going to be busy -- growth figures for much of the eurozone are released in the morning.

We’re about to find out if Germany is in recession, and if the wider European economy stagnated..... See you in the morning....GW

That increase in Americans resigning their jobs may herald a pick-up in earnings...

Think quitters never win? Not so in the labor market...rising "quits" often foreshadow mounting wage pressures. pic.twitter.com/uodA3uvIC5

— Carl Riccadonna (@Riccanomix) November 13, 2014

America’s employment market continues to improve, according to the latest US labour force data.

The number of job hires jumped to a six-year high of five million in September, with the job hire rate hitting 3.6%, up from 3.3% in August.

And the percentage of people quitting their jobs hit a six-year high of 2.0%, up from 1.8% in August.

"Take This Job and Shove It" index at cycle highs pic.twitter.com/EZXgCk7Sb2

— Ed Bradford (@Fullcarry) November 13, 2014

Last month, 2.8 million people quit a job, the most since April 2008. http://t.co/dWDdYSljXk pic.twitter.com/3kybcNEinz

— Real Time Economics (@WSJecon) November 13, 2014

ECB governing council member Sabine Lautenschlaeger didn’t really cause a stir in Stockholm today, despite speculation that she might criticise calls for more stimulus measures.

Instead, the German central banker announced that the ECB has received capital-raising plans from the banks which failed its stress tests last month.

We have received these plans ...on Nov 10, and are now in the process of thoroughly checking them with the aim to provide banks with an assessment before the end of the year”,

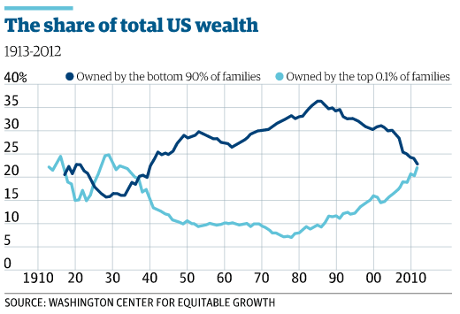

Interested in inequality? Check out this piece by my colleague Angela Monaghan on how American wealth has become increasingly concentrated in the hands of, well, a handful of ultra-rich:

Wealth inequality in the US is at near record levels according to a new study by academics. Over the past three decades, the share of household wealth owned by the top 0.1% has increased from 7% to 22%.

For the bottom 90% of families, a combination of rising debt, the collapse of the value of their assets during the financial crisis, and stagnant real wages have led to the erosion of wealth.

Full piece: US wealth inequality - top 0.1% worth as much as the bottom 90%

Afternoon reading: The FX affair

Financial experts have been digesting the huge fines handed down yesterday to banks who didn’t prevent their traders manipulating the foreign exchange market.

And two camps are emerging. One, led by veteran City analyst David Buik, are aghast that Forex traders were illicitly sharing information to make profits, often at their own clients expense.

Buik, who has been working in the markets for 52 years, says Thursday was the saddest day of his career. He writes:

Any thought of a quick return of respect and trust towards the financial sector has been blown out of the water by a small collection of mindless, greedy, selfish and arrogant congenital idiots.

He’s now reached the conclusion that fining banks simply doesn’t work -- as my colleague Nils Pratley also argued last night.

The forex scandal proves fines don’t deter bad banks. So ban them from trading

However, former stock broker Dan Davies has written a fascinating piece explaining the underlying story in the FX market, using the example of buying and selling oranges.

ON MONDAY: You are on your way to the fruit market, because you want to buy five oranges. Someone you’ve never met before accosts you on your way and says “Hey, you! Could you buy me five oranges please? I’ll give you the money when you come back and pay you ten pence for doing it”. You think what the hell, and say yes.

Down at the market, there is one stall which has five oranges for sale at 50p each, and another stall with five oranges for sale but charging 55p each. You buy ten oranges and head back home.

Your customer is waiting back at your gate. He gives you your ten pence, and asks “How much did my oranges cost?” What do you tell him?

By Friday, you’re in quite a pickle....Oranges, lemons and forex

And Bloomberg columnist Matt Levine has a fine explanation of why FX traders were sharing information and the limited power it gave them, (not that it makes it right!):

These guys really were cheating. By knowing in advance what their buddies were doing, by concentrating orders in one set of hands, by feeling out the non-chat-room banks, the traders in their chat rooms did get an unfair advantage that allowed them to feel comfortable trading in inefficient ways that did push the price around more than pure supply and demand would dictate.

But this isn’t Libor manipulation, where they just made stuff up.

