/First%20Solar%20Inc%20logo%20and%20stock%20price-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

First Solar, Inc. (FSLR) is a leading American manufacturer of thin-film photovoltaic solar modules using cadmium telluride (CdTe) technology. Headquartered in Tempe, Arizona, the company operates a vertically integrated model that covers design, manufacturing, sales, and services, including project development, EPC, and O&M for utility-scale solar plants worldwide. The company has a market capitalization of $25.55 billion.

First Solar’s stock has reaped the gains from strong solar demand and the Inflation Reduction Act incentives. Over the past 52 weeks, the stock has gained 43.2%, while the broader S&P 500 index ($SPX) is up 14% over the same period.

However, uncertainty arising from shifting policies has introduced some weakness. First Solar’s stock is down 8.9% year-to-date (YTD), while the S&P 500 index has increased marginally over the same period.

Next, we compare the solar technology stock’s performance with that of its own sector. The State Street Technology Select Sector SPDR ETF (XLK) has gained 19.6% over the past 52 weeks, underperforming the stock, but dropped only 4.1% YTD, outperforming FSLR. The stock had reached a 52-week high of $285.99 in December 2025, but is down 16.8% from that level.

For the third quarter, First Solar’s net sales grew 79.7% year-over-year (YOY) to $1.59 billion, while its EPS grew from $2.91 to $4.24. Despite sound growth, the results fell short of analysts’ expectations. The company also narrowed its 2025 net sales guidance from $4.90 billion-$5.70 billion to $4.95 billion-$5.20 billion, while lowering its volume sold expectation from 16.7 GW-19.3 GW to 16.7 GW-17.4 GW.

The United States Patent and Trademark Office (USPTO) denied three Inter Partes Review (IPR) applications from JinkoSolar, Mundra Solar, and Canadian Solar, which aimed to overturn the company’s Tunnel Oxide Passivated Contact, or TOPCon, patents through a review process. This ruling supports First Solar’s competitive edge in the TOPCon segment.

For the fourth quarter of 2025 (to be reported on Feb. 24, after the market closes), Wall Street analysts expect First Solar’s EPS to increase 43% YOY to $5.22 on a diluted basis. EPS is also expected to increase 21.7% annually to $14.63 for fiscal 2025, followed by a 58.8% improvement to $23.23 in fiscal 2026.

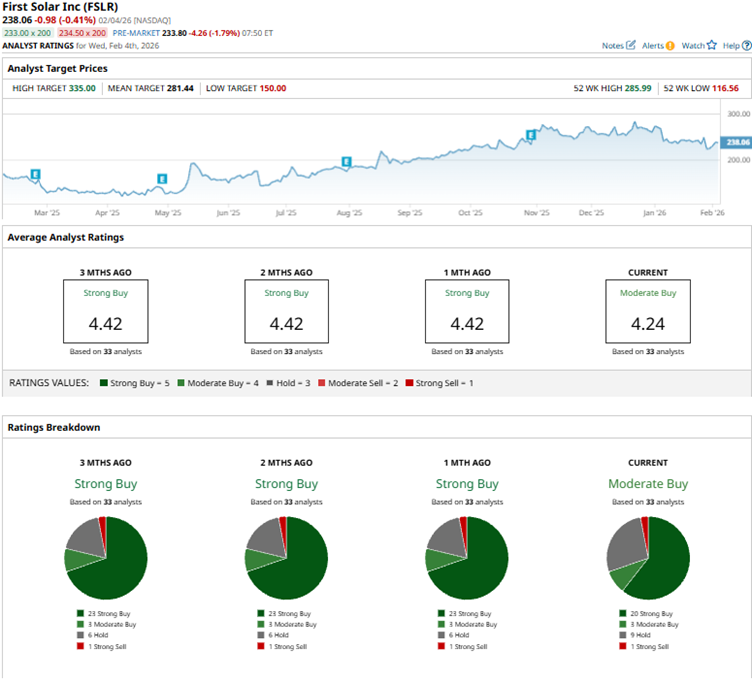

Among the 33 Wall Street analysts covering First Solar’s stock, the consensus is a “Moderate Buy.” That’s based on 20 “Strong Buy” ratings, three “Moderate Buys,” nine “Holds,” and one “Strong Sell.” The ratings configuration has become less bullish than a month ago, with the overall rating changing from “Strong Buy” to “Moderate Buy” as the number of “Strong Buy” ratings decreased from 23 to 20.

The company’s stock slid 10.2% intraday on Jan. 29 after analysts at BMO Capital downgraded it from “Outperform” to “Market Perform” and lowered the price target from $285 to $263, citing potential competitive pressure from an increase in domestic solar manufacturing.

First Solar’s mean price target of $281.44 indicates an 18.2% upside over current market prices. Moreover, the Street-high price target of $335 implies a potential upside of 40.7%.