And finally (probably), the Syriza party has released an 8-page statement saying draft legislation regarding the re-opening of the state TV channel ERT will be put to parliament on March 5th. No dates were given for other reforms.

As we reported this morning, sources reckon some bills will be held back until after Monday night’s eurogroup....

That’s all from us, unless anything dramatic happens. Thanks, as ever, and goodnight, GW

Greece’s Mega TV on its flagship evening news programme is now reporting that euro group officials have suggested the money needed to cover the looming IMF loan (€1.5bn) could be forthcoming if Greece comes up with “convincing reforms” at next Monday’s meeting.

Ie, reforms that could take immediate effect such as a privatization of some kind or the announcement of new taxes (Helena adds)

Updated

Over in Athens Greece’s Labour Minister has announced that the €751 minimum wage will be re-instated in installments, with the first being delivered this year.

Previously, Skourletis had said the minimum wage would be re-introduced sometime in 2016 - so the news is likely to be well greeted, says Helena Smith, our correspondent, who adds:

The former Syriza party spokesman told BHMA FM radio station that collective work agreements - a major demand of unions - would also be brought back. Both were central to the radical left party’s pre-election campaign program.

Greece’s creditors shouldn’t take fright. In the documents sent to Brussels last week, Athens agreed to “streamline and over time raise minimum wages in a manner that safeguards competiveness and employment prospects.”

Meanwhile.....

#Greece playing up its geopolitical status: "we could have a bridge role between Europe and Russia," says Greek foreign min

— Helena Smith (@HelenaSmithGDN) March 3, 2015

The Greek public, on balance, back the stance taken by their government in the bailout talks -- particularly finance minister Yanis Varoufakis.

That’s according to a poll for Star TV tonight:

#MRB poll: 70.4 pct have positive view of handling by FinMin #Varoufakis #Greece

— Kathimerini English (@ekathimerini) March 3, 2015

MRB poll for Star TV Would you have liked govt to take tougher stance in talks even if it led to euro exit? No 59.8 Yes 38.4 #Greece

— MacroPolis (@MacroPolis_gr) March 3, 2015

#MRB poll: 52.2 pct against gov't taking a tougher stance if it were to lead to capital controls #Greece

— Kathimerini English (@ekathimerini) March 3, 2015

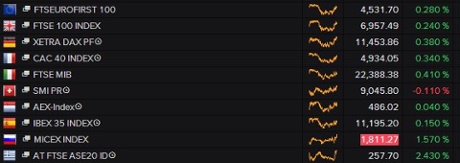

The blue-chip FTSE 100 index is down 40-odd points, or 0.7%, in late trading:

FTSE soggy -46 @ 6894 - Barclays -3.25%, Direct Line -0.7%, Travis Perkins -4%, Moneysupermarket -10%, Pace +8%, Ashtead -1%, Glencore -3%

— David Buik (@truemagic68) March 3, 2015

Barclays may also have to put banking scandals behind it before trying to persuade customers to pay for current accounts.

As Japer Lawler of CMC Markets reminds us, this morning’s results were tainted by mistakes of the past:

Shares in Barclays dropped after the bank reported an annual net loss having put aside an extra £750m for FX rigging fines and £200m for insurance mis-selling.

Excluding exceptional costs Barclays turned a profit but the underlying business cannot come to the fore with no end in sight for litigation.

Updated

Successful prosecution of former Morrison Treasurer Paul Coyle by FCA for insider dealing is first time for a former FTSE100 exec

— Giles Turner (@turnergs) March 3, 2015

Chief executive of @Barclays tells @itvnews he wants end to "free" current accounts in interests of transparency. http://t.co/PKGD326BFw

— Joel Hills (@ITVJoel) March 3, 2015

Legal news. The former Group Treasurer and Head of Tax at Wm Morrison Supermarkets plc, has been jailed for 12 months for insider dealing.

Paul Coyle, who today pleaded guilty to 2 counts of insider dealing, was also ordered to pay £15,000 towards prosecution costs and a Confiscation Order in the sum of £203,234.

The Financial Conduct Authority explains:

Between 24 January and 17 May 2013 Coyle, through his role at Morrisons, was regularly privy to confidential price sensitive information about Morrison’s ongoing talks regarding a proposed joint venture with Ocado Group plc.

Coyle took advantage of this information by trading in Ocado shares between 12 February and 17 May 2013 using two online accounts which were in the name of his partner.

