Investors should welcome the subdued growth rates projected for corporate earnings in the current and subsequent quarters.

That’s not our instinct, of course, since at first glance the sharply declining earnings growth rate seems alarming. Facebook’s parent Meta Platforms (FB) reported disappointing earnings and future growth prospects, and its stock plunged more than 26%. Before that, Netflix (NFLX) earnings fell short of Wall Street expectations, and its stock plunged 22%.

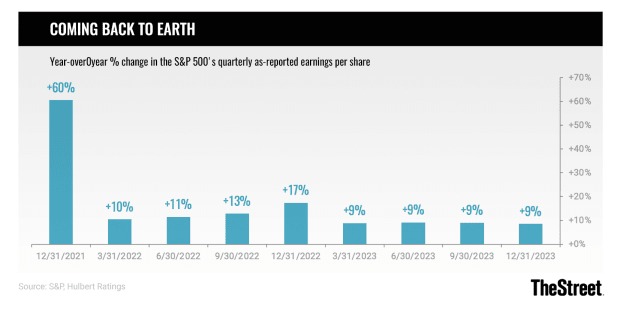

Though these two examples are extreme, the disappointing earnings these two companies reported are consistent with what Wall Street is experiencing generally. In the fourth quarter of 2021, the S&P 500’s earnings per share are estimated to have been 60.5% higher than in the comparable quarter of 2020. (I say “estimated” because we don’t yet know the final number, since not all companies have reported. The 60.5% year-over-year increase is calculated on the basis of the two-thirds of S&P 500 companies that have reported and S&P estimates for the remaining third.)

In contrast, for the first quarter of 2022 — the current quarter, in other words — the comparable year-over-year growth rate is estimated by S&P to be 10.4%. (See chart.) And since Wall Street analysts are often too optimistic, it’s entirely possible that the final number will be even lower.

TheStreet

The reason I say that investors might want to welcome the lower earnings growth rate traces to research conducted by Ned Davis Research. The firm reports that the S&P 500 has produced above-average performance in quarters with earnings growth rates similar to what’s projected for the current quarter. The relevant statistics, reflecting data back to 1927, appear in the table below.

To be sure, the data in the table reflect averages, and there’s considerable variation from quarter to quarter. Take the last quarter of 2021: Even though the blistering earnings growth rate it experienced is associated with a barely positive average return for the overall market, the S&P 500 nevertheless rose for the quarter at an annualized rate of nearly 50%. You can chalk up this up to either random fluctuations or the stock market getting ahead of itself in the last months of 2021.

Yet another possibility is that the historical precedents no longer apply. But the economic theory underlying those precedents seems more relevant than ever these days: Too-fast earnings growth rates indicate an overheated economy that will, in turn, force the Federal Reserve to raise interest rates. From this perspective, a more subdued growth rate is less likely to force the Fed’s hand, and therefore more likely to be sustainable.

The current quarter is already nearly half over, and far from rising at the robust rate that the historical average suggests, it has declined 5.9% — equivalent to an annualized loss of 22%. It’s always possible that the market will be a loser for the entire quarter, or that it could recover smartly over the next six weeks and finish the quarter with gain.

Regardless, the point of this walk down memory lane is that a declining earnings growth rate is not, in and of itself, a reason to give up on the stock market.

Rising interest rates, inflation and market volatility are on the horizon. You don’t want to miss out on this exclusive opportunity to unlock Action Alerts PLUS at our lowest price of the year.