European markets close lower after recession news

European markets have closed, and with the eurozone in recession it's not surprise that it's been another down day.

Worries about the US fiscal cliff and tension in the Middle East have also combined to unsettle investors.

• The FTSE 100 is down 0.77% or 44.26 points to 5677.75

• Germany's Dax has fallen 0.82%

• France's Cac has closed 0.52% lower

• Italy's FTSE MIB has finished down 0.59%

• The Athens market is 0.84% lower

• But Spain's Ibex has bucked the downward trend, up 0.29%

On that note, it's time to draw things to a close. Thanks for all your comments and we'll be back tomorrow.

Greece calls for details of citizens' offshore accounts with HSBC

Over in Greece there appears to be movement on the tax evasion front, reports our correspondent Helena Smith

With Greek baying eor punishment to be meted out to tax cheats, the country's finance minister Yiannis Stournaras has today written to George Osborne asking for further information on Greek citizens who were recently revealed to hold offshore accounts with HSBC in the channel isle of Jersey.

"We had no idea about their existence and were surprised when their names were included on the list recently made public by HSBC," said a senior finance ministry official. "The minister sent the letter because he wants to get to the bottom of it. Tax evasion is one of our biggest problems."

An estimated 57,000 Greeks are believed to have transferred banks deposits abroad since the debt crisis' oubtreak in Athens in late 2009.

In a separate development, the finance minister announced that the country was also poised to dispatch letters to some 15,000 Greeks who moved a €5bn abroad without declaring it to tax authorities. "More than €2bn of that amount could be recouped in taxes," said the finance ministry official. "Ordinary Greeks who are suffering from so much austeirty want to see some action."

Germany's Merkel repeats opposition to Greek debt haircuts

German chancellor Angela Merkel has once again rejected the idea that governments should take a loss on their loans to Greece.

While calling on European finance ministers to find a quick solution to Greece's financial problems she told reporters at a joint press conference with French prime minister Jean-Marc Ayrault:

I hope the time is near when we can reach the solution that is needed. Of course we did not talk about debt haircuts, you know our view and that has not changed, nor should it.

According to Reuters, Ayrault added:

The moment of decision regarding Greece is approaching. The important thing is to do everything to keep Greece in the eurozone, there is a consensus on this essential point.

Not everything surely, if debt haircuts have been ruled out.

More downbeat news from the US. The Philadelphia Federal Reserve's index of business confidence fell by 10.7 points in November, compared to a 5.7 point rise in October, the worst result since July.

Hope for Greece from IMF?

Could there be a breakthrough with Greece? A spokesman for the IMF has said it has done what it could to help the country reach debt sustainability.

According to Reuters, IMF spokesman William Murray told reporters:

Clearly there have to be other actions taken to reach debt sustainability.

That seems to mean Greece's European lenders need to do more but he would not spell out what actions were necessary. The IMF wants lenders to write-down some of their debt, something Germany for one is not happy with.

Then came this:

IMF’s spokesman says IMF has extended debt maturity and lowered rate on Greece debt

— Fabrizio Goria (@FGoria) November 15, 2012

Update

It seems the extended debt maturity refers to past rule changes, not a new development. Oh well, we could hope...

IMF headline on Greek debt "lower rates" simply relates to change in IMF rules in 2011 under "NAB" imf.org/external/np/se…

— Owen Callan (@OwenCallan) November 15, 2012

Eurozone woes could push Denmark into recession

Back with recession watch, Denmark is likely to join those reporting an economic downturn, according to its finance minister.

In an interview with Reuters, Bjarne Corydon said the third quarter could see a second successive fall in output, following a 0.4% decline in the previous three months. This meets the technical definition of a recession.

He said economic growth for the whole year could fall short of the government's forecast of 0.9%, but he expected a rebound to 1.7% in 2013. He said:

Our general view is that 2012 is going to be a disappointing year, mostly just because of the developments in Europe... and sustained uncertainty over the eurozone.

Mario Draghi's speech which we referred to earlier has been published in full on the ECB website.

More on Spain's decision to help people struggling with their mortgage payments. Martin Roberts in Madrid writes:

Spain’s cabinet has just passed a decree freezing the final stage of seizing homes for two years for the most needy following public outrage over recent suicides of people who were about to be evicted.

