European markets end week on a bright note

Slightly better than expected economic growth figures from France and Germany, and indeed the overall eurozone number as well, have helped support markets ahead of this weekend’s G20 meeting. Greece exited recession, which added to the positive mood, but on the other hand, Italy fell back again. Overall though, it was a fairly upbeat end to the week. The final scores showed:

- The FTSE 100 finished up 18.92 points or 0.29% at 6654.37

- Germany’s Dax edged 0.05% higher to 9252.94

- France’s Cac closed 0.35% better at 4202.46

- Italy’s FTSE MIB added 0.97% to 18,965.41

- Spain’s Ibex ended up 0.07% at 10,148.0

- The Athens market dipped 0.81% to 890.74

On Wall Street, the Dow Jones Industrial Average is currently down 15 points or 0.09%.

On that note, it’s time to close up for the evening. Thanks for all your comments, have a good weekend and we’ll be back on Monday.

More on the protests in Greece from Helena Smith:

Greek students have left a trail of banners and graffiti behind them as they marched through Athens this afternoon. In a display of their dermination against a government they now accuse of employing heavy -handed tactics, in addition to selling out to international creditors, this banner in front of Athens University reads: “Police get out from the university. Hands off asylum and down with the government” and demands that the rector of the school immediately resigns.

Ahead of commemorations marking the 1973 Polytechnic Uprising, the rector has refused to grant students access to university campuses - the asylum long seen as a hallowed right of students after the collapse of military rule in 1974. The main boulevards are peppered with freshly painted slogans some of which have not been seen since the height of the euro crisis. Students marching on parliament this afternoon pledged to step up protests over the weekend with many saying “the end of the government has arrived.”

“The government has miscalculated gravely on this. All Greece needs is a spark (to erupt) and this may be it,” said a law school student who gave his name as Petros Pappas. Such fears are shared by older Greeks who expressed shock this afternoon at the level of violence used against Athens university on Thursday. “The violence last night against students protesting peacefully was disproportionate and shows that the government is very fearful of young people becoming the spark of a fire that it won’t be able to comtrol,” said Leonidas Aposkitis, aged 50, who marched through Athens after taking part in Thursday’s demonstration.

And yet more positive news from the US economy.

Consumer confidence rose to a seven year high in November (so far), helped by falling unemployment - as the Fed’s James Bullard has been saying - and lower petrol prices.

The Thomson Reuters/University of Michigan first reading on its consumer sentiment index came in at 89.4, above the 87.5 reading expected by economists and up from the revised 86.9 seen in October.

Outlook brightens for holiday shopping as retail sales outperform and consumer sentiment rises...gas prices are helping, to be sure.

— Carl Riccadonna (@Riccanomix) November 14, 2014

Updated

The better than average performance of the US jobs market is inconsistent with interest rates at near zero, a member of the US Federal Reserve has said.

Speaking to an audience in St Louis, Jame Bullard said he did not see low inflation readings as a reason to delay a move away from low rates. He said (courtesy Reuters):

[Jobs growth] suggests that over the next year, it will become more and more difficult to point to labour market performance as a rationale for a near-zero policy rate.

Bullard is a notable hawk but is currently a non-voting member of the Fed’s rate setting committee, until 2016. Even so, the idea of rising US rates is gaining ground, hence the strength in the dollar.

Fed’s Bullard: Job Market Gains No Longer Justify Current Fed Policy: Federal Reserve Bank of St. Louis… http://t.co/QjjtQOIrjB WSJ

— FinanzLinksWORLD (@FinanzLinksWelt) November 14, 2014

The positive US figures is giving the dollar a lift, with sterling falling to a 14 month low against the US currency. Nicholas Ebisch, currency analyst at Caxton FX said:

Retail sales data in the US beat expectations this afternoon, coming in at 0.3% when 0.2% was expected. This comes in along with a string of positive data for the US dollar. The dollar index is currently at 88.24, which is its highest point since mid-2010. The US economy continues to be the brighter spot in a global economy that is struggling with growth, thereby boosting the dollar continuously higher.

Still with the US, and import prices fell in September by 1.3%, the most in more than two years.

The fall was due for the most part to lower costs for imported fuels following the recent crude price slump. The strong dollar also meant that it was cheaper for Americans to buy imports.