This is tinkering at the edges of real supply and demand. And it helps to explain why their profits seem to have been relatively modest and inconsistent. There was only so much they could do. And sometimes they just got it wrong.

Banks Manipulated Foreign Exchange in Ways You Can’t Teach.

Updated

Just in -- the number of Americans signing on for jobless benefit jumped by 12,000 last week, to 290,000.

Economists had only expected a 2,000 rise.

BREAKING: Jobless claims hit 290,000 vs. 280,000 estimate. http://t.co/dbcoqEA2Oo pic.twitter.com/F7aDXaLDzI

— CNBC (@CNBC) November 13, 2014

The oil price is hitting new four-year lows, with Brent crude now down to $78.71 per barrel.

That’s a drop of over $1.50, or 2%, today, amid talk of the oil market being flooded with supplies.

Oil company share prices are being hit -- Royal Dutch Shell are down 2% in London, and Tullow Oil has shed 3.6%.

Updated

Quick tweak: Berkshire Hathaway are paying $4.7bn in P&G’s own shares for Duracell, which will be recapitalised with $1.7bn of cash from P&G before being sold to Warren Buffett.

So there’s $6.4bn sloshing around here, but I think effectively P&G will be $3bn better off in return for selling their battery business.

Updated

Berkshire Hathaway to buy Duracell

The Duracell Bunny is moving to a new warren, literally.

Berkshire Hathaway, the group run by veteran investor Warren Buffett, has just announced it is acquiring the Duracell Battery Business from Procter & Gamble.

84-year old Buffett, who like the Duracell bunny is known for his stamina, says:

“I have always been impressed by Duracell, as a consumer and as a long-term investor in P&G and Gillette

“Duracell is a leading global brand with top quality products, and it will fit well within Berkshire Hathaway.”

More here.

Updated

Jaguar Land Rover workers have turned down a pay offer worth an extra 15% over the next three years, ITV’s Joel Hills reports.

Workers at JLR overwhelmingly reject (96%) company's latest pay offer. Unite threatening ballot for industrial action unless talks resume.

— Joel Hills (@ITVJoel) November 13, 2014

The offer is worth 7.7% in the first 12 months – an ‘inflation-busting’ increase in anyone’s book. The staff at JLR reckon they deserve a better deal, though, given the company’s success.

JLR is thriving but workforce unhappy with way the wealth is being shared. Company making record profits but faces threat of strike action.

— Joel Hills (@ITVJoel) November 13, 2014

Updated

The Brent crude oil price will keep falling, reckons Capital Economics’ experts....

Capital Economics - Brent to drop to $70 by end 2016. "The world will soon be awash with oil"

— Mike Bird (@Birdyword) November 13, 2014

Updated

Analyst: inflation and oil add to eurozone gloom

This morning’s eurozone inflation data, and the latest fall in the oil price, add to the gloom in the eurozone, reckons Edward Knox, currency analyst at Caxton FX.

With the oil price continuing to drift with very little support, and increasing geo-political risks today’s announcement will have done no favours for Mario Draghi and his team.

Monetary easing is a tool that they still have in their locker, and the pressure to use this will have increased this morning. Mounting expectations of further stimulus down the line will most likely have a negative impact on the single currency going forward. The US dollar, backed by the resurgent US economy is the currency most primed to take advantage of the weaker outlook in the euro zone.

Reminder: German annual inflation remained at 0.8% in October and French CPI rose to 0.5%, but Italian prices are up just 0.1% in the last year, while in Spain they are down by 0.1%.

Greece’s unemployment rate has fallen, but that’s partly because more adults dropped out of the labour force this summer.

The Greek jobless rate dipped to 25.9% in August, down from 26.1% in July. That’s an improvement on the 27.8% recorded a year ago. (these rates are all seasonally adjusted.)

ELSTAT reports that the number of unemployed Greeks fell by 20,398 in August compared to July. But the number in employment also fell month-on-month, by 15,698.

The number of people classed as ‘inactive’ (neither in work nor looking for work) jumped by 31,709 during the month. More here.

Oil price hits new four-year low

The oil price has hit a new four-year low today, in another sign of economic weakness.

Brent crude has fallen another to $79.38 in the last few minutes, as weak Chinese data added to warnings that the world could see a ‘glut’ of oil.

Brent fell below $80 per barrel for the first time since September 2010 last night, after the US Energy Information Administration lowered its output forecast and predicted that Saudi Arabia would cut supply.