Economy Minister Luis de Guindos said families earning up to €1,597 a month will be eligible, as will large families, or those with children aged under three or disabled dependants. Unemployed debtors or those not eligible for unemployment benefit will also be covered.

“The overdue rate on mortgages is above 3%. There are many people who punctually meet their mortgage payments,” de Guindos told a news conference after the cabinet meeting. “The decree is for especially vulnerable members of society. The government thinks it is urgent to defend them.”

De Guindos also gave details of the “bad bank” due to be set up this month to pick up toxic assets from Spain’s ailing banks, a pre-condition for receiving funds from a European bailout worth up to €100 bn.

“The company (bad bank) will have a máximum limit of €90 bn although the amount is expected to be around €60 bn,” de Guindos said. “The average price adjustment at which assets will be transferred from Banks to the holding company will be 50%.”.

US jobs, inflation and manufacturing figures disappoint

Disappointing data from the US, although Hurricane Sandy can shoulder some of the blame.

The number of people making new claims for jobless benefits rose to an 18 month high last week, up by 78.000 to 439,000, well above the forecast of 375,000. Meanwhile consumer prices rose 0.1% in October - partly due to a rise in rent charges - and manufacturing activity in New York state slowed in November for the fourth month in a row.

US futures - showing a 14 point decline before the figures - are now down 26 points.

Spain approves two year suspension of forced evictions

Back with Spain, and the government has just approved a plan to suspend forced evictions for two years for the most needy who are no longer able to pay their mortgages.

More soon.

With the eurozone in recession, here's a graphic showing GDP growth (or lack of it) among a number of major economies, including the US as well as Europe.

IMF's Lagarde to cut short Asia trip to attend eurogroup meeting

IMF head Christine Lagarde will have to pass up the joys of Cambodia for (yet another) meeting in Brussels next week.

She is currently on a visit to Asia but has cut this short to head back for more talks about tackling the eurozone crisis. IMF spokesman Gerry Rice, quoted on Reuters, said:

The managing director will participate in the eurogroup meeting on 20 November as she usually does and that will mean shortening her current trip to Asia.

She was due to attend a meeting of ASEAN nations early next week, but she may face a more fractious get-together instead. At a news conference in Brussels earlier this week, disagreements between the IMF and the eurogroup flared up. Eurogroup chairman Jean-Claude Juncker said Greece should be given extra time to lower its debt-to-GDP target, while Lagarde wanted the country to meet its original target.

The latest hope is that Tuesday's meeting will finally give the go-ahead for Greece's aid package, which would at least be something.

But the disagreements are nowhere near resolved. According to Belgian paper De Standaard ECB governing council member Luc Coene said today that part of Greece's debt would probably have to be writen down to help solve the country's problems. This is anathema to the likes of Germany, of course, which has repeatedly rejected the idea.

Coene also reportedly said Spain urgently needed a bailout.

Earlier there were reports that Spain could be seeking help directly from the IMF rather than a bailout, but this appears to have been denied by the country's economy secretary Fernando Jimenez.

Protests against German diplomat in Greece

It appears that a German diplomat was involved in an incident with irate citizens in Greece today, as anger against Berlin boiled over.

Protesters in Greece's second city, Thessaloniki, have hurled coffee at a German diplomat amid resentment over austerity measures advocated by Berlin.

They broke into a conference centre where mayors of Greek and German cities were due to meet.

It was not immediately known if the diplomat had been hurt.

The incident was provoked, I think, by comments made by German deputy labour minister Hans-Joachim Fuchtel. He claimed that studies had found that 1,000 German local civil servants could do the work of 3,000 Greeks.

This video clip appears to show German Consul Wolfgang Hoelscher-Obermaier being targeted today

That's via Keep Talking Greece which has more details.

And on that note, I've got to dash so Nick Fletcher has the controls.... Thanks all. GW

Mario Draghi urges leaders to act now

While we were digesting the news of the eurozone recession, European Central Bank president Mario Draghi was making another attempt to urge policymakers to resolve the crisis.

Speaking at Bocconi University in Milan, Draghi warned that the current market calm will not last for ever.

Leaders must take advantage of the lull to dispel once and for all the uncertainties that hang over the single European currency, he added.

