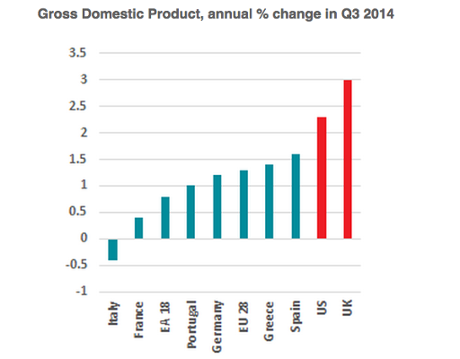

Germany narrowly avoided recession, with growth of just 0.1%, while France grew by 0.3% and Greece - whose long slump has now ended - grew by 0.7%. But Italy fell into another recession, shrinking by another 0.1%.

You can see more details in our live blog, and have your say

Here’s what economists are saying:

Richard Boxshall, senior economist at PwC:

“Today’s figures show continued very sluggish growth in the eurozone, but it has avoided lapsing back into recession. The former powerhouse of the bloc, Germany, grew at a modest rate of just 0.1% in Q3, while France was the surprise with growth of 0.3%. However, the detailed data showed that the ‘French surprise’ was primarily driven by relatively strong government spending growth, which is unlikely to be sustainable in the medium term. Meanwhile, Italy has fallen back into a mild recession.

“In contrast, most peripheral countries continue to grow at relatively strong rates with Greece growing seven times faster than Germany, closely followed by Spain and Portugal.”

Nick Kounis of ABN AMRO:

The big underperformer was Italy. GDP fell by 0.1% in Q3 following a 0.2% decline in Q2. This means it has now officially entered its third recession since 2008. For governments that think that the ECB’s conservativeness is at the heart of the eurozone’s problems, the comparison between Italy, on the one hand, and Spain and Greece is telling. Spain and Greece have done more in terms of structural reforms, and have also seen sharp falls in wages. This internal devaluation has restored competitiveness back close to the start of the euro levels. In Italy wages have remained extremely elevated.

We expect eurozone economic growth to slowly improve in the coming quarters on the back of the decline in the euro, the fall in oil prices, easing bank lending and other financial conditions and the upswing in US demand.

Danae Kyriakopoulou of the Centre for Economics and Business Research

Economic output in the Eurozone expanded by 0.2% quarter-on-quarter in Q3 2014, according to data released by Eurostat this morning. Germany and France, the currency bloc’s two biggest economies, surprised on the upside: the German economy managed to avoid recession, growing by 0.1% and beating economists’ consensus expectation for a 0.1% decline. The surprise was even more positive for France, whose economy expanded by 0.3% again beating expectations for a 0.1% decline. Meanwhile, the Italian economy contracted by 0.1%.

The fact that such weak growth rates are a cause for cheer is worrying in itself. After a false dawn when the Eurozone exited recession just over a year ago the fundamentals and overall economic picture have failed to see a substantial improvement.

Digging below the headline number for overall economic expansion the picture in Germany is highly worrying: German exports fell by 5.8% from July to August while industrial production saw its biggest decline since 2009 over the same period, contracting by 4.8%. Much of this is due to a slowdown in some of Germany’s key trading partners, notably China and other emerging markets, Ukraine and Russia, as well as the rest of the Eurozone. In other words, the German economy is starting to feel the pain of the austerity policies that it so fiercely advocated elsewhere in the Eurozone. As a capital goods exporter, Germany had been one of the prime beneficiaries of credit-driven demand in China but this is now also reversing: falling property prices and credit growth are bringing forward China’s choice between a slowdown towards a more sustainable growth trajectory and a continued credit-fuelled but unsustainable expansion. The recent rhetoric from Beijing points to a commitment to the former, and this is likely to suppress Germany at least in the short term.

This all suggests that despite the headline news of an acceleration in growth this quarter the overall picture in the currency bloc remains bleak. The European Central Bank is already doing “whatever it takes” to keep the Eurozone ship afloat: interest rates have been lowered to negative territory (the first time this has been done by a major central bank), and additional measures such as longer-term refinancing operation schemes (TLTROs) and an asset-backed securities (ABS) purchasing programme are in effect. The ECB President Mario Draghi recently also reiterated the governing council’s unanimous commitment to consider yet more unconventional measures.

In such a loose monetary context today’s figures are a great disappointment and highlight the need for fiscal expansion to support efforts on the monetary side. Given the periphery countries’ struggle with fiscal consolidation (most are running high budget deficits and have little room to increase spending), this leaves Germany as the best-placed candidate to set the fiscal motors in motion. It is thus time for Germany to reconsider its pledge to run a balanced budget next year and “take one for the Eurozone team”. Given its own recent weakness a move towards fiscal expansion will likely help its own economy along the way, too.

Chris Williamson of Markit:

“The Eurozone enjoyed stronger than expected economic growth in the third quarter, providing welcome news that fears of a renewed recession look exaggerated. However, the data will diminish hopes that the ECB will feel the need to take further action to stimulate growth.

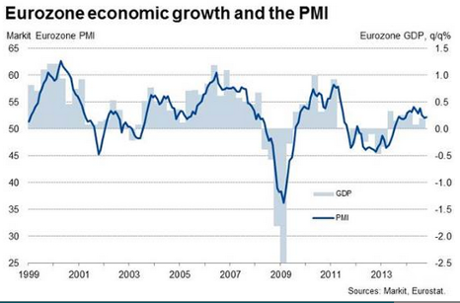

“Official data from Eurostat showed gross domestic product rose by 0.2% in the three months to September. The region is also now estimated to have grown 0.1% in the second quarter rather than stagnating, as previously estimated.