Export prices fell 1%, as the global economy weakened.

Over to the US, and retail sales for October have come in better than expected, a positive sign of returning consumer confidence and good news for the economy ahead of the key Christmas shopping period.

Retail sales - excluding volatile elements such as cars and gasoline - rose 0.5% last monthcompared to expectations of a 0.4% rise, and the biggest increase since August.

Overall they rose 0.3%, higher than the expected 0.2% increase.

Sales at food service and drinking places up 0.9% in October. Less spent at the pump. More spent at the bar. pic.twitter.com/JDH5IQvVdR

— Joseph Weisenthal (@TheStalwart) November 14, 2014

Updated

The news that Greece has left recession comes as the country is gripped by scenes of protesting students.

Our Athens correspondent, Helena Smith, explains:

Tensions are very much on rise after overnight riots outside Athens Polytechnic (where the 1973 student uprising set in motion the events that lead to the fall of Greece’s hated military regime) and a student take-over this morning of Thessaloniki University.

As I write, students are marching through Athens.

Protestors are up in arms over government’s controversial decision to implement a lock-out at all tertiary education institutions in run-up to the anniversary this Monday. Usually, university students have used the three-day period set aside for commemorations to stage sit-ins (that are themselves often marked by clashes between left and right wing students).

Tensions have been fueled by anger over tuition costs & other international-mandated educational cuts - and they show no sign of abating ahead of Monday’s anniversary.

Videos have been released that also depict riot police using excessive force to remove protestors from the scene of the Polytechnic last night. Riot police resorted to using tear gas and stun guns to remove students from the sight - without giving them any prior warning that they should get out of the way! Outside Athens University’s law School tensions are also high today.

On that note, I’m handing over to my colleague Nick Fletcher.

Updated

Richard Boxshall, senior economist at PwC, points out that Europe’s core countries are now lagging behind the periphery, such as Spain and Greece.

“Today’s figures show continued very sluggish growth in the eurozone, but it has avoided lapsing back into recession. The former powerhouse of the bloc, Germany, grew at a modest rate of just 0.1% in Q3, while France was the surprise with growth of 0.3%. However, the detailed data showed that the ‘French surprise’ was primarily driven by relatively strong government spending growth, which is unlikely to be sustainable in the medium term. Meanwhile, Italy has fallen back into a mild recession.

“In contrast, most peripheral countries continue to grow at relatively strong rates with Greece growing seven times faster than Germany, closely followed by Spain and Portugal.”

Larry Elliott: eurozone must act fast to avoid a lost decade

Our economics editor, Larry Elliott, writes that eurozone leaders must not shelter behind the fact that today’s growth figures could have been worse.

He writes:

Policymakers are deluding themselves if they believe that narrowly avoiding recession is the same as being on the road to recovery. The eurozone today is starting to look worryingly like Japan in the 1990s: little growth, crippled banks, export dependent. All it lacks to make the comparison complete is deflation, and one further negative shock would make that a reality too.

It’s clear what the eurozone needs. It needs monetary activism from the ECB. It needs fiscal activism, both from individual countries and from pan-European institutions such as the European Investment Bank. It needs Germany to realise that generalised belt-tightening has been self-defeating. And it needs all those things fast.

Here’s his full analysis: How can the eurozone escape a lost decade?

A reminder that Germany and France are above their pre-crisis peaks, but the wider eurozone is not - and Italy’s decline is quite alarming.

*NEW POST* #graficodellasettimana: l’#Europa che non cresce e l’#Italia in #recessione > http://t.co/wWXnOJ79Ki #PIL pic.twitter.com/N3hsKclDI0

— Advise Only (@AdviseOnly) November 14, 2014

Chris Williamson of data firm Markit flags up that France’s growth rate is even weaker if government spending is stripped out:

Any GDP growth in #France since 2010 has been mainly due to government spending (which is up 7.0% since 2010 Q4) pic.twitter.com/5NPzGTAEhB

— Chris Williamson (@WilliamsonChris) November 14, 2014

Germany needs to “take one for the team” and boost its borrowing, rather than stick to balancing the books, reckons Danae Kyriakopoulou, economist at the CEBR:

In such a loose monetary context today’s figures are a great disappointment and highlight the need for fiscal expansion to support efforts on the monetary side.

