European Commission encouraged by Greek talks

The European Commission has said it believes a deal on a third Greek bailout in time for 20 August, when the country has to pay €3.2bn to the European Central Bank, is possible.

Reuters has received a statement from EC spokeswoman Mina Andreeva in response to earlier comments from Greek finance minister Euclid Tsakalotos that the talks could be concluded this week.

According to the news agency, she said:

The European Commission is encouraged by the progress made so far. We are moving in the right direction and intense work is continuing.

The constructive collaboration with the Greek authorities should allow the negotiations on a new three-year programme to progress rapidly.

[If all sides stuck to last month’s summit commitment] agreement is possible in order to allow for a first disbursement under the new ESM programme in time for the payment Greece is due to make on August 20.

It is an ambitious yet realistic timetable.

On that note of optimism, it’s time to close up for the evening. Thanks for all your comments, and we’ll be back tomorrow.

European markets end mixed in calmer tradign

A day after the Athens market recorded a 16.2% collapse, the first day it had opened for five weeks, it fell back again but only by 1.22% as some signs of normality returned.

Returned everywhere, that is, except to the Greek banking sector, which saw leading banks lose around 30% for the second day running on the prospect of the banks being recapitalised after savers withdrew their cash in waves this year before the introduction of capital controls.

But non-financial shares gained ground and Socrates Lazaridis, chief executive of Hellenic Exchanges was quoted by Reuters as saying:

The second day of trading showed clear signs we are moving towards a normalisation of the market after the long shutdown.

In the rest of Europe it was a more mixed picture, with Spain and Italy seeing the most dramatic moves. The final scores showed:

- The FTSE 100 fell 2.05 points or 0.03% to 6686.57

- Germany’s Dax edged up 0.11% to 11, 456.07

- France’s Cac closed 0.16% lower at 5112.14

- Italy’s FTSE MIB fell 1.02% to 23,473.25

- Spain’s Ibex ended down 1.02% at 11,150.5

On Wall Street the Dow Jones Industrial Average is currently down 10 points or 0.06%.

Lenders to meet again tomorrow with Finance Min Tsakalotos & Economy Min Stathakis to recap issues discussed over last few days #Greece

— Nick Malkoutzis (@NickMalkoutzis) August 4, 2015

#Greece & lenders yet to agree on GDP & primary balance forecasts but Tsakalotos thinks pace of progress good & bridge loan won't be needed

— Nick Malkoutzis (@NickMalkoutzis) August 4, 2015

Greek FinMin Tsakalotos says there are still some differences with lenders on new privatisation fund, reports @NikasSotiris #Greece

— Nick Malkoutzis (@NickMalkoutzis) August 4, 2015

Updated

#Greece FinMin Tsakalòtos says timetable for agreement, vote on #ESM loan and first disbursement looks realistic.

— Yannis Koutsomitis (@YanniKouts) August 4, 2015

More from Greek finance minister Euclid Tsakalotos, who said he expected talks with the country’s lenders about a third bailout would be completed in the next few days.

After meeting representatives of the IMF, European Commission, ECB and the ESM rescue fund, he said, “Everything will be concluded this week,” reported Reuters.

The Athens stock market has closed down 1.22%, the day after its 16.2% record fall as it reopened after a five week halt in trading.

Most losses were in the banking sector as worries continued about the need to recapitalise Greece’s financial institutions.

After 30% declines on Monday - the largest falls allowed before limits are imposed - Greece’s banks saw similar declines today. Piraeus Bank once again hit the 30% limit, while Eurobank Ergasias, Alpha Bank, National Bank of Greece and Attica Bank all lost between 26% and 29.7%.

#Greece bank shares lost half of their value in just two sessions and 2/3 in the post-election period. #economy #banking #markets #stocks

— Manos Giakoumis (@ManosGiakoumis) August 4, 2015

Creditor talks going well - Greek finance minister

The talks on privatisation between Greece and its lenders are going better than expected, according to finance minister Euclid Tsakalotos.

There were no significant disagreements, he told reporters during a break in the talks. He said (quotes courtesy Reuters):

We have submitted a proposal to them. They said they would examine it and come back to us.

There were small divergences in views. I don’t think there will be a problem. Discussions have gone better than I expected.

Updated

The European Council has approved changes to the EFSM financial assistance fund which could help Greece if it decides to ask for another bridging loan as talks on a third bailout continue. That might be needed if no agreement is reached by 20 August when a €3.2bn payment is due to the European Central Bank.