Barclays CEO: Free current accounts may have to go

Back in the UK, the boss of Barclays has suggested that the era of free current accounts should end.

Antony Jenkins made the comments in an interview with ITV News’s business editor Joel Hills, after Barclays reported its result this morning.

It’s being shown tonight (6.30pm on ITV 1); here’s a flavour:

Joel Hills: In terms of switching rates being so low and some people have suggested that charging for current accounts, upfront charges for current accounts would actually eliminate some of the competition issues, where do you stand on that? Is it a good idea?

Antony Jenkins:

Well as you know there is going to be a big investigation into the current account market. I have always believed, since this was first introduced in the 80’s, that not having a price point, if you like, around the current account, was probably not helpful for consumers because it’s very hard to make a judgement about something when there’s no price attached to it. So broadly speaking, I think having a bank account that there is a price point for is a positive. Now there already are bank accounts that have that quality to them, but it’s not across the whole system and I think...

Joel Hills: That’s what we want to see?

Antony Jenkins:

I do think that that would be a step forward, yes. It’s difficult to achieve of course because the banks can’t do that, it would probably have to be regulated or legislated.

Joel Hills: Why couldn’t the banks do that?

Antony Jenkins:

Well because we’re not allowed to work together on matters like this, for good reason.

Joel Hills: And if one of you went?

Antony Jenkins:

That’s the other problem, if one of us moved to a charging model it would be likely that we’d lose a lot of business because people would go to the free model.

It’s an important issue (although I’m not sure Jenkins should be proposing we all pay for banking services straight after getting a multi-million pound pay packet). Hopefully the ongoing competition inquiry into Britain’s banks will make some progress on it.

Stephen Lewis, chief economist at ADM Investor Services, isn’t surprised that more investors now believe Greece could leave the eurozone over the next year.

He cites two reasons.

1) Greece’s country’s financial position has weakened significantly during 2015:

The budget numbers Athens reported for January were seriously off target, leaving ground to be made up if the primary budget surplus is to meet the level specified in Greece’s second bailout agreement. However, there is every reason to suppose that the budget numbers for February were just as bad as January’s, seeing that the political and financial uncertainty that dampened business activity in the first month of the year continued after Syriza’s 25 January election victory.

2) The new government has upset other eurozone partners, making negotiations over a new bailout trickier:

Trust between the Greek government and its creditors was damaged when Mr Varoufakis was reported to have described his agreement with the Euro Group on 20 February as a clever form of words. To his fellow finance ministers, his remark did not appear to signify the serious intent to take reforming measures that they had expected. More damaging still was Mr Tsipras’s claim last week that Spain and Portugal had formed a hostile axis against Greece. Both right-wing governments in those countries were, he said, fearful that, if Greece were granted concessions, their own voters would switch their allegiance to political parties ready to fight for similar treatment. While what Mr Tsipras said may very well be true, the breach of EU protocol will not be easily forgotten.

Mr de Guindos, Spain’s finance minister, spoke out of turn yesterday, claiming that the euro zone finance ministers were considering a €30bn-50bn third bailout package for Greece. Mr Dijsselbloem’s office has been unwilling to provide any confirmation that talks are under way on this matter; he wants to avoid complicating matters.

Spain’s government does have its own problems, though:

"Come on #Tsipras" : brilliant #cartoon by @georgopalis #Greece #Spain #Syriza #Podemos #Rajoy pic.twitter.com/SroajMtsEg

— Olivier Drot (@OlivierDrot) March 3, 2015

Greek financial news site Capital.GR reports that Yanis Varoufakis held a conference call with officials from Greece’s creditors today:

A teleconference btwn #Greece FinMin and Costello, Mazuh, Goyal (troika), took place earlier today via @capitalgr http://t.co/QfsbEpaTj1

— Efthimia Efthimiou (@EfiEfthimiou) March 3, 2015

That’s Rishi Goyal of the International Monetary Fund, Declan Costello of the European Union, and Klaus Mazuh of the European Central Bank.

So, the same three institutions are keeping an eye on Athens, even though the hated “Troika inspections” have apparently been abolished.

