Why is there so much confusion around trusts? In my opinion, it is because they are often used the wrong way and not used for the right reasons.

We had some clients whose attorney tried to get them to do a trust they did not need.

Fortunately, they had a reliable guide to step in and tell them they did not need to spend the money to get a trust.

So how do you know if you need a trust? Let's dive in.

There are two types of trusts:

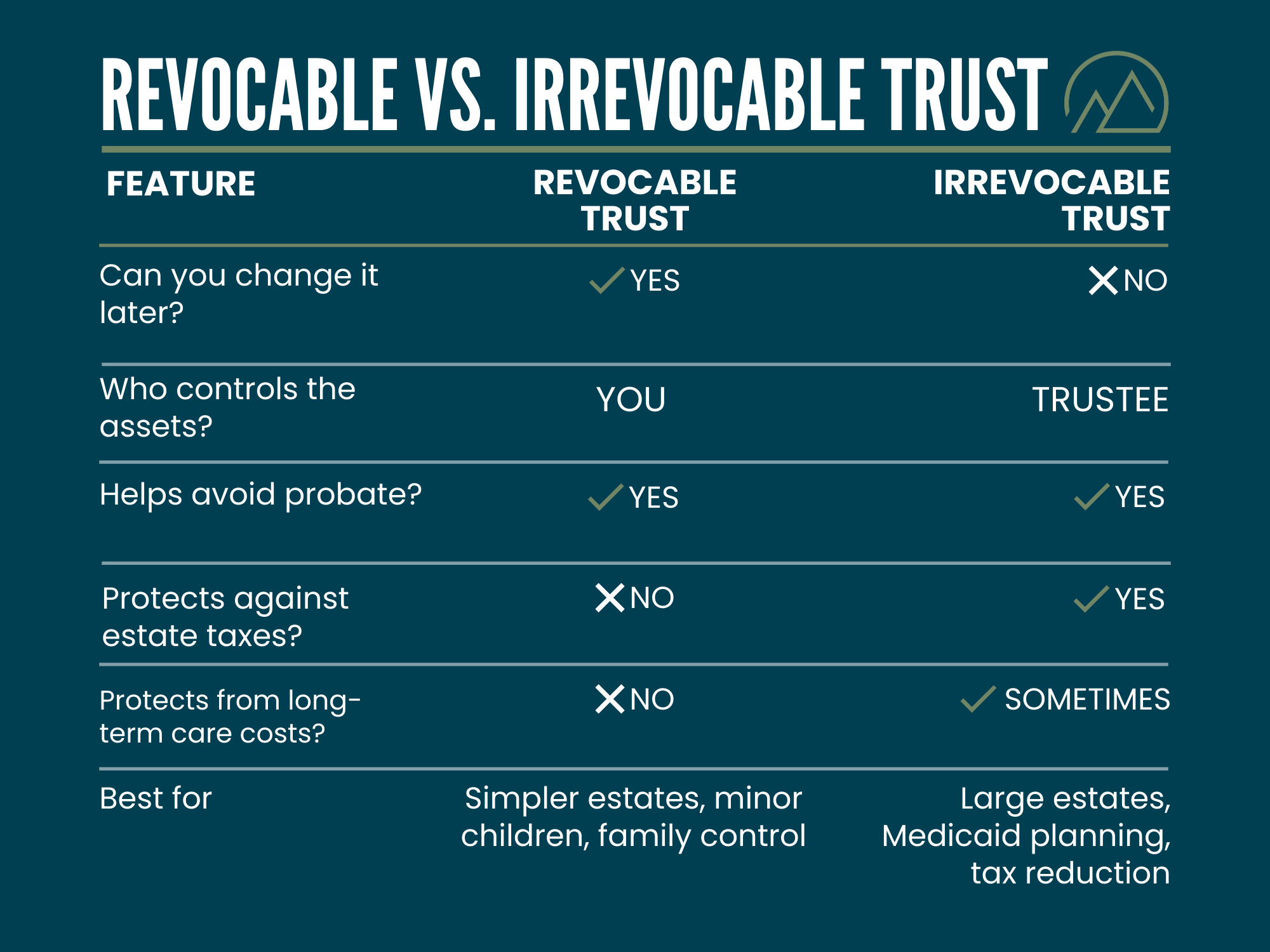

1. Revocable trust

This is the simpler of the two types of trusts. There are some great uses for it, but we see this type of trust misused often because most people do not need it (especially our clients who are in or near retirement).

Some of the time, if they do not have a complex situation, basic estate planning documents will suffice and, in turn, be more affordable than establishing a trust. Especially if they are in a state that offers the ability to title their home as transfer on death (TOD) and avoid probate.

This type of trust could be good in certain circumstances, such as when you:

Don't trust your kids. Some may laugh at this, but there are certainly times when this can be the case. With this trust, you can limit how much your children are able to spend each year.

We had a client who allowed her kids to take out only $20,000 per year from her estate.

We also had a client take a more extreme approach and didn't allow her children to touch the money until they were 60. At least they will have a great retirement!

Want to keep your money in your bloodline in case, for example, a divorce happens.

Have minor children (under 18). In this case, a trust can be important to ensure they have detailed plans for using the funds.

2. Irrevocable trust

You should consider using this type of trust if you are looking to protect against long-term care costs and estate taxes. But understand, just like the revocable trust, not every client needs this.

Who might benefit from this trust?

Those who may need long-term care protection may need to consider this type of trust. We commonly see irrevocable trusts used in times of Medicaid planning, which is a way to shield your assets from being accessed if you were to need them for long-term care events.

The idea is that if you move the assets out of your estate, then they are safe.

Keep in mind that you must have moved the assets out for a period of time in order for them not to be counted for Medicaid purposes. Here in Ohio, that is five years, but it could be different depending on the state you are in.

This type of trust is also used for estate planning. This is not a concern for many people right now, considering that estate taxes don't kick in until the value of your estate reaches $15 million.

However, even if you do not have that much wealth, I would still encourage you to consider planning for estate taxes. Why? The estate tax threshold has been well below $1 million in the past. Do you think the government will find ways to get hardworking and smart people to pay more taxes?

The way estate taxes work is that any money you have over the limit could be taxed at a 40% tax rate, leaving almost as much money to Uncle Sam as your beneficiaries.

The good news? You can find ways to avoid having Uncle Sam as a beneficiary when it comes to estate taxes. This could involve using a tool like an irrevocable trust.

Remember that most irrevocable trusts do not allow you to retain ownership of the assets you put into it.

However, if you structure it the right way, then you could still be able to access it and benefit from using it.

Pro tip: Be aware of listing your trust as an IRA beneficiary.

If you pass away and leave your IRA to a trust, then you would pay "trust rates," which could be as much as 37%.

Instead, if you leave your IRA to a person rather than a trust, your beneficiary would pay only federal income tax rates, which, for most, would be 12% to 24%.

In the end, we would advise working with a retirement planning team that assists with estate planning and helps in facilitating the estate planning documents you need.

At our firm, we refer to this as a "one-stop shop." A one-stop shop financial planning team can make sure you get what you need and get it done the right way so that you do not have to pay more taxes and fees than you need to.

Related Content

- Eight Types of Trusts for Owners of High-Net-Worth Estates

- Four Reasons Retirees Need a (Revocable) Trust

- Here's What Being in the 2% Club Means for Your Retirement

- Are You a 'Midwestern Millionaire'? Four Retirement Strategies

- Five Opportunities if You're in the 2% Club in Retirement

This article was written by and presents the views of our contributing adviser, not the Kiplinger editorial staff. You can check adviser records with the SEC or with FINRA.