Summary

Time for a mid-afternoon summary:

- Oil prices have continued to slide on Monday. Benchmark Brent crude is hovering above $54 a barrel and expected to fall further.

- The FTSE100 has extended its losses, down 1.35% to 6,457 points.

- Germany’s DAX is down 1.43%, after data showed weaker-than-expected inflation in December, raising expectations that the European Central Bank will be forced to act to curb deflationary pressures in the eurozone.

- A spokesman for Angela Merkel has rebutted reports that Germany expects Greece to leave the eurozone. But a report that German officials are relaxed about a Grexit has opened up new rifts in Germany’s political class.

That’s all from today’s business blog. Thank you for following and commenting.

Updated

Around 400,000 jobs will be created in 2015, pushing the unemployment rate down to its pre-recessionary levels, according to the labour market economist John Philpott.

The economist has forecast that unemployment will fall to 1.7m, dropping back to the rate of 5.2%, not seen since before the recession.

Average weekly earnings will grow by 2.5%, outstripping inflation for the whole of 2015.

While this will be “the best [year] overall for the UK labour market since 2007”, not all workers will notice a marked improvement in their lot.

Philpott writes that the labour market divide will widen in 2015.

Workers with particular technical skills or personal talents in high demand will begin to fare noticeably better in relative terms as will those working for organisations voluntarily prepared and able to offer low skilled workers the Living Wage. But in a labour market still oversupplied with people desperate for whatever work is on offer, employers unable or unwilling to improve working conditions will continue to have no difficulty in hiring staff into minimum wage jobs or on zero-hours contracts without any fringe benefits. This will serve to further widen what has become a clear structural ‘workforce divide’ within the UK’s ultra-flexible and lightly regulated labour market.

A Greek exit from the eurozone poses dangers to the rest of the currency union, writes Capital Economics.

The economics consultancy, which won a £250,000 prize on the least disruptive way to break up the euro, chides investors for their sanguine view on recent developments in Greece.

It would be complacent to conclude that Greece’s travails present no dangers to the currency union. For a start, the last eurozone crisis also began as an isolated development in Greece, before spreading to other countries. In that sense, the lack of contagion so far provides limited comfort.

Secondly, the fact that the latest Greek crisis has occurred despite a significant improvement in the country’s economic performance and sharp drop in its budget deficit is arguably a warning to other supposedly healthier countries that they are not immune from renewed market fears. Other countries with very high debt ratios, such as Italy and Portugal, appear most vulnerable.

And finally, it is far from clear that the policy advances made in recent years are adequate either to ensure a smooth Grexit or to deal with renewed difficulties in other countries. Not only is the ECB’s bond-buying power unproven, but it is unlikely that the bailout funds are big enough to resolve serious problems in a country like Italy. In short, while much hangs on the January 25th election, there is a clear risk that growing uncertainty over Greece’s future in the euro-zone will come to have broader negative economic and market effects in 2015.

Grexit talk creates rift in German SPD

The latest Grexit rumours have created division within the Social Democratic party, the junior partner in Germany’s grand coalition.

Kate Connolly, the Guardian’s Berlin correspondent, reports:

A heated row has broken out within the German government over how to deal with Greece in the event it votes a left-wing party into power.Following an election pledge by Alexis Tsipras, the head of the Syriza party, to cancel austerity measures and write off much of Greek debt in the event he wins, Germany’s economics minister Sigmar Gabriel has warned Athens that Berlin can “no longer be blackmailed”.His admonition came after it was reported that Chancellor Angela Merkel and her finance minister Wolfgang Schäuble believe the Eurozone could weather a Greek exit and that such a scenario would be almost unavoidable were Syriza to win.

But Gabriel’s message to the Greek electorate has sparked misgivings within his Social Democratic Party (SPD), some of whose members have accused him and Merkel of adopting a highly risky approach. The German government has been accused of trying to influence the outcome of the Greek election with its warnings. But some experts have advised that the tactic could backfire if Greek voters decided to call the German government’s bluff.

