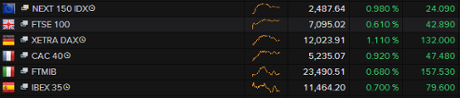

European markets mixed, with Greece down sharply

With the impasse between Greece and its creditors showing no signs of ending, ahead of yet more European meetings, investors were reluctant to take too many changes, writes Nick Fletcher, despite some positive company results which gave some support. The final scores showed:

- The FTSE 100 finished up 10.80 points or 0.15% at 7062.93

- Germany’s Dax added 0.4% to 11,939.58

- France’s Cac closed up 0.1% at 5192.64

- Italy’s FTSE MIB dipped 0.4% to 23,240.26

- Spain’s Ibex ended up 0.33% at 11,422.3

- The Athens market fell 3.33% to 704.74

On Wall Street the Dow Jones Industrial Average is currently down 69 points or 0.39%.

On that note, we’ll call it a day. Thanks for all your comments and we’ll be back again tomorrow.

Updated

Greece and Gazprom hopeful of deal

Here’s more the talks between Greek premier Alexis Tsipras and the head of Gazprom Alexei Miller from our correspondent Helena Smith in Athens:

Although the Russian’s visit has been decidedly silent on the news front – with neither Miller nor any of his interlocutors today making statements – well-placed aides are saying both sides are confident some sort of agreement will be signed imminently.

A working group is to be established with the aim of setting up a “road map” of benchmarks that Moscow and Athens will commit to in the coming months. Investment in the Greek part of the pipeline – that will run from Russia’s Black Sea coast through Turkey to Greece and into Europe via the Republic of Macedonia – is estimated at €2bn with Greece reaping the rewards of thousands of jobs and enhanced geopolitical stature, insiders said.

Meanwhile, the Greek government’s decision to bolster state coffers with the sequestered funds of local municipalities has been described as a coup d’etat - not by the political opposition but a Syriza MP – highlighting just how incendiary the move has been.

“It is tantamount to a coup d’etat that does not suit our character and leftwing conscience,” Yannis Micheloyiannakos, a Syriza deputy from Crete railed this afternoon. “Nothing can justify the government’s action.”

Updated

Greece may have bought six week’s grace if it succeeds in annexing local government funds, Bloomberg says:

Greek officials expect an order that local governments transfer funds to the central bank will keep the country afloat until the end of May as European policy makers turn up the heat on Prime Minister Alexis Tsipras.

Municipalities’ reserves are estimated at about €1.5bn, according to a person familiar with the matter, who spoke on condition of anonymity. Officials in Athens ruled out also seizing pension funds and the cash reserves of state companies because there wasn’t a need and the move would unnecessarily fuel anxiety, the person said.

With bailout talks stalled, access to cash is becoming increasingly critical. Resistance at the European Central Bank to further aiding the country’s stricken lenders is growing and the ECB is studying measures to rein in emergency funding for Greek banks, people with knowledge of the discussions said.

Full story:

Greece buys six week’s space with transfer of city funds

Some snaps coming out from Reuters on the talks between Athens and Russia’s Gazprom:

- 21-Apr-2015 16:31 - GREEK ENERGY MINISTER SAYS ATHENS HELD “CONSTRUCTIVE” TALKS WITH GAZPROM CEO MILLER

- 21-Apr-2015 16:31 - GREEK ENERGY MINISTER SAYS HOPES WE WILL REACH DEAL ON RUSSIAN GAS PIPELINE SOON

- 21-Apr-2015 16:32 - GREEK ENERGY MINISTER SAYS BELIEVES EUROPEAN UNION WILL SUPPORT RUSSIAN GAS PIPELINE

With deadlines for Greece coming and going, it’s perhaps no surprise that even eurozone officials are tired of setting a timeframe for the country to sort out its finances.