The council ratified an agreement made when the EFSM provided a €7.16bn loan last month, and is designed to protect non-eurozone members in case of any default. It said:

The regulation ensures that financial assistance from the EFSM to a euro area member state will only be granted if legally binding provisions are in place guaranteeing that non-euro area member states are immediately and fully compensated for any liability they may incur as a result of a failure by the beneficiary to repay the financial assistance in accordance with its terms.

Now that changes to #EFSM are agreed, Greece can apply for 2nd bridge loan to pay ECB on 20/8 http://t.co/C87HatuOCN https://t.co/lM9qyt1RDl

— Pieter Cleppe (@pietercleppe) August 4, 2015

Afternoon summary

- Greece expects to conclude a bailout deal within two weeks, before it needs to make a €3.2bn repayment to the European Central Bank

- Greek banking shares have lost almost 30% for the second day in a row. The Athens stock exchange has slid 2%.

- Oil and commodity prices have stabilised after their recent sharp falls. Brent crude is up 1.1% at $50 a barrel

- Chinese stock markets have bounced back after new rules on short-selling came into force

- The UK government has kicked off the sale of RBS, and George Osborne has defended the £1bn loss to the taxpayer.

- London-listed drugmaker Shire has made an unsolicited $30bn bid for US group Baxtala, a recent spin-off from Baxter that specialises in haemophilia

- Wall Street has opened slightly lower. The Dow Jones is down 0.04% at 17589.65 while the Nasdaq has slipped 0.06% to 5112.221. In Europe, Germany’s Dax is down 0.05% at 11438.28, while France’s CAC has shed 0.35% to 5102.35 and the FTSE 100 index in London is trading 0.1% higher at 6696.14.

Returning to Greece, Athens and its lenders agreed on Monday that any pension reforms would not affect individuals who retired before the end of June 2015. On Tuesday, talks shifted onto the recapitalisation of banks and privatisation matters. Talks are taking place between Greece’s finance and economy ministers and their counterparts at the troika/quartet.

News of Shire’s approach comes hot on the heels of its acquisition of a small New York-based biotech called Foresight Biotherapeutics, which is working on an eye drop for infectious conjunctivitis, known as pink eye. And in January, Shire bought NPS Pharma, a US firm whose main product aims to alleviate bowel disease.

Shire may want Baxalta, but attempting a cross border, all stock, hostile offer for a company with strong defenses is not a great start.

— DAVID FABER (@davidfaber) August 4, 2015

Shire CEO Flemming Ornskov did an interview last month w/ @TimmermanReport discussing acquisitive interest. http://t.co/HsbK0wQVlN $SHPG

— Luke Timmerman (@ldtimmerman) August 4, 2015

Updated

Shire swoops on Baxalta with hostile $30bn bid

In the corporate world, London-listed drugmaker Shire has swooped on US group Baxalta with a hostile, all-share bid worth $30bn. Baxalta has just been spun off by Baxter and makes treatments for haemophilia. Last summer Shire agreed a $54bn takeover by US drugs group AbbVie, only to see it fall through after the Obama administration clamped down on overseas acquisitions driven by tax avoidance.

Together, Shire and Baxalta, which is listed on the New York Stock Exchange, would have sales of $20bn in 2020. Shire, best known for its hyperactivity drugs but which now specialises in rare diseases, went public with its proposal after Baxalta rebuffed the approach. Shares in Shire fell nearly 5% on the news, making them the biggest loser on the FTSE 100 index.

Shire’s chief executive, Flemming Ornskov, wrote to his counterpart, Ludwig Hantson at Baxalta:

Other than a brief meeting on 10 July at which we outlined our proposal and its benefits, your lack of engagement has been surprising. You have left us with no choice but to make our proposal known to your shareholders. We believe they deserve an opportunity to consider it.”

Updated

Professor Charles Goodhart, the respected London School of Economics economist who used to sit on the Bank of England’s monetary policy committee, has warned that delaying a rate hike because of economic uncertainty would be a great policy error.

The downside risks associated with the Chinese stock market slide and the possibility of Greek default are the sort of things policymakers have to look through, Goodhart told Market News International after a Fathom Monetary Policy Forum event. He argued that uncertainty is always present and can always be cited as a reason for delay.

