Time for a quick afternoon summary:

- Greece has made a €450m debt repayment to the International Monetary Fund.

- The head of the IMF, Christine Lagarde, has rang the alarm bell about the eurozone in a speech that pointed to the risks of low growth and high unemployment.

- Tens of thousands of people have demonstrated against public spending cuts in towns and cities across France.

- European markets are slightly up on the day. French investors have shrugged off today’s nationwide strikes - the CAC 40 is up by more than 1% at 5,192 points. The FTSE 100 is up 1% at 7008.12 pence; Germany’s DAX is up 0.74% at 12,125 points.

That is all from us today. Thank you for following and for all your comments.

Hot off the press:

The boss of the International Monetary Fund has made an impassioned plea for governments to make the next decade one of sustainable and inclusive growth that cuts national debt burdens and tackles high unemployment, writes the Guardian’s economics correspondent Philip Inman.

Christine Lagarde warned that developed and emerging economies still suffering the after-effects of the 2008 crash must collaborate better to avoid an era of low growth.

Speaking ahead of the Washington-based organisation’s spring conference next week, Lagarde welcomed a recovery in the US and UK, which she said was “firming up”, but voiced concerns about the eurozone and pointed to Russia and Brazil as major trading nations in economic trouble.

With overall growth moderate, the global economy continues to face a number of significant challenges. For example, what I have called the ‘low-low, high-high’ scenario: the risk of low growth-low inflation and high debt-high unemployment persists for a number of advanced economies.

Read the full story here.

If you are a really keen, you can watch Lagarde speak via this video link.

In Paris a large rally has taken place today against public spending cuts. Tens of thousands of people have been marching in towns and cities across France, with the largest demonstration in the capital.

Trade union leaders (pictured above) have led the marchers, although one of the largest unions, the CFDT, declined to take part. It argues that the savings the government wants to make are not on the same scale as austerity in other eurozone countries.

Airlines, such as Air France, Easyjet and Ryanair, have cancelled hundreds of flights. Radio France has scaled back programming, as part of an ongoing four-week industrial dispute. The Eiffel Tower was closed.

Updated

Markets are undoubtedly cheered by the news that Greece has made a €450m debt repayment to the IMF.

In the US, the latest weekly jobless claim numbers came in lower than expected. The number of claimants increased by 14,000 to a seasonally adjusted 281,000 for the week ended 4 April, the Labor Department said.

Economists had predicted a bigger rise to 285,000. The figures for the week before were also revised down by 1,000.

There were no nasty surprise from the Fed last night either, which has helped to underpin investor confidence today.

This from CMC’s Michael Hewson:

Last nights Fed minutes didn’t tell us anything that we didn’t already know, given the removal of “patience” from the guidance language, and the differences of opinion articulated by several members since that meeting.

The minutes did show us that members were split three ways between a potential lift off [in rates] in June, and a lift off in September with at least two favouring a delay until 2016, which suggests that the consensus needed for a change in policy still remains some way off.

Given that these minutes pre dated the most recent economic data we can probably presume given recent comments that those who favoured a June move could well be revising that assessment, indeed Atlanta Fed President Dennis Lockhart stated as much in comments earlier this week, when he talked about a possible July or September window.

US markets mixed; European markets build on gains

US markets are relatively quiet:

- Dow Jones: -0.1% at 17,894.33

- S&P 500: +0.2% at 2,087

- Nasdaq: +0.0.1% at 4,379.72

Meanwhile European markets have built on earlier gains and the FTSE is back above the 7,000 mark.

- FTSE 100: +0.9% at 7,001.6

- Germany’s DAX: +0.7% at 12,124.68

- France’s CAC: +1% at 5,190.18

- Italy’s FTSE MIB: + 0.8% at 23,776.52

- Spain’s IBEX: +0.5% at 11,718.6

Greece repays IMF loan

It’s official. Greece has successfully completed the repayment of a €450m IMF loan owed today according to a Greek government official.

The payment has been made.

Short and sweet.

Updated

Varoufakis: Greece is frustrated by lack of progress on reforms

The Greek finance minister said Greece is not entirely happy with the way the negotiations on reforms is being approached by its creditors.

The Greek government would like to press ahead with certain urgent reforms before agreeing on others, but the process dictates that the whole package must be agreed upon first.

He used the Greek banks’ non-performing loans - 35-40% of all loans - as an example. The government would like to create a bad bank for nom-performing loans to kickstart the flow of credit into the financial system.

We are keen to begin implementing this yesterday, but everything is on hold until the negotiations are finished.

We want to get on with the low hanging fruit and then move on to the high hanging fruit.

The conversation ends with Joseph Stiglitz heaping praise on Varoufakis, and describing the discussion as “spectacular”.