Of course, the money is going to run out at some point but as has become pretty clear today, any idea of a deal at Friday’s meeting seems fanciful. And Reuters is now reporting:

Eurozone finance ministers will not set any deadline for Greece to come up with reforms to get more funding because such time limits lead to brinkmanship in negotiations, a senior euro zone official said on Tuesday.

Greece, which is quickly running out of cash, pledged to its eurozone partners in February that by the end of April it would agree with creditors on a comprehensive list of reforms to get €7.2bn remaining from its bailout.

Eurozone officials had expected the list to be presented to eurozone finance ministers this Friday in Riga. This would allow for a faster disbursement of cash to Athens, helping the debt-laden country avoid default on loan repayments on May 12.

But no package will be ready by then and it is also unlikely it will be ready by the end of the month. This is mainly because in the past weeks Greece has not been providing the creditors with the financial data they seek or saying clearly what reforms it plans.

Greek Prime Minister Alexis Tsipras will meet German Chancellor Angela Merkel at a European Union summit on migration on Thursday and the two are expected to discuss the funding crisis.

Speaking in Vienna, European Commission President Jean-Claude Juncker urged Greece to step up efforts to strike a deal with its, warning that talks were not advanced enough to find a quick solution.

A senior euro zone official involved in the talks said there had been some improvement in negotiations very recently, but not enough for a deal.

“There is a clear pick up in activity, there is a clear pick up in engagement, but we are a significant way away from a signal that a result is in sight,” the official said.

“(But) the use of deadlines, which leads to certain brinkmanship and unnecessary excitement, will not be done again.”

Summary: Greek crisis rumbles on

A quick recap.

Friday’s meeting in Riga, which had been inked in as a key deadline, is unlikely to see progress. As one official put it this afternoon:

“There is a clear pick up in activity, there is a clear pick up in engagement, but we are a significant way away from a signal that a result is in sight.”

#grexit eurozone and greece have lost 2 months, riga 'will not be a huge discussion, not such a lot will be happening' - eu official

— Ian Traynor (@traynorbrussels) April 21, 2015

Eurogroup chief Jeroen Dijsselbloem, though, has warned that Greece’s money is running out.

The European Central Bank has raised the pressure on Greece; sources have leaked that the ECB could rein in some the emergency liquidity that is keeping Greece’s banks afloat.

That report has driven Greek government debt prices down to new record lows, with yields deeper into danger zone. Greece’s five-year bond is now changing hands at a yield of over 20%.

Greece sweep 10-yr 13.54 +25½ 5-yr 20.15½ +57½ 3-yr 29.76 +107½

— Steve Collins (@TradeDesk_Steve) April 21, 2015

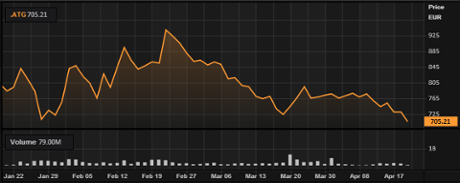

The Greek stock market also fell sharply, with the ATG index closing 3.3% lower at 704 points. I think that’s the lowest level since 2012.

Meanwhile in Athens, the boss of Gazprom has met with prime minister Tsipras. There’s doubt, though, that Greece could unlock financial help from Russia by agreeing to a new pipeline.

Photos of the meeting between Greece’s PM, Alexis Tsipras, and Gazprom chief Alexei Miller just arrived; it looks pretty cordial.

As covered earlier, the two men were expected to discuss cutting Greece’s energy costs, and perhaps a new pipeline to run from Russia through Greek territory.

Updated

The chairman of the White House Council of Economic Advisers has warned that the world economy would be badly hit if Greece crashed out of the single currency.

In an interview with Reuters in Berlin, Jason Furman swept aside the notion that a Grexit could be contained easily.

He said:

“A Greek exit would not just be bad for the Greek economy, it would be taking a very large and unnecessary risk with the global economy just when a lot of things are starting to go right.”

