/Hilton%20Worldwide%20Holdings%20Inc%20grand%20vacations%20sign%20by-%20jewhyte%20via%20iStock.jpg)

McLean, Virginia-based Hilton Worldwide Holdings Inc. (HLT) operates as a hospitality company that owns, leases, manages, develops, and franchises hotels and resorts. With a market cap of $63.8 billion, Hilton operates through the Management & Franchise and Ownership segments.

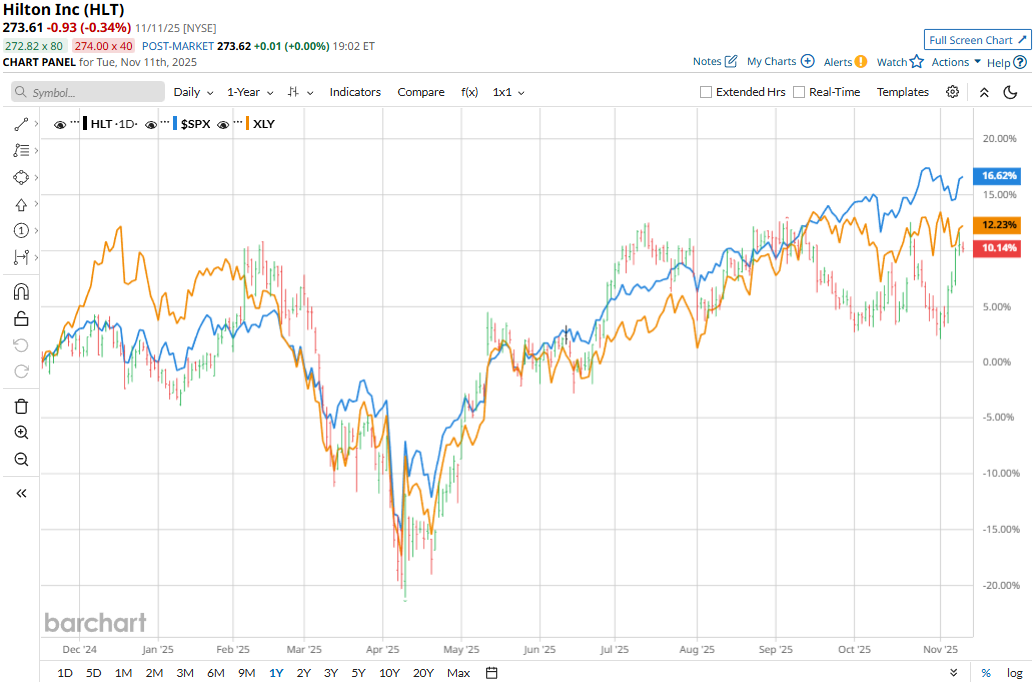

The hospitality giant has notably lagged behind the broader market over the past year. HLT stock prices have gained 10.7% on a YTD basis and 9.3% over the past 52 weeks, compared to the S&P 500 Index’s ($SPX) 16.4% returns in 2025 and 14.1% gains over the past year.

Narrowing the focus, Hilton has outpaced the sector-focused Consumer Discretionary Select Sector SPDR Fund’s (XLY) 6.8% uptick in 2025 and 9.2% gains over the past 52 weeks.

Hilton’s stock prices gained 3.4% in the trading session following the release of its better-than-expected Q3 results on Oct. 22. The company’s system-wide comparable revenue per available room declined 1.1% on a currency-neutral basis compared to the year-ago quarter. However, after considering the impact of forex translation and 23,200 net new room additions, the company’s topline observed a notable growth. Overall, its topline came in at $3.1 billion, up 8.8% year-over-year and 3.5% above Street expectations. Further, its adjusted EPS increased 9.9% year-over-year to $2.11, beating the consensus estimates by 3.9%.

For the full fiscal 2025, ending in December, analysts expect HLT to deliver an adjusted EPS of $8.02, up 12.6% year-over-year. Further, the company has a solid earnings surprise history. It has met or surpassed the Street’s bottom-line estimates in each of the past four quarters.

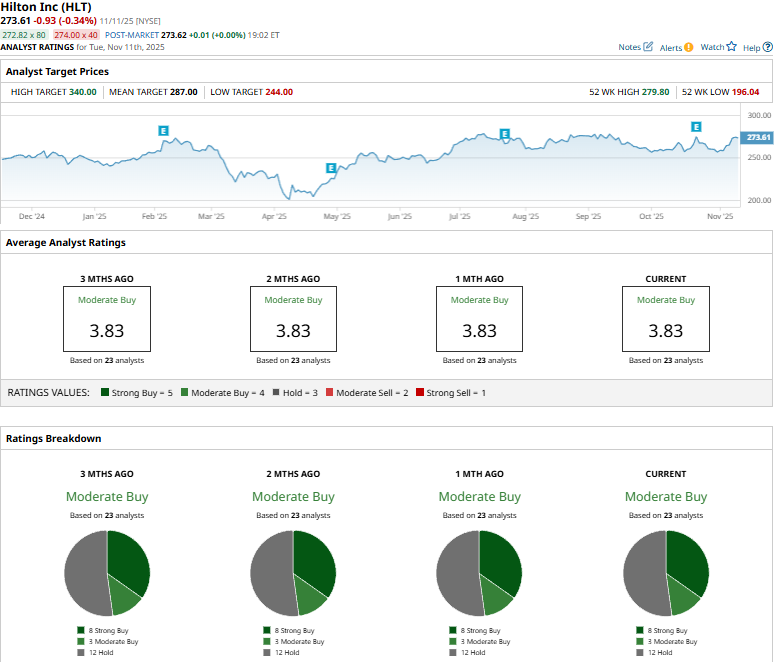

Among the 23 analysts covering the HLT stock, the consensus rating is a “Moderate Buy.” That’s based on eight “Strong Buys,” three “Moderate Buys,” and 12 “Holds.”

This configuration has remained stable over the past three months.

On Oct. 24, Truist Securities analyst Patrick Scholes maintained a "Hold" rating on HLT and raised the price target from $246 to $253.

Hilton’s mean price target of $287 represents a modest 4.8% premium to current price levels. Meanwhile, the street-high target of $340 suggests a notable 24.3% upside potential.