Here's Draghi's key quote:

With the ECB unconventional measures, we have been able to steady the course...We have gained precious time, but this is not infinite.

It's now almost four months since Draghi declared that the euro was irreversible. He must be frustrated that little has been achieved since.

We still don't even have a decision on Greece's aid package - although I see that German Finance Minister Wolfgang Schaeuble has just announced that this will definitely happen next Tuesday....

Greece won't default tomorrow

Greece has definitely dodged the risk of defaulting tomorrow. This morning Athens raised nearly €940m in short term bonds. Added to the €4.1bn of bills sold on Tuesday, and it has the resources to cover the €5bn debt that matures on Friday.

Panic over

German immigation rising

As RobertSchuman pointed out in the comments below, new data has shown rising immigration in Germany, with another half a million people arriving in Europe's biggest economy in the first half of 2012.

My colleague Nadine Schimroszik has looked into it, and notes that the number of people that moved to Germany from recession-hit Greece, Spain and Portugal rose more than 50% compared to a year earlier.

Nadine adds:

According to provisional results from the Federal Statistical Office today, the number of Greeks that immigrated jumped by 78%.

The immigration from Spain to Europe’s biggest economy increased by 53%, exactly the same with Portugal. All three countries are struggling with massive austerity measures and very high unemployment rates.

Overall, 501.000 people moved to Germany from January to June, and the majority were EU citizens. That is an increase of 15% compared to 2011.

Guardian readers share protest photos

Many thanks again to everyone who has shared their photos from yesterday's pan-European protests -- more have been arriving today.

My colleague Hannah Waldram has now created a handy gallery to let you browse them:

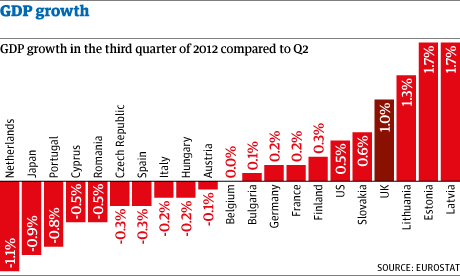

Eurozone recession round-up

Here's a round-up of today's quarterly GDP data by country (it's not exhaustive as several countries haven't released data yet).

Belgium: 0.0%

Bulgaria: + 0.1%

Czech Republic: - 0.3%

Germany: + 0.2%

Estonia: +1.7%

Spain: - 0.3%

France: + 0.2%

Italy: - 0.2%

Cyprus: - 0.5%

Latvia: + 1.7%

Lithuania: + 1.3%

Hungary: - 0.2%

Netherlands: -1.1%

Austria: -0.1%

Portugal: - 0.8%

Romania: - 0.5%

Slovakia: +0.6%

Finland: + 0.3%

United Kingdom: +1.0%

Larry Elliott: worse ahead for the eurozone

Our economics editor, Larry Elliott, warns that the eurozone is likely to keep contracting in the fourth quarter of 2012, perhaps by as much as 0.5%.

He writes:

Clearly, parts of the Euro Zone are suffering grievously from slow growth, frighteningly high levels of unemployment and falling living standards.

The fact that euro zone GDP still fell even when Germany and France were growing indicates that activity was falling quite fast in some of the smaller economies. The problems of Greece, Spain, Portugal and Italy have been well documented: the worry in today’s numbers was that “core” countries like Austria and the Netherlands saw their economies shrink in the third quarter.

For Angela Merkel and Francois Hollande, the worrying message from the data is that the contagion is spreading from the periphery to the core.

Larry points out that the prospects not much brighter for next year.

Greece has just signed up to another batch of spending cuts, the Spanish economy is in freefall and Germany will continue to struggle all the while world trade remains weak. European banks remain in a parlous state and would go under without life support from the European Central Bank and national governments. The first half of 2013 will be grim.

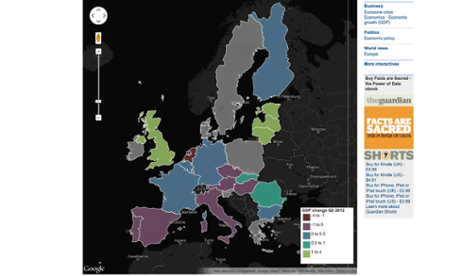

Interactive Map of today's GDP data

My colleague @nickvanmead had swiftly created an interactive map showing today's GDP data for the whole EU.