Here’s the story: White House adviser says ‘Grexit’ carries major risks

Here’s a snap of the irate Greek mayors’ meeting:

Local government leaders anger at govt emergency fund. Meeting live: http://t.co/oT5DbthiEM #Greece pic.twitter.com/0MHdjPLOEg

— Derek Gatopoulos (@dgatopoulos) April 21, 2015

Jeroen Dijsselbloem, the head of the eurogroup of finance ministers, has just warned that Greece is running short of time and money.

- EUROGROUP’S DIJSSELBLOEM: HAVE TO REACH AGREEMENT WITH GREECE IN COMING WEEKS

- DIJSSELBLOEM: GREECE’S MONEY IS RUNNING OUT

- DIJSSELBLOEM: GREEK EXIT OF EUROZONE WOULD LEAD TO DANGEROUS INSTABILITY FOR GREECE, EUROPE

Greek mayors blast minister over cash raid

Over in Athens scenes of pandemonium have erupted as local municipalities gather to discuss what is being described as the government’s “outrageous decision” yesterday to sequester spare funds from local authorities.

Helena Smith reports that mayors attending an emergency meeting of the Central Union of Greek Municipalities (KEDE) hurled abuse at the deputy finance minister Dimitris Mardas when he announced that the “internal loan” would be enforced “for at least two months.”

“Is this your democracy?” protestors were heard saying. Media outlets quoted several of the mayors as telling Mardas:

“the money is ours and we will do with it what we want.”

Municipalities are demanding that the order be immediately revoked.

The Bank of Greece has been told to take these cash reserves with immediate effect, to help cover Greece’s looming debt repayments and wage and pension bills.

KEDE, which is expected to meet in emergency session for several hours yet, says it will hit back with a series of protests and demonstrations and take the case to Greece’s Supreme Court, the highest tribunal in the land.

Meanwhile in Brussels, EU officials have just revealed that Greece’s lenders (the ‘institutions’, formally known as the Troika), have been pushing for such a move.

On #Greece govt move to seize municipal funds: "institutions" have urged such a move for "many, many weeks" to centrally manage cash.

— Peter Spiegel (@SpiegelPeter) April 21, 2015

Greek fiscal situation well manageable with decree on centralising municipal cash, euro source

— Bruno Waterfield (@BrunoBrussels) April 21, 2015

Updated

No hope of Greek deal this week - Brussels

EU officials have told reporters in Brussels that Friday’s eurogroup meeting of finance ministers is extremely unlikely to deliver a deal over Greece.

"We are now where we really should have found ourselves 2 months ago," says #EU official of current #Greece talks.

— Peter Spiegel (@SpiegelPeter) April 21, 2015

"It would be extremely diff to keep to this deadline on the 30th of April," #EU off says of deadline for #Greece to submit final reform list

— Peter Spiegel (@SpiegelPeter) April 21, 2015

'A significant way away from a signal that the end is in sight,' source, hinting at eurogroup next week, difficult to meet deadline

— Bruno Waterfield (@BrunoBrussels) April 21, 2015

So, we could be looking at the May 11 Eurogroup meeting for a breakthrough that would unlock Greek funds.

Or possibly even later?

EU Official Says June 30 Is Most Important Deadline For Greece

— Steve Collins (@TradeDesk_Steve) April 21, 2015

Updated

Just in: a photo of Greece’s energy minister Panagiotis Lafazanis (left) meeting Gazprom chief Alexei Miller today.

Updated

Only a "brief presentation on state of play in #Greece" at Friday's #Eurogroup in Riga, says #EU official.

— Peter Spiegel (@SpiegelPeter) April 21, 2015

Eurozone officials are downplaying the chances of a big breakthrough on Greece at Friday’s meeting of eurozone finance ministers:

Not a lot will happen in Riga, says senior euro source #Grexit

— Bruno Waterfield (@BrunoBrussels) April 21, 2015

It’s also not expected to be a marathon session:

"Not such a lot will be happening in Riga," says #EU official. #Eurogroup meeting likely 3-3.5 hrs. #Greece

— Peter Spiegel (@SpiegelPeter) April 21, 2015

Heads up. EU officials are about to brief the Brussels press pack about Friday’s eurogroup meeting, where Greece will be top of the agenda.