One of the great errors of policymaking is the view that ‘There are a lot of things we don’t know and many of these will become apparent over the next three months, so why not wait three months until you are more certain?

The reason why that is an error is because there are lots more things that become uncertain over the next three months, and so the degree of uncertainty is pretty well constant at all times. But noone sees it in that way.

Goodhart recalled that when he was on the MPC, from 1997 until 2000, virtually all the BOE quarterly forecasts began by describing the economic situation as uniquely uncertain. He said policymakers had to guard against the fallacious belief that if they just wait a little longer they will be to avoid mistakes because the right course of action will become clearer. He told MNI:

It won’t become more obvious. You are just as likely to make mistakes if you wait.”

Updated

Britain’s tax intake has been below Greece’s, according to OECD figures for 2012. Greece’s tax revenues were 33.5% of GDP, while the UK’s tax revenues made up 32.9% of GDP.

Britain's tax intake is below Greece's. https://t.co/VlTQ3Q20fr

— Aditya Chakrabortty (@chakrabortty) August 4, 2015

Are our taxes too high? Latest available figures from OECD. pic.twitter.com/HFmkmpcTJB

— Jo Maugham QC (@JolyonMaugham) August 4, 2015

-30% yesterday, -27% today. Not the best couple of days trading for Greek banks: pic.twitter.com/X4PLD5pvPU

— Jamie McGeever (@ReutersJamie) August 4, 2015

Greece’s banking crisis has led to more people turning to plastic, Bloomberg reports. Until last month, the vast majority of Greek pensioners didn’t even have a cash card, which led to the scenes in July of elderly Greeks lining up in despair outside banks, the newswire writes.

In a country where cash is king and undeclared transactions still make up about a quarter of the economy, about 1 million debit cards have been issued by banks since the government closed lenders for three weeks and imposed controls on euro bills. Emergency measures that some officials warned might spur the black market are showing signs of doing the opposite.

Alpha Bank issued about 220,000 cards in July, more than all of last year, as mainly pensioners realized that they had to access their money at cash machines and elsewhere, said Leonidas Kasoumis, general manager for household lending. Supermarket and gasoline sales paid by debit cards doubled in the wake of controls; usage in the countryside tripled, he said.

“Capital controls were a big trigger,” Kasoumis said. “It’s good for merchants, because cash is limited; it’s good for banks because it reduces operational costs. But the best news is for the economy.”

The restrictions on cash were introduced in late June as banks hemorrhaged money and were kept alive by a drip-feed from the European Central Bank. Greeks can withdraw €420 ($460) a week, though there’s no limit on spending with debit cards provided the transaction is within the country.

You can read the full story here. Greece has the lowest number of electronic payments per head in the EU, according to ECB figures.

Updated

Property prices in Greece are falling at a faster pace: the latest figures from the Bank of Greece show apartment prices dropped 5.6% year-on-year in the second quarter, following a 4.1% fall in the first quarter. Residential property prices have plunged more than 40% since 2008 when Greece slid into a deep recession.

Connor Campbell at Spreadex says about the Greek government’s hopes of achieving a bailout deal by 18 August:

The likelihood of this being achieved should become clearer in the next few days, as the drafting of an agreement gets underway. The technical talks, which have yielded surprisingly little news beyond last week’s IMF debt relief claim, conclude today, and hopefully will give way to a livening up of this already interminable August (and yes, I’m away we are only four days in).”

Europe's main stock markets slip, Athens down 1.3%

Europe’s main stock markets are slipping again, with weak oil prices still weighing on energy shares. A warning from German carmaker BMW about slowing sales in China helped drag the Dax in Frankfurt lower.

The Athens stock exchange, which lost a record 16% on Monday, its first day of trading in five weeks, has slid a further 1.3%. Its banking index, which comprises the four main lenders, is now down 27.1%, just above the 30% daily loss limit at which trading is halted. National Bank of Greece, Greece’s biggest bank, and Attica Bank are both trading 22% lower. Without the banking stocks, the Athens index would be up on the day.

UK’s FTSE 100 down 0.16% at 6678.02

Germany’s Dax down 0.17% at 11424.78

France’s CAC down 0.5% at 5092.72

Updated

#Greece said to target bank recapitalization by mid-december. Greek depositors will not be bailed-in, BBG reports citing CenBank Official.