“The official data confirm business survey data which show the Eurozone economy struggling to expand in the face of numerous headwinds but nevertheless managing to eke out modest growth and avoid recession. High levels of unemployment continue to hold back consumer spending, while business in the core countries of France and Germany continue to cut back on investment in a sign of increased economic uncertainty and widespread pessimism about the outlook.

“The surveys point to further malaise extending into the fourth quarter, adding to the impression that there are few signs of the region pulling out of this torpor. The headline Markit Eurozone PMI recorded 52.1 in October, down slightly from an average of 52.8 in the third quarter and running at a level signalling another modest 0.2% expansion of GDP in the fourth quarter.

“Policymakers will at least be reassured that fears of a renewed recession look overplayed, for the time being at least. The better than expected GDP reading (analysts were on average anticipating a mere 0.1% rise) means ECB looks even less likely to announce any further measures to boost growth until it can assess the impact of the additional €1 trillion of liquidity it already plans to inject into the economy.

“Germany skirted recession by the narrowest of margins, with GDP rising 0.1% in the three months to September after a 0.1% decline in the second quarter (which was revised up from a 0.2%.contraction). The stagnation seen over the past two quarters as a whole is a major concern, especially after Germany provided such a strong contribution to growth in the region at the start of the year. GDP had surged by 0.8% in the first quarter. Both households and exporters helped boost the German economy in the third quarter, but capital expenditure suffered a worryingly sharp decline.

“France reported 0.3% growth of GDP, likewise rebounding from a 0.1% decline in the second quarter to thereby avoid falling back into a technical recession. France’s performance was flattered, however, by a 0.8% jump in government spending, the largest rise since the second quarter of last year. Once a 0.3% contribution from inventories to GDP in the third quarter is also taken into account, the French economy’s performance suddenly looks a lot worse than indicated by the headline GDP number. As in Germany, a sharp decline in capital expenditure also raises worries about business confidence and points to weak future growth.

“Signs of growth reviving in some peripheral countries was confirmed, with Spain’s economy growing by 0.5% and Greece by 0.7%. Italy, however, suffered a 0.1% drop in GDP as its slid back into its third recession since the financial crisis struck.

“In other countries, the Netherlands and Belgium GDP growth came out in line with the euro area average of 0.2% but Austria’s economy was stagnant.”

Andy Scott, associate director at HiFX

“The news that the Eurozone’s economy is performing marginally better than expected in the third quarter, gives hope that the future is looking bright for the single currency bloc. After all, the ECB has cut lending rates to almost zero - making it cheaper than ever to borrow money - as well as cutting deposit rates to a negative, effectively charging banks to hold on to excess money. It is also engaged in a Q.E. ‘light’ programme to increase the availability of cash that banks and financial companies have to lend.

“However, it’s important to consider the bigger picture and when you do, it’s clear that the future appears to be rather gloomy still. Unemployment remains incredibly high for a group of mostly developed economies at 11.5% and though it dropped at the end of last year and the start of this year, it hasn’t fallen since May.

Bill Adams, senior international economist for PNC Financial Services Group.

Real GDP growth in the Eurozone picked up to 0.2% in non-annualized quarter over quarter terms in the third quarter of 2014; growth in the second quarter was revised up to 0.1% from 0.0% in the previous release. France expanded 0.3% from a quarter earlier in the third quarter, and Germany 0.1%. Italy shrank again in the third quarter, with real GDP down 0.1%.

From a year earlier, real GDP in the Eurozone grew 0.8 percent in the third quarter, unchanged from a quarter earlier. While Germany is slowing, France is slow, and Italy is still mired in recession, the crisis economies that aggressively reformed their labor markets are now seeing better growth than the Eurozone average: Portugal grew 1.0% from a year earlier in the third quarter, Spain 1.6%, and Greece 1.4%. Ireland’s third quarter real GDP growth was not released in today’s Eurostat report, but after very robust growth in the second quarter (6.5% in year-ago terms) it is surely also outpacing the Eurozone average.

There was a long and acrimonious debate during the depths of the euro crisis about whether painful labor market reforms stimulate growth. Labor market reforms are often lumped in with austerity, since both are highly unpopular, but they analytically quite different - Italy, for example, has chosen more austerity than labor reform, and suffering the consequences. Clearly labor reforms didn’t boost growth in the short run, but two to three years after the most turbulent period of the crisis, the countries that swallowed that bitter medicine are seeing growth dividends. The third quarter GDP report will surely be cited in German arguments that labor market reforms are even more important than cutting deficits.

The third quarter real GDP report is highly encouraging, and should silence the talk of a triple-dip recession for the euro area. But actually, the trend is mostly unchanged. Growth is modest and trending under 1.0 percent, not enough to bring the unemployment rate in the Eurozone back to normal anytime soon. For monetary policy, this weak growth is, while better than recession, insufficient to raise CPI inflation back to the ECB’s below-but-close-to-2.0 percent target. An okay GDP report buys the ECB some time to wait and see how effective its asset purchase programs currently underway will be, instead of moving rapidly into government bond purchases.