Almost time for everyone's favourite live tweeting event: the pre-#eurogroup background briefing pic.twitter.com/ik5ofbE3M6

— Peter Spiegel (@SpiegelPeter) April 21, 2015

Details to follow......

The National Bank of Hungary just became the latest central bank to ease monetary policy; cutting rates by 0.15% to a new record low of 1.8%.

Hungary cuts interest rates for second time this year. A total of 27 central banks around the world have eased policy so far this year.

— Jamie McGeever (@ReutersJamie) April 21, 2015

Greece’s energy minister Panagiotis Lafazanis is starting talks with Gazprom’s CEO Alexey Miller in Athens. On the agenda, a possible gas pipeline deal that could bring cheaper energy to Greece.

Our correspondent Helena Smith reports:

Insiders in the governing Syriza party, where Lafazanis heads the militant faction known as the Left Platform, have been telling me this morning that one of the top priorities in discussions today will be achieving a reduction in the price of gas that Greece imports from Russia.

Close to 60% of the country’s gas supplies come from Russia but costs are high because supplies are transferred in liquified form by sea tanker making Greek gas among the costliest in Europe.

“The biggest priority in talks today will be getting agreement on reduction of costs. Ideally, we would like to seal a deal where costs are brought down by 20%,” one well-placed source said.

“It’s not only about the pipeline and any prepayment that Moscow might make. If an agreement benefits Greece we will sign it and we may just be days away from doing that.”

Vasillis Moulopoulos, who presides over the company that owns the Syriza aligned newspaper Avgi, told the Guardian that Athens had every right to pursue a multi-dimensional foreign policy that included reaching out to Russia and China.

“Every other European country does it, so why can’t Greece?...Angela Merkel has been to Moscow three times, but as soon as [Alexis] Tsipras goes, a huge fuss is made.”

But Syriza, he said, was also willing to make the compromises necessary to clinch an interim deal with creditors at the EU and IMF to unlock the funds the country now so desperately needs.

“It is clear that Syriza cannot immediately enforce all its pre-election pledges and it is willing to go back on certain things,” he told me, adding that privatisations might be among the concessions the leftists were willing to make.

“But there are certain red lines, such as reducing wages and pensions and doing away with collective work agreements, which exist all over Europe, which we cannot accept. Certain mistakes may have been made on our part as this is a government that lacks experience but on the other hand Europe is also making some absurd demands that no one could accept. This government will not take decisions that are critical for the country if they do not have the endorsement of the people.”

Giving added gravitas to the prospect that his leftist-led coalition may resort to early elections or a referendum in the event of deadlock Tsipras repeated, this week that solutions can always be found. “Democracy cannot be blackmailed,” he said. <end>

Incidentally, energy expert Nikos Tsafos has argued that talk of a €5bn windfall for Greece from Gazprom could be hot air:

Deflating the Russia-Greece #energy connection http://t.co/foBszInAAo

— Nikos Tsafos (@ntsafos) April 21, 2015

Greek local authorities revolt over cash grab

Greece’s mayors are up in arms about the government’s order to hand over cash reserves.

Associated Press reports:

Authorities from municipalities across Greece will hold an emergency meeting Tuesday after the government ordered reserves from state enterprises to be placed in a common account to help the country meet its financial obligations and avoid default.

Following an emergency decree, funds from anything from hospitals to local government will be made available for short-term loans to the state.

Athens Mayor Giorgos Kaminis said his municipality would argue the decree was unconstitutional, while other mayors have told local media they are considering appealing the order in court. Opposition parties have expressed outrage.

There are also reports from Greece that the transfer will last until the end of May:

#Greece AltFinMin Mardas reportedly told Municipalities Union leaders that mandatory transfer of assets will last for 'two months'.