Given the periphery countries’ struggle with fiscal consolidation (most are running high budget deficits and have little room to increase spending), this leaves Germany as the best-placed candidate to set the fiscal motors in motion. It is thus time for Germany to reconsider its pledge to run a balanced budget next year and “take one for the Eurozone team”.

Given its own recent weakness a move towards fiscal expansion will likely help its own economy along the way, too.

This handy chart from the FT shows how Greece grew faster than Germany in the last quarter:

Greek growth bounces back, outpaces Germany for first time since 2007 http://t.co/ybF1pbIVUP pic.twitter.com/tpj79Srent

— Robin Wigglesworth (@RobinWigg) November 14, 2014

Updated

EZ Q3 #GDP still dismal at 0.2 pct, but at least not as dismal as expected pic.twitter.com/JAnf6EDCGb

— Global Markets Forum (@ReutersGMF) November 14, 2014

What recession? In the Great Depression US jobless rate rose to 25%. In Greece it's now 25.9%, down from over 27%

— Teacher Dude (@teacherdude) November 14, 2014

The eurozone countries who have implemented structural reforms are now enjoying economic growth, points out Bill Adams, senior international economist for PNC Financial Services Group:

While Germany is slowing, France is slow, and Italy is still mired in recession, the crisis economies that aggressively reformed their labor markets are now seeing better growth than the Eurozone average: Portugal grew 1.0%t from a year earlier in the third quarter, Spain 1.6%, and Greece 1.4%.

Ireland’s third quarter real GDP growth was not released in today’s Eurostat report, but after very robust growth in the second quarter (6.5% in year-ago terms) it is surely also outpacing the Eurozone average.

Labour market reforms are paying off, Adams reckons:

There was a long and acrimonious debate during the depths of the euro crisis about whether painful labor market reforms stimulate growth. Labor market reforms are often lumped in with austerity, since both are highly unpopular, but they analytically quite different - Italy, for example, has chosen more austerity than labor reform, and suffering the consequences. Clearly labor reforms didn’t boost growth in the short run, but two to three years after the most turbulent period of the crisis, the countries that swallowed that bitter medicine are seeing growth dividends.

Updated

Richard Grieveson of the Economist Intelligence Unit is worried that Germany performed so badly in the third quarter, with growth of just 0.1%.

“Declining investment growth in the third quarter is a particular concern, both for Germany and the euro zone more broadly.

“The outlook remains week. Overall the main impediments to German growth—structural weakness in other key euro zone markets, tensions with Russia and a lack of political will to invest—remain in play, and are unlikely to change in the coming quarter.”

Updated

Many ppl scratch their heads w Greece's growth amid deep fiscal consolidation. 2 answers: Tourism rev up 12%, real wages increase in Q2 & Q3

— Yannis Koutsomitis (@YanniKouts) November 14, 2014

Peter Vanden Houte of ING point out that the eurozone has still not recovered all the output lost since the financial crisis began:

Before getting overexcited by the slightly better than expected growth figure, one should bear in mind that the current growth pace is only about half the potential growth rate and that the Eurozone’s GDP is still more than 2% below its level at the start of 2008.

Not exactly an economic boom.

GDP figures, reaction starts here

Reaction to today’s growth figures is flooding in, so I’ll mop up the best:

Nancy Curtin, chief investment officer of Close Brothers Asset Management, says investors will take a little comfort, but no more:

“On their own, these growth figures are nothing to write home about, but in the context of the negative news emerging from the eurozone in recent months, the simple fact that growth isn’t slowing will reassure investors.

But let’s be clear, the outlook for the Eurozone is still heavily clouded. Inflation remains in the doldrums, employment across the bloc is not improving, and manufacturing is in a state of near stagnation.

Eurozone GDP: A recap

What have we learned this morning?

The eurozone has posted another quarter of unimpressive growth, with GDP up just 0.2% over the summer. (rolling coverage starts here)

Greece is no longer in recession - indeed, it grew faster than any other euro member in the last quarter (although Ireland, for example, hasn’t reported yet).