We should keep "troika" for tweeting purposes. #Greece

— Tom the Observer (@typicalexpat) March 3, 2015

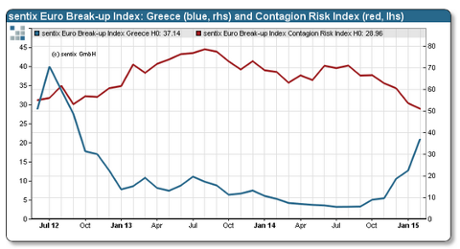

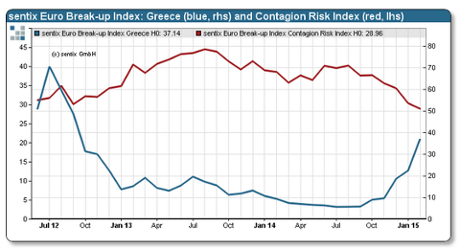

Lunchtime summary: Grexit fears on the rise

Time for a recap.

It’s been another day largely dominated by Greece, after a new report found that almost 40% of investors expect at least one member of the eurozone to break away this year.

Research firm Sentix’s euro break-up index jumped to 38% this morning, from 24% a month ago. That’s a two-year high. The group warned:

The development is driven by a clearly worsening assessment of investors concerning Greece....

Despite the solution which was found last week for Greece ever more investors expect the Mediterranean country to leave the euro soon.

Grexit fears are now their highest since late 2012, and will dominate the markets for months, Sentix added.

As Greek rumblings continues ever more investors expect #Greece to leave Euro. #Grexit risk at 37%, highest since '12 pic.twitter.com/hlrDNMDaQT

— Holger Zschaepitz (@Schuldensuehner) March 3, 2015

Peter Schaffrik, head of European rates strategy at RBC, agrees that Greece’s bailout extension alone had not removed fears that Greece could quit the euro area:

“So far there is an agreement in principle, but have they really made substantial progress? I’m not so sure.... What we need is implementation, and for both sides to live up to expectations, and then we can become a bit more relax.”

Greek government sources have told us today that the government may not present its new reform proposals until next week. A delay would allow the government to make progress at Monday’s meeting of eurozone finance ministers.

Finance minister Yanis Varoufakis (when not blowing kisses to motorcyclists) has played down calls for Greece to return to the drachma.

He’s also promised that Greece will do everything possible to meet its debt repayments this month.

And the EU has denied that a third bailout is being developed.

Meanwhile, the wider European economy appears to be recovering -- German retail sales have smashed forecasts, while Spanish unemployment fell in February.

But European firms have reported falling prices for their goods at the factory gate, suggesting deflation fears may linger.

Syriza MP Costas Lapavitsas’ observation that Greece’s best hope, now, is to leave the euro [see 8.11am post] has not gone without comment in Athens.

Helena Smith reports:

The noted London University economics professor, who has moved back to Greece to represent the radical left Syriza in parliament, was quickly taken to task by none other than fellow academic Yanis Varoufakis.

The Greek finance minister quipped that:

“Lapavitsas has built an entire career on the return of the drachma,”

Rumblings in the ivory towers are not new. Syriza has more academics in its ranks (many tenured professors abroad) than any other party, with a good few holding strident differences of opinion.

Lapavitsas belongs to the far left camp of Syriza; “The extra parliamentary left,” he recently told me.

Varoufakis, in stark contrast, has described himself as “an erratic Marxist” and, as such, has shown an uncanny ability to cherry pick his way through policies (his views on Greek privatisations are the polar opposite of those held by the far left).

Lapavitsas admitted he would do things differently (if he were ever in Varoufakis’ shoes, which the media here is quite convinced he would like to be), but went out of his way to speak kindly of the new finance minister when we talked last month.

He told me that:

“Yanis Varoufakis has found himself in a position of pressure that no Greek fiannce minister has found himself in for five years...

He is a good economist with a strong pedigree and wide experience of the world economy.”

And a fine line in Twitter corrections...

@Hugodixon Only I never said that Hugo.... Your Greek needs some brushing up (or better sources)

— Yanis Varoufakis (@yanisvaroufakis) March 3, 2015

Updated

Greek bonds have rallied this morning, pushing down the yield (or interest rates) on the debt.

The yield on Greek 10-year bonds has dipped to 9.76%, from 9.9% last night, meaning its value has risen.

FastFT reckons the rumours of a third bailout for Greece is calming fears of a default (Yanis Varoufakis’s promise to present solid reform plans at next Monday’s eurogroup meeting may also help)

Greek bonds rally after talk of third bailout http://t.co/UjBnCIqLLl

— fastFT (@fastFT) March 3, 2015

More from the Treasury committee.....