— Yannis Koutsomitis (@YanniKouts) April 21, 2015

Greece’s scramble for cash comes as the rest of the eurozone wallows in an ocean of liquidity.

This morning, the 3 month Euribor rate – which measures the cost of lending between eurozone banks – fell below zero for the first time ever. That means banks have so much cash that they’re actually paying (a little bit) to lend to each other:

#EUR003M #Euribor 3 month first time negative -0.001 It's getting cold down there... pic.twitter.com/bmLPRgXIVT

— Emmanuele Spadaro (@Orospies17) April 21, 2015

Economist Shaun Richards is struck by the contrast, saying:

There is a flood of liquidity in the Euro area as evidenced by another interest-rate benchmark plunging through the ice into below zero territory.

Yet the place that most needs it,Greece, finds itself in a desert lacking liquidity and after last night’s move by its government there must be fears of another deposit outflow. This is a cycle which sucks ever more breath out of the Greek monetary system.

Greece faces a cash crunch just as the Euro area is awash with liquidity http://t.co/cXZhf2O9nC via @notayesmansecon #Grexit #Bonds #ELA

— Shaun Richards (@notayesmansecon) April 21, 2015

Updated

The leaders of Greece and Germany will hold talks in Brussels on Thursday, on the sidelines of the emergency EU Summit on migration (that’s via Reuters).

Royal Bank of Scotland’s analysts believe the crisis could lead to a third bailout, an exit from the Eurozone or a new government.

RBS: "Do not confuse a missed payment (or even default) with Grexit risk, which we think is still very unlikely" pic.twitter.com/vzeNTqTBGQ

— Katie Martin (@katie_martin_FX) April 21, 2015

Updated

Even if Greece can meet its IMF repayment in May, it faces larger bills in June - and then hefty repayments to the European Central bank over the summer.

Greece’s existing bailout expires at the end of June, so further funding will be needed by then.

Updated

Greece’s finance minister told reporters this morning that talks with creditors are going ‘very well’, according to Greek newspaper Enikos.

Enikos says:

Greece’s negotiations with its creditors are going “very well,” Finance Minister Yanis Varoufakis told waiting reporters outside the Ministry of Finance Tuesday.

Ased how the talks in Paris are going. “Very well, we continue.”

Varoufakis did not, however, answer a question on how long can Greece continue to cover its financial needs without assistance, and just wished the reporters a good day.

#Varoufakis asked: how long can #Greece continue to cover its financial needs? -http://t.co/4BmjURGKPL pic.twitter.com/8EgVa8GVKe

— enikos_en (@enikos_en) April 21, 2015

Eirini Tsekeridou, fixed income analyst at Julius Baer, reckons Greece will eventually cave in to its creditors’ demands on taxes, pensions, and privatisations.

But given the “high political instability”, Julius Baer isn’t prepared to hold Greek debt right now.

Tsekeridou also warned that yesterday’s decision to take cash reserves from Greek state bodies will only delay Greece’s cash crunch:

“We would like to remind that Greece has to pay €200m to the International Monetary Fund (IMF) on 1 May as well as €1.4bn in maturing Treasury bills on 8 May, while pensions and public sector salaries amount to around €1.7bn.

The risk of missed payment is pushed down the road towards month-end or possibly beginning of May, but the solution found signals desperation and is not viable; the issue will arise sooner rather than later.”

Updated

This is a notably gloomy tweet from Francesco Papadia, the former director general for Market Operations at the European Central Bank.

#Greek economic, fiscal, liquidity situation is progressively deteriorating, mutual trust disappeared and no visible progress on negotiation

— Francesco Papadia (@FrancescoPapad1) April 21, 2015

Updated

One of the world’s most powerful investors has predicted that Greece will be ‘kicked out’ of the eurozone unless it agrees to its creditors demands:

Larry Fink, the head of US investment management giant BlackRock, told a conference in Singapore today that:

“If Greece does not capitulate, Europe has no choice but to kick Greece out...