— Holger Zschaepitz (@Schuldensuehner) August 4, 2015

This is Piraeus Bank -51% in two days... We need a name for this chart. pic.twitter.com/x05r9omPEN

— Jonathan Ferro (@FerroTV) August 4, 2015

It has taken Labour a while to respond to the RBS share sale. Chris Leslie MP, Labour’s shadow chancellor, says:

George Osborne’s rush to begin the sell-off of RBS has meant a loss to the taxpayer of as much as £1bn.

Taxpayers who bailed out RBS and who have now lost out will want to know why the Government has sold these shares at a discount and while the bank is still awaiting a US settlement for the mis-selling of subprime mortgages.

Getting back the taxpayers’ money is not an impossible objective and the Chancellor is dismissing this too lightly.”

Greece expects bailout deal by 18 August

Athens expects to conclude a bailout deal with international creditors by 18 August, with the drafting of the agreement starting on Wednesday, a government spokeswoman said. Greece faces a key deadline on 20 August when it needs to repay a €3.2bn bond held by the ECB.

Olga Gerovasili told Greece’s Skai TV station:

The first phase of negotiations ends today and the second phase starts, which really contains the details of drafting [the deal].

If the terms of the [EU] summit are met, I think that we will have a deal by the 18th of this month.”

Updated

Calm returns to world markets

A degree of calm has returned to financial markets around the world (with the notable exception of the Athens exchange). The price of Brent crude oil is hovering around $50 a barrel, up nearly 1%. Copper has also firmed, rising to $5,240 a tonne after hitting a six-year low of $5,142 on Monday, and Chinese stocks bounced more than 3% after new rules on short-selling came into force.

Investors who borrow shares must now wait one day to pay back loans, according to statements from the Shanghai and Shenzhen stock exchanges issued after the close of trading on Monday. The restrictions are the government’s latest measures to stem the rout, which has led to almost $4 trillion being wiped off China’s stock markets.

Wu Kan, a Shanghai-based fund manager at JK Life Insurance, told Bloomberg News:

All the government’s measures including restrictions on short selling are working now. It’s a rebound and given the momentum, it may last for some days.”

Updated

Spanish unemployment falls due to temporary jobs

Spanish unemployment data just out shows that the number of Spaniards out of work has fallen for the sixth month in a row in July. However, nearly all the hiring is in temporary seasonal jobs.

Of the 1.8m contracts created in July, more than 93% were temporary. Labour Ministry data showed the overall number of jobless fell by 74,028, or 1.8%, month-on-month to 4.05m people.

Nationwide: UK house prices rise 0.4% in July

The latest figures from Nationwide building society show house prices across the UK edged up by 0.4% last month, hitting a new high of £195,621. Nationwide estimates that homebuyers paid a collective £275m less in tax in the first six months of the year as a result of changes to stamp duty in December, as my colleague Hilary Osborne reports.

After a fall in June which took the annual rate of price inflation to a two-year low, July’s price rise pushed it back to 3.5% – a level that Nationwide’s chief economist said was close to the historic pace of earnings growth.

Robert Gardner said:

After moderating over the past 12 months, there are tentative signs that annual house price growth may be stabilising close to the pace of earnings growth, which has historically been around 4%.

This would bode well for a sustainable increase in housing market activity, though whether this will be maintained will depend on whether building activity can keep pace with increasing demand.”

Updated

The FTSE 100 and the German stock market are now in positive territory. The FTSE is up nearly 20 points, or 0.27%, at 6707.69, while the German Dax has edged 5 points higher to 11448.87. France’s CAC is still trading down 0.4% at 5101.99.

Producer prices in the eurozone slipped 0.1% in June, according to the EU’s statistics office Eurostat.

“Can anyone, apart from some politicians, who thinks that the taxpayer will ever get all its money back for the bailing out of Royal Bank of Scotland, please raise their hand now?” asks Michael Hewson at CMC Markets UK.

No, I didn’t think so, but this still doesn’t adequately explain the timing behind last night’s announcement that the UK government is paring down its 78% stake in the bailed out lender by 5%, at a time when markets are fairly quiet, and volumes low.

Putting to one side the fact that the UK government at the time paid over the odds for the bank, the beginning of the sale process was always going to be politically toxic.

Unsurprisingly the main criticism has been that the sale is being done at a significant discount to the purchase price, but realistically that was always going to be the case, given that on an adjusted basis the peak in the share price in 2007 sits at 6,071p.