Carney admits the Bank's rep has "taken a knock" as a result of the forex rigging scandal. "It hasn't been a pleasant experience".

— Angela Monaghan (@angelamonaghan) March 3, 2015

Carney tells MPs the Bank has made "fairly radical changes" to the way it deals with market intelligence in light of forex rigging scandal

— Angela Monaghan (@angelamonaghan) March 3, 2015

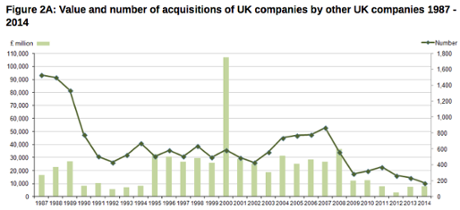

Factoid of the day: the number of takeovers involving UK companies has hit its lowest level since records began in 1987.

That’s mainly due to a steady decline in the number of acquisitions of British companies by other UK firms in recent years. More here.

Total M&A activity involving UK companies fell in 2014 to lowest numbers since records began http://t.co/hnwgv24ib1 pic.twitter.com/iJx710QfHk

— Alberto Nardelli (@AlbertoNardelli) March 3, 2015

Mark Carney has conceded that the Bank’s chief currency dealer, Martin Mallett, would probably have been fired over the FX scandal, if the BoE hadn’t found other reasons to dismiss him (the day before its report was published....)

Carney asked by MP Jesse Norman whether he would have fired Mallett on Grabiner findings alone. His answer (in short) was yes.

— Angela Monaghan (@angelamonaghan) March 3, 2015

Carney says that if Mallett hadnt been fired for other violations, in his opinion, Mallett should've gone for not escalating forex issues

— James Titcomb (@jamestitcomb) March 3, 2015

Mallett's 20 failings took place over an 8 year period according to Carney #bbcnews

— Ramzan Karmali (@RamzanK) March 3, 2015

The European Union has reiterated that they’re not working on a third bailout for Greece (as Spain’s finance minister suggested yesterday).

EU SPOKESWOMAN SAYS WORK HAS NOT STARTED ON THIRD GREEK BAILOUT

— Jonathan Ferro (@FerroTV) March 3, 2015

Governor Mark Carney is adamant that the Bank of England has seriously beefed up its market intelligence operations since it learned that foreign exchange traders had been manipulating the FX market:

Carney says BoE has improved professionalisation now e.g. Bank staff have 'escalated' 50 concerns, 40 of which have been referred to the FCA

— Angela Monaghan (@angelamonaghan) March 3, 2015

Carney says Bank has improved market intelligence gathering approach. Separating the "gossip" from strategic issues.

— Angela Monaghan (@angelamonaghan) March 3, 2015

Carney: Bank is expanding its market intelligence team from 10 full-time staff to 15.

— Angela Monaghan (@angelamonaghan) March 3, 2015

After an early rally, the London stock market has subsided with the FTSE 100 up just 5 points.

Barclays is now the biggest faller, down 3% after investors digest its drop in statutory pre-tax profits and new provisions for banking scandals.

Foreign exchange rigging fines weigh on Barclays results http://t.co/XqNIFyTP1t

— Jill Treanor (@jilltreanor) March 3, 2015

Mining stocks are also down, after Glencore cut the value of some assets.

David Madden, market analyst at IG, sums up the mood in the City this morning:

There is a sense of déjà vu in London after the market got off to a strong start only to be brought back down to Earth by the commodity stocks. Taylor Wimpey shares hit a new seven-year high after the homebuilder more than doubled its dividend. The company kept up with its competitors by posting a steady increase in annual profits and a solid start to the spring selling season. The Help to Buy scheme and a more regulated mortgage market will keep the housebuilder happy.

Barclays registered a 12% increase in underlying pre-tax profits, but when you consider the provisions set aside for PPI and FX manipulation it swings to a 21% drop in profits. The bank may be at its strongest ‘since the financial crisis’ but the fines and provisions have detracted from the company’s balance sheet. Barclays’ capital structure isn’t under question, and as long as legal costs loom over the bank the share price will remain restricted.

Glencore’s shares are back below 300p after the mega miner took a hit of over $1.1 billion due to asset write-downs. The trading division delivered a 15% increase in earnings, but it wasn’t enough to prevent core profits slipping by 2% on the year. The company reduced its net debt position to lessen its over-dependence on loans, but the cash flow situation is still strong enough to raise its dividend.