The Europeans have no choice but to be firm. The outcome of Greece unwilling to meet its obligation is very negative for Greek citizens.”

BlackRock's Fink: “If #Greece does not capitulate, Europe has no choice but to kick Greece out” http://t.co/Gs03B7MRDL via @business

— Zoe Schneeweiss (@ZSchneeweiss) April 21, 2015

Despite today’s rumours, analysts at Citi suggest that the ECB probably won’t pull the plug on Greece’s emergency liquidity support this month:

Citi thinks that #ECB would review ELA on May6 or May20. In meantime, a 2/3 majority of votes cast by ECB GovCouncil required to stop #ELA.

— Holger Zschaepitz (@Schuldensuehner) April 21, 2015

(the ECB is due to hold non-monetary policy meetings on those dates)

Updated

Charts: Greek market hit by ECB rumours

Greece’s stock market has hit its lowest level since Syriza won January’s general election.

The reports that the ECB might pull the plug on Greece’s banks are sparking a hefty selloff in Greek bank shares, as these charts show:

Unless the market recovers, it could hit its lowest closing level since the heights of the eurozone crisis in 2012:

#Greece stocks poised for lowest close since Sept. 2012 pic.twitter.com/wV582dnC4M

— Richard Bravo (@richbravo2) April 21, 2015

Some reaction to the ZEW survey:

CHART: #Grexit risk NOT derailing euro-area recovery. #ZEW current situation component rises to 4-year high in April. pic.twitter.com/WtFGLPF9Lo

— Maxime Sbaihi (@MxSba) April 21, 2015

ZEW's German economic sentiment index dips a little

Just in: German economic optimism has dropped for the first time since last October, but current conditions remain extremely bright.

That’s according to the ZEW Institute latest survey. Its economic sentiment index dipped to 53.3 from 54.8 last month, showing more caution

However, its current conditions index jumped to 70.2, up from 55 last month; the highest since July 2011. That shows that analysts believe the German economy is currently in rather decent shape.

Germans feeling great! pic.twitter.com/usgtPP5Bh1

— Lex van Dam (@lexvandam) April 21, 2015

German ZEW Current Conditions Index at 45-month high of 70.2, but Econ Sentiment slips slightly to 53.3 (54.8 in Mar) http://t.co/YLVY5cb5lL

— Markit Economics (@MarkitEconomics) April 21, 2015

Updated

Bloomberg: ECB is losing patience with Greece

Here’s the Bloomberg story that has rattled the Greek stock market, pushed down the euro, and raised new fears that Greece could default:

The European Central Bank is studying measures to rein in Emergency Liquidity Assistance to Greek banks, as resistance to further aiding the country’s stricken lenders grows in the Governing Council, people with knowledge of the discussions said.

ECB staff have produced a proposal to increase the haircuts banks take on the collateral they post when borrowing from the Bank of Greece, the people said, asking not to be named as the matter is private. While the measure hasn’t been formally discussed by the Governing Council, it may be considered if Greece’s leaders fail to quickly convince euro-area finance ministers they can reform their economy and secure bailout funds, one of the people said.

Greek lenders are mostly locked out of regular ECB cash tenders while the country’s government, which holds talks with euro-area partners in Riga this week, tussles with its creditors over the much-needed aid payments. Instead, the banks currently have access to about €74bn ($79bn) of emergency funds from their own central bank -- an amount that has been rising and which will be reviewed this week.

There’s “no doubt” that the ECB is losing patience with Greece, said Frederik Ducrozet, an economist at Credit Agricole CIB in Paris.

“Greek banks will need more funding before long, so in a way larger haircuts or a lower ELA cap are equivalent.”

The ECB staff proposal outlines three routes for reducing the amount of cash lenders can access for a given amount of collateral, one of the people said. The haircuts set under ELA operations aren’t public. An ECB spokesman declined to comment....