A Grexit, experts warn, would be hugely expensive to Germany in particular, and could further destabilise an already shaky Euro. Gabriel told the Hannoverschen Allgemeinen Zeitung that the German government’s goal was to see Greece stay in the Eurozone, but that it also expected Athens to fulfill its promises to the EU.

Regardless of who forms the next government, we expect that they stick by the agreements made with the EU. The Eurozone is considerably more stable and robust than it was several years ago, which is why we can no longer be blackmailed.

But the vice chair of the SPD’s parliamentary group, Carsten Schneider, said Gabriel’s position was “unsupportable”.

Johannes Kahrs of the conservative wing of the SPD, tweeted:

Merkel and Schauble are on their own regarding their U-Turn over Greece and Europe. That way will only be even more expensive for the tax payer.

Simone Peter of the opposition Greens called the debate over a Grexit “highly irresponsible”.

Updated

German inflation brings "irresisible" pressure for QE - Capital Economics

The fall in German inflation has raised expectations that the European Central Bank will start buying government bonds to support prices in the eurozone.

Jennifer McKeown, senior economist at Capital Economics, said there is a good chance of further falls in inflation in the coming months.

With weaker economies elsewhere in the euro-zone set to register even lower outturns, the euro-zone figure released this Wednesday is set to be negative for the first time since October 2009. Such a development would surely make the pressure for the ECB to implement quantitative easing at its January meeting irresistible.

On Wednesday, we will get EU-wide data on prices.

#ECB about to dial up QE? German headline inflation decreased to 0.1% in December, from 0.5% in November.

— David Jolly (@davjolly) January 5, 2015

#German CPI falls to 0.2% y/y, further impeding needed adjustments in #EZ relative prices. Unless you think deflation is great, of course.

— Simon Tilford (@SimonTilford) January 5, 2015

Updated

German inflation in a chart

German inflation getting close to the good old days of 2009. pic.twitter.com/tn5BbKAq6z

— Joseph Weisenthal (@TheStalwart) January 5, 2015

Energy and food have dragged down prices in Europe’s largest economy.

Consumer prices rose 0.1% in Germany in December, compared to the previous year.

Prices for goods fell by 1.2%, including:

- Energy -6.6%

- Food -1.2%

Prices for services rose 1.4%

Source: Reuters

German inflation falls to 5-yr low

German inflation fell to 0.1% in December, its lowest level in five years, according to figures just released by the Federal Statistics Office.

The figure was below economists expectations of a 0.2% increase in prices.

Hollande: only Greece can decide its euro future

French President François Hollande said on Monday that “Greece alone” can decide on whether to stay in the euro, writes Anne Penketh, a Guardian correspondent in Paris.

Hollande was asked about a German report over the weekend that Chancellor Angela Merkel would let Greece leave the single currency, during an interview on France-Inter radio. But he said that the Greeks were “free to decide their government” in the forthcoming elections, and that “as for Greece remaining in the eurozone it’s up to Greece alone to decide.”

He noted that both Greece and Spain had “paid a heavy price” to keep the European currency, and that there had been a “radical” reaction from fringe parties. But he played down the danger of electing the radical Syriza party in Greece and Podemos in Spain, saying that they could not be compared to the risks from the extreme-right. And if the radicals were elected in either country, he added, they would have to stick to the commitments of previous governments, in particular regarding the management of debt.

He added that “the rules governing the euro,” should be respected.

Hollande used the turmoil in Greece to reaffirm that the EU now needed to ditch its unpopular German-led austerity policies. “Europe can’t be identified with austerity, now that the euro has been stabilised,” he said.

Asked about the divergence between Germany and France on austerity measures, he announced that he would meet Merkel and the President of the European parliament, Martin Schulz, next Sunday to discuss “the future of Europe and Franco-German relations”.