It lets you see which countries are back in recession, and which are still managing to grow. Click here to see it: Eurozone falls back into recession

Analyst views

Howard Archer of IHS Global Insight points out that the eurozone has effectively been in recession for some time, even if GDP data only confirmed it this morning. Unemployment, for example, has been hitting new double-digit record highs for months.

Archer adds:

Latest data and survey evidence remain generally weak, and the odds currently strongly favour the Eurozone suffering further GDP contraction in the fourth quarter of 2012. Significantly, Germany looks to be in severe danger of contracting in the fourth quarter, as does France.

And Jennifer McKeown of Capital Economics said:

The business surveys point to far worse to come throughout the region in the fourth quarter. With austerity starting to hit French households and German unemployment beginning to rise, the outlook for domestic spending is bleak even in the core.

Official details

Eurostat's official statement announcing that the eurozone is in recession is online here.

Early reaction to the eurozone recession

The news of the eurozone recession hasn't spooked the markets, although there had been some optimism this morning that the growth in Germany and France might help the region dodge a second contraction.

Here's some early reaction from economists and analysts:

Eurozone gdp -0.1% in Q3. Back in recession. Euro having a reasonably good day. Gloom is deep. No one is surprised. Can get worse tho.

— kit juckes (@kitjuckes) November 15, 2012

The euro zone dodges disaster in Q3, but doesn’t rebound. GDP growth is not fast enough to make debt problems melt away, says @edwardhadas.

— ReutersBreakingviews (@Breakingviews) November 15, 2012

Dear #EU leaders, if you don't change course now, I will call the headmaster from my catholic school who'll box ur ears as only he knows how

— Sony Kapoor (@SonyKapoor) November 15, 2012

How eurozone slid into a double-dip

This is the second time that the eurozone has tumbled into recession since the financial crisis began in 2008.

It has been inching towards a slump since the euro crisis flared up a year ago, as this quarterly GDP data shows:

Q3 2012: -0.1% (just released)

Q2 2012: -0.2%

Q1 2012: 0%

Q4 2011: -0.3%

On a year-on-year basis, the eurozone economy is now 0.6% smaller than a year ago, driven by the slump in peripheral economies.

The wider European Union managed growth of +0.1% during the last three months, so has shrunk by 0.4% over the last 12 months.

Official: Eurozone in recession

The eurozone is officially in recession!

Eurostat has just reported that GDP fell by 0.1% in the third quarter of the year. That follows the 0.2% contraction in the previous three months - and means the eurozone is in its second recession since the financial crisis began in 2008.

More to follow

Will strikes make a difference?

Yesterday's strikes mass and protests may have been dramatic, but the Wall Street Journal questions whether it will force a change of direction in Europe:

The WSJ reckons that leaders are "inured to protests" after four years of economic distress, adding:

Protest fatigue, declining levels of unionization and factionalism within the labor movement have combined to take much of the bite out of strikes as tools for changing government policy, analysts said.

More here: Big Europe Strikes Have Little Effect

Surprise fall in UK retail sales

UK retail sales took a nasty fall in October, down 0.8%.

The data, just released, suggests Britain is weakening. The Office for National Statistics said consumers cut back on clothing, food and fuel – all signs of people hunkering down.

We'll have a full story shortly.

More on the Dutch slump

This morning's dire GDP data from the Netherlands (a 1.1% contraction in just three months), appears to be clear evidence that the eurocrisis has now struck deep at the previously-secure North:

Some fools thought crisis could be contained RT @djfxtrader: Dutch Economy Contracted 1.1% in Third Quarter

— Yiannis Mouzakis (@YiannisMouzakis) November 15, 2012

Core. RT @djfxtraderDutch Economy Contracted 1.1% in Third Quarter

— Matina Stevis (@MatinaStevis) November 15, 2012

Italian GDP better than expected

Another twist - Italy's GDP has beaten expectations.

The Italian economy shrank by 0.2% in the third quarter -- a much smaller decline than the 0.8% slump suffered in Q2.

That's an encouraging sign - and may suggest that the euro area manages to dodge recession (we'll find out in an hour)

Netherlands economy in trouble

Some alarming data from the Netherlands -- its GDP tumbled by 1.1% in Q3, compared to the previous quarter. Economists had only expected a decline of 0.2%.