MPs now asking whether the terms of reference for Grabiner's review went far enough. Carney says he wasn't involved with striking terms.

— Angela Monaghan (@angelamonaghan) March 3, 2015

Back in parliament, Bank of England governor Mark Carney has defended the official inquiry into its role in the foreign exchange-rigging scandal, led by Lord Grabiner.

My colleague Angela Monaghan is tweeting the key points from the Treasury committee:

Carney defiant, insisting Grabiner review got to the "heart of the matter" on Bank's role in the forex scandal (not guilty of impropriety)

— Angela Monaghan (@angelamonaghan) March 3, 2015

Carney defends the timing of the firing of its chief currency dealer Martin Mallett, a day before Grabiner report was published. 1/2

— Angela Monaghan (@angelamonaghan) March 3, 2015

Carney says a review of e-mails and phone calls revealed a "series of misjudgments" by Mallett that could not be ignored. 2/2

— Angela Monaghan (@angelamonaghan) March 3, 2015

Carney: Mallett's misjudgments incl sharing BoE docs externally, violation of IT policy, venturing personal opinions, inappropriate language

— Angela Monaghan (@angelamonaghan) March 3, 2015

Carney also distanced himself from Lord Grabiner’s own combative performance at the Treasury Committee in January.

It showed “Neither the tone nor demeanour I would have adopted,” said the governor (as calm and collected as ever).

Greece’s finance minister appeared to be in good spirits this morning, as he headed off to work:

#Varoufakis blows kiss to passer by on his way to work - VIDEO - #Greece - http://t.co/bT1Rg3qICi pic.twitter.com/WBeSACvE9n

— enikos_en (@enikos_en) March 3, 2015

Fitch will downgrade Greece without 'durable' deal

Greece’s credit rating will be cut unless it agrees a long-lasting agreement with its partners over its funding needs, rating agency Fitch warned this morning.

Reuters has the story:

Greece needs to secure a “durable” aid agreement with the rest of the euro zone to avoid a further downgrade of its already sub-investment grade sovereign rating, one of Fitch’s top analysts said on Tuesday.

“We believe that an agreement will ultimately be reached between Greece and its European partners as Grexit would be costly for both parties. Failure to reach a durable agreement would lead to a rating downgrade,” Fitch’s head of EMEA sovereigns, Ed Parker, said in a question and answer session In the Reuters Global Markets Forum chatroom.

Fitch currently rates Greece’s debt as ‘highly speculative’ with a B rating, just three notches up from default.

Updated

European factory gate prices have fallen for the fourth month in a row, Eurostat reports.

The amount that firms were paid for their goods fell by 0.9% month-on-month in January, and were 3.4% lower than a year ago.

CHART: Luxembourg was only euro-area member with positive PPI reading in January. Energy prices continued to decline. pic.twitter.com/51HD8iH4u8

— Maxime Sbaihi (@MxSba) March 3, 2015

That’s a signal that consumer prices in the eurozone may keep falling for some months, keeping deflation fears on the agenda.

Howard Archer of IHS Global Insight says it’s uncomfortable news for the European Central Bank:

Underlying price pressures across the Eurozone look set to be limited for some considerable time to come because of the constraining effects of large output gaps in many countries following prolonged weak economic activity and still high unemployment.

Greek reform bills "could be delayed"

Over in Athens, sources are telling our correspondent Helena Smith that “there is a good chance” the government will delay sending some draft laws aimed at alleviating Greece’s “humanitarian crisis” to parliament.

Helena writes:

The laws were due to be gradually presented this week. On Monday, the government unveiled the first of the reforms – providing food stamps, reconnection of disconnected electricity supplies and shelter – for 300,000 families mostly in the poorer suburbs of Athens.

Other bills, however, including the introduction of a new scheme for repayment of overdue taxes and security contributions and the re-opening of the public broadcaster, ERT – shut down by former prime minister Antonis Samaras in June 2013 – are not likely to be brought before the House until after next week’s euro group meeting in Brussels on Monday.

“There is a lot of number crunching that has to be done and that takes time,” said one government official. “There is a good chance the legislation will be postponed for a couple of weeks.”

The new government may well want to get the lay of the land at the upcoming euro group. There have been rumblings of disquiet from Euro zone officials over some of the bills.