Germany has dodged recession too (details), but Italy was less fortunate (details). France grew a little faster than expected, but thanks to government spending rather than trade and investment (details)

#Eurozone Q3 GDP: Former crisis countries recover solidly, Germany in temporary rough patch. http://t.co/4qxieQ37NX pic.twitter.com/Ooga5zmF1C

— Berenberg Economics (@Berenberg_Econ) November 14, 2014

And economists remain concerned that the euro economy is struggling, and needs bolder reforms.

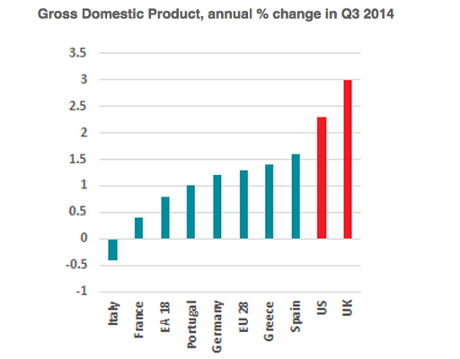

Here’s how the main European economies fared in the last three months:

- Germany: +0.1% quarter-on-quarter

- France: + 0.3% q/q

- Spain: + 0.5% q/q

- Italy: -0.1% q/q

- Portugal: +0.2% q/q

- The Netherlands: +0.2% q/q

- Greece: +0.7% q/q

- UK: + 0.7% q/q

- Poland: +0.9% q/q

- The eurozone: +0.2% q/q

- The EU: +0.3% q/q

Eurostat’s full report is here.

An old friend returns RT @MacroPolis_gr: #Greece seasonally adjusted Q3 GDP +0.7% QoQ. Positive QoQ growth for the 3rd straight quarter

— Nick Malkoutzis (@NickMalkoutzis) November 14, 2014

Updated

Greece finally growing again according to today's estimates from Eurostat. But GDP still around a fifth below peak: pic.twitter.com/ph1ZdKtwhH

— Ben Chu (@BenChu_) November 14, 2014

Cyprus’s recession continued, with GDP falling by 0.4% in the last three months.

That means only it, and Italy, shrank in July-September

Of the 14 EZ countries to report 3Q GDP q/q, only two are negative: Italy and Cyprus. Austria flat. All others positive.

— Richard Barley (@RichardBarley1) November 14, 2014

This chart, of GDP compared to a year ago, shows the long depths of Greece’s recession:

#Greece exits recession after 6yrs in debt crisis. 3Q Flash GDP +1.7% On Year. pic.twitter.com/IBvQf9xvT7

— Holger Zschaepitz (@Schuldensuehner) November 14, 2014

It appears that Greece actually exited recession in the first three months of 2014.

The data just released by Eurostat shows that the Greek economy grew by 0.8% in January-March, and by another 0.3% in April-June, before posting 0.7% growth in the third quarter.

Today’s numbers include recent revisions to the way eurozone data is calculated.

And we don’t normally get quarterly GDP figures for Greece - this is a welcome change.

@RoelD_ Υes, there were 2 consecutive revisions recently, so today's data sums them all up. @RobinWigg @AlbertoNardelliI

— Yannis Koutsomitis (@YanniKouts) November 14, 2014

Updated

Eurozone economy grew 0.2% in third quarter, slightly better than expected. France helped with 0.3% growth and recession ended in Greece.

— Gavin Hewitt (@BBCGavinHewitt) November 14, 2014

GREECE’S RECESSION IS OVER.

At long, long last, Greece’s recession has ended, after almost six years of misery.

Greek GDP rose by 0.7% in the third quarter of 2014, according to figures just released by Eurostat.

That ends a slump that began in autumn 2008, as the financial crisis was at its height and the pillars of the economic system were wobbling.

A series of austerity packages have wiped around a fifth off Greece’s economy since.

Eurostat also reports that Greek GDP is up by 1.7% over the last 12 months. The Greek Recovery has finally started....

Updated

Euro area GDP up by 0.2% in Q3 2014, +0.8% compared with Q3 2013 #Eurostat http://t.co/T41elp66hc pic.twitter.com/KpTCmpAsLL

— EU_Eurostat (@EU_Eurostat) November 14, 2014

Eurozone economy grew by 0.2% last quarter

Breaking: The eurozone grew by 0.2% in the third quarter of 2014.