The peak this year currently sits at 414p, which equates in old money to 41.4p before the 10 for 1 stock consolidation we saw in June 2012. The share price is currently sitting just above one year lows and the lows this year at 326p, but since the beginning of 2013 the share price has gone pretty much nowhere, which is a pretty poor return by anyone’s standards,

The recent return to profitability may have helped push forward the decision making process after the bank announced a 27% rise in net profits for Q2 last week, but the fact remains that there is billions of taxpayers’ money tied up in a bank not generating a return, that could be put to better use.

The banking sector does appear to be showing signs of turning itself around and freed from the dead hand of political control the bank is more likely to show signs of recovery if it is freed from this particular anchor.

The bank continues to sell off assets as it continues to cut down its stake in US operation Citizens with another $2bn sale announced last week. Litigation costs are likely to continue to be a drag on profitability for some time to come, with US regulators looking into mortgage mis-selling, but the bank continues to restructure its operations with a more domestic focus and it is likely to be more successful in doing that without the UK government peering over its shoulder.

The start of the disposal process may well have fired the starting gun on the re privatisation process, but the process still has a long way to go before being complete.

Maybe subsequent stakes may well yield a higher return for taxpayers, but waiting and hoping for a distressed asset to come back into break even territory is no way to generate the best return.

Better to free up the capital in the coming weeks and months and put it to better use.”

The pound has dipped, falling to $1.5583 after the weaker construction PMI. It also lost ground against the euro, to 70.38p.

Traders and analysts are eagerly awaiting Thursday, when the Bank of England releases its quarterly inflation report, its interest rate decision and the minutes of its policy meeting which are expected to reveal the first split in the nine-member committee. Markets expect three members to vote for a rate rise.

Updated

Stefan Friedhoff, global corporates managing director for construction at Lloyds Bank Commercial Banking, said:

This data comes as something of a surprise in a sector in which optimism currently outweighs pessimism. A few months on from the general election, the trading environment is now more settled.

Meanwhile, firms have generally adapted well to the new normal. Unrealistic pricing in bidding rounds is largely a thing of the past and the reality of the current situation is being factored into contracts so there is a lower probability of mistakes being replicated.

Order books and pipelines look healthy and there is every chance the sun will continue to shine on the sector even after the summer is over.”

Housebuilding activity grew at the slowest pace since April, underlining the challenges faces by the government in tackling Britain’s chronic housing shortage.

Markit senior economist Tim Moore said:

Commercial activity was a key growth driver during July, which partly offset ongoing weakness in civil engineering and softer residential building trends. Survey respondents commented on a variety of growth constraints afflicting the residential building sector, including long lead-in times for new projects, scarce supplier capacity, skill shortages and stretched sub-contractor availability.”

Construction firms took on fewer new workers last month, but Markit said hiring is still higher than the historical average.

UK construction growth slows unexpectedly

Growth in the UK’s construction industry slowed unexpectedly in July due to weaker housebuilding and civil engineering.

The Markit/CIPS Uk construction purchasing managers’ index fell to 57.1 after hitting a four-month high of 58.1 in June. This wrongfooted economists who had expected activity to improve to 58.4.

Some non-financial stocks are rising in Athens, such as gaming group OPAP, up 3.5% and energy infrastructure group Metka, up 8.4%.

The Athens bourse is now down 3.4%, dragged down by heavy losses in banking shares.

Eurobank equities analyst Nick Koskoletos says:

Following yesterday’s massive sell-off, there was significant dislocation in share valuations which triggered investors’ interest in high-quality, non-financial stocks.

The recent fall in commodity prices is likely to be short-lived, believe economists at Capital Economics. “We do not expect the renewed falls in commodity prices on Monday to be the beginning of another major leg down in natural resources markets,” they write.

We would caution against getting too carried away by these recent developments. For a start, the Chinese PMIs were probably dragged down by temporary factors. China’s major manufacturing hubs were affected by bad weather last month, while the collapse in the stock markets on the mainland probably damaged business sentiment. Note too that the official PMI was not as weak, suggesting that Markit’s measure may have overdone the decline.

What’s more, there are already signs that the policy support implemented in recent months has begun to boost economic activity. And the authorities still have plenty more ammunition at their disposal to prevent conditions from worsening any further.

The upshot is that most of the bad news from China is probably already priced into the market, suggesting that commodities are unlikely to fall much lower. We suspect that some recovery in demand will actually lift prices in the months ahead.