Updated

The House of Commons Treasury Committee is starting to question Bank of England governor Mark Carney about the BoE’s investigation into misconduct in the foreign exchange market.

Anthony Habgood, chairman of the court of the Bank of England, should also be there.

There’s a live stream here (I’ll keep half an eye on it).

It could be quite interesting, as the Bank has been criticised for setting “very low tests” when it examined its own role in the scandal.

Bank of England foreign exchange investigation too narrow, says MP

However....some UK construction firms did warn that uncertainty in the build-up to May’s general election may hit demand.

First look at UK PMI suggests there is a lot to be positive about within UK construction. Election seen as potential blip to activity though

— World First (@World_First) March 3, 2015

UK construction sector posts strong growth

Just in: Britain’s construction sector racked up surprisingly strong growth last month.

Markit’s Construction PMI, which measures activity across the sector, rose to 60.1 last month. That shows the fastest growth since October last year.

Markit/CIPS UK Construction PMI Feb: 60.1 (est 59; prev 59.1)

— Live Squawk (@livesquawk) March 3, 2015

Housebuilding, commercial construction and civil engineering all reported stronger growth last month, and firms also reported a jump in confidence.

Another signal that Britain’s economy, like Germany and Spain, may be picking up....

Go the UK ! Markit: Sharpest expansion of construction activity for four months #GBP #GDP

— Shaun Richards (@notayesmansecon) March 3, 2015

The Athens stock market is outperforming the rest of Europe, up around 2% in early trading.

That follows finance minister Yanis Varoufakis’s pledge to take six firm reform policies to Brussels next Monday. Investors may also be calmed by his promise that Greece will do everything in its power to meet its March debt repayments.

Our Athens correspondent, Helena Smith, tweets:

#Greece deputy pm Giannis Dragasakis denies that technical teams from dreaded "troika" - oops "institutions" - in Athens tmr

— Helena Smith (@HelenaSmithGDN) March 3, 2015

The latest Spanish unemployment figures also suggest that Europe’s economy is reviving.

The number of Spaniards out of work fell by 13,538 last month, or 0.3%, as factories and building firms took on more staff.

That’s the biggest fall for any February since 2001, according to Spain’s Labour Ministry.

After some traumatic years, Spain’s economy is currently one of the fastest-growing members of the eurozone.

The issue, though, is whether voters will give the current government the credit, or push for the change offered by the Podemos party?.....

Key question: what conclusions will Spanish voters draw from contrast between Spain's recovery and Syriza-induced disaster in Greece?

— Simon Nixon (@Simon_Nixon) March 3, 2015

Updated

German retail sales hit seven-year high

German consumers hit the shops with remarkable vigour last month, in the latest signal that Europe’s largest economy is gaining strength.

German retail sales jumped by 2.9% month-on-month in January, the biggest jump since January 2008.

Although this measure is volatile, it suggests confidence is growing in Germany, as the economy picks up pace and unemployment keeps falling.

JPM calles the rise in German retail sales "legendary": pic.twitter.com/1pRLXnh9RA

— Richard Barley (@RichardBarley1) March 3, 2015

I forgot to link earlier, sorry, but here’s the Sentix survey:

“Grexit“ more probable despite new programme

Here’s another chart from this morning’s Sentix’s eurozone survey, showing that fears of Greece leaving the eurozone are at their highest level since autumn 2012.

As Greek rumblings continues ever more investors expect #Greece to leave Euro. #Grexit risk at 37%, highest since '12 pic.twitter.com/hlrDNMDaQT

— Holger Zschaepitz (@Schuldensuehner) March 3, 2015

2014 was a good year for Barclays CEO Antony Jenkins.

The bank reports this morning that Jenkins received a pay packet of £5.5m, including a £1.1m bonus, even though the bank set aside £1.25bn to cover the cost of the foreign-exchange rigging scandal.

Jenkins has already defended it, telling the BBC’s Today Programme that:

“On this occasion I judged it was right for me to take my bonus....Barclays today is a stronger business, with better prospects, than at any time since the financial crisis.

My colleague Jill Treanor’s story on Barclay’s results is here:

Foreign exchange rigging fines weigh on Barclays results

Europe’s banks will not be subjected to a full stress test this year.