That’s according to Eurostat, based on the various growth figures released by member states (our rolling coverage starts at 6.30am GMT).

Slightly better than some economists had expected.

So, another quarter of limp growth that won’t do enough to drag down Europe’s painfully high unemployment rates. Reaction to follow....

Greece to pass into growth territory in 2 mins

— Yannis Koutsomitis (@YanniKouts) November 14, 2014

No City economist surveyed by Bloomberg expected Italy to grow in the last quarter. Many expected a deeper downturn.

This is how optmistic economists were on Italy. 22 GDP estimates ranging from -0.5% to 0%.

— Jonathan Ferro (@FerroTV) November 14, 2014

Europe’s economy is basically stagnating, says Marc Ostwald of ADM Investor Services.

He reckons today’s growth figures do little to assuage concerns about the region’s outlook.

Outside of Spain, the Eurozone economy is flatlining, with the risk of a renewed recessionary lurch not to be underestimated.

And leaders, not central bankers, need to act, he adds:

Still the fact remains that it is the very disparate collective of national governments that “need to act” rather than the ECB, which will effect no change to that outlook whatever it does as long as politicians do not co-operate.

Incidentally, we already know that Spain grew by 0.5% in the third quarter.

That data, released last month, means that the Spanish economy was the best performing Big Four euro economy. And not far behind the UK.

EU 7 biggest economies GDP'Q3 qoq: - Poland +0,9% - UK +0,7% - Spain +0,5% - France +0,3% - Netherlands +0,2% - Germany +0,1% - Italy -0,1%

— Rafał Hirsch (@rafalhirsch) November 14, 2014

Economists has expected Portugal to grow by 0.4%, though....

Portugal’s economy has racked up another quarter of growth, with GDP rising by 0.2% between July and September.

Twice as fast as Germany!

Official: Portugal now has bigger GDP growth than Germany...didn't see that one coming.

— Nordic Stocks (@NordicStock) November 14, 2014

IMF chief Christine Lagarde has told the BBC that European leaders must do more to create jobs.

Italy back in recession as Germany, France eek out growth. I asked IMF's Lagarde who warned of that risk & says job growth still needed #G20

— Linda Yueh (@lindayueh) November 14, 2014

Poland’s economy outperformed the eurozone in the last quarter - with growth of 0.9%.

Its economy is 3.3% larger than a year ago, beating forecasts.

Italy’s economy has now either shrunk, or been flat, for the last 13 quarters in a row!

It began contracting in the third quarter of 2011, and the recession didn’t stop until the third quarter of 2013, when GDP stagnated.

Italy then shrank a little in Q4 2013, was flat in Q1 2014, and has now shrunk in Q2 and Q3.

This chart from ISTAT tell the story:

More details here

Updated

In Italy GDP in the last quarter fell 0.1%, the 13th Q without any growth. Economy remains in recession, likely to contract 0.4% this year

— Gavin Hewitt (@BBCGavinHewitt) November 14, 2014

Third recession in Italy since 2008. -0.1 qoq GDP in Q3. Difference with Spain is stark and a reflection of lack of reform/wage falls in IT.

— Nick Kounis (@nickkounis) November 14, 2014

Italy back in recession as GDP falls 0.1%

Breaking: Italy has fallen back into recession, as its economic malaise continues.

Italian GDP fell by 0.1% in the third quarter of 2014, broadly as expected.

That follows a 0.2% contraction in the second quarter of 2014, which means prime minister Matteo Renzi has a technical recession on its hands. (GDP was flat in the first three months of 2014).

Italian GDP has fallen by 0.4% over the last year.

Italy falls back into recession: #GDP down 0.1% in Q3 (-0.2% in Q2)

— Markit Economics (@MarkitEconomics) November 14, 2014

*ITALIAN ECONOMY SHRANK 0.1% IN 3Q, MATCHING MEDIAN ESTIMATE

— lemasabachthani (@lemasabachthani) November 14, 2014

Coming up, Italy’s GDP....

italy gdp next, or ‘la speranza’

— lemasabachthani (@lemasabachthani) November 14, 2014

The French CAC stock index has risen by 0.4% in early trading, as traders welcome the news that its economy grew by 0.3% last quarter.

Germany’s DAX is up by 0.2% following the news that Germany avoided recession.