The Footsie is now down 0.5% at 6655.09. Connor Campbell, financials analyst at Spreadex, says:

Tuesday brings with it the quietest day in a week otherwise full of data, leaving the FTSE extra susceptible to any downturn in the commodity sector.

So far Brent Crude and copper are tentatively in the green as they take back some of Monday’s losses; this still leaves the former teetering just above $50 per barrel whilst the latter is only marginally higher than yesterday’s lows.

Lagging behind the commodity stocks themselves are the FTSE’s weighty oil and mining firms, with BP and Shell especially looking shaky. The continuation of this commodity drag has meant the UK index underwent another lifeless open, as it continues its struggle to substantially break 6700.

An expected improvement in the construction PMI is unlikely to help the FTSE out as investors focus on the commodity issues, but a strong figure could give a boost to the pound.

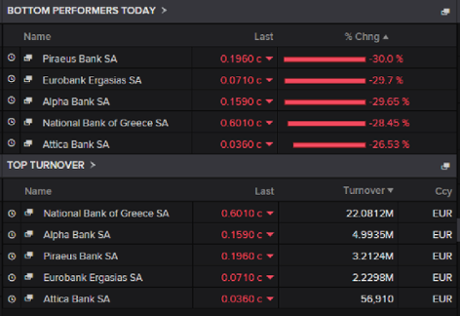

Greek banking stocks plunge again

In Athens, the main banking stocks are getting battered again: they’ve lost more than 29% in early trading, close to the 30% daily limit for losses. The Greek banks index has lost 29.46%. The stock market as a whole opened 4.5% lower and is now trading 0.2% higher.

Attica Bank -24.49%

National Bank of Greece -29.05%

Alpha Bank 29.65%

Eurobank -29.7%

Piraeus Bank -30%

Updated

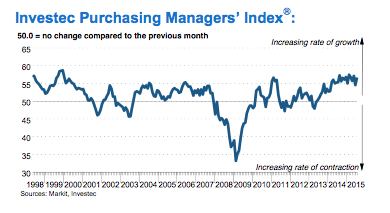

In sharp contrast to Greece, Ireland’s manufacturing sector powered ahead last month. The Investec PMI showed growth of output, new orders and employment all picked up, but factory gate prices fell for the second month running.

Brent crude briefly crept above $50 a barrel before dipping below again.

In London, Smiths Group is the biggest riser on the FTSE 100 index after reports that the activist hedge fund ValueAct has become a shareholder in the company, which makes a range of products including airport scanners and medical devices. The news comes just days after the San Francisco-based hedge fund revealed it had become the largest investor in the aerospace group Rolls-Royce, one of Britain’s biggest manufacturers.

The Financial Times reported (£) that ValueAct has been building a stake in Smiths since the company appointed a new chief executive and sparked hopes for a strategic review of the sprawling business. Smiths shares are up more than 7% at £12.32.

Updated

Chinese shares rise, oil up... but European stock markets open lower

Asian shares recovered somewhat on Tuesday, with Japan’s Nikkei recouping earlier losses and ending the day 0.1% lower. The Shanghai Composite Index rose 3.7% while the CSI 300 index added 3.1%.

Oil prices have also firmed, with Brent crude trading 0.85% higher at $49.94 a barrel while New York crude is 1% ahead at $45.68.

In Europe, stock markets have opened lower, however:

Germany’s Dax down nearly 40 points, or 0.35% at 11404.01

France’s CAC down 24 points, or 0.47%, at 5096.28

UK’s FTSE 100 down 34 points, or 0.5%, at 6654.21

French bank Crédit Agricole and German carmaker BMW are among the worst performers following second-quarter results while energy stocks are being dragged lower by weak oil prices. BMW warned about the impact of China’s economic slowdown on its business.

Updated

Here’s our full story on RBS... and a handy timeline: Royal Bank of Scotland: from bailout to sell-off. And you can find out more about the background here: RBS sale: Fred Goodwin, the £45bn bailout and years of losses.

Of course RBS is being sold at a "loss"! It's much, much smaller than the bank that was bought for £45.2bn

— Iain Martin (@iainmartin1) August 3, 2015

Flawed logic in @RBS sale document. Avg daily trading volume should be compared to free float not market cap. pic.twitter.com/yzrl8ZWb13

— Louise Cooper (@Louiseaileen70) August 4, 2015

Updated

Chris Leslie, Labour’s shadow chancellor, responded to the “fire sale” of RBS shares, on Monday:

RBS had to be bailed out urgently, but it doesn’t have to be sold off at the same speed.