Few finance ministers are as ready and economics literate as @yanisvaroufakis says @josephstiglitz #NewThinkingParis

— The Institute (@INETeconomics) April 9, 2015

Varoufakis says that Greece needs to agree three key things with its eurozone partners:

- An appropriate primary surplus

- An investment package for the productive parts of the Greek private sector

- A serious discussion about Greek debt [he stresses he is not talking about a debt haircut]

#Varoufakis: "The crisis has taken such a turn where the line bw Left and Right has been blurred."

— The Greek Analyst (@GreekAnalyst) April 9, 2015

Varoufakis gives a sense of the pressure felt by the new Greek government immediately on being elected in January.

In conversation with American economist and Nobel Laureate Joseph Stiglitz, he said:

The day after we were elected we faced an asphyxiatingly tight timetable.

We went to our partners and said: can we find some common ground? Can we extend our deadline from the one month we have, so that we can sit around the table and think about what needs to be done?

[We needed a plan] to ensure that Greece no longer features in the headlines.

Varoufakis: reform is a dirty word in Greece

Yanis Varoufakis:

Reform is a word that resonates in Greece like the word democracy does in Iraq. Reform is a dirty word in Greece.

If people hear the word reform in Greece they think their pensions will be cut. Small businesses think VAT will be increased.

We need to give reform a good name again. Greece has to become a reformable society again. We are keen to sit down with our partners and prioritise reforms.

Varoufakis: euro crisis was inevitable

Yanis Varoufakis, the Greek finance minister, is appearing on a panel at a conference hosted by The Institute for New Economic Thinking at the OECD in Paris.

He says that while the crisis in Greece in 2010 threatened the disintegration of the eurozone, the same country is now bringing about consolidation.

He hopes the eurozone can end the “toxic” tendency of one eurozone country turning against another. [Wonder who he is talking about?]

Varoufakis says a eurozone crisis was always inevitable.

The way we designed the eurozone was crying out for a crisis like this to happen.

As my colleague Katie Allen reported over the weekend:

The last time UK interest rates were on hold for a longer stretch was between 1940 and 1951 when the UK was ravaged first by war and then by reconstruction efforts, as it was led by a succession of governments (including Clement Attlee, who was prime minister between July 1945 and October 1951).

Bank rate was cut from 4% to 2% during 1939 and then stayed there until a hike to 2.5% in November 1951.

There was next to no chance of any drama today.

Most economists agree that the next move in UK rates will be up, but with annual inflation falling to a record low of zero in February, there is no pressure on the MPC to raise borrowing costs at the current time (despite a backdrop of economic growth).

Victoria Clarke, economist at Investec:

At present the outlook for UK interest rates is receiving relatively little attention, in part because the general election is stealing the limelight but also because the February record low zero inflation rate has left many thinking lift-off for rates is now a way off.

Our suspicion is that we could well see rate lift-off talk re-ignite before too long, particularly if UK recovery momentum builds through the spring against a background of an improving euro area economy, helping the UK’s external position.

Updated

Bank of England holds rates at 0.5%

No pre-election shocks here.

The Bank of England’s Monetary Policy Committee has left interest rates on hold at 0.5% and quantitative easing unchanged at £375bn at its final meeting before the general election on 7 May.

Rates have been in hold for the entire duration of this parliament, and longer - the MPC cut rates to an all-time low of 0.5% in March 2009.

Further details about the mood of the nine members of the MPC will be revealed on 22 April when the minutes of the meeting are published.

Over in Athens, senior government ministers are expressing confidence that Greece will successfully conclude negotiations over reforms with its creditors in the coming weeks.

The Guardian’s Helena Smith reports:

Sounding more optimistic than perhaps any other leading Greek government official to date, the minister of state, Alekos Flambouraris, said he expected Athens to have sealed a deal with international creditors by the time euro area finance ministers hold their next scheduled meeting on 24 April.

“At the Euro Group on April 24 there will 100 per cent be an agreement,” he told Mega TV on Thursday morning.

“The institutions [EU, ECB and IMF] are taking a hard line, it is the strategy they are following, but we aren’t accepting it and in the end they will back down. It is not in their interest to not release funds,” insisted Flambouraris who is often described as a mentor figure for prime minister Alexis Tsipras.

“We are not going to give in to pressure and we will succeed in getting an agreement.”

Some more reaction now to those poor UK trade figures earlier, which showed the trade in goods deficit hit a seven-month high of £10.3bn in January as exports fell but imports rose.

The British Chambers of Commerce (BCC) says the trade figures are the latest evidence that the government’s hoped-for rebalancing towards more manufacturing and exports remains elusive.

David Kern, the BCC’s chief economist:

It is clear that the UK is not yet making adequate process to rebalance the economy towards net exports.

Unless we see firm action to improve our export performance, it is not clear how we will sustain strong growth in the long-term.

The UK’s trade deficit with the EU reached a record high in the last three months, and while the EU is our largest trading partner, it is vital that we capture more of the export market in the fast growing economies beyond Europe.