The Dutch economy has already been in, and out, of recession twice since the crisis began. It appears to be heading into another slump:

AAA-rated 5th largest € #Netherlands close to triple dip recession: Q3 GDP plummets -1.1% est -0.2%, unemployment rsises to 6.8% vs est 6.7%

— Linda Yueh (@lindayueh) November 15, 2012

Austria's GDP drops 0.1%

Bad news for Austria - it's GDP fell by 0.1% in the last quarter; its first quarterly contraction since the financial crisis began in 2008.

Austria had appeared immune from the worst effects of the euro crisis, with unemployment rates below 5% - but it's another sign that Europe's core is now being hit.

Spanish recession confirmed

Spain's economy shrunk by 0.3% in the last quarter, officials confirmed this morning. That's in line with the provisional data released earlier this month.

Finland shrinking

Finland's statistics office has reported that the country has shrunk by 1% over the last 12 months, based on September's GDP.

Full quarterly data wasn't released.

Economists had expected that today's data would show that the eurozone shrank by -0.1% in the last quarter, following the 0.2% contraction in the previous three months.

That would mean recession. However, the better-than-expected data from France and Germany has prompted some rethinking.

Germand & French GDP better than expected. Are EZ forecasts for 10am too low?

— Mike van Dulken (@Accendo_Mike) November 15, 2012

We'll find out at 10am GMT.

UK AAA rating at risk

The UK actually grew five times faster than France or Germany in the third quarter (The Olympics helped Britain expand by 1% between July and September).

But before local readers dig out the Jubilee bunting, we should note that Moody's warned late last night that it will revisit the UK's AAA rating early next year.

Larry Elliott, our economics editor, explains that Moody's will probably strip Britain of its prized triple-A if the country sinks back into recession.

In its annual health check on Britain, Moody's served notice to the chancellor that it would be carefully monitoring how he managed the difficult balancing act between growth and deficit reduction over the coming months.

The ratings firm said it had not yet decided whether to cut Britain's credit rating but said it could act in the new year either if growth prospects worsened or if Osborne failed to stick to a demanding timetable for reducing national debt.

Germany slowing, but still growing

Europe's biggest economy is clearly feeling the effects of the eurozone crisis, but it's refusing to buckle.

Germany's growth of 0.2% in the last quarter is weaker than Q2's +0.3%, or the 0.5% in the first three months of the year. But it's also stronger than the meagre 0.1% growth economists had expected.

Germany's statistical office said foreign demand made "positive contributions" to gross domestic product in the third quarter, with private consumption also higher.

Carsten Brzeski, ING economist, said Germany's strong labor market, wage increases and exports were all keeping it afloat.

The crisis denier. German economy grew 0.2% QoQ in 3Q and shows similarities with national soccer team... bit.ly/RZsNQG

— Carsten Brzeski (@carstenbrzeski) November 15, 2012

France beats forecasts

City experts had predicted another quarter of flat GDP for France, but actually its economy posted rare growth - 0.2% in the last quarter.

It's not all good news - GDP for the second three months of 2012 was revised down to -0.1%. But still no recession.

It's a much-needed tonic for president François Hollande, whose attempts to implement spending cuts and labour reforms have killed his post-election honeymoon.

Viva La France econony actually expands

— Steve Collins (@TradeDesk_Steve) November 15, 2012

Eurozone growth figures released today

Good morning, and welcome to our rolling coverage of the eurozone financial crisis, and other major events across the world economy.

After Wednesday's public protests, today is much more about economics -- has the eurozone fallen into recession?

GDP data for the third quarter of 2012 is being released this morning – and the early numbers are surprisingly positive.

France's economy expanded by 0.2% in the third quarter, defying predictions that it would finally slide into recession.

And in the last few minutes, Germany has also reported 0.2% GDP growth between July and September. That's a slowdown on earlier in the year, but still growth.

So it's possible that the eurozone may be in better shape than economists feared.

We'll be tracking the data all morning, along with full reaction to yesterday's protests (if you missed them or want to relive the drama, yesterday's live blog covers the full story - from pre-dawn protests to the final rally in Madrid).

There's also a meeting between Mario Draghi and Mario Monti in Milan today.