Please consider two new terms you should know in retirement:

- Longevity protection. The steps you can take to ensure that the money you thoughtfully saved and carefully grew during your working years doesn’t run out before you do, no matter how long you live.

- Qualifying longevity annuity contract. Commonly called a QLAC, this type of deferred income annuity funded out of your rollover IRA account provides guaranteed lifetime income starting at an age you select but no later than 85.

I’m not trying to turn you into an actuary or pension specialist, but an understanding of those terms can make a huge, positive difference in your plan for retirement income and your peace of mind.

Planning for a long life

Living too short a life is unfortunate and sad. So is living so long you outlast your savings. However, while we can’t say with certainty how long we will live, we can prepare ourselves if we are surprised by living beyond our life expectancy.

A poll conducted by the Global Financial Literacy Excellence Center with the research organization TIAA Institute, showed that most of us aren’t thinking enough about how long we might live and the new set of late-in-life expenses. More women are well-versed in the details of longevity than men, the poll shows. Financial literacy follows the same trend.

For the basics, if you’re like our sample 70-year-old female retiree, according to certain actuarial models your life expectancy is 89 if you’re in good health; it’s 87 for a man. Remember this factoid: 50% of you will live beyond life expectancy.

Most of us will be able to count on Social Security — and it’s a lifetime benefit. Will benefits be cut when, without governmental intervention, the Social Security program becomes insolvent in or around 2033? Only Congress can tell. And what percentage of your budget is covered by Social Security?

Retirement income alternatives

Traditional retirement income planning, using only investments, predicts how long your savings will last based on probabilities. Certainty is better when faced with these life risks. In other words, you need planning that allows you or your adviser to bring in longevity protection, and while the government isn’t always the first place we look for solutions, a QLAC, which Congress approved and recently expanded, addresses longevity protection with guaranteed income starting later in life.

As I wrote in my article Curious About a QLAC? SECURE 2.0 Act Gives This Annuity a Boost, “A QLAC is technically a deferred income annuity purchased by a tax-free transfer of a portion of your tax-qualified accounts generally made after age 55. That transfer, in addition to adding a QLAC to your plan, represents a reduction in your account for the purposes of determining taxable required minimum distributions, or RMDs. So, if you used 25% of a $400,000 qualified account, your $100,000 purchase of a QLAC would immediately reduce your RMDs by 25%. And the income from a QLAC could be deferred until as late as age 85.”

Sounds a little technical, but the easier version is that you can spend up to $200,000 from your pre-tax accounts like a 401(k) to buy a QLAC, which will defer RMDs on that amount. At the same time, income payments will begin at an age you decide — no later than 85.

QLAC recipients can use the money for whatever they choose, including a trip to Paris or season box seats to their favorite NFL team. But often they spend it on late-in-life health care or housing costs that otherwise might force them to move out of their long-term homes.

How it works

Providing longevity protection through a QLAC can minimize and even eliminate the risks of running out of money.

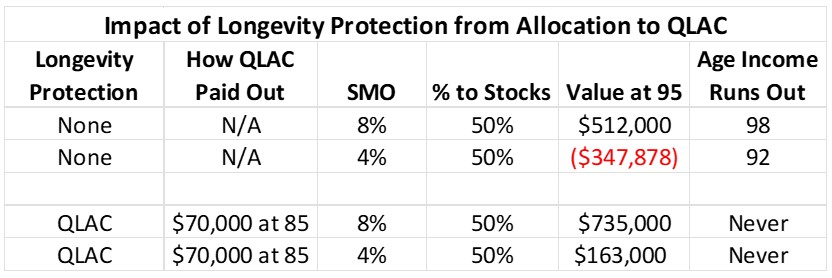

Let’s use the Go2Income planning tool and some standard assumptions to measure the risks and rewards. To simplify that analysis, we’ll use our sample investor, Sally, age 70, with $1 million of retirement savings in a rollover IRA account. She understands that she can and must do better than the 4% rule (or $40,000 per year) and instead is targeting 6%, or $60,000 per year, growing at 2% a year until age 85. That additional income of $20,000 and growing can make a big difference in her plan — provided it lasts a lifetime.

She orders two Go2Income plans with only investment portfolios and a 50/50 split between stocks and bonds. It’s a little aggressive, but she needs that to meet her ambitious goal of $60,000 annually. Her first plan assumes a long-term return in the stock market of 8%, and she ends with $512,000 at age 95. So far so good. Then she tests her second plan at a lower rate of return of 4%, which has occurred over long periods, about 10% of the time. In this case, her savings run out at age 92. Of course, the years before the run-out will be a time of high anxiety.

Now Sally tests the investment of $200,000 from her rollover IRA savings to purchase a QLAC. She runs the same two stock market scenarios and learns that a QLAC keeps the plan going for life. At an 8% stock market return, her plan is worth $735,000; at 4%, her plan has not run out of money — and she has $70,000 of guaranteed income for the rest of her life coming from a QLAC.

Here is a summary of the results:

Convinced of the efficacy of longevity insurance and QLAC, she tested different options to deploy the QLAC in her plan: (a) laddered QLAC income — reduces longevity protection but acts as an income inflation hedge; or (b) beneficiary protection — reduces late-in-life longevity protection in return for protecting her beneficiary in case of early passing. Visit our QLAC calculator to get a free quote to evaluate these options.

Other forms of income that suggest a need for longevity protection

The important part is to have a tool, like Go2Income, that can provide a fair and objective analysis of the advantages and disadvantages of QLAC or other options. While you’re at it, here are some other income streams that might need protection:

- Rental property that will be sold

- A 10- to 15-year payout from a business or investment

And probably the biggest — drawdowns from the equity in your home. In the next article, we will discuss how by using a home equity conversion mortgage (HECM), also known as a reverse mortgage, you can generate additional tax-free cash flow to 85 and substantial liquidity after 85. A QLAC is what makes it work.

Whether you consider a QLAC as a stand-alone improvement to your retirement, or integrated within Go2Income, order a complimentary Go2Income plan to help you find the best, most efficient plan for your income future.