John Allan, chairman of the Federation of Small Businesses:

Despite recent positive signs from the UK’s trade deficit, there has been little indication of sustained improvement in overall export performance. This is partly due to challenging conditions in key export markets such as Europe, but it underlines why supporting businesses to export, particularly in emerging markets, must remain at the forefront of policy thinkers’ minds.

Whoever forms the next government must think about how they will help business to find new markets overseas. Support needs to be coherent and link with other advice and training, matching the ambition of our start-ups and small firms that want to grow and develop into the British success stories of the future.

Alan Clarke, economist at Scotiabank, said the trade figures backed up other official data suggesting growth may have slowed in the first quarter of 2015 from 0.6% in the fourth quarter of 2014.

Unofficial business surveys - notably the PMI surveys on the services, manufacturing and construction sectors - are indicating stronger growth.

Clarke:

Before today’s trade data it was a coin toss between whether to believe the strong PMI data (which pointed to strong GDP) or the weak output data (pointing to weak GDP).

On the back of the trade data, my bias is on the output data. I think we are looking at a very good chance of GDP growth slowing to just 0.4% quarter-on-quarter in Q1.

Updated

Greek deflation slows

Annual consumer prices deflation slowed to 2.1% in Greece in March, from 2.2% in February.

Greece’s EU-harmonised rate of deflation, which brings it into line with the rest of the eurozone, was 1.9% in March, unchanged from February.

Greece has been in deflation for the last 25 months, as wage and pension cuts as well as a severe downturn have weighed on prices.

Easing deflation in Greece will cheer policymakers at the European Central Bank, which is in the process of pumping €1.1 trillion into the eurozone financial system in an attempt to boost growth and ward off a deflationary spiral in the wider region.

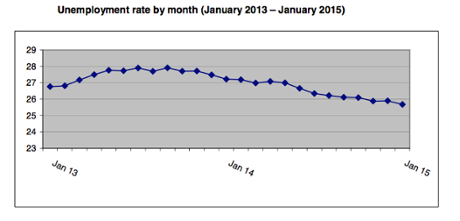

Greek unemployment eases

The Greek unemployment rate eased slightly to 25.7% in January from 25.9% in December according to the statistics agency Elstat.

The jobless rate has been falling after hitting a record high of 28% in September, but remains more than double the eurozone average of 11.3% in February.

There were 1.2m unemployed people in Greece in January, down 13,435 compared with December.

Youth unemployment remains high in Greece, at 50.1% in January.

UK trade deficit widens; pound falls

A nasty set of trade figures for the UK this morning.

The UK’s trade in goods deficit widened unexpectedly in February to a seven-month high of £10.3bn from £9.2bn in January. It was driven by a fall in exports, while imports rose according to the Office for National Statistics.

Exports of goods fell by £900m over the month to £23.2bn - the lowest in almost four and a half years. Imports meanwhile rose by £300m.

The pound fell to its lowest level against the dollar in more than a week after the figures were published. It fell 0.7% to $1.4763.

The euro rose against the pound to 72.785p from 72.66p.

The export-led recovery so-hoped for by the government has failed to materialise, with economic growth still heavily dependent on the services sector and consumer spending.

Rebalancing, what rebalancing?

In 2012, George Osborne set a target of doubling UK exports to £1 trillion by 2020. A major part of the plan was to become less dependent on exports to Europe, instead opening up trade links with faster growing economies such as China and India.

This didn’t go to plan in Feb according to the ONS:

“The widening of the trade deficit between January and February 2015 mainly reflects a fall in exports of goods to non-EU countries, particularly to the United States.”

Paul Hollingsworth, economist at Capital Economics:

February’s trade deficit came in worse than expected and will have re-ignited fears that the strong pound and weakness in demand in the euro-zone is acting as a straightjacket on exporters.

Updated

Before one Greek deadline has passed, we’ve got another one to contend with.

Eurozone deputy finance ministers have given Greece a deadline of six-working days to come up with revised reform proposals according to the Greek newspaper Kathimerini.

The two sides met in Brussels on Wednesday. The deadline has apparently been set so that a deal can be reached at a Eurogroup meeting on 24 April, unblocking the bailout aid so badly needed by Greece.

Without the funds, a “Grexident” - accidental Greek exit from the euro - is a distinct possibility.

Michael Hewson chief market analyst at CMC Markets UK, is sceptical that this latest deadline will make any difference.

Yesterday’s talks between Greece and the Eurogroup ended with the Eurogroup issuing the Greeks with an ultimatum to present acceptable proposals for fiscal, pension and labour market reform in the next six days, whatever that means.

Given that we’ve been here so many times before, ultimatums generally only work when there is a threat of a significant sanction at the end of the deadline, and short of throwing Greece out of the euro it would seem that any sanction is likely to be limited, particularly if Greece continues to muddle through.