Mike van Dulken, head of research at Accendo Markets says the growth data is “providing some relief regarding the woes of the struggling region”.

Updated

If you’re just tuning in, here’s our early story explaining today’s eurozone growth data:

Eurozone growth figures: Germany avoids triple-dip recession

Dutch Q3 GDP +0.2 QoQ on expectations of +0.3%

— Arne Petimezas (@APetimezas) November 14, 2014

Another picture of Angela Merkel in New Zealand, this time charming a kiwi.

Practising how to keep @David_Cameron calm? RT @noahbarkin: ... and comforting a grumpy Kiwi pic.twitter.com/SSRyZvvJqV

— Luke Baker (@LukeReuters) November 14, 2014

Updated

Just realised that the Dutch growth rate in the second quarter of 2014 has been revised down, to 0.6% from 0.7% originally.

Just in: the Netherlands economy slowed in the last three months.

Dutch GDP rose by just 0.2% in the July-September quarter, down from 0.6% growth between April and June.

Updated

Angela Merkel will have learned that Germany avoided recession during a trip to New Zealand:

#Mekel nose-kissing Maori during New Zealand visit pic.twitter.com/niyFOpeZXK

— Noah Barkin (@noahbarkin) November 14, 2014

The Slovak economy grew faster than expected - with GDP expanding by 0.6% during the quarter.

More GDP figures.... Hungary grew by 0.5% in the third quarter, matching the growth recorded in April-June.

On an annual basis, GDP rose by 3.2%, down from 3.9% three months ago. The country’s statistics body said there was a slowdown in the auto industry and in construction.

Updated

Britain’s government will be relieved that Germany has avoided recession (details start here), says Ed Conway of Sky News:

If there is one person who will almost as delighted as Angela Merkel, the German Chancellor, that the euro area’s two biggest economies are not in recession, it is George Osborne.

The last thing he needed ahead of a testy election campaign was a serious UK slowdown caused by factors entirely beyond his control.

But....

The fact remains that however much Britain increases its exports outside the EU, its economic fate will still be inextricably tied to that of the euro area.

And while the prognosis looks a touch brighter today, the long term outlook is hardly brilliant.

Germany dodges recession and George Osborne sighs. Analysis by @EdConwaySky : http://t.co/ikGCdPMpkF

— Sky News Business (@SkyNewsBiz) November 14, 2014

And the excellent George Magnus, UBS’s former chief economist, is equally downbeat:

Germany's 0.1% and France's 0.3% Gdp rise in Q3 hailed as some sort of victory in European game of whac-a-mole. Grinding nominal contraction

— George Magnus (@georgemagnus1) November 14, 2014

Kit Juckes, top currency analyst at Societe Generale, points out that the eurozone economy is still weak and troubling:

The underlying story, which is going to be with us for a long time, is of stagnation and of hopes of recovery repeatedly being dashed unless someone gets some policy-making heads and knocks them together.

Updated

Europe is experiencing a “Waterworld recovery”, says Alberto Gallo of RBS, and time is running out.

Speaking on Bloomberg now, Gallo’s explaining that it is a mistake to rely on liquidity from central banks to stimulate growth, rather than making structural economic reforms.

He warns that this can’t go on much longer, as inflation - and inflation expectations - are falling.

We are getting close to Japanification here, there’s not a lot of time left.

Updated

The Czech Republic has missed expectations, growing by 0.3% during the third quarter.

That won’t affect the eurozone growth figures, though, as the Czechs (like Romania) aren’t in the euro.

Romania’s economy grew by a healthy 1.9% in the third quarter of 2014, its statistics body just reported. That means it has expanded by 3.2% over the last year.

The euro has dipped in early trading against the US dollar, to $1.245.

#France and #Germany return to growth but Euro is not bothered. Common currency down 0.4% vs Dollar at 1.245. pic.twitter.com/FoJSrtw9ZN

— Holger Zschaepitz (@Schuldensuehner) November 14, 2014

Updated

We’re about to get another splurge of GDP data from smaller European countries, including Austria, Hungary, Romania and the Slovak and Czech Republics.

Updated

So why did Germany’s economy grow so weakly last quarter?