The news today that China’s industrial production expanded at a slower rate in October also hit the oil price, as Mike van Dulken, head of research at Accendo Markets, explains:

Oil remains under the cosh after China Industrial production data confirmed the nation’s slowdown moving into the fourth quarter of the year, intensifying questions over global demand while production is rising.

Brent crude extended losses from a four-year low, trading near $80 a barrel amid signs that OPEC remains unwilling to reduce output

— Francine Lacqua (@flacqua) November 13, 2014

The price of a barrel of Brent Crude Oil remains below US $80 (79.69) as commodity #Disinflation pressures mount.

— Shaun Richards (@notayesmansecon) November 13, 2014

The OPEC group is due to meet later this month, but oil analysts aren’t convinced that producers will agree action to underpin the oil price.

Last night, Saudi oil minister Ali al-Naimi tried to calm talk of a price war raging in the energy market, saying:

Talk of a price war is a sign of misunderstanding, deliberate or otherwise, and has no basis in reality...

“We want stable oil markets and steady prices, because this is good for producers, consumers and investors.”

As this chart shows, the oil price has been sliding since the summer.

On course for five successive monthly declines in a row for #Brent #Oil - worst performance since 2008 - pic.twitter.com/ZZjjQ8xcuB

— Michael Hewson (@mhewson_CMC) November 13, 2014

Good news for consumers, but bad for oil producers in the Middle East and for Russia. It also pushes down inflation, which households will welcome, but central bankers in the euro area will not....

Updated

Eurozone forecasters cut growth and inflation projections

A group of Europe’s top economists and forecasters have slashed their growth and inflation forecasts for the eurozone, highlighting the region’s economic problems.

They have warned the European Central Bank that they expect euro inflation to be just 0.5% this year, down from 0.7%; and 1.0% in 2015, down from 1.2% previously.

They also expect weaker inflation in 2016 too -- just 1.4%, down from 1.5%.

In other words, well short of the ECB’s target of just below 2% even in two years time, even with the stimulus measures already agreed.

The panel of 61 economists and academics also cut their forecast for GDP growth this year to 0.8%, from 1.0%.

They also expect little improvement in 2015, with predicted growth cut to 1.2% from 1.5%. Or in 2016, where projected growth is lowered to 1.5% from 1.7%.

They warn that geopolitical threats from Ukraine and the Middle East, and the threat of lower from China and the US, could all potentially hit growth.

This is what Bank of England governor Mark Carney was talking about yesterday, when he warned that the spectre of economic stagnation was looming over Europe.

These forecasts are included in the ECB’s Monthly Bulletin, which was just released (it’s online here). That Bulletin warns that:

Since the summer months, incoming data and survey evidence have overall indicated a weakening in the euro area’s growth momentum.

adding that the risks surrounding the economic outlook for the euro area continue to be on the downside.

In particular, the weakening in the euro area’s growth momentum, alongside heightened geopolitical risks, could dampen confidence and, in particular, private investment. In addition, insufficient progress in structural reforms in euro area countries constitutes a key downward risk to the economic outlook.

The panel of independent experts warned that there is a risk that a “sustained period of low growth and low inflation” would put firms off from investing and employing staff.....

It’s a stark warning, ahead of tomorrow’s growth figures (from 6.30am GMT sharp!)

Updated

October’s Italian inflation data is just out, and it shows that prices inched up by just 0.1% over the last year, and also on a month-on-month basis.

#Italy | OCT FINAL CPI M/M: 0.1% V 0.1% PRELIM; Y/Y: 0.1% V %0.1 pic.twitter.com/kCopvO7Lec

— Ioan Smith (@moved_average) November 13, 2014

Back in the UK, Bank of England deputy governor Ben Broadbent has warned that real wages and productivity need to rise for Britain to enjoy a proper recovery.

Speaking to the BBC, Broadbent said it was “extremely welcome” that real wages are finally rising. but:

“What is true is that it’s hard to have a sustained recovery in which ... productivity and real rates of pay don’t start to rise,”.

Yesterday’s unemployment report showed that earnings grew faster than inflation in September, after years of squeezed living standards.

#Inflation numbers out this morning: Germany: +0.8% (0.8% in Sep) France: +0.5% (0.4% in Sep) Spain: -0.1% (-0.2% in Sep)

— Markit Economics (@MarkitEconomics) November 13, 2014

Spain remains in deflation

Here comes the Spanish inflation data.... and it shows that prices are still lower this year than in 2013.

The Spanish consumer prices index fell by 0.1% annually in October, matching September’s decline. On a EU-harmonised basis, CPI fell by 0.2%.