The European Banking Authority, which ran a health-check of the sector last autumn, announced the move (or non-move) this morning:

EuropeanBankingAuthority EBA decided not to carry out an EU-wide stresstest in 2015(next 2016) http://t.co/x2vm0IbB09 pic.twitter.com/AJ924klQzx

— Salim DEHMEJ (@sdehmej) March 3, 2015

Writing in the Guardian today, Syriza MP Costas Lapavitsas argues that Greece’s best hope of ending its deflationary economic spiral is to leave the euro.

Lapavitsas warns that the next four months will be very tough for Athens as it tries to meet the demands of its lenders:

Tax income is collapsing, partly because the economy is frozen and partly because people are withholding payment in the expectation of relief from the extraordinary tax burden imposed over the last few years. The public purse will come under considerable strain already in March, when there are sizeable debt repayments to be made.

He also reckons that Syriza must admit that its pre-election promise of ending austerity within the eurozone isn’t achievable:

The most vital step is to realise that the strategy of hoping to achieve radical change within the institutional framework of the common currency has come to an end. The strategy has given us electoral success by promising to release the Greek people from austerity without having to endure a major falling-out with the eurozone.

Unfortunately, events have shown beyond doubt that this is impossible, and it is time that we acknowledged reality.

More here: To beat austerity, Greece must break free from the euro

Survey: 38% of investors expect eurozone break-up

More investors expect the eurozone to fracture over the next 12 months than at any time since the Cyprus bailout crisis of March 2013.

The Euro Break-up Index, calculated by German research group Sentix, jumped to a two-year high of 38% in February, from around 24% in January, with more investors predicting a Greek exit.

That shows that the battles over Greece’s bailout have raised new fears over the stability of the single currency, even though a four-month extension was agreed.

Sentix’s chief Sebastian Wanke says:

The development is driven by a clearly worsening assessment of investors concerning Greece....

Despite the solution which was found last week for Greece ever more investors expect the Mediterranean country to leave the euro soon.

Wanke added that investors will be pondering the dangers of Grexit over the next few months.

The survey took place between 26 and 28 February, so immediately after Greece’s creditors agreed to extend its bailout until the end of June.

Worth remembering that Greece’s government, other top Eurozone politicans, and the head of the IMF, have all insisted that the eurozone will not break up.

Updated

The agenda: Third Greek bailout on the cards?

Good morning, and welcome to our rolling coverage of the world economy, the financial market, the eurozone, and business.

Greece remains top of the agenda this morning, as the Athens government strives to hit its looming funding needs and push through reform plans – in the face of internal opposition.

As we covered in yesterday’s blog, Spain’s finance minister Luis de Guindos stirred the rumour pot, telling reporters in Pamplona that:

“We are negotiating a third rescue for Greece.”

That’s been officially denied by eurozone officials; a spokeswoman for eurogroup chief Jeroen Dijsselbloem insisting:

“Euro zone finance ministers are not discussing a third bailout.”

Curious. At *some point* the eurozone needs to start pondering what happens when Greece’s four-month extension ends. First, though, it needs to clear its immediate demands for cash.

Finance chief Yanis Varoufakis declared on TV last night he’s “certain” that Greece will repay its bills in March, especially the repayments owed to the IMF.

#Varoufakis on #enikos : Greek #repayments will be made in full - #Greece #IMF #bailout http://t.co/9p9ZRAfeoV pic.twitter.com/MdDqg5CGxL

— enikos_en (@enikos_en) March 3, 2015

And economy minister George Stathakis has told the Daily Telegraph that Greece can tap various cash “buffers” to keep afloat....

In the meantime, Greece needs to develop its reform plan ready for next week’s Eurogroup meeting (yes, another one)

in athens, we're looking at the end of creative vagueness as finmin varoufakis says he'll go to monday's eurogroup with 6 proposed reforms

— Diane Shugart (@dianalizia) March 3, 2015

Also coming up today....

MPs on the Treasury Committee will question Bank of England governor Mark Carney, over their investigation of the foreign exchange-manipulation scandal, from 10am GMT.

The monthly UK Construction PMI survey is released at 9.30am GMT.

UK bank Barclays is releasing its results this morning -- the top line is that it’s put aside another £750m to cover the cost if its role in that FX-rigging scandal. That takes the provision for the last six months to £1.25bn (!):

Barclays provides £1.25bn for forex rigging investigations, another £200m for PPI

— Jill Treanor (@jilltreanor) March 3, 2015

We’ll be tracking all the main events through the day as usual...

Updated