ING’s Carsten Brzeski has a few theories; including problems in major trading partners including China, France and Italy; and the Ukraine crisis which has hurt trade with Russia and dented business confidence.

But he also argues that “virtuous circle is coming to an end”.

The resilience of the labour market against the slowdown might not only be a sign of strength but also simply the last stage of Germany’s reform super cycle, which started more than ten years ago.

Updated

French finance minister: we need to grow faster

The French government has received today’s GDP figures cautiously, even though growth was a little stronger than expected last quarter.

France’s finance minister Michel Sapin has pointed out that growth of 0.3% isn’t enough to fix the country’s jobs crisis:

“Economic activity has picked up slightly but remains too weak to ensure the job creation our country needs.”

Updated

ING analyst Julien Manceeaux isn’t too impressed by this morning’s French GDP report.

He’s disappointed that growth in the second quarter was revised down to minus 0.1%.

Figures published this morning first showed that GDP growth in Q2 has been revised downwards to -0.1% after 0,0% in Q1.

This makes the small rebound [+0.3%] announced for Q3 a rather weak one, especially as it was mainly driven by stock accumulation and public spending.

The shine has been knocked off Germany’s second economic miracle, says Carsten Brzeski of ING.

He writes:

Almost all the glamour of the second German Wirtschaftswunder seems to be gone. Chances are high that after the release of the Eurozone data at 11am CET, today’s data mark the first time the German economy underperformed the rest of the Eurozone in two consecutive quarters since the doomy days of the crisis in late 2008 and early 2009.

Brzeski adds that the German economy has grown by an average of 0.2% QoQ each quarter since early 2013:

This makes the Eurozone’s powerhouse rather a one-eyed king in the land of the blind than an economic superman.

Updated

ABM Amro’s Nick Kounis has stuck his neck out, and predicted that the eurozone grew by 0.2% in the third quarter of 2014.

Given member states that have already reported, looks like eurozone GDP just scrapped 0.2 qoq in Q3 following 0.1 in Q2.

— Nick Kounis (@nickkounis) November 14, 2014

We get the overall eurozone growth figure at 10am GMT.

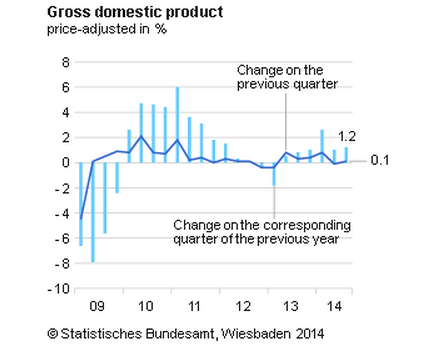

German GDP, the details

“The German economy turned out to be stable in a difficult global economic environment,” says its Statistics Office.

And the details of today’s GDP report show that consumer spending and trade are responsible for the 0.1% growth.

But (as with France) business capital investment fell during the last quarter, suggesting firms may have been spooked by the weak eurozone economy and the Ukraine crisis.

Destatis says:

Positive contributions were made mainly by households, which considerably increased their final consumption expenditure in the third quarter of 2014, according to provisional calculations. Foreign trade also supported the German economy. The increase in exports was higher than that of imports.

Consequently, the balance of exports and imports had a slightly positive effect on the GDP in a quarter-on-quarter comparison. By contrast, total gross fixed capital formation decreased.

Here’s the full report.

Some perspective from Bloomberg’s Jonathan Ferro -- Germany’s 0.1% growth is welcome, but it’s hardly a blast.

German avoids another recession... with growth of 0.1%. Yes, 0.1%. This is good news and that shoud tell you lots about Europe rght now.

— Jonathan Ferro (@FerroTV) November 14, 2014

Updated

Germany’s second-quarter GDP has also been revised upwards, to show a -0.1% contraction rather than the -0.2% first estimated.

The news that Germany has narrowly avoided a recession will sent relief through the global economy.

It also takes a little pressure off the European Central Bank to consider additional stimulus measures to stimulate the euro economy.

kein Schadenfreude as Germany avoids triple-dip.

— kit juckes (@kitjuckes) November 14, 2014

Germany avoids recession with 0.1% growth

Breaking: Germany has avoided recession, JUST.

German GDP grew by a measly 0.1% in the third quarter of 2014, having contracted in the previous quarter.