Labour has always supported the eventual return of RBS to the private sector but taxpayers who bailed out the bank will want their money back and will be suspicious of any fire sale. The Chancellor needs to justify his haste in selling off a chunk of RBS while the bank is still awaiting a US settlement for the mis-selling of sub-prime mortgages.

Two years ago George Osborne said he would only countenance a sale of RBS when ‘the bank is fully able to support our economy and when we get good value’. Neither of these tests has yet been passed.”

After RBS share sale plans leaked share price fell from £3.42 to £3.37 and then further 2% discount offered to institutional buyers

— Paul Lewis (@paullewismoney) August 4, 2015

£2.1bn from selling RBS shares at £3.30 which were bought for £5 is around £1bn loss. That's 5.4% of holding. All at that price £20bn loss

— Paul Lewis (@paullewismoney) August 4, 2015

Total disgrace that the government has sold shares in RBS. They were clearly going back to 700p, err, eventually. pic.twitter.com/xiYfUzXnUC

— Mike Bird (@Birdyword) August 4, 2015

RBS bailed out by last gov. This gov is selling it back. Bank of England Governor says selling now is in “interests of the wider economy"

— George Osborne (@George_Osborne) August 4, 2015

Updated

UK government starts RBS sell-off at £1bn loss to taxpayer

George Osborne has kicked off the first sale of shares in the Royal Bank of Scotland since it was rescued in 2008, at a loss of £1bn to the taxpayer, our City editor Jill Treanor reports. The government has sold £2.1bn of RBS shares (a 5.4% stake) at 330p a share, a 2% discount.

The chancellor faced criticism from Labour politicians and trade union officials that he should have waited for the bank to achieve more deep-rooted reform before embarking on a major privatisation.

But George Osborne said it was the right thing to do for the British taxpayer.

The chancellor sanctioned the first sale of the stake in RBS, which was announced on Monday night, in a move which cuts the taxpayer shareholding from 79% to just below 73%. Slightly more shares than expected were sold to major City investors after the stock market closed on Monday, crystallising a loss for the taxpayer after £45bn was ploughed into the bank to rescue it amid the financial crisis in 2008-2009.

RBS chief executive Ross McEwan said:

I’m pleased the government has started to sell down its stake. It’s an important moment and reflects the progress we are making to become a stronger, simpler and fairer bank. There is more work to be done but we’re determined to build a bank the country can be proud of.”

Hilarious that labour criticise government for failing to sale RBS profit.. Yet it was labour that bought into it at too high a price.

— Louise Cooper (@Louiseaileen70) August 4, 2015

Updated

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

European stock markets held up surprisingly well on Monday despite weaker Chinese data which put more pressure on commodities and the sharp sell-off on the Greek stock market when it reopened after a five-week shutdown .

The Athens exchange plunged 23% before closing 16% lower, its worst performance since records began in 1985. Banking shares got hammered and closed down 30%. Sentiment was also hit by a slump in the Greek manufacturing PMI survey to a record low.

Greek banks could come under further pressure, as Michael Hewson, chief market analyst at CMC Markets UK, explains:

The severity of the decline suggests that any bailout is likely to come in well above the €86bn numbers being bandied about, which in turn is likely to make any discussions about debt relief even more contentious. Any increase in tensions as we get closer to the €3.2bn ECB repayment date on 20 August is likely to see Greek banks come under further pressure in the coming days.

Weak Chinese manufacturing numbers triggered a sell-off in Asian stock markets and sent commodities lower on Monday. Brent crude dropped below $50 a barrel for the first time since January. Commodity prices have been suffering because China is the world’s biggest consumer.

European stock markets are set to open lower.

FTSE100 is expected to open 23 points lower at 6,665

DAX is expected to open 38 points lower at 11,405

CAC40 is expected to open 18 points lower at 5,102

Hewson adds:

The pound will be in focus once again today with the release of the latest construction PMI data for July, in the wake of yesterday’s rebound in the manufacturing PMI from a two year low.

Expectations are for the construction sector to improve from 58.1 to 58.6, in the process shifting the focus to this week’s latest Thursday trifecta of Bank of England rate meeting, minutes and inflation report.

Updated