Full story: ECB Is Studying Curbs on Greek Bank Support

Paul Mason of Channel 4 has his suspicions over the timing of this leak:

Outbreak of frenzied threats to Greece by ECB, briefed via BBG, usually means political talks with Eurogroup making progress.

— Paul Mason (@paulmasonnews) April 21, 2015

Default fears are hitting Greek bonds too, pushing prices down to even more worrying levels:

The two-year Greek bond yield (or interest rate) hit 29.4% this morning.

Greek Bond yields move higher as worries Grow. #Greece's 2yr and 3yr yields heading towards 30%, highest since 2012. pic.twitter.com/iF1qrW2o0i

— Holger Zschaepitz (@Schuldensuehner) April 21, 2015

The Athens stock market is dropping in early trading as fears over Greece’s finances rise.

The ATG index has shed 2%, led by Piraeus Bank, which has tumbled by 12.5%.

Greek banking stocks fall to record low, -4% today and -50% since late Feb as #Grexit fears mount: pic.twitter.com/KSGxowuwfq

— Jamie McGeever (@ReutersJamie) April 21, 2015

More leaks from the European Central Bank, suggesting it may impose tighter rules on Greek banks in return for emergency liquidity.

BREAKING: ECB staff plan to raise haircuts on Greek bank collateral; sees haircut of 75% in orderly default - sources pic.twitter.com/R44P7MkWRe

— CNBCWorld (@CNBCWorld) April 21, 2015

Some analysts are speculating that the ECB is unhappy about yesterday’s decree, forcing local authorities to transfer their cash funds to the ECB.

That move would drain cash out of commercial banks, making them more reliant on the ECB’s emergency funds.

Gazprom chief Alexie Miller is visiting Athens today to discuss “current energy issues of interest” with prime minister Alexis Tsipras, according to the energy ministry.

The ministry declined to comment on rumours that Gazprom could pay up to €5bn to Greece in return for deal to extend its planned Turkish Stream gas pipeline.

Such a cash injection could be crucial for Athens. But as the AFP newswire explains, it’s not a done deal:

If the deal is indeed sealed, any advance payment would be a welcome source of revenues for Greece, which is struggling to unlock 7.2 billion euros in desperately needed international bailout funds.

Analysts are however sceptical, as the Turkish Stream pipeline is not expected to come into service until 2019 and Ankara and Moscow are struggling to come to a final deal.

“2019 is a long way into the future. I’d be surprised if Russia were really to pay Greece such an amount of money four years in advance for a risky project which still needs to be vetted by EU regulators,” said Holger Schmieding of Berenberg bank.

European stock markets are still shrugging the Greek crisis off, though:

Euro weakening

The euro has lost ground in the currency markets this morning, dropping almost 0.7% against the US dollar to $1.066.

Augustin Eden at Accendo Markets says Greece continues to weigh on investors’ minds today.

There is unease surrounding Russia’s role in the situation, he says - fuelled by Gazprom chief Alexie Miller’s trip to Athens.

Could Putin afford to extend his hand to the troubled nation? Some think not, which is seen as a good thing while others are genuinely worried that he can and will According to reports, The Kremlin is willing to offer up to €4.5B to Athens as an advance for a planned natural gas pipeline through the country.

Wonga suffers £37m loss after clampdown

Just in: Wonga has posted a £37m loss for 2014, even bigger than expected, as the clampdown on Britain’s payday loan industry hits home.

Hot off the Reuters terminal:

- WONGA FY PRETAX LOSS 37.3 MLN STG VS PRETAX PROFIT 39.7 MLN

- WONGA FY REVENUES 217.2 MLN STG VS 314.7 MLN STG

- WONGA SAYS 2015 RESULTS WILL REFECT ANOTHER TOUGH YEAR

- WONGA SAYS WILL LOOK TO LAUNCH NEW PRODUCTS, SEEK DEBT FUNDING IN 2016

- WONGA SAYS DEFAULT RATE FELL TO 6.6 PCT IN 2014 FROM 6.9 PCT

Revenues dived at Wonga after the company agreed to clean up its act and bring in effective credit check.This led it to write off £220m of loans to 375,000 borrowers who should ever have been lent money in the first place.