Updated

Greece has paid the IMF according to some on Twitter, but no official confirmation yet...

Greece repays €448m to IMF - BREAKING - http://t.co/RUywL6Ci0o

— enikos_en (@enikos_en) April 9, 2015

Confirmed: #Greece has forwarded €448ml repayment to #IMF.

— Yannis Koutsomitis (@YanniKouts) April 9, 2015

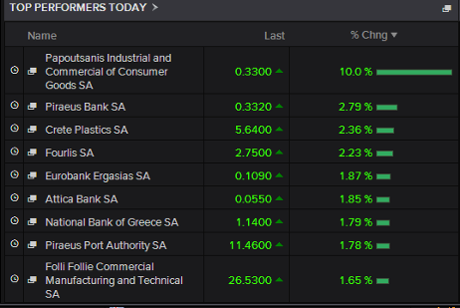

Greek shares are also up this morning, with the ATG index rising 0.7% to 773.09.

Top risers:

European markets open higher

European markets are up this morning.

A lack of nasty surprises in the Federal Reserve minutes last night (more on that soon), and expectations that Greece will honour its debt repayment today appear to have boosted investors.

- FTSE 100: +0.5% at 6,968.92

- Germany’s DAX: +0.5% at 12,092.52

- France’s CAC: +0.6% at 5,165.77

- Italy’s FTSE MIB: +0.5% at 23,685.32

- Spain’s IBEX: +0.1% at 11,663.6

Greek official: we will pay up today

An unnamed Greek government official has told Reuters that Athens will repay the €450m instalment due today.

The payment has been scheduled and will go out later today.

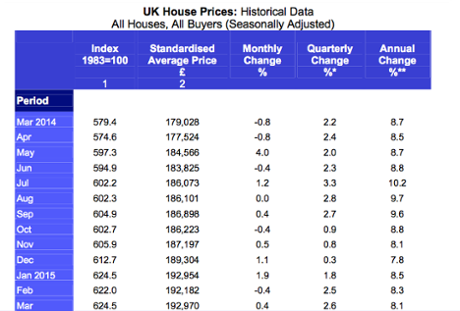

Halifax: UK house prices rise 0.4% in March

The average price of a UK house rose 0.4% last month, to £192,970 according to mortgage lender Halifax.

It followed a 0.4 fall in prices in February, and beat economists’ expectations of a 0.2% increase.

Prices were 7.8% higher than March 2014. However, Halifax prefers to use quarterly comparisons to calculate annual house price changes. On that basis, annual house price inflation slowed to 8.1% in March from 8.3% in February.

Martin Ellis, housing economist at Halifax, said house price growth was likely to slow as 2015 progressed.

The recent return to real earnings growth for the first time in several years, very low mortgage rates and last December’s stamp duty changes are supporting housing demand.

The rising level of house prices in relation to earnings should, however, curb house price growth and activity. The annual rate of house price growth, which has continued to ease in the first quarter of 2015, is forecast to end the year at 3-5%.

Agenda: Lagarde speaks; Bank of England decision

We will of course be keeping a very close eye on developments in Greece, as well as the other key events and data out today.

Please keep your comments coming.

- The Bank of England’s Monetary Policy Committee will publish its April decision at noon. While no change is expected - rates will almost certainly be left on hold at 0.5% and quantitative easing remain unchanged at £375bn - it is a historic moment. It is the final decision before the general election on 7 May, and rates have been on hold for the entire parliament. The last time interest rates were on hold for a longer stretch was between 1940 and 1951.

- Before that at 9.30am the Office for National Statistics will publish the latest UK trade figures for February, revealing whether or not the government made any progress on its export drive during the month.

- IMF boss Christine Lagarde will give a speech in Washington at 10.30am (15.30 UK time) on the state of the economy, the challenges, and the risks in a pre-IMF/World Bank spring meetings address.

- In the US, the latest weekly jobless claim numbers will give us a snapshot of the labour market, which has disappointed recently.

Greece: deadline day arrives

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

Another day, another crucial moment for Greece.

The government must repay an International Monetary Fund loan of €450m (£326m) or risk a default.

The Greek finance minister Yanis Varoufakis spent last weekend reassuring IMF managing director Christine Lagarde that Greece would honour its debt and meet the deadline.

Repayment seemed all the more likely after Greece raised €1.14bn on Wednesday at an auction of six-month Treasury bills.

But markets will want reassurance that the payment has been made. A failure to repay the debt would be significant, potentially triggering a messy default.

And while a repayment of the loan would trigger instant relief in markets, a high degree of uncertainty about the future of Greece persists.

There is still no agreement between Greece and its creditors over a package of reforms. Agreement is essential if Greece is to secure another tranche of funding under the existing bailout agreement.

Hold on tight.