The eurozone is unlikely to stage a full recovery until the Greek problem is solved, according to a former senior policymaker at the European Central Bank.

Lorenzo Bini Smaghi, an ex-member of the executive board of the ECB, warns that solving the Greek debt problem will be exceptionally difficult.

In an article on the FT’s exchange blog, he writes that Greece’s creditors will be reluctant to reduce its debt burden.

But politics also pose irreconcilable problems.

The problem is that the Greek people have made it clear that they do not want to exit the euro, as they consider it their only anchor against domestic political inefficiency and instability. The populist parties have understood this, and now claim they will be able to circle the square while staying in the monetary union. The claim is unrealistic, but the people of Greece might be too exasperated to grasp that. It is generally too late when people realise that they cannot have back the cake they just ate.

More here (metred paywall)

A European Commission spokesperson in Brussels has said “the euro has proved its resilience”.

Twitter is a bit sceptical.

*EU SAYS THE EURO HAS PROVED ITS RESILIENCE - here's how pic.twitter.com/uiOO4uuNDR

— Bruno Waterfield (@BrunoBrussels) January 5, 2015

The Grexit index is on the rise again. Joseph Weisenthal of Bloomberg has put together this nifty chart.

Mentions of "grexit" in news stories pic.twitter.com/6JKP9Rjx1M

— Joseph Weisenthal (@TheStalwart) January 5, 2015

The rest of Europe is doing its utmost to let Greece know that a vote for SYRIZA is basically a vote out the door.

— Joseph Weisenthal (@TheStalwart) January 5, 2015

Warnings of an apocalyptic future and a row over government debt. It can only mean one thing: an election campaign has started. Not that one. The Greek election on 25 January.

Greece’s two largest parties have been trading accusations, as campaigning got underway at the weekend.

Prime Minister Antonis Samaras said Greece would be forced out of the eurozone if left-wing anti-austerity party Syriza won the election.

Speaking at his party congress on Saturday, Alexis Tsipras, leader of Syriza, vowed to end “unreasonable and catastrophic”austerity.

He said a Syriza-led government would write down most of the nominal value of Greece’s debt.

That’s what was done for Germany in 1953, it should be done for Greece in 2015.

As Bloomberg reports, a wild card in the election is former Greek Prime Minister George Papandreou who on 3 January announced the formation of a political party called the Democratic Socialists. Papandreou, a former leader of the Socialists (Pasok), was prime minister from October 2009 to November 2011.

Source: Ekathimerini, Bloomberg

Updated

Germany rebuts Grexit claims

The German government has poured more cold water on that Spiegel story that Angela Merkel is ready to see Greece exit the eurozone.

Via the wires:

- German govt spokesman says there is no change in stance of the German govt towards Greece.

- German finance ministry spokesman, we expect Greece to stick to its commitments.

- German govt spokesman says Greece has long-term commitments, a new govt will not change that.

Mounting pressure on ECB as German inflation falls

The European Central Bank is coming under growing pressure to inject a dose of stimulus in the eurozone, amid mounting evidence of falling prices.

German inflation is expected to have fallen in December, when data is published later today.

Figures from five German states released this morning showed across-the-board declines in the annual inflation rate, largely because of falling energy prices.

German regional CPIs point to downward bias. #Germany's dec #Inflation probably just 0.2% vs 0.3% exp. (via Citi) pic.twitter.com/GORxvqThl8

— Holger Zschaepitz (@Schuldensuehner) January 5, 2015

Uh-oh... German state inflation rates droop further http://t.co/mVQIDJbRvx pic.twitter.com/hNX2lBsfGm

— Robin Wigglesworth (@RobinWigg) January 5, 2015

Reuters reports from Berlin:

Prices in the big state of North Rhine-Westphalia inched up just 0.1% down sharply from a 0.7% rise in November.