Executive chairman Andy Haste admits there is more work to do:

“We know it will take time to repair our reputation and gain an accepted place in the financial services industry, but we’re determined to deliver on our plans and serve our customers in the right way.”

Updated

Bloomberg: ECB may curb Greek banks support

The European Central Bank is considering reining in its support for Greek banks, as concern grows in Frankfurt over Greece’s bailout talks.

That would potentially put Greek banks in an even trickier position, as they are relying on the ECB’s emergency funding to stay afloat.

Here’s the story:

The European Central Bank is studying measures to rein in Emergency Liquidity Assistance to Greek banks, as resistance to further aiding the country’s stricken lenders grows in the Governing Council, people with knowledge of the discussions said.

ECB staff have produced a proposal to increase the haircuts banks take on the collateral they post when borrowing from the Bank of Greece, the people said, asking not to be named as the matter is private. While the measure hasn’t been formally discussed by the Governing Council, it may be considered if Greece’s leaders fail to quickly convince euro-area finance ministers they can reform their economy and secure bailout funds, one of the people said.

Full story: ECB Is Studying Curbs on Greek Bank Support

ECB said to study curbs on Greek Bank support as unease grows, great scoop ECB/Athens team, @Jeffrey_Black, @Stefan_Riecher , @nchrysoloras

— Francine Lacqua (@flacqua) April 21, 2015

The Greek people may be losing faith in their government’s strategy, according to a new opinion poll.

TV station Skai found that 45% of people agree with the stance, down from over 70% two months ago:

@YanniKouts that is more falling apart...

— Yiannis Mouzakis (@YiannisMouzakis) April 21, 2015

The Agenda: Gazprom chief in Greece as crisis escalates

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

Fears over Greece continue to build, after Athens issued a decree yesterday ordering local authorities to move their cash reserves to the central bank.

The move has intensified speculation that Greece is running out of funds to meet its obligations, as Stan Shamu of IG explains:

The Greece situation is starting to escalate yet again and given the dire situation the country is in, some analysts are already speculating on a third bailout. Greece is in a tough cash position and latest reports suggest Prime Minister Alexis Tsipras has ordered local governments to deposit reserves with the central bank.

The situation is very time sensitive at the moment and it seems unlikely we’ll see a solution by the key dates. The issue of a Grexit will also remain on investors’ minds and many will ponder exactly what sort of an impact this would have on the region.

Given Greece has a lot more to lose than the euro area, many feel the country will end up succumbing to the eurozone’s demands despite attempting to put up a fight. Perhaps this is why the single currency is not completely crumbling on Greece fears.

Fears that Greek banks may soon run out of the collateral they need to access emergency ECB funding also looms over the eurozone:

Times Business front page: Greek banks 'close to collapse' as debt soars. http://t.co/rXmgGK5cdW by @BrunoBrussels) pic.twitter.com/7zOiQ7PPfv

— TimesBusiness (@TimesBusiness) April 21, 2015

But could Gazprom step into the breach?

The head of the Russian energy giant is heading to Athens for talks with prime minister Alexis Tsipras today; could a deal to build a pipeline through Greece be on the cards? There were reports on Sunday (later denied) that this could be worth €5bn to Greece.

Alexei Miller’s visit is also overshadowed by the news that the EU is bringing anti-competition charges against Gazprom later this week.

Also coming up today...

We get a new healthcheck on the German economy at 10am BST, when the ZEW Institute publishes its latest survey of investor confidence.

And in the UK, payday loan firm Wonga is due to release financial results shortly. It’s expected to post a sizeable loss of perhaps £35m, following a regulatory clampdown.

I’ll be tracking all the main events through the day....

Updated