That’s broadly in line with expectations, and means that Europe’s largest economy has avoided the humiliation of a technical recession.

So, a turnaround, but not a great performance.

*GERMAN ECONOMY GREW 0.1% IN 3Q, MATCHING MEDIAN FORECAST

— lemasabachthani (@lemasabachthani) November 14, 2014

Next stop Germany after #France has beaten with Q3 GDP growth of 0.3% qoq. pic.twitter.com/IMogFsL2Fc

— Holger Zschaepitz (@Schuldensuehner) November 14, 2014

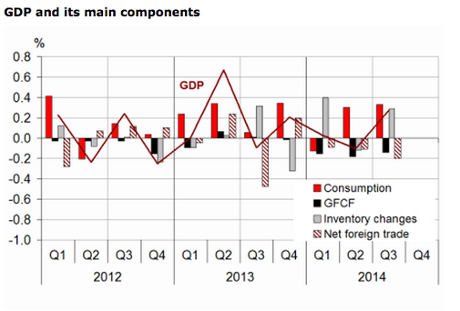

French GDP headline number better than details. Investment spending contracted further by 0.6% QoQ and inventories offset net exports drag.

— Frederik Ducrozet (@fwred) November 14, 2014

French GDP: Household spending up, net trade down

France’s growth 0.3% in the last quarter was driven by household spending and government spending. Companies restocking their inventories also helped.

But net trade, and capital investment (firms spending on new equipment etc), both fell again.

Details:

- Households’ consumption expenditure: up 0.2%

- General government expenditure: up by 0.8%

- Total gross fixed capital formation: down 0.6%

- Exports recovered, by 0.5%, while imports rose by 1.1%.

- That means that foreign trade made a negative contribution to GDP -- 0.2%

- Inventory building added 0.3% to GDP

France’s GDP report is online here.

Updated

Nick Kounis of ABN Amro confirms that French growth has beaten forecasts -- that’s a phrase I’ve not been able to write often, recently.

French GDP was better than expected at 0.3 qoq in Q3. Germany the big question mark but eurozone looks to keep head above water...

— Nick Kounis (@nickkounis) November 14, 2014

17 minutes until we get Germany.....

Updated

Frederik Ducrozet of Credit Agricole is excited that the curve of French GDP curve has been reversed.

Youpi, l'inversion de la courbe du PIB! *FRENCH ECONOMY GREW 0.3% IN 3Q; MEDIAN FORECAST 0.1%

— Frederik Ducrozet (@fwred) November 14, 2014

France’s 0.3% growth in the third quarter of 2014 is the strongest performance since 2011, says Mark Barton on Bloomberg TV.

He adds:

That shows you the state that the French economy has been in for the last four years.

*FRENCH ECONOMY GREW 0.3% IN 3Q; MEDIAN FORECAST 0.1%

— lemasabachthani (@lemasabachthani) November 14, 2014

French GDP rises by 0.3%

Here we go! France’s economy faster than economists expected in the third quarter of 2014.

GDP rose by 0.3% in the July-September quarter, beating expectations. That’s a rare piece of good news for president Hollande.

However, it’s not ALL good news. The GDP for the second quarter has been revised down, from 0% to minus 0.1%.

Still, a decent start to GDP Day.

Reaction to follow....

The Agenda: It's eurozone GDP day

Good morning. It’s time to discover how the eurozone economy performed in the third quarter of 2014, and the results may not be pretty.

Over the next few hours, GDP data from across the single currency will be released by national statistics bodies. This data will then show how well, or badly, the region performed.

Economists believe the data will confirm the eurozone economy struggled over the summer, with domestic weakness and geopolitical crises overseas hitting growth.

The big question is, how badly did Germany do? It’s economy shrank in the second quarter of this year - another contraction would mean a technical recession.

Here’s the order of business:

-

France: 6.30am GMT (7.30am CET)

-

German: 7am GMT

-

Austria, The Slovak and Czech Republics, Hungary and Romania: 8am GMT

-

The Netherlands. 8.30am GMT

- Italy: 9am GMT

- The whole eurozone 10am, along with the eurozone inflation figure for October

A poor morning’s results will put more pressure on the ECB to take unconventional actions to stimulate the eurozone. Hold onto your hats......