Burbank, California-based The Walt Disney Company (DIS) operates as a global entertainment company. Valued at $214.9 billion by market cap, the company's businesses include media networks, parks and resorts, studio entertainment, consumer products, and interactive media.

Shares of this entertainment giant have outperformed the broader market over the past year. DIS has gained 27% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 16.6%. However, in 2025, DIS stock is up 7%, compared to the SPX’s 7.8% rise on a YTD basis.

Zooming in further, DIS’ outperformance looks less pronounced compared to the Communication Services Select Sector SPDR ETF (XLC). The exchange-traded fund has gained about 26.7% over the past year. However, the ETF’s 11% gains on a YTD basis outshine the stock’s single-digit returns over the same time frame.

Disney's outperformance is driven by strong Q2 earnings, streaming momentum with 126 million Disney+ subscribers, and growth in domestic parks and experiences. The company also expects double-digit segment operating income growth in Entertainment for fiscal 2025, which is expected to fuel the rally and positive analyst sentiment.

On May 7, DIS shares closed up by 10.8% after reporting its Q2 results. Its adjusted EPS of $1.45 exceeded Wall Street's expectations of $1.18. The company’s revenue was $23.6 billion, beating Wall Street forecasts of $23.1 billion. DIS expects full-year adjusted EPS to be $5.75.

For the current fiscal year, ending in September, analysts expect DIS’ EPS to grow 16.3% to $5.78 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

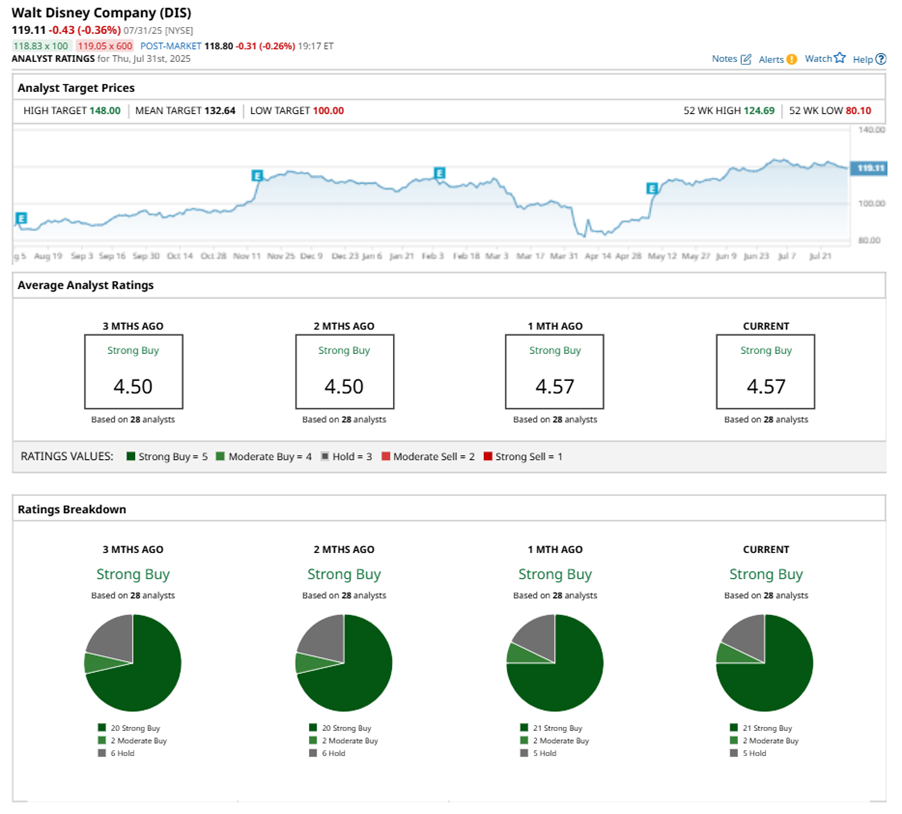

Among the 28 analysts covering DIS stock, the consensus is a “Strong Buy.” That’s based on 21 “Strong Buy” ratings, two “Moderate Buys,” and five “Holds.”

This configuration is more bullish than two months ago, with 20 analysts suggesting a “Strong Buy.”

On Jul. 29, Mizuho Financial Group, Inc. (MFG) maintained a “Buy” rating on DIS with a price target of $138, implying a potential upside of 15.9% from current levels.

The mean price target of $132.64 represents an 11.4% premium to DIS’ current price levels. The Street-high price target of $148 suggests an upside potential of 24.3%.