In Bavaria, prices rose 0.3% year-on-year, down from 0.8 %. In Hesse, annual inflation fell to zero from 0.5 % in the prior month, while in Baden-Wuerttemberg inflation slowed to 0.1 % from 0.5 % previously.

A preliminary pan-German inflation figure for December is due to be released on Monday at 1300 GMT. Broader inflation data for the entire 19-nation euro zone is due on Wednesday.

Last week ECB President Mario Draghi said the risks to price stability had increased and the bank had to be ready to act.

European Central Bank boss hints at stimulus to fight deflation

BoE expected to delay rate rise

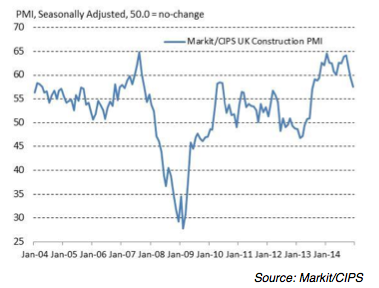

Slowing growth in the UK construction industry has heightened expectations that interest rates will remain unchanged for most of 2015.

Howard Archer, chief UK economist at IHS, says the prospects for construction look decent, although it is likely to expand at a slower rate in 2015 than the previous year.

Following on from a weaker manufacturing survey, the softer December construction purchasing managers’ survey will likely sustain strong belief that the Bank of England will not be raising interest rates before the latter months of 2015. There can be no doubt that the Bank of England will kick off 2015 by keeping interest rates unchanged at 0.50% at the conclusion of the January MPC meeting on Thursday

Updated

This graph tells the 10-year story of the UK construction industry: a massive fall in 2009 and faltering return to growth.

David Noble, chief executive officer at the Chartered Institute of Procurement & Supply, the co-organiser of the survey, said construction was on a weaker trajectory than that seen in recent months.

The sector is still expanding with the index posting at a higher level than the longer-term average, and led primarily by residential development - but it has become a victim of its own success as it struggles to keep up with its own speed of recovery. With increases in new business, comes pressures on the availability of talented staff and a squeeze on the performance of supply chains.

He said the election was making construction managers more cautious.

Levels of positive outlook remain high with 52% of respondents expecting a rise in business activity in 2015, though this month’s sudden drop in the strength of the civil engineering sub-sector and this year’s General Election is adding a note of caution.

I expect we will hear a lot more of this argument in the next four months...

Biggest year for homebuilding since 1997

Growth in the UK construction industry slowed in December to a 17-month low, despite a sharp increase in home building, according to the latest monthly Markit/CIPS survey.

According to Markit, 2014 was the best year for British house building since records began in 1997.

But a decline in civil engineering projects meant that overall construction saw slowing growth.

The headline figure was 57.6 in December, down from 59.4 in November on an index when anything over 50 counts as expansion.

Tim Moore, senior economist at Markit and author of the Markit/CIPS Construction PMI, said:

UK construction output growth retreated further in December, but another strong expansion of house building activity ensured that the sector continued to perform impressively overall. Indeed, over the course of 2014, UK construction firms recorded the strongest calendar year of residential building since the survey began in 1997.

A sharp recovery in house building, as well as resurgent demand for commercial development projects, continued to boost staff recruitment and sub-contractor pay rates across the construction sector in December.

Updated

UK contruction industry expansion slows

Breaking news: the British construction industry grew at its slowest rate since July 2013, although residential building remained robust.

Around 1 million extra passengers flew Ryanair in December as the budget airline’s attempts to be nicer to customers seems to be paying off.

My colleague Sean Farrell reports:

The number of customers flying with the Irish carrier jumped 20% to 6.02 million as seat occupancy rose to 88% from 81% a year earlier. Ryanair used to ground many of its aircraft during winter, but this year it has filled more seats while flying more planes.

In the year to December, Ryanair’s customer numbers rose 6% to 86.4 million customers.

Ryanair’s shares are up 0.3%, bucking the downward trend on the FTSE.