Spanish CPI inflation rate at -0.1% Y/Y in October, core rate -0.1% #deflation

— MineForNothing (@minefornothing) November 13, 2014

On a monthly basis, prices picked up by 0.5% between September and October.

But as with France and Germany, the long-term trend is clear.

The long-term trend of German and French inflation shows a clear direction....

German CPI at 0.7% but... pic.twitter.com/leVZIqlTBo

— Adnan Chian (@AdnanChian) November 13, 2014

@fwred @graemewearden 7 year direction pic.twitter.com/PA5zKN2Mjj

— Ioan Smith (@moved_average) November 13, 2014

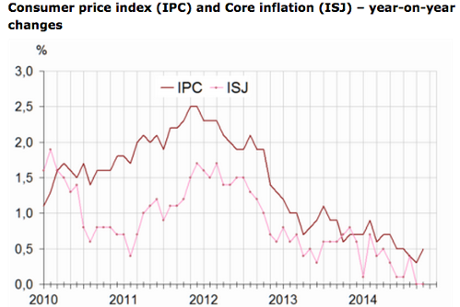

France’s statistics body, INSEE, says that rising costs of food and services helped to push the French inflation rate up to 0.5% last month.

However, the prices of manufactured products declined in October and those of energy, especially those of petroleum products, went on falling.

And annual core inflation, stripping out volatile items like food and fuel, was flat for the second month running, as this chart shows:

French inflation comes in at 0.5%

Here comes the French inflation report...and it’s slightly more encouraging than expected.

However, the data also shows that Europe’s second-largest economy remains worryingly close to deflation.

France’s consumer prices index (harmonised) rose by 0.5% annually in October, up from 0.3% in September. That beats forecasts of 0.4%.

Prices were unchanged month-on-month.

#EU #FRENCH OCT. EU-HARMONIZED CPI RISES 0.5% FROM YEAR EARLIER, a bit higher than expected

— liuk (@liuk__) November 13, 2014

A long way from the ECB’s target of inflation close to, but below, 2%.

Still, Credit Agricole’s Frederik Ducrozet is encouraged by the move:

Upside surprise to French HICP inflation, UP by one tenth to 0.5% YoY (+2 tenths on CPI). Nothing spectacular, but direction matters.

— Frederik Ducrozet (@fwred) November 13, 2014

Updated

German inflation confirmed at just 0.8%

German inflation rate remains weak, with prices in Europe’s largest economy rising by just 0.8% over the last year.

Data released by federal statistics office Destatis showed that the German consumer prices index rose by 0.8% in October, or just 0.7% on an EU-harmonised basis.

Prices actually fell by 0.3% in October compared with September.

http://t.co/aUjQDWlWoD @ECB’s #Weidmann: Likelihood of #deflation remains small. Meanwhile,#German MoM #CPI @ -0.3%. pic.twitter.com/Hwy33Z9qae

— Domenico De Giorgio (@degiorgiod) November 13, 2014

That confirms the flash estimates from earlier this month, and underlines that Germany’s economy is experiencing weak demand. But has it fallen into recession? We find out in 24 hours time, when the GDP data is released.

Updated

The agenda: Inflation reports from the eurozone

Good morning, and welcome to our rolling coverage of the financial markets, the world economy, eurozone and business.

Coming up today... new inflation figures from the Eurozone’s Big Four economies are all released this morning.

The latest consumer prices index figures from Germany, France, Italy and Spain will show whether the eurozone remains close to deflation, and requires additional stimulus measures.

Europe. CPI numbers out today and will have a big influence on central bank policy. If very low will see more free money into europe

— Wayne McCurrie (@WayneMcCurrie) November 13, 2014

The overall inflation figure for the whole eurozone is released tomorrow, along with growth data for the third quarter of this year.

We might get a new insight into the state of play at the European Central Bank at 1pm when Sabine Lautenschläger, a member of the ECB’s governing council, gives a speech.

As Michael Hewson of CMC Markets puts it:

Given all the chatter about splits in the governing council it might well be listening to the other German on the ECB council, Sabine Lautenschläger later this morning when she gives a speech in Stockholm, and who like Bundesbank chief Jens Weidmann is not a fan of QE.

We’ll also be digesting new data from China earlier this morning. Growth in Industrial production and retail sales both dipped last month, adding to concerns that its economy is slowing.

Good morning. No cheerful news. China's slowdown continues into fourth quarter http://t.co/B1PWoCXNxR via @fastFT

— kit juckes (@kitjuckes) November 13, 2014

And this afternoon, we get the latest weekly US jobs figures.

I’ll be tracking all the main events through the day....