European stocks stage modest recovery after opening falls

European stock markets have got off to a mixed start. Most of the main bourses opened down on reports of a Greek exit from the eurozone, but have since recovered. France and Germany’s main exchanges have edged into positive territory, after falling in early trading.

- FTSE100 -0.2% at 6,531 points

- Germany’s DAX +0.2% at 9,785 points

- France’s CAC +0.44% at 4,271 points Was down 0.7%

- Italy’s FTSE MIB -0.26% at 19,067 points

- Athens ATG index -0.9% at 826 points Was down 1.9%

Updated

Hollande: Greeks must decide on euro future

François Hollande has said it is up to Greece to decide whether they wish to remain in the single currency.

Speaking on French radio this morning he said:

When it comes to Greece’s membership of the eurozone, it is for Greece alone to decide.

Arguably, the weakness of the French economy could be more decisive for the eurozone.

Hollande said he hoped economic growth would be above 1% in 2015 and 2015 - higher than official forecasts.

Adopting the masochism strategy, he also took responsibility for high unemployment and the weak state of the French economy.

I am president of the Republic. I am not going to say [France’s low growth] is the fault of the foreigner... the fault of the crisis.

Source: RFI

Rouble falls agains the dollar

It is an unhappy start to the new year for the Russian currency.

The Russian rouble has fallen by almost 5% against the dollar to 58.51 roubles in early trading after oil prices hit a five-year low.

A barrel of Brent crude fell to $51.40 on Monday, its lowest since May 2009.

Russia depends on oil revenues for more than half its state budget.

Dyson warns on May's immigration plan

An interesting business story on the Guardian’s front page today:

The entrepreneur and inventor Sir James Dyson has hit out at Teresa May’s plans to expel international students once they have graduated.

The home secretary wants the Conservatives to make a manifesto commitment to force students from outside the EU to leave the UK on completing their degrees.

Sir James Dyson, best-known for his bagless vacuum cleaners, described the plan as “short-sighted”.

In an article in the Guardian he writes:

Theresa May’s latest ploy to swing voters concerned about immigration magnifies my worry: she wants to exile foreign students upon qualification from British universities. Train ’em up. Kick ’em out. It’s a bit shortsighted, isn’t it? A short-term vote winner that leads to long-term economic decline. Of course the government needs to be seen to be “doing something”. But postgraduate research in particular leads to exportable, patentable technology. Binning foreign postgraduates is, I suppose, a quick fix. But quick fixes don’t build long-term futures.

Updated

Summary

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and the business world.

The euro has fallen to a nine-year low against the dollar this morning, following a report that German chancellor Angela Merkel is ready to see Greece leave the currency union.

According to the report in the weekly magazine Der Spiegel, German officials believe a Greek exit is almost inevitable in the event that left-wing opposition party Syriza wins the Greek election on 25 January.

The magazine quotes German government officials, who sound pretty relaxed about a Grexit.

One source said:

The danger of contagion is limited because Portugal and Ireland are considered rehabilitated.

This line was echoed by Fredrik Erixon, director of the European Centre for International Political Economy in Brussels.

He told Bloomberg

Many European officials believe a Greek exit would be manageable, and in contrast to 2010-2011, we wouldn’t see the same cascading effect on countries like Spain or Ireland.

But the German government has insisted it wants Greece to stay in the eurozone.

Sigmar Gabriel, the German economy minister and leader of the Social Democrats, said there were no plans for Greece to leave the currency union.

That is why we can’t be blackmailed and why we expect the Greece government no matter who leads it, to abide by the agreements made with the EU.

The euro fell to 1.18605 against the dollar on Monday, its lowest since March 2006, but later edged up to 1.1948

The expectation of monetary stimulus from the European Central Bank is also driving sentiment on currency markets, after ECB chief Mario Draghi dropped a heavy hint of more action in an interview last week.

We are also expecting data on German inflation and UK construction PMI figures.